CROX - Crocs: My Top Value Pick For 2024 And Beyond

2023-10-27 10:00:00 ET

Summary

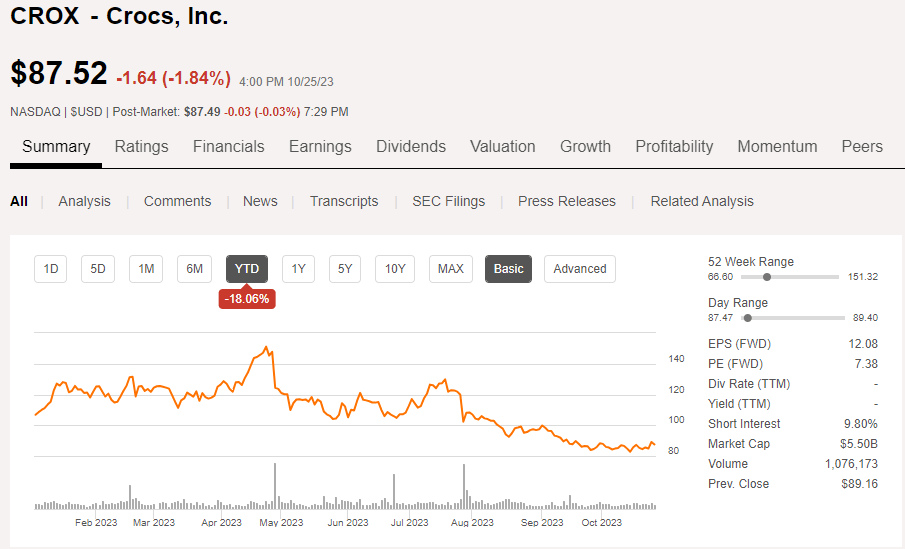

- Crocs' performance has been volatile, with shares falling 18% year-to-date.

- Crocs is a quality business with strong branding, attracting a wide range of consumers and influencers. It has a massive geographical exposure and is gaining popularity among Gen Z.

- The shift to direct-to-consumer sales can potentially increase already high margins for Crocs.

- The company is aimed at deleveraging, which I think can happen quickly enough to increase buybacks in the near future.

- Crocs is dirt cheap.

Main thesis

Crocs' (CROX) performance has been a rollercoaster so far as shares tumbled 18% year-to-date. The metrics growth is cooling down after the Covid impulse, and the acquisition of HEYDUDE added problems to the parent brand. But I think the company had it long coming as it's very hard to keep the same growth pace with no low base effect. And still, the company is still crushing it in terms of DTC sales, capturing market share thanks to penetration in Asia and Europe and margin expansion. Crocs is an amazing business with a promising growth strategy but the market is still sleeping on it keeping valuations incredibly low, which opens up a buying opportunity.

{kind=link}

What makes a good value stock?

A value stock is generally described as a stock of a structurally undervalued company (i.e. with a market valuation lower compared to its peers). That doesn't mean our goal is to simply find businesses with lower-than-average multiples (even if we are using forward ones like forward P/E or forward EV/Sales).

The whole idea behind value investing is to get value from the asset thanks to its low valuation. But there is no real value in the company with decreasing market share, low profitability with no signs of improvement, and no sustainable business model, is there? That's why I focus on 4 different factors when looking for value ideas:

- Low forward valuation multiples compared to other companies in the industry

- A high-quality sustainable business model that has a wide competitive moat

- Competent management that is focused on the long-term prospects of the company and shareholders' gains

- Increasing profitability or a clear path to one

So here are 4 reasons why Crocs stock is my personal favorite value idea.

Reason 1: Crocs is a quality business with strong branding

Few would argue that Crocs have taken the fashion world by storm. For a long time, the company's shoes remained a niche product. The demand came from vacationers at seaside resorts, yachtsmen, and children, but was criticized for ugliness and replaced by much cheaper counterfeits retailing at $5-$10. Times have changed, however, and clogs, which not so long ago were considered ugly, have gained great popularity among ordinary consumers and are suddenly everywhere now. And that's not just because of marketing but because of the globally developing anti-fashion trend.

More than just a brand or a shoe, Crocs is often perceived as a lifestyle choice that traditional, boring shoes in favor of comfort and practicality. That trend is set by influencers such as Ariana Grande, Justin Bieber, Madonna, John Cena, Mario Batali and Drew Barrymore. Previously, in order to look like their idol, fans had to buy clothes for thousands of dollars, which not everyone could afford. Now they have the opportunity to purchase part of the image of their favorite star for less than $100.

