HLBZF - CRH: Undervalued And Catalyst Ahead

2023-03-09 15:19:01 ET

Summary

- CRH is underfollowed, overlooked, and undervalued.

- Large infrastructure spending programs in the USA and Europe set the business up for a decade of solid earnings.

- The company has decided to migrate its primary listing from the UK to the USA.

- This serves as a massive catalyst to a rerating as CRH trades at a substantial discount to US peers.

- Seeking Alpha Quant ratings vindicate my view with a STRONG BUY rating.

Who are CRH plc and what do they do?

CRH plc (CRH) is a leading provider of building materials solutions across the globe. They are the invisible hand that touches everything we do by supplying Aggregates, Cement, Lime, Ready-mix Concrete, Asphalt, Paving and construction services to govts, large corporations and retail customers all over the world.

They consider themselves "the essential partner for road and critical utility infrastructure, commercial building projects and outdoor living solutions." With a market cap of $38bn they have size and scale to boot, and their reach is vast with 75800 people in twenty-nine countries on the payroll.

In a full turnkey offering, with market leading positions in both the USA and Europe, they can supply all that you need and then build whatever you need from the ground up. They leverage their scale and experience to provide end to end solutions for their customers and with that they benefit from cost control and better procurement which allows them to keep prices in check, margins to expand. A good recipe for growth and cash generation.

Literally anything from the roads, we drive on to the buildings we work, live, and play in. Anything that requires constructing and then subsequent maintenance or refurbishment falls into their wheelhouse.

Effective 1 Jan 2023 the company announced a new organisational structure. Where two distinct offerings are housed.

Material Solutions: 72% of Sales / 71% EBITDA

This division is split in two, the first known as 'Essential Materials' is a leading provider of essential building materials like cement and aggregates. You can think of it as all the raw materials and products the company uses to undertake 'construction'.

These assets are finite, valuable, and difficult to replace. They hold a leading position in North American regional aggregates reserves and a number 1 position in Europe. This is a high margin business and heavily integrated into the solutions business (which we'll get to next). They sell their product and raw materials into the construction division where it's used for building solutions.

The 'road solutions' business is the second part of this division, it is no1 in sustainable road solutions and can do everything from design, manufacturing, and installation all the way to subsequent maintenance and recycling at the products end of the life. This business is linked to the division above and will source its materials from it.

Building Solutions: 28% of Sales / 29% EBITDA

Again, we have two subdivisions here, the first, 'Building and Infrastructure solutions' is viewed by the company as the leader in the provision of critical utility infrastructure and commercial solutions. It's fully integrated with the essential materials business in that the materials used for construction are sourced directly from it. The road solutions division works closely with this one to build the road infrastructure needed for its projects.

The second part here known as 'outdoor living solutions' focuses beautifying the project landscape. So, if building solutions builds an apartment block, outdoor living will come in and lay down decking and lawn, construct fences etc. Both new and remodeled projects are undertaken. This company is benefiting from structural growth drivers such as migration, lifestyle changes and suburbanisation.

CRH are highly experienced in large scale and complex construction projects and stand to benefit from all the investment that the US, via the Infrastructure Investment and Jobs Act (IIJA) and the Inflation Reduction Act (IRA) and Europe courtesy of the NextGenerationEU recovery funding program put in place.

The Opportunity

Today I'm going to present to you a company that has a massive tailwind going for it, is cheap on a relative and absolute basis and then on top of this has a catalyst to crystalise substantial upside from current prices. Nothing is a slam dunk in investing, but upside here is palpable if you agree with the thesis and have some patience. Let's start with the opportunity.

Why is CRH a good Investment?

I love infrastructure as an investment, real assets have proven to be excellent hedges against inflation. They're tangible, and predictable and whether it's the home you live in, the grocery store you shop in or the data centre housing the cloud infrastructure used to store the crypto you're mining we all need it.

One thing growth and value investors can agree on is that every type of company needs some or other physical home to operate.

CRH builds those for us and as long as populations grow, consumption increases or assets require maintenance and refurbishment CRH will have customers.

The USA is the largest part of the business and accounts for 75% of the companies EBITDA. This is opportune because between IIJA and the IRA, congress invested over $1.25 trillion across transportation, energy, water, and broadband sectors for the next five to 10 years, and it's all starting now. What's important to realise is that this isn't a stimulus boost akin to Quantitative Easing this is a long-term commitment to rebuilding and refurbing American infrastructure. It's not a drop and go approach but a gradual release of funds over several years.

Europe although smaller in its contribution to the group is equally important. It's the most regulated construction market globally with exacting specifications. The region has been forward thinking in sustainability and is driven by innovation. This allows for the 'cross selling' of skills and experience into the larger USA business which has been practically proven by the doubling of profits in its Ash Grove cement business in the USA after acquiring it in 2017. This flow of information has become useful and perhaps even critical as it provides its end-to-end turnkey solutions offering for major sized projects in the USA.

Central and Eastern Europe is also a rich hunting ground for infrastructure projects supported by EU Funding and with their market leading position in materials, products & services they are very well placed. This market is roughly 70% the size of the US and so offers significant opportunity.

