CPG - Crescent Point: Running After That Untamed Ornithoid

2023-11-07 12:45:55 ET

Summary

- Crescent Point Energy has announced its acquisition of Hammerhead Energy for approximately $2.55 billion.

- The purchase will enhance Crescent Point's drilling inventory profile.

- We tell you why we think the Data suggests that we look elsewhere for returns.

Note: All amounts are in Canadian Dollars unless noted otherwise.

Our last public coverage of Crescent Point Energy Corp. ( CPG ) was some time back and it got a rare "strong buy" backing from us. This was despite an acquisition that we were not extremely thrilled about.

So we understand the skepticism towards the purchase. We still think it was not bad, and you have to give management some runway here, considering their execution over the last three years in general and their Kaybob results in particular. If oil prices land up remaining anywhere over USD60 over the next decade, and that is certainly the way we see it, you will be glad they made this purchase.

Source: Acquisition And Impact On Future Returns

CPG was a positive delight for bankers and it did not stop there. It bought Spartan Delta's Montney assets for $1.7 billion three months later . It then sold North Dakota assets at a very poor metric for just $675 million , five months after that. Despite these transactions, the stock did OK, and kept with the broader S&P 500, without adding any mentions of "AI." Of course, all of that was just until this morning.

Seeking Alpha

Crescent Point Energy Q3 2023 Results

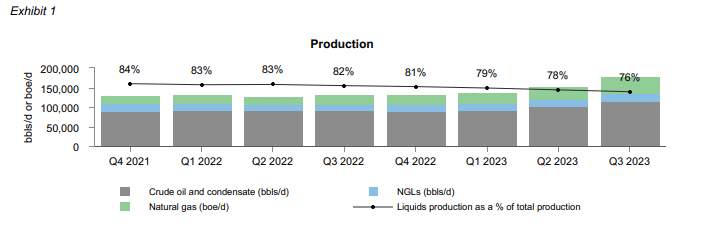

Before we get on the transaction du jour, we will briefly touch upon the released Q3-2023 results from CPG. The results were in line with estimates and production came in at about 181,000 barrels per day. Adjusted funds from operations came in at $1.28 and the capex conducted was at $315 million. CPG's shift away from liquids was apparent once more and the transactions earlier in the year saw the company's liquid profile drop from 81% in Q4-2022 to 76% in Q3-2023.

{kind=link}

If you go back even further, you can see that CPG was once a liquids powerhouse. Note the 91% in Q3-2020.

CPG Q2-2022 Results

This change is of course reducing per barrel returns and CPG is unlikely to command a premium valuation in its peer group. Of course, the flip side is that CPG is now far more levered to natural gas prices, and should we see a spike, we will get the extra juice to the bottom line.

CPG continued plowing back cash in buybacks by buying 11.4 million shares at an average of $10.96. It also did yet another extra special dividend for $0.02.

Crescent Point To Acquire Hammerhead Energy

It appears that three major capital transactions in one calendar year were not enough for CPG, and they went ahead and decided to close the year strong on that front.

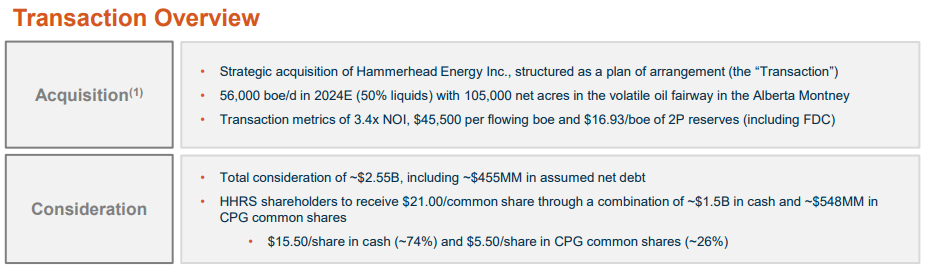

CPG is pleased to announce that it has entered into an arrangement agreement (the "Agreement") to acquire Hammerhead Energy Inc. ( HHRS ) ("Hammerhead"), an oil and liquids-rich Alberta Montney producer, for a total consideration of approximately $2.55 billion, including approximately $455 million in assumed net debt, consisting of cash and common shares of the Company (the "Transaction").