This causes a massive stir, which plays into the hands of Crocs. The company actively promotes its brand independently through collaborations with popular brands and artists. For example, after the photo of Nicki Minaj wearing pink Crocs, this model sales soared 49 times in 2021. The shoes created in collaboration are extremely popular. For example, this summer Crocs' collaboration with Barbie was hyped enough to be sold out the first weekend it came out. Overall, the main love for the brand comes from Gen Z, which placed Crocs in the 6th place of favorite brands among all clothing brands.

Massive geographical exposure should also be mentioned as it increases overall market share and shows brand strength.

Asia is starting to become another important long-term growth driver for the Crocs brand, as it currently lacks regional penetration compared to the US. In the second quarter, revenue in Asia grew 39% in constant currency, with growth spreading across the region, including China, Australia, South Korea and Southeast Asia. Another exceptional quarterly growth came from China, where second-quarter revenue increased by more than 100%, another sign of potential in that market. During the popular off-season festival in June, Crocs had the second-highest sales on Tmall among all casual shoe brands. In the near future, management expects China's share of total revenue to double from the current 5% to 10%.

{kind=link}

Reason 2: DTC shift is a way to higher profitability

The power of the Crocs brand can be compared to huge retail names like Calvin Klein or Louis Vuitton, although these companies produce different products. Crocs sell their shoes for $50-70, although their cost is $15-20, and fakes that look the same, but are made of a different material, are sold for $5-10. But nevertheless, the company manages to sell more than a hundred million pairs of shoes per year and has margins similar to those of premium apparel brands.

Crocs is also better at turning revenues into net profits than its competitors.

Despite high margins, I believe the company still has to find a way to bring them higher for shareholders' additional value as shareholders are directly interested in earnings that can be distributed in the form of dividends or buybacks.

Previously, retailers dictated terms for Crocs with branding that was not as strong as it is today. A lot has changed as the consumer has become the main factor. The relationship between manufacturer and consumer is reaching a new level - face-to-face, without an additional layer in the form of a retailer. DTC is a massive opportunity to increase margins as there is no retailer to mark up the price.

Crocs' CEO, Andrew Rees says they target higher DTC sales instead of wholesale:

Our global CRM database is also accelerating in key markets with the expansion of programs like SMS and the app. As we mentioned last quarter to gain better control of our brand and realize higher ASP, we anticipate transitioning some of our Croc's Etail business that sits in our wholesale equipment to a direct digital sale both on Crocs.com as well as marketplaces, where we will sell directly to the consumer. This will result in lower wholesale sales and higher DTC sales.

Source: Author, Crocs

Reason 3: Deleveraging and massive buyback potential

After acquiring HEYDUDE for $2.5 billion the debt increased to $2.8 billion. The company managed to shrink to just $2 billion, but it still sits high as the net debt-to-equity ratio is 156% now. But this is alright since it's well covered by operating cash flow (42% if we add cash) and interest payments are covered by EBIT (>5x coverage).

Crocs' management is aimed at quick deleveraging and targets a 1.0x - 1.5x net debt / EBITDA ratio. If we assume TTM EBITDA growing at a current CAGR of 7.2%, it would take 2 quarters to bring gross leverage down to 1.49x. There is still $1 billion in buyback left under the current program, which means that 17.7% of all shares can be bought back at $90 per share. That is great news for shareholders as buyback yield can get as high as 10% then.

Source: Crocs

Reason 4: Dirt cheap

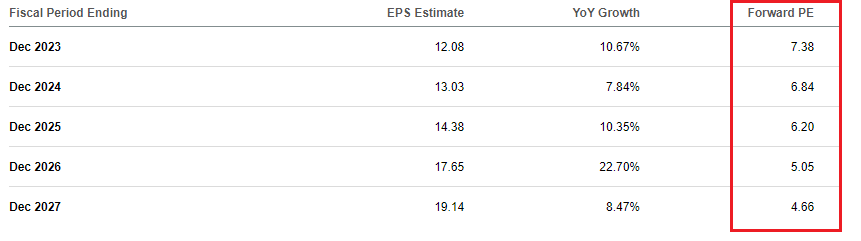

Despite the fact that the capitalization of Crocs has grown 20 times over the past 5 years, this company is valued inexpensively, because financial flows have grown along with the shares. But the 20% drop this year left the already fairly cheap company structurally undervalued. Forward P/E based on EPS projections is single-digit despite double-digit growth.