The region via its NextGenerationEU recovery funding program has added over Euro 800bn to the region's future investment activities for the 2022-2027 budget period. The most important beneficiaries are similar, think renewable energy, rail, electric vehicle charging infrastructure, and hydrogen. Central and Eastern European markets are set to gain most. Europe has also demonstrated increased demand for the full end to end services that the company provides in the USA, which slots right into the company's long-term plan for sustainable growth.

Why I think it's cheap

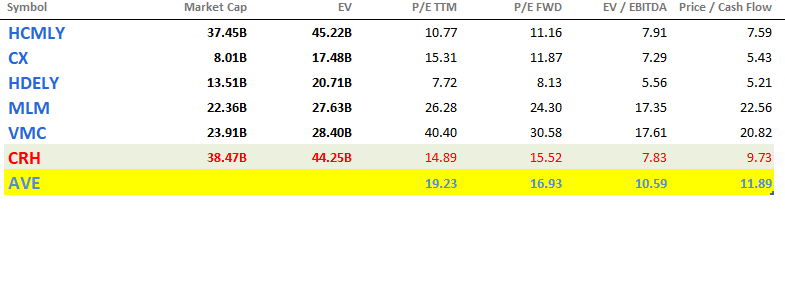

Looking at the peer group the most comparable in terms of product offering are Vulcan Materials Company ( VMC ) and Martin Marietta Materials Inc ( MLM ). Holcim ( HCMLY ) and HeidelbergCement ( HDELY ) are more focused on cement and related products, but I've included them here for completeness.

CRH Peer Group Comparison (Seeking Alpha)

{kind=link}

Direct peers are trading at huge premiums to CRH. On a forward PE perspective, the discount to VMC and MLM is 49% and 36% respectively. Looking at EV/EBITDA the discount is over 50%. This seems just far too wide for my liking.

The business is performing incredibly well results out on March 2, 2023 proved as much.

2022 Financial Highlights (Company Presentation)

{kind=link}

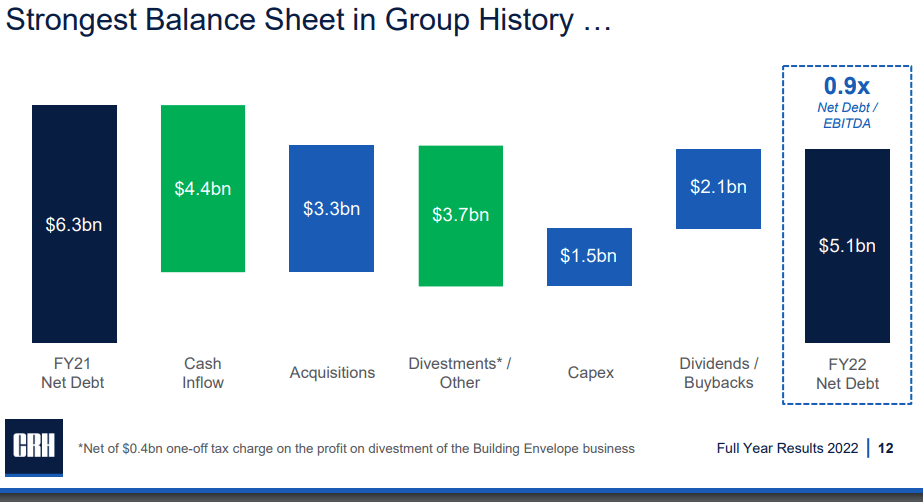

In a tough environment of rising rates and sky-high inflation the company grew all metrics impressively - even margins widened by 10bps. This shows operating leverage in what has clearly been a challenging time. They generated $2.5bn in free cash flow and ended their financial year with the strongest balance sheet in their history.

Balance Sheet Bridge (Company Presentation)

{kind=link}

What is the company worth?

Perhaps the peer group is too expensive I mean an average FWD PE of 27x and average EV/EBITDA multiple of 17.5 does seem a little steep but the market might just be pricing in the expected $1trn plus of investment due to hit the economy over the next decade? For the sake of prudence, we'll apply a 20% discount to the peer set which gives us room for a derating of those companies just in case they're too dear and they reset lower at some point.

PE Valuation:

The current average PE of its two closest peers is 33x.

The average FWD PE for MLM and VMC is 27x.

Taking CRH to 21.5x earnings (20% discount to peers) based on reported EPS of $3.50 implies a target of $ 75.60.

EV/EBITDA Valuation:

The current average peer group EV/EBITDA multiple is 17.5 vs 7.83 for CRH. Using a 20% discount here too and taking the CRH multiple to 14 implies a share price of $ 110.00.

Turning to a DCF we get the following:

I'm using 12% earnings growth for the next 5 years on the assumption of US and EU govt programs filtering into the economy and benefitting the company (this is compared to 14% earnings growth last year). Then ill reduce the terminal growth rate right down to 0.5% per annum to be ultra conservative. The discount rate I'll use is 8.5% which is the long-term average return expectation for the S&P 500. This also happens to be their weighted average cost of capital ((WACC)).

