SHOO - Crocs: Underappreciated Business Ready To Buyback 17% Of Shares

2023-08-30 05:40:55 ET

Summary

- Crocs has identified four key pillars for future growth: digital sales expansion, increasing sandal market presence, enhancing brand recognition for Hey Dude, and tapping into international markets, particularly China.

- CROX stock is currently undervalued compared to its peers, with a forward price-to-earnings ratio of 7.8x and an attractive free cash flow yield of 12.5%.

- The company boasts strong profit margins, outperforming competitors like Nike and Deckers Outdoor, and has a 5-year average ROIC of 24%.

- Lastly, due to large debt repayments, Crocs is recommitted to buying back shares with $1 billion left in share repurchases under the latest program.

Crocs ( CROX ) stock is out of flavor, while consumers keep buying the clogs in masses. The company beat on both earnings and revenue in July, yet it could not stop the decline in stock price. There are 4 pillars that offer sustainable growth. Nonetheless, Crocs is trading as the cheapest stock compared to peers. In this article I lay out my thesis of why Crocs is heavily underappreciated by the market.

Business Overview

Crocs provides consumers with casual footwear in more than 85 countries worldwide through two distribution channels: wholesale and direct-to-consumer.

Crocs sells products under two brand names: Crocs and Hey Dude . The latter one was recently acquired by Crocs for $2.05 billion in cash and $450 in Crocs shares issued to the founder of Hey Dude. While it was an expensive acquisition, the new brand fits Crocs high margin and growth business model.

{kind=link}

The Crocs brand is a niche in the market with its unique design and comfort. The rise of Croc shoes to global prominence can be attributed in part to strategic celebrity endorsements and collaborations. The transition in focus to sandals shows the brand's ability to maintain relevance and appeal in an ever-changing fashion landscape. Sandal revenues are expected to grow almost 30% in 2023 to $400 million. The core markets with growth opportunities for the Crocs Brand are China, India, South Korea, the U.S., and Europe.

The Hey Dude brand focus is on casual style, comfort and easy-going footwear. The brand signature design is characterized by light materials and ergonomic sole. Hey Dude Shoes has experienced a rapid rise in popularity, thanks in part to its strong online presence and direct-to-consumer model. The collaborations with celebrity, like Dude Perfect who have 60 million subscribers on YouTube, increase the brand recognition greatly. The Hey Dude brand has mainly been selling in the U.S. and is expanding more into Europe throughout 2023.

Growth Opportunities

Crocs has 4 important pillars that should grow the business in the coming years.

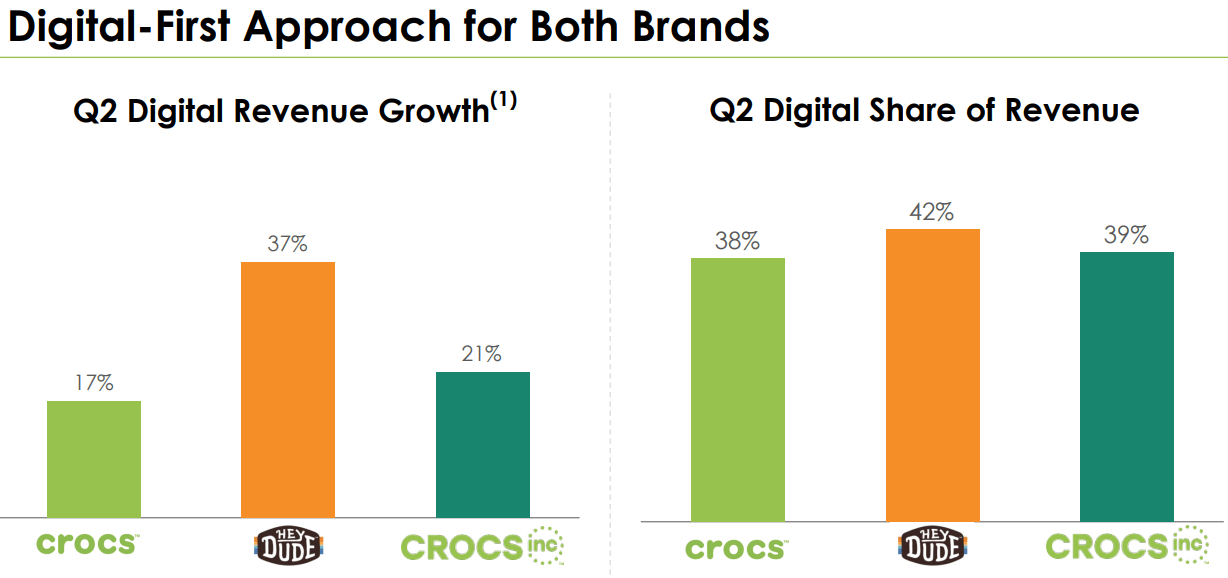

The first one is digital sales . Digital sales includes sales directly to consumers through the company-owned websites, third-party marketplaces, and wholesale sales to global e-tailers.

{kind=link}

The increasingly popularity of sandals is another key pillar for the company. The sandals market is massive and can deliver Crocs with further revenue growth in the coming years.