{kind=link}

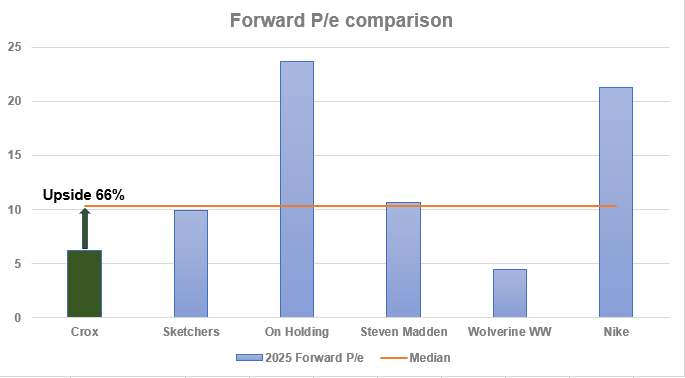

If we compare Crocs to other footwear companies using median P/E, the situation just gets more confusing as businesses with lower growth pace and worse profitability are somehow trading with a higher multiple.

Source: Author, Seeking Alpha data

{kind=link}

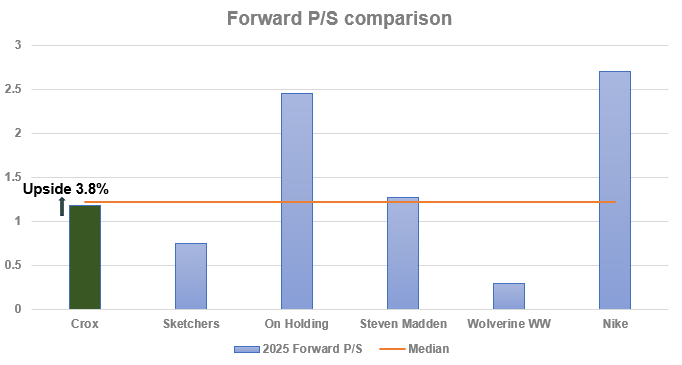

The similar forward P/S model suggests only a 3.8% undervaluation of the company. However:

- The only two companies cheaper than Crocs are Sketchers (SKX) with a 13.8 percentage points lower margin and Wolverine World Wide (WWW) with nearly 0 growth rates. Given its branding advantage and higher margins, CROX should trade with a premium, but somehow that's not the case.

- P/E is still a better metric here since it's more important to materialize revenue into profits which other companies have problems with, judging by lower margins.

Source: Author, Seeking Alpha data

{kind=link}

Risks to consider

Firstly, there is a slowdown in sales of HEYDUDE, which is associated with weak orders from wholesalers due to a lack of available funds and the lack of a clear sales history for the second half of the year, in contrast to the long-selling Crocs. HEYDUDE is hampered by discounts and promotions, which has led to a decline in the average selling price. And I think the situation will remain this way in the coming quarter, which is partly due to such a weak revenue forecast for Q3. Moreover, brand distribution opportunities will be limited, especially due to the transition to ERP and warehouse facilities, in the second half of the year. As a result, we'll likely see a decline in both HEYDUDE's revenue and earnings for some time. The management believes that the decline is temporary and expects to return to the growth trajectory later, but a clear plan is unknown here and this likely scares investors.

Secondly, the clothing and footwear sector is very sensitive to economic instability and consumers' tastes shift. Over the past 10 years, big names like Escada, Christian Lacroix, American Apparel, and Versace have filed for bankruptcy. Crocs' revenue is not diversified and largely depends on sales of Crocs themselves, so if their popularity suddenly declines, the company will face declining sales and financial difficulties.

Takeaway

Despite a quality business model, high margins, and buyback potential, Crocs is trading at 6.2x 2025 forward P/E, which is one of the lowest in the industry. The market completely ignores it and continues to focus on negative factors, like HEYDUDE troubles. Well, I recommend taking advantage of this approach as it creates a real opportunity to buy a cheap stock with good prospects.

Editor's Note: This article was submitted as part of Seeking Alpha's Best Value Idea investment competition , which runs through October 25. With cash prizes, this competition -- open to all contributors -- is one you don't want to miss. If you are interested in becoming a contributor and taking part in the competition, click here to find out more and submit your article today!

For further details see:

Crocs: My Top Value Pick For 2024 And Beyond