CPG - Crescent Point Energy: Their Shares Becoming Much Rarer

2023-03-07 14:54:44 ET

Summary

- Crescent Point Energy benefited immensely during 2022 thanks to the booming oil and gas prices.

- This saw them deleverage significantly and also start directing more cash toward shareholder returns.

- When looking ahead into the medium term, their share buybacks look set to run rampant and thus remove upwards of 40%+ of their outstanding shares.

- Colorfully speaking, this means their shares could get rarer and therefore foretell a higher share price given the supply-to-demand change.

- This also boosts their dividend prospects as well as limits downside risk and thus, I believe that maintaining my buy rating is appropriate.

Introduction

When last reviewing Crescent Point Energy (CPG) back in late 2022, at the time they were seemingly on autopilot in 2023 but excitingly as my previous article highlighted, I could see big things possibly coming in 2024. Since the market seemingly continues ignoring their desirable value, this time around we cast a lens further afield into the next five years to assess their medium-term outlook with their shares becoming much rarer, speaking colorfully as their share buybacks run rampant due to their low valuation.

Coverage Summary & Ratings

Since many readers are likely short on time, the table below provides a brief summary and ratings for the primary criteria assessed. If interested, this Google Document provides information regarding my rating system and importantly, links to my library of equivalent analyses that share a comparable approach to enhance cross-investment comparability.

