CPG - Crescent Point Energy: Pessimism Is Fully Priced 12.5% Total Yield

Summary

- Crescent Point Energy production is mostly unhedged for 2023. Let's put a spotlight on this bearish aspect. Let's fully air this out.

- CPG's shareholder returns profile of 12.5% total yield discussed.

- CPG is priced at around 5x this year's free cash flow. How investors should think about this.

Investment Thesis

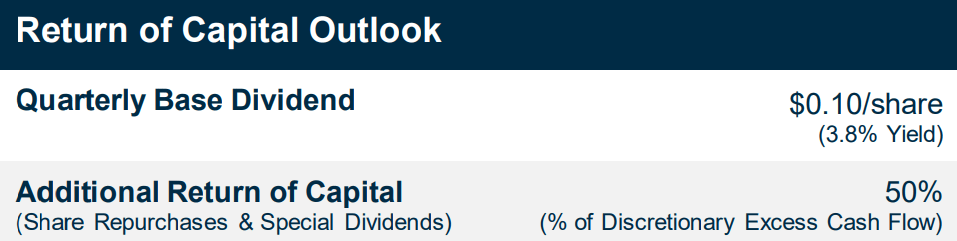

Crescent Point Energy ( CPG ) has a very simple framework to reward its shareholders. CPG continues to increase its base dividend. As it stands, the base dividend reaches a 4.5% yield.

Then, after this base dividend is paid out, CPG is committed to returning 50% of its free cash flow to shareholders via special dividends and repurchases.

Meanwhile, the stock is cheaply valued at 5x this year's free cash flow. So, even though I'm attracted to this stock because of its cheap valuation, what I'm really bullish about here is that shareholders are getting their capital back to the tune of approximately 12.5% total yield.

This is my no-heroics-needed investment case for Crescent Point Energy.

Let's Discuss Some Bad News

Before we go any further, let's face up to the bad news.

{kind=link}

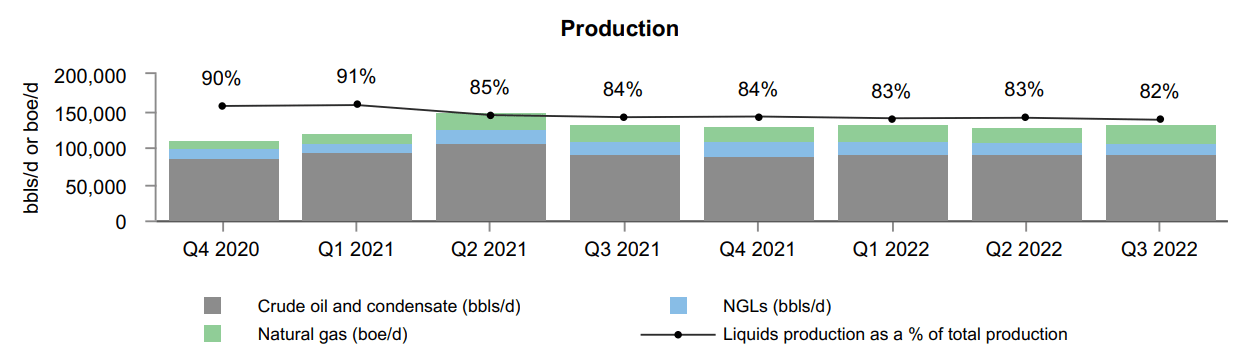

About 80% of CPG's production is from liquids. That's predominantly crude oil and condensates.

And by and large, going into 2023, CPG's production is unhedged.

