HLBZF - CRH: Strong Results Can Continue To Drive Price Up

Summary

- The Irish building materials provider CRH plc saw a 9% rise in price after it released its 2022 results today.

- It continues to grow its sales and EBITDA, and its EPS has exceeded analysts' expectations, too. With a relatively reasonable P/E, CRH plc continues to look like a good buy.

- A slowdown in U.S. construction and elevated inflation might impact CRH plc, but its long-term performance is still notable.

The Irish building materials company CRH plc (NYSE: CRH ) is up 9% as I write today after it released its full-year results , and also said that it is moving its primary listing to the U.S. The pickup in price is not new. It started in November last year, and CRH plc has made pretty much continuous gains since. It is now up by 16.6% year-on-year (YoY) and almost 26% up year-to-date [YTD].

This was to be expected. CRH plc has solid financials and is a big building materials supplier. There was little doubt that it would start rising again, which is why I put a Buy rating on it first in November last year. It is up over 28% since then. I then reiterated the rating again in February this year, and it has gained 10% since. Its results look good, to be sure (see chart below), which is encouraging. But how much more CRH plc's price can rise now depends on the fine print of the results as well as what the valuations indicate.

{kind=link}

Sustained growth, EBITDA surprise

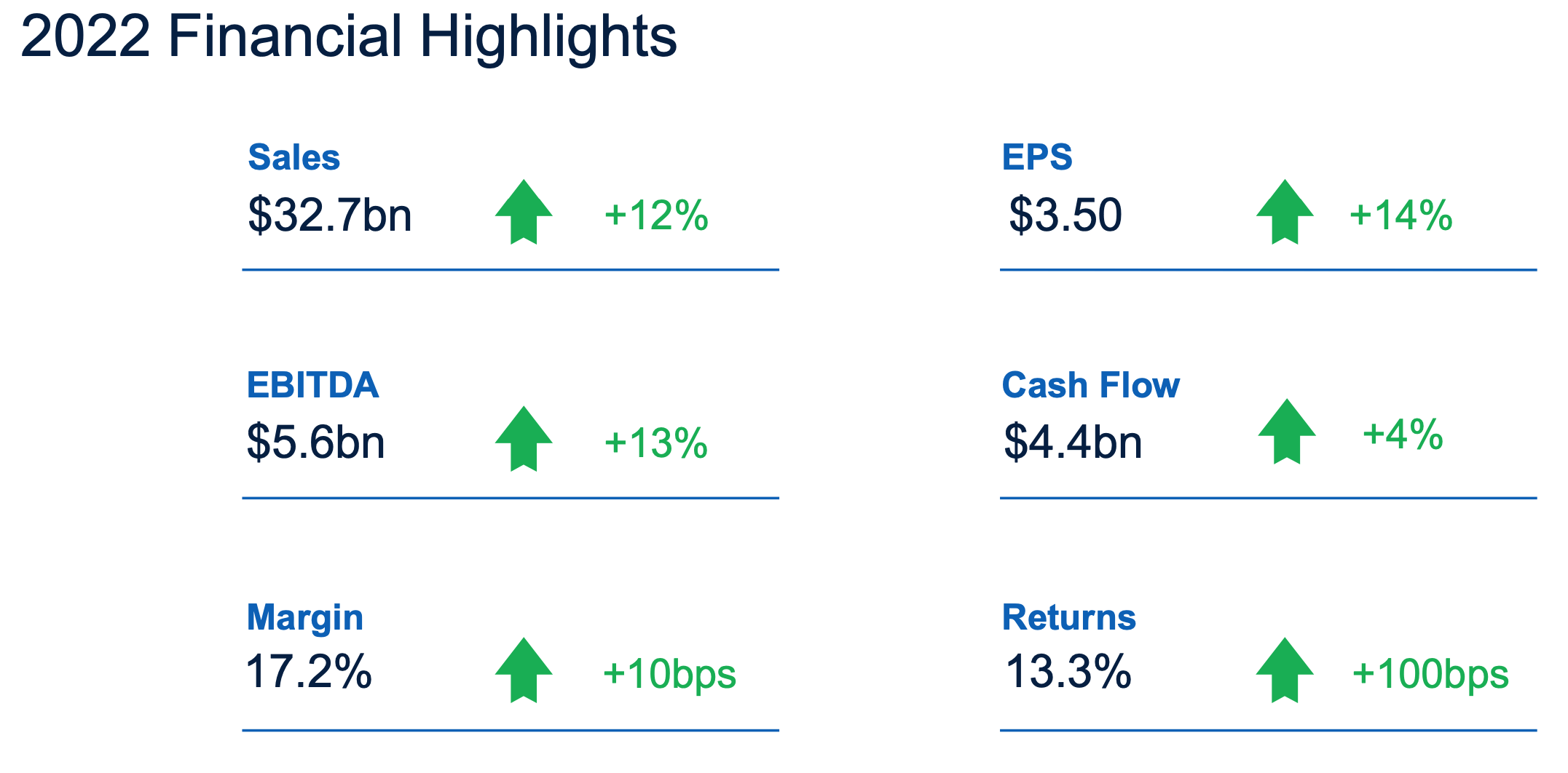

First, the results. The company’s revenues increased by 12% YoY in 2022, this is the same as the 12% seen last year. It is slightly slower than the 13% rise seen for the first nine months of the year, though, indicating softening in the final quarter, but on the whole, growth is sustained.

CRH's EBITDA, too, has seen some slowing down, with a growth of 13% for the year, compared to 16% last year and 14% for the first nine months of 2022. This was expected, though, as input costs increased. But here is the real rub. The EBITDA levels at USD $5.6 billion, have slightly exceeded the company’s guidance of USD 5.5 billion . Its EBITDA margin is also up 10 basis points to 17.2%, which is notable at a time of high inflation.