Author

Detailed Analysis

{kind=link}

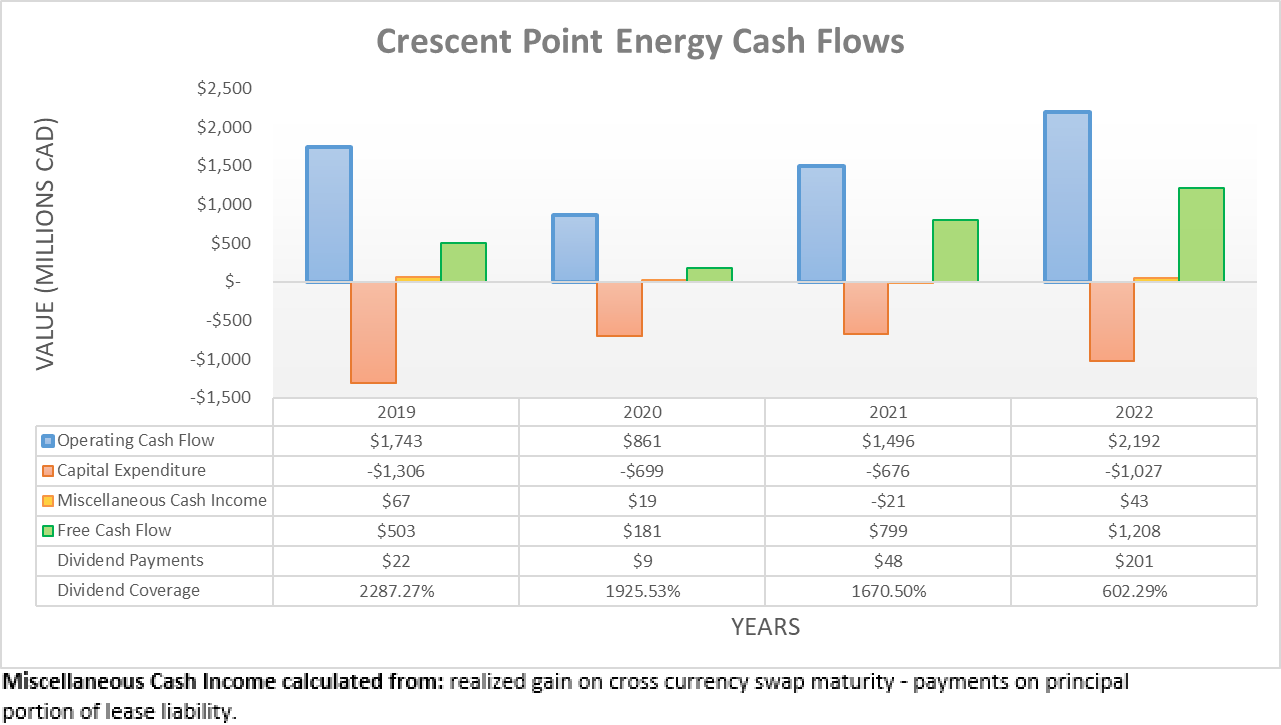

Following their very impressive cash flow performance during the first nine months of 2022, the fourth quarter saw it ease on the back of lower oil and gas prices but nevertheless, it stayed strong. As a result, their full-year operating cash flow landed at C$2.192b and thus a massive increase of circa 47% year-on-year versus their previous result of C$1.496b during 2021. Even more importantly, their free cash flow during 2022 landed at C$1.208b, which provided ample scope to deleverage and start directing more cash towards shareholder returns, as my earlier article discussed.

{kind=link}

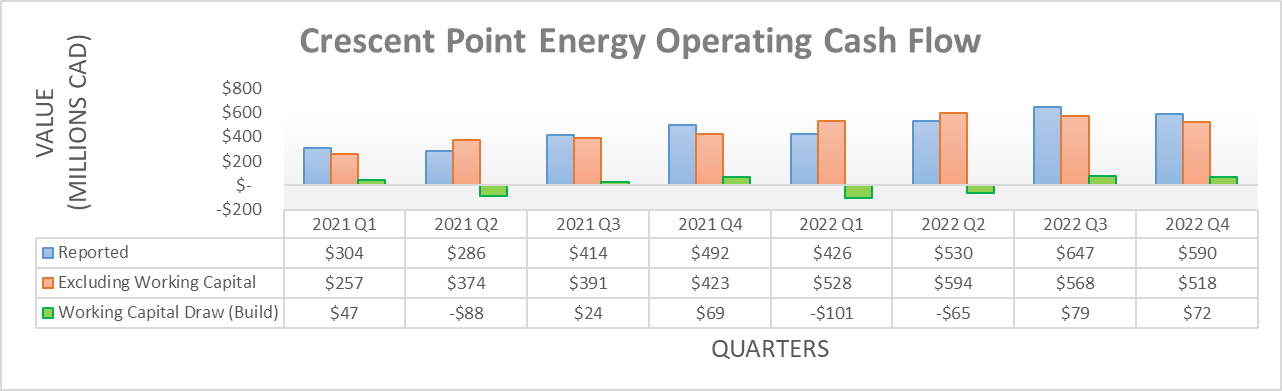

When zooming into their quarterly operating cash flow, the fourth quarter of 2022 saw a reported result of C$590m, although it was helped by a C$72m working capital draw that leaves their underlying result at C$518m. Despite being their lowest quarterly result during 2022, this is largely due to tough competition from their other results with it easily beating their highest underlying result of C$423m during 2021. That said, the outlook for 2023 and beyond is far more important for shareholders and thankfully, even if oil prices remain under pressure, they can still generate ample free cash flow, as per the commentary from management included below.

"As we look to 2023, we are on track to generate $1 billion of excess cash flow at $75 WTI pricing, allowing us to return over $600 million of capital directly to our shareholders, while also delivering per share growth and further net debt reductions."

-Crescent Point Energy Q4 2022 Conference Call.

The inherent volatility of oil and gas prices makes giving exact guidance impossible, although even if Western Texas Intermediate oil prices only average circa $75 per barrel, management still forecasts C$1b of excess cash flow. When management speaks of their "excess cash flow", it is effectively another word for their free cash flow, similar to how their "funds flow" is essentially their operating cash flow.

Obviously, no one can see the future but in my opinion, assuming that Western Texas Intermediate oil prices average circa $75 per barrel going forwards into 2023 and beyond seems to be a reasonable middle-of-the-road basis, especially with prices currently around $80 per barrel. The economic outlook in the short-term is not particularly strong in the Western world but on the other hand, China is reopening from their Covid-19 lockdowns, whilst OPEC continues to manage their supply and sanctions on Russia cap the potential of one of the largest producers in the world. Not to mention that closer to home, the United States is planning to begin refilling their strategic petroleum reserve after selling down massive quantities in 2022.