{kind=link}

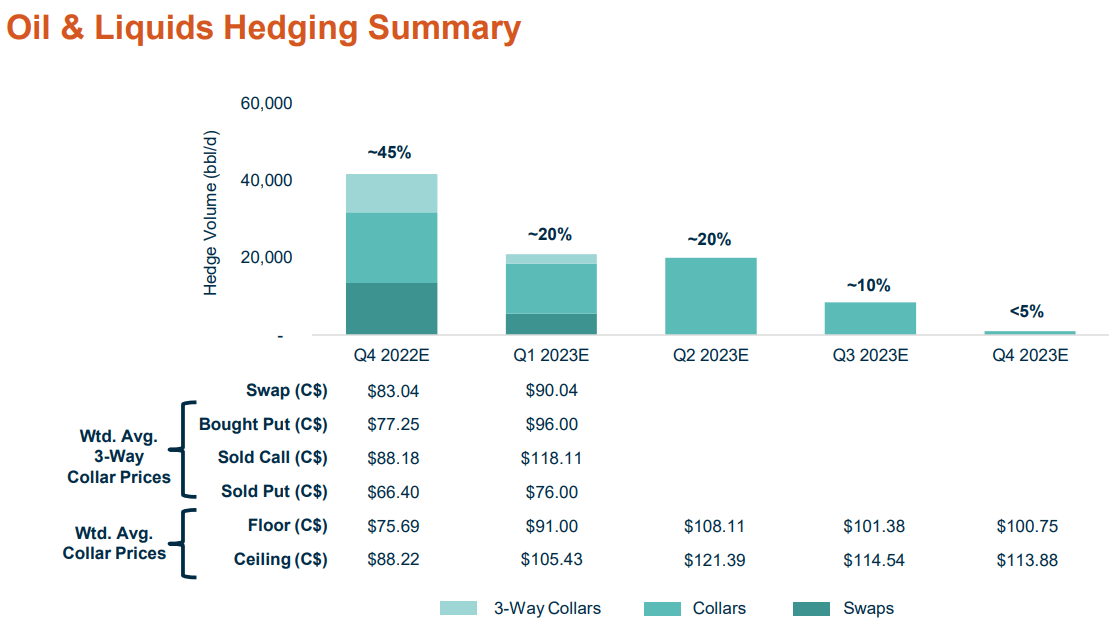

If I were to be finicky, I would note that around 20% of its production for oils and liquids is hedged. And these hedges are at higher prices than the current spot market prices. But again, this means that 80% is unhedged for its oil and liquids production.

Thus, for all intents and purposes, CPG enters 2023 mostly unhedged. And exposed to the vicissitudes of the spot market.

The Core of the Thesis

The bear case is that we are entering a global recession and the demand for oil will be capped in 2023. Indeed, it's worthwhile remarking that right now, oil prices are significantly lower than since the Russian invasion took place.

This wasn't supposed to have played out in this manner. Indeed, the expectations throughout 2022 were that oil prices were going to be higher given the recently imposed sanctions on Russian oil.

Nonetheless, instead of focusing on what should have taken place, let's instead put a spotlight on what is now actually happening. To this effect, let's assume that oil prices average $75 WTI.

In fact, rather than working off hopeful scenarios where China's reopening leads to oil demand increasing, or OPEC's production cuts providing support for oil prices. Let's move away from these bullish considerations. Let's instead focus on what CPG shareholders are likely to get in 2023.

Shareholder Returns Profile, +12.5% Combined Yield

{kind=link}

The CPG December presentation reminds investors that 50% of its discretionary excess cash flows will be returning to shareholders.

Recall, this discretionary excess cash flow is free cash flow after CPG's base dividend payout.

After CPG's 25% increase in its base dividend to CAD$0.40, the base dividend alone is paying out 4.5% yield.

And then, on top of that, CPG is committing itself to return 50% of its remaining free cash flow.