DCF Value = $ 70.80

DCF assumptions (Author)

So, with an eye on three different metrics, we get a range of $ 70.00 - $ 110.00 which is quite vast. If we stick with the low end though a potential return of 36% seems possible.

But what's the catalyst?

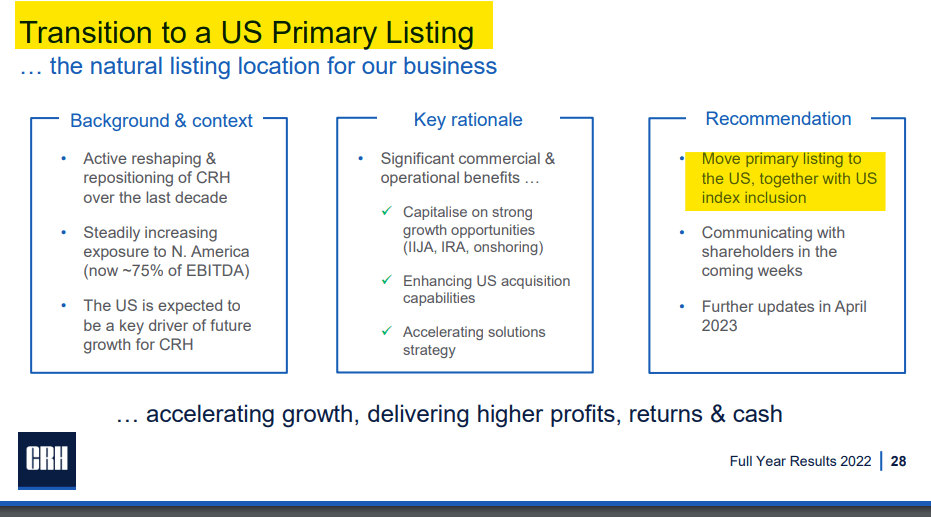

So, what's going to get us there you ask? Well, this is my view. The company was born and raised in Ireland and then moved its primary listing to the UK. This now puts the company in the European Universe primarily from a research and investment perspective. Despite 75% of earnings now originating from the US it's still getting valued like and compared to European businesses.

The catalyst to change this and crystalise a higher rating would come from the company moving its primary listing to the USA and away from the UK and in the latest earnings release management confirmed that this was now in motion.

Transition to US listing (Company Presentation)

{kind=link}

This is exactly what's going to get us our rerating in my view. I've demonstrated how I think the company cheap especially when compared to its direct US peers and now that it's going to be listed alongside them like for like comparisons are more likely. More US analyst research time will be allocated to the name. This becomes especially true when the company is included in US indices. That would be the major event as passive buyers jump in and it forces fundamental research teams to analyse the company in order to ensure market benchmarks are understood.

Time and patience are required however as the index inclusion requirements for different indices vary but in the example of the S&P500 a market cap of $12.7bn is required and annual dollar value traded to float adjusted market cap must be greater than 0.75 (that implies potentially a year of trading in the US to demonstrate this)

The Seeking Alpha ratings page shows just 2 US analysts out with recommendations on the stock at present vs VMC with 21 and MLM with 19. From a US context it's pretty much 'unheard of'. Even doing a followers check on Seeking Alpha yields comparable results.

Number of followers:

MLM = 11.73K

VMC = 17.27k

CRH = 3.9k

But wait there's more… Seeking Alpha Quant picks have outperformed the market by a handsome margin. The quant model has a remarkable success rate of beating the market and CRH is featured as a strong buy with a Quant rating of 4.89 here.

What are the risks?

CRH operates in a cyclical industry, building cycles are impacted by things like GDP growth, interest rates, employment growth and population growth. The cycle is elongated this time however due to massive govt spending programs, in my view, but nonetheless this must be considered.

Costs need to be monitored as high rates of inflation and supply constraints of things such as fuel can impact business performance.

Debt levels need to be watched alongside the cost of debt and its duration. This is important particularly for companies that are cyclical by nature. Cash flows need to be able to cover debt repayments or servicing costs throughout the cycle.

Acquisitions made by the business such as CRH have integration risk and price risk. Management has to ensure they pay a fair price and get the perceived value extracted from such M&A deals.

The shift in listing may not happen or if it does a rerating may not occur. Perhaps the valuation against peers is justified or VMC and MLM are just far too expensive and fall to valuations similar to where CRH is now.

Conclusion

CRH is a company with a cheap valuation operating in an industry with massive tail winds which are expected to last for at least a decade. The company is underfollowed in the US Markets and on Seeking Alpha despite it generating most of its earnings in the country, this is primarily because the business is domiciled in the Europe with a primary listing in the UK. Management's intention to move the listing to the US sets the tone for a large rerating and is a major catalyst to unlocking value for shareholders.

The stars are aligning for the investment too as its cheap valuation and strong backdrop have also generated a strong buy on the seeking alpha quant list where tis currently ranked as 4 in its sector and 1 in its industry.

CRH is a strong buy.

For further details see:

CRH: Undervalued And Catalyst Ahead