After wrapping these headwinds and tailwinds together, it is not difficult to see their forecast for circa C$1b of free cash flow during 2023 coming to fruition of which at least C$600m they intend to send towards the pockets of shareholders. Even if they opt not to push past this point, C$600m of shareholder returns still equates to a very high circa 11% yield on their current market capitalization of approximately C$5.5b at the present CAD to USD exchange rate of $0.73. Whilst they have their base quarterly dividends of C$0.10 per share and special dividends that vary quarter-to-quarter, it seems the majority is coming back via share buybacks, as per the commentary from management included below.

"We continue to focus on share repurchases as our primary tool within this framework, given our current valuation."

-Crescent Point Energy Q4 2022 Conference Call (previously linked) .

Normally, I am not always a fan of this approach but in light of the market seemingly ignoring the desirable value offered by their ample free cash flow and thus, the resulting double-digit shareholder yield, I am more open to share buybacks than previously. Whilst already positive, the final piece of the puzzle is their medium-term free cash flow guidance, as per the commentary from management included below.

"Under our current 5-year plan alone, we expect to generate over $4.2 billion of cumulative after-tax excess cash flow at $75 per barrel pricing."

-Crescent Point Energy Q4 2022 Conference Call (previously linked) .

Barring a sudden and prolonged oil price crash, they stand to generate C$4.2b of free cash flow across a five-year period of time. Whilst their future rate of deleveraging beyond 2023 remains uncertain, at the moment their net debt stands at circa C$1.5b as subsequently discussed and thus even if they opt to repay every last cent in the coming years, this still leaves another C$2.7b of free cash flow remaining for shareholders that amounts to roughly half of their current market capitalization. That said, this is merely a baseline because they realistically may not opt to repay the entirety of their net debt and therefore, this could climb higher to 60% or even 70%.

This is a truly impressive outlook that carries ramifications not only for their shareholder returns but also for their overall share price. Since they are presently intending to direct the majority of their free cash flow towards share buybacks instead of dividends, it means the next few years should see their outstanding share count plunge rapidly as their buybacks run rampant. It is quite possible to see a reduction in the magnitude of 30% to 40%, maybe even more and thus to put this colorfully, it could be said there are going to become much rarer, which in turn foretells desirable returns for investors who buy now.

Whilst yes, their shares will never be as rare as say gold per se, this is more so a fun way to think about the simple law of supply and demand that exists for every asset, both tangible or intangible. If their outstanding share count drops massively across the next five years as I expect, their supply will have fallen off a cliff, whereas I personally see no reason to expect their demand will dissipate significantly in the foreseeable future. Therefore as evident anywhere in the economy, a higher share price is almost certain to follow this supply-to-demand change, at least to the same 30% to 40%+ reduction their outstanding share count sees.

Apart from making a higher share price very likely in the coming years, these share buybacks also foretell much higher special dividends as their outstanding share count shrinks lower. In turn, this should also boost their dividend yield and thus appeal to income investors, which means they could realistically command a higher valuation in the market, thereby further enhancing their upside potential. Finally, this could also simultaneously decrease the downside risk of their shares by potentially removing such a large percentage of their float from the market.