"This strategic consolidation is an integral part of our overall portfolio transformation," said Craig Bryksa, President and CEO of Crescent Point. "The acquired assets, which are situated in the volatile oil window in the Alberta Montney and adjacent to our existing lands, provide significant value with premium drilling inventory, infrastructure ownership and scalable market access. This transaction is expected to be immediately accretive to our per share metrics and to enhance our return of capital profile for shareholders.

Source: Seeking Alpha

Makes sense, right? CPG kept claiming they had the best assets in 2022 and then did four major transactions to basically change the whole profile of what they had. But let's look at the transaction objectively to see what we can glean. The purchase price is not the worst on a 2P basis. But we have to keep in mind that this is just 50% liquids and it will push CPG's falling liquids metric further down.

CPG November 2023 Presentation

{kind=link}

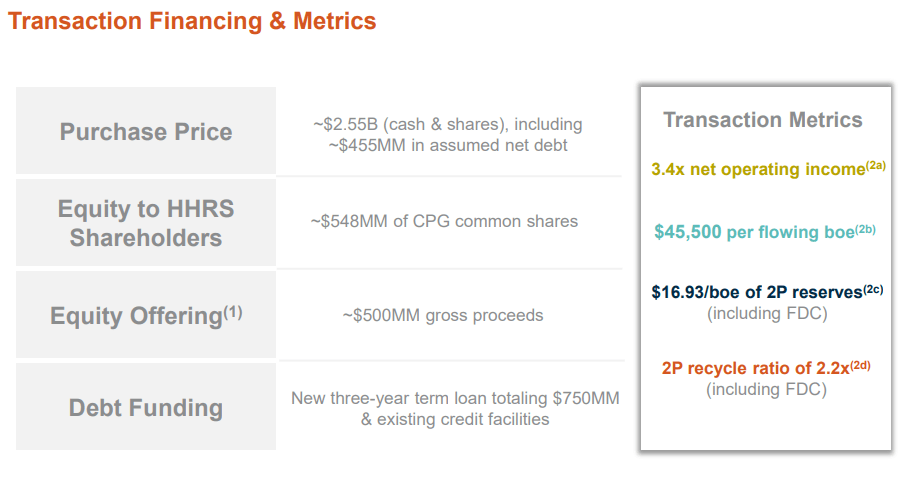

The size also is quite massive. Before the news, CPG sported a $5.741 billion market capitalization. This transaction is huge in relation to that.

Debt metrics will go up, initially at least. Roughly about $1.05 billion of that $2.55 billion total enterprise value of the purchase will be financed via equity exchange and the large secondary offering announced. The rest will be debt.