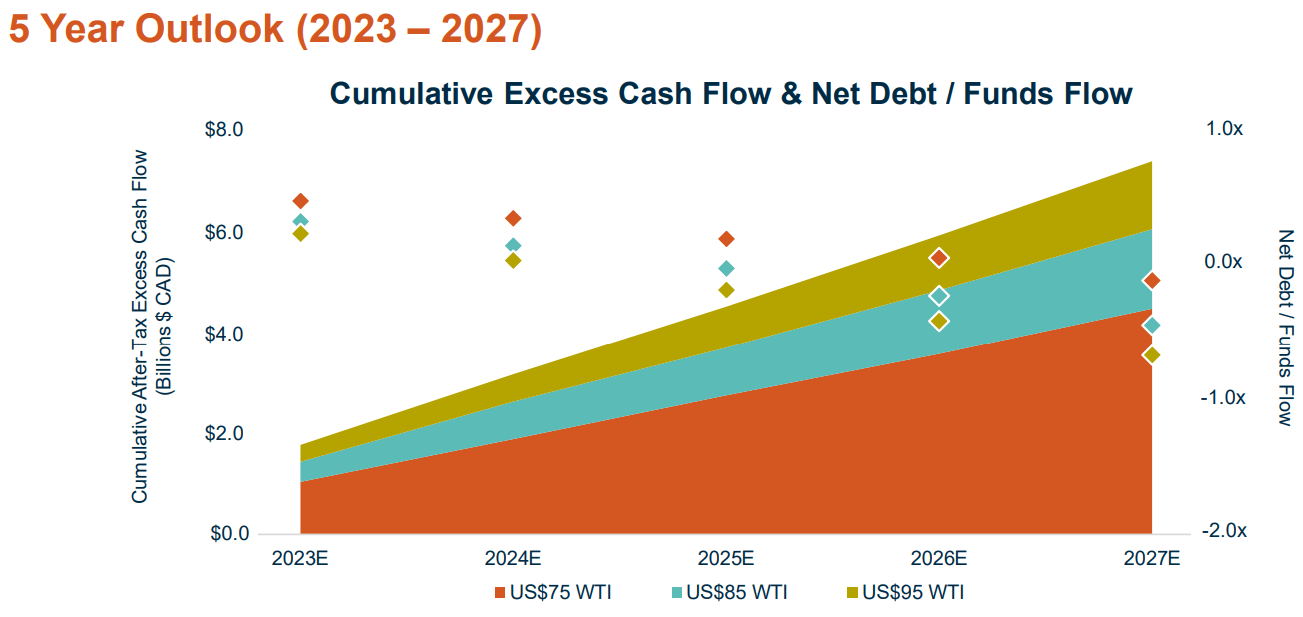

If we assume that WTI stays around $75 in 2023, we are looking at around CAD$1 billion of free cash flow before the base dividend payout.

So, this means we are looking at least CAD$400 million to be paid out via its 50% return on capital program. That means approximately 8% is to be paid out via share repurchases and special dividends.

Accordingly, when all is said and done, investors considering this stock right now are likely to get a 12.5% total yield. Without any heroics.

CPG Stock Valuation -- 5x Free Cash Flow

{kind=link}

I'm very bullish on energy. Yet, I realize that the market is jittery. Understandably. We have been led to believe that ''nobody'' should be a buy-and-hold investor of oil stock. We've been led to believe that oil stocks are not the place to hide as we are about to face a global recession.

And precisely because of this dictum, so many investors have eschewed being long-term holders of energy stocks. Particularly, you'll find, small-cap energy stocks. Stocks that have a capital return program that mostly favors repurchases over dividends. Why is this the case?

Because investors have learned the hard way that in most cases, management has been poor fiduciaries of excess capital. Buying back shares at the highs, and fully hitting the breaks on buybacks when stocks trade at the lows.

Put simply, investors don't believe in this sector. They don't believe in management's capital allocation strategy. And in consequence, that's why CPG is priced at around 5x free cash flow.

The Bottom Line

I've layout a no-nonsense investment thesis of what's at play here. I explained that irrespective of all the bullish talk about oil prices should be heading, I've instead put my argument on what WTI prices actually are. Simply put, I've used $75 WTI as my base case.

And at this price, I lay out that CPG's shareholders are likely to get around 12.5% total yield. With this sort of capital return program, investors are rewarded for sticking around.

For further details see:

Crescent Point Energy: Pessimism Is Fully Priced, 12.5% Total Yield