{kind=link}

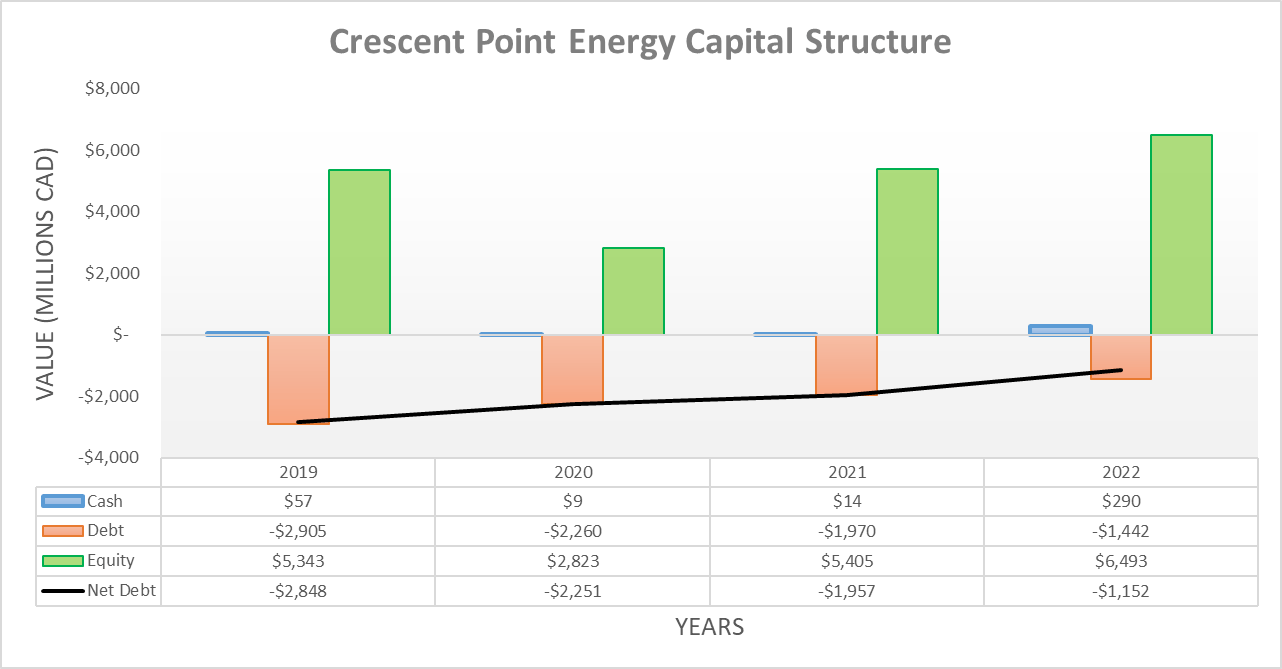

Thanks to their strong cash flow performance during the fourth quarter of 2022, their net debt once again continued to drop lower to C$1.152b versus its previous level of C$1.231b following the third quarter. Going forwards into 2023, their net debt will temporarily spike higher to circa C$1.5b when their results for the first quarter land given their recent acquisition, as per the commentary from management included below.

"Subsequent to the year-end, we successfully closed the acquisition of certain Kaybob Duvernay lands and associated production for cash consideration of $370 million. Our net debt as of closing of this deal on January 11, 2023, was approximately $1.5 billion."

"Based on our guidance for the year, we expect our net debt at year-end '23 to be less than $1.1 billion at $75 WTI or 0.5 times net debt to adjusted funds flow."

-Crescent Point Energy Q4 2022 Conference Call (previously linked) .