CPG November 2023 Presentation

{kind=link}

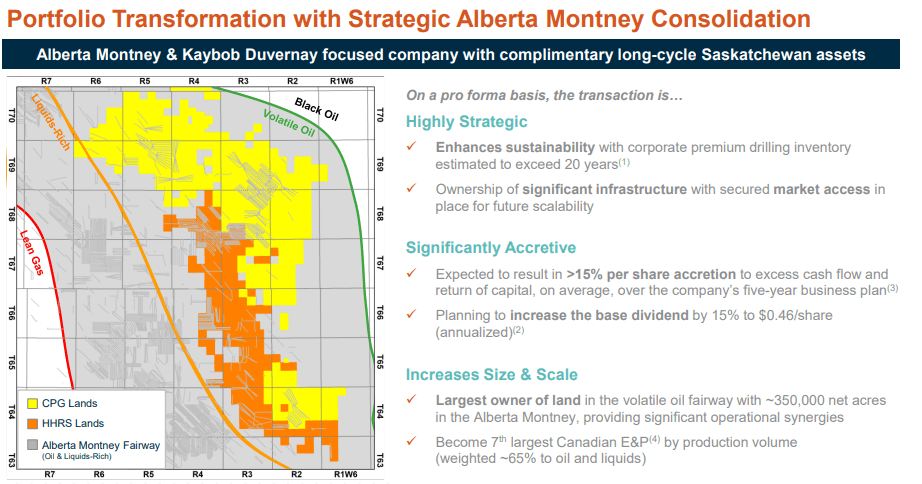

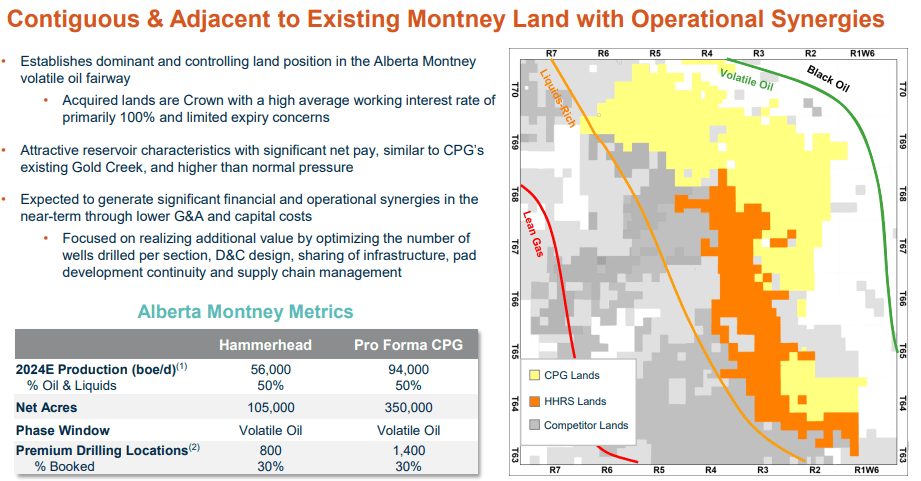

So your debt to EBITDA will look pretty bad (at least relative to rest of 2023) on close if you use the very first quarter. But this is a very nice fit for CPG on a location basis. Just look at that location layout.

CPG November 2023 Presentation

{kind=link}

People use the "hand in glove" phrase quite often, but here it may actually apply. It also might be one of those rare occasions that the constantly promised synergies actually materialize.

CPG November 2023 Presentation

{kind=link}

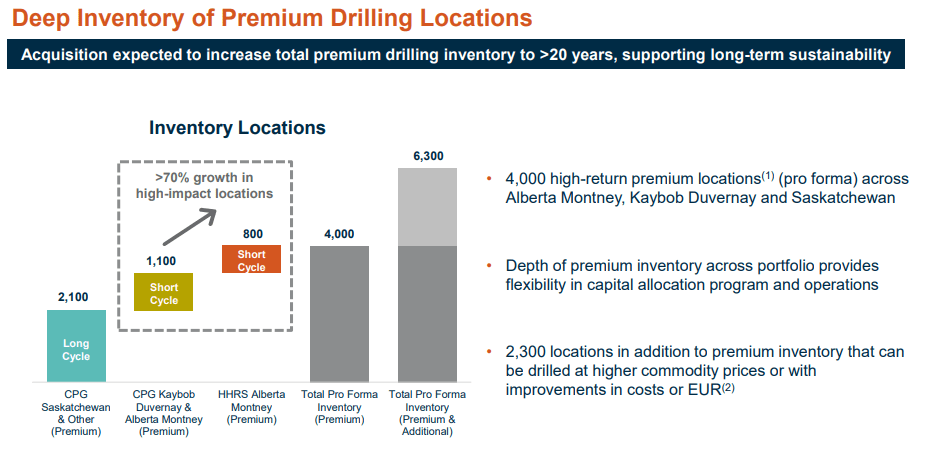

This also adds a lot of inventory to the CPG arsenal, but one has to wonder just exactly how much inventory the company needs to accumulate in Canada. The chart shows the evolution of the drilling locations in Canada along with the transactions to date.