{kind=link}

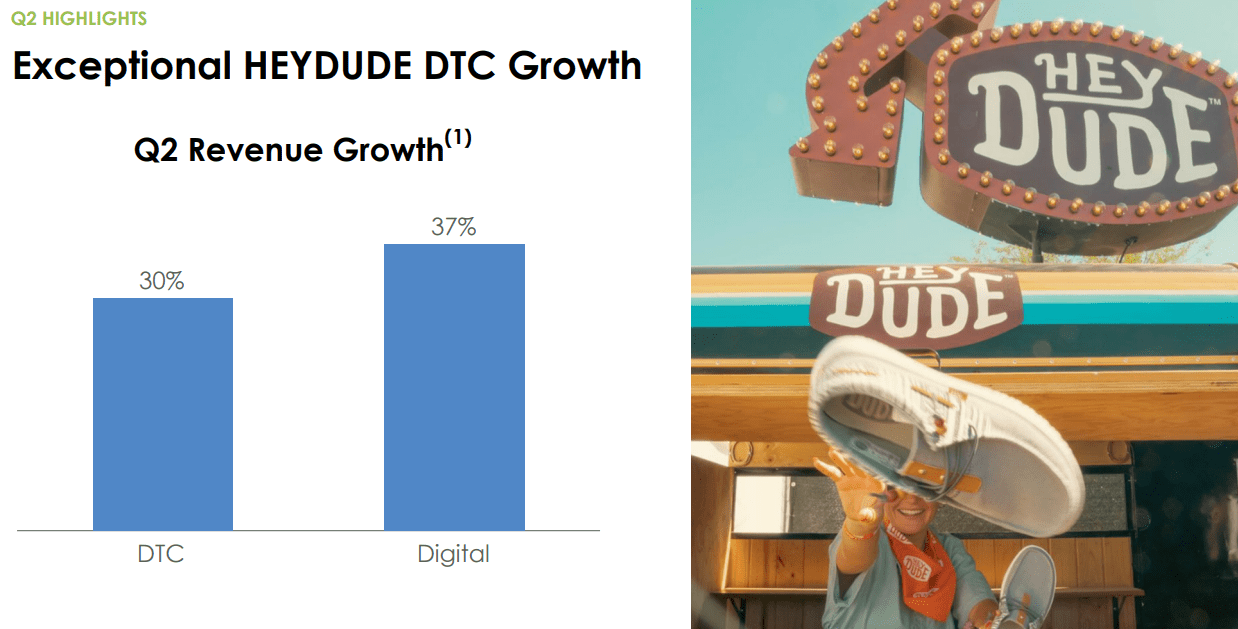

The third pillar for the company is increasing the brand recognition and distribution for the Hey Dude brand . Next year a new distribution center will open in Las Vegas to fix the storage and logistics situation for Hey Dude. Further, growing the brand international with a main focus in Europe is another promising prospect.

{kind=link}

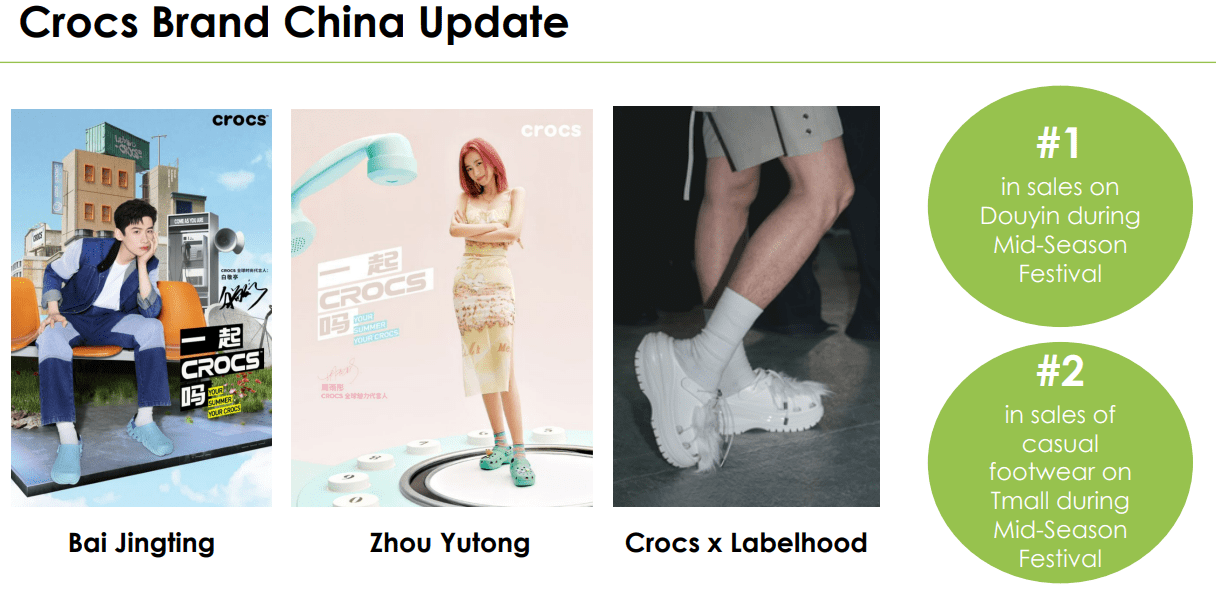