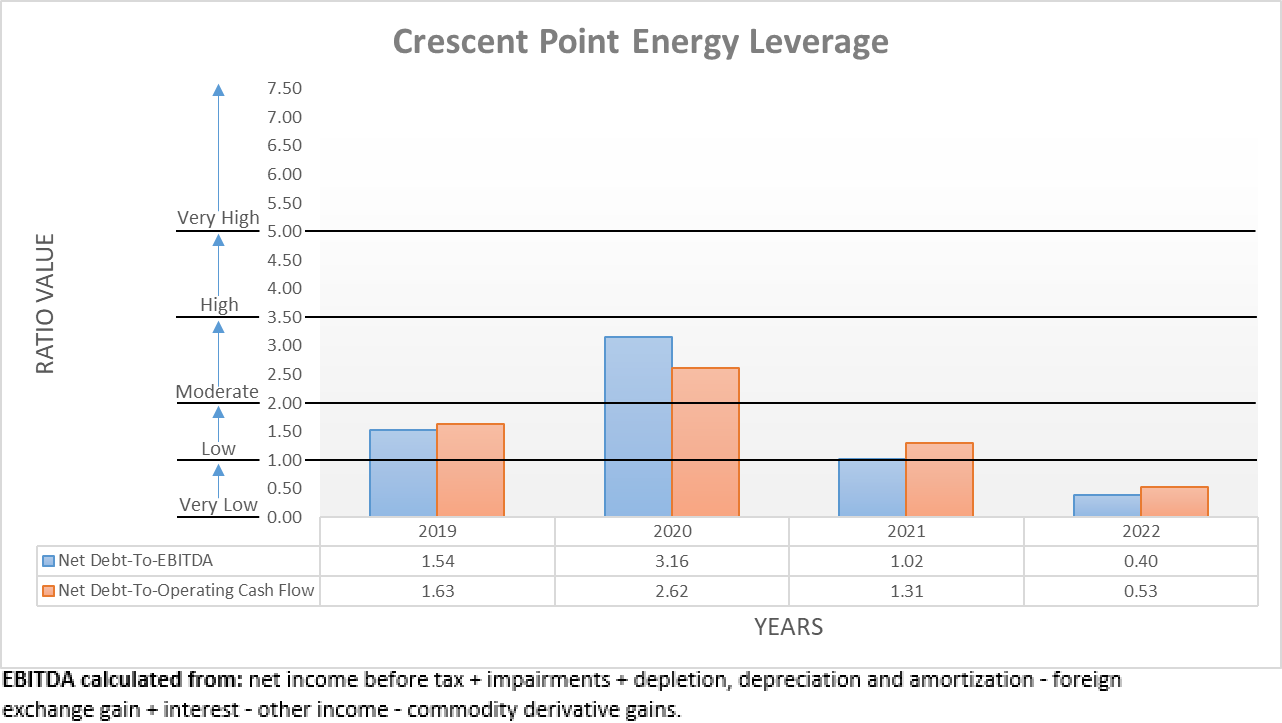

Due to their aforementioned ability to generate ample free cash flow even without booming oil and gas prices, they forecast repaying this additional debt before 2023 ends. As a result, this does not materially alter the aforementioned equation for their shareholder returns going forwards. In light of this outlook and accompanying modest change since conducting the previous analysis, it would be redundant to reassess their leverage, debt serviceability or liquidity in detail, especially as their medium-term outlook was the primary focus of this follow-up analysis.

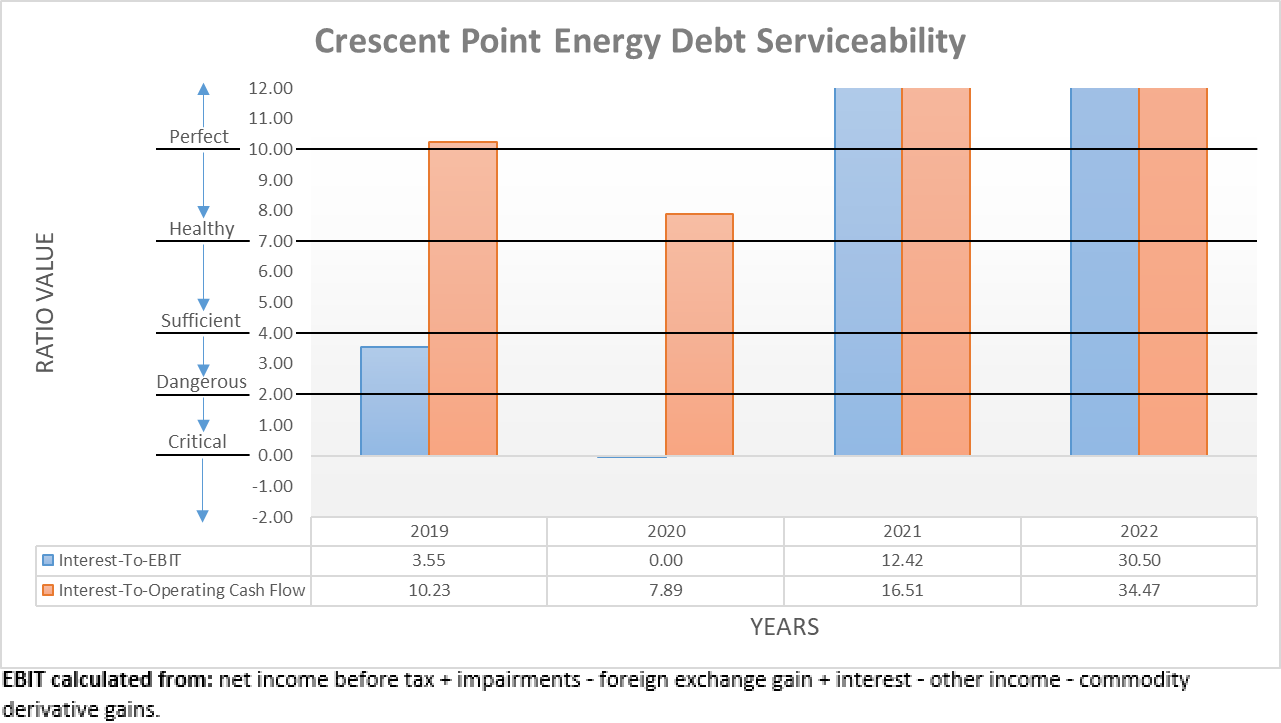

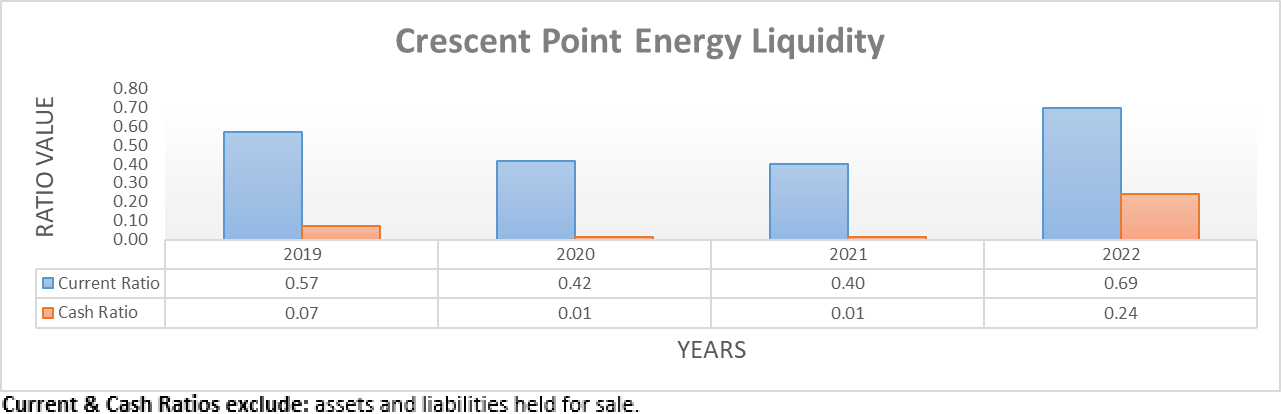

The three relevant graphs are still included below to provide context for any new readers, which to zero surprise sees their leverage down in the very low territory with their net debt-to-EBITDA at 0.40 and net debt-to-operating cash flow at 0.53, thereby sitting well beneath the applicable threshold of 1.00. Similarly, their debt serviceability remains perfect with interest coverage of 30.50 and 34.47 when compared against their EBIT and operating cash flow, respectively. Thanks to their strong cash flow performance, their liquidity is now strong, not necessarily because of their current ratio of 0.69 but rather, their far more impressive cash ratio of 0.24. If interested in further details regarding these topics, please refer to my previously linked article.

{kind=link}

{kind=link}

{kind=link}

Conclusion

Unless oil prices plunge through the floor and stay there for a prolonged time, it looks as though shares of Crescent Point Energy are going to become much rarer, as their share buybacks run rampant and thus send their outstanding share count plunging by upwards of 40%+ in the next five years. When combined with the accompanying prospects for much higher dividends, there is only so long the market is likely to continue ignoring their desirable value and thus as a result, their share price is very likely to trend higher in the coming years, which means that I believe maintaining my buy rating is appropriate.

Notes: Unless specified otherwise, all figures in this article were taken from Crescent Point Energy's SEC Filings , all calculated figures were performed by the author.

For further details see:

Crescent Point Energy: Their Shares Becoming Much Rarer