CPG November 2023 Presentation

{kind=link}

Outlook

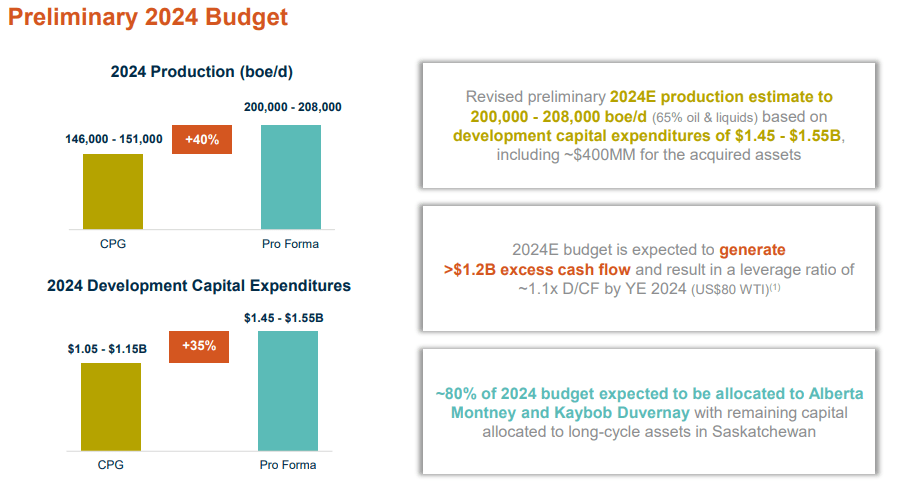

If you're interested in a large production base and a larger company, well, you will get it. CPG will be comfortably over the 200,000 barrels per day mark, assuming the transaction closes in December 2023 as expected.

CPG November 2023 Presentation

{kind=link}

But the key facet of this transaction is why HHRS is selling. This little-known oil company is controlled by Riverstone. Riverstone and its affiliates owned 86% of the total shares. From HHRS's perspective, this is likely a liquidity move. Any time a company that has such a small public float sells out, you have to consider that as one of the primary motivating factors. One additional factor here is that while CPG stressed the great EBITDA and NOI metrics they did not stress on the most important metric. Free cash flow. Possibly because HHRS has none currently. Capex exceeded net cash flow from operations in 2023.

CPG November 2023 Presentation

{kind=link}

This is not remotely a one-off situation either. Looking at 2024 and 2025 estimates you see that current strip prices, HHRS would generate about $450-$500 million of operating cash flow while conducting $400 million of capex. The company will be spending $500 in 2023 as well and this was a reduction from its earlier estimates of $527 million. So there's a story here of getting capital efficiencies down the line, but at present this remains a very challenging case for free cash flow, unless oil and natural gas prices increase significantly. We believe this is the Achilles heel of this transaction, and while the premium may not seem like much, it's really going to detract from CPG's performance.

Verdict

Our primary position here was to take advantage of the very large implied volatility in the stock and sell a large premium. We did this in October 2022 and used the January 2024 covered calls.

Author's App

That return profile is based on the NYSE trading stock and is in US dollars. The covered call has substantially outperformed the buy and hold strategy with the sold calls decaying from $2.10 to $0.35. At present, we are far less enchanted with the CPG strategy. Free cash flow yields are going to drop like a stone here and if we see $65 oil in a recession, CPG will really regret this transaction. The very weak Canadian dollar is partially offset here for the company (as in oil in Canadian dollars has stayed really firm). So we cannot get too negative, despite this dubious move. We're moving to a Hold rating and are still weighing the best roll for the existing calls.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

For further details see:

Crescent Point: Running After That Untamed Ornithoid