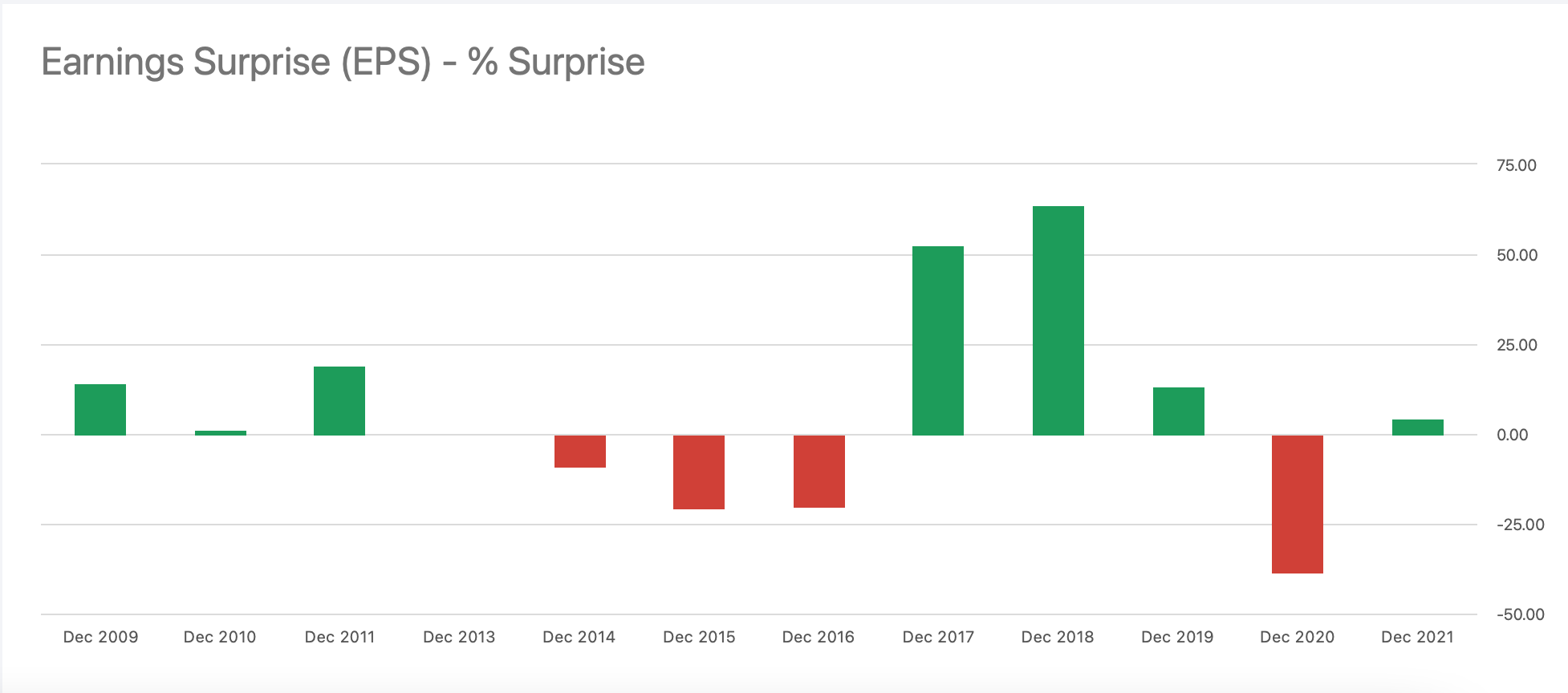

Further, at USD $3.5, the earnings per share [EPS] are also ahead of analysts’ expectations at USD $3.4, making it the fifth year in the last six years when CRH has managed to report an upside surprise on EPS estimates (see chart below). The one year when it did not was 2020, which, of course, was because of COVID-19-related challenges.

{kind=link}

Positive outlook

The company is also positive about growth this year, on a mix of increased demand and better pricing. It expects infrastructure demand in both the U.S. as well as Central and Eastern Europe to be driven by public funding. In the U.S. in particular, it should benefit from the Inflation Reduction Act [IRA], which aims to ramp up the green economy.

The U.S. market is important for CRH, which accounts for 63% of the company’s revenues. In fact, in its outlook, CRH plc mentions in that context “The non-residential sector is supported by government funding initiatives in clean energy and the onshoring of critical manufacturing.” Further, as Ashtead, CRH’s LSE-listed FTSE 100 ( UKX ) peer with significant interests in the U.S. construction market, points out , besides IRA, the Infrastructure and CHIPS Acts should bolster the construction industry, too.

CRH also expects repair, maintenance and improvement activity, as also stable infrastructure demand, to support its business in Europe as such. Better pricing is expected to be another catalyst for growth in 2023. The U.S. residential segment is the only place where it expects weakness because of rising interest rates.

P/E suggests more upside

This sounds quite positive, mostly. But CRH plc's price is also trading close to all-time highs now, so what does it mean for its valuation? My calculations indicate a trailing twelve months [TTM] GAAP price-to-earnings (P/E) ratio of 14.8x. Now, this is an increase from the 12.8x when I wrote about it last in February, and definitely higher than the 11.2x when I covered it in November 2022.

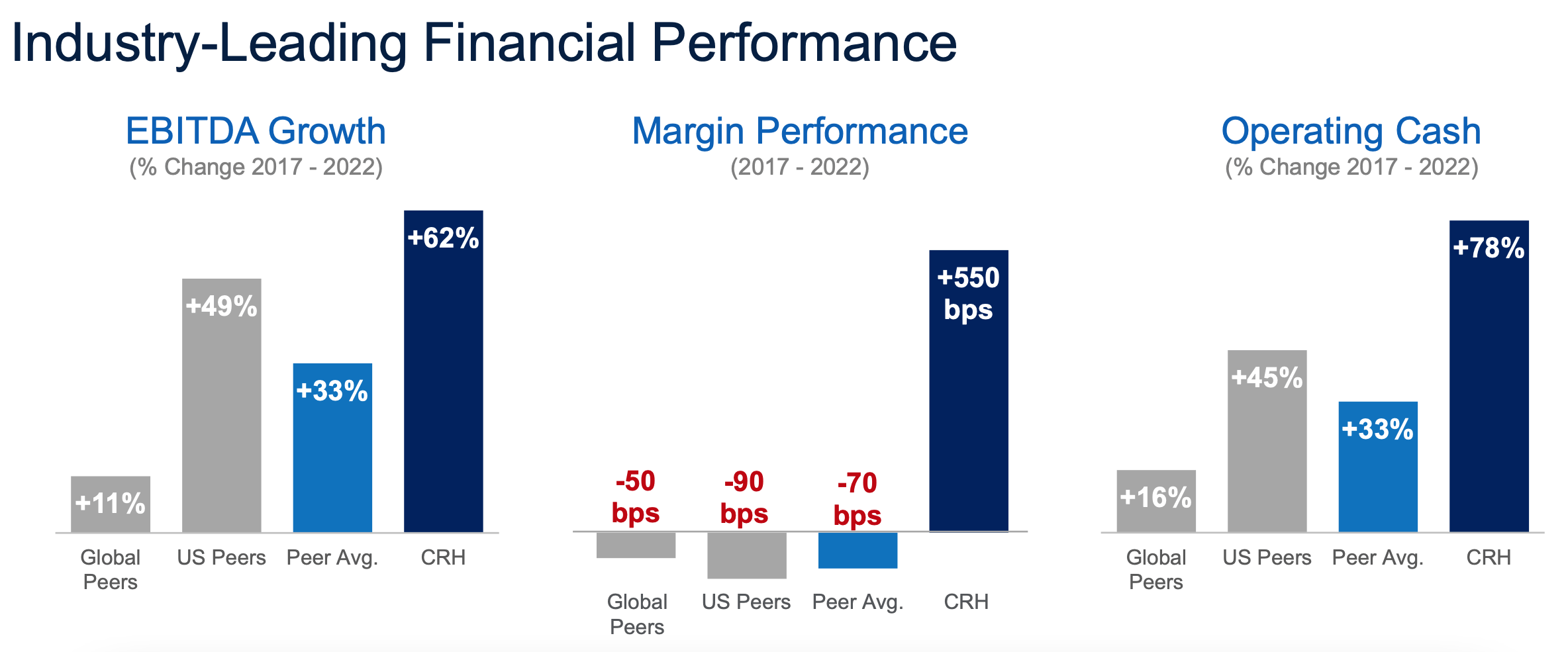

At the same time, it remains firmly below its median P/E of 21.5x over the past ten years. It is also lower compared to U.S. peers like Vulcan Materials ( VMC ), which is at 40.4x and Martin Marietta Materials ( MLM ) at 26.1x. It is somewhat overvalued compared to global peers like Holcim ( HCMLY ) at 10.4x, Heidelberg Cement ( HDELY ) at 7.7x and Cemex ( CX ) at 14.3x. On the whole, though, it appears that there is likely to be more upside to CRH. This is particularly as its performance is superior in some respects to peers (see chart below).

{kind=link}

The risks

Despite all that it has going for it, the U.S. construction sector is challenged right now. It is the biggest drag on the economy’s growth, and that could tell on CRH’s growth in 2023. Already, the numbers indicate some softening in sales growth even as the full-year numbers look alright. It is a relief that inflation has started coming off, but it will be a while before it comes back to the Fed’s target rate of 2%. The company is confident that it can increase prices, but how much by remains to be seen.

What next?

All in all, though, CRH plc has more going for it than not. Its latest results continue to show sustained growth. Its EBITDA has not just grown, it is ahead of expectations, as is its EPS. Even with an increase in price over the past few months, its P/E ratio does not look particularly inflated either. There can be short-term concerns regarding the slowdown in the U.S., as well as in Europe, but the company believes it is well placed at this time. In fact, the public spending impetus can support the construction sector at this time.

I would look out for its upcoming results to see how it is faring. But from an investing perspective, CRH plc still remains a Buy for me. It has yielded a 134% price return over the past 10 years, and there is little to suggest that it will stop performing now.

For further details see:

CRH: Strong Results Can Continue To Drive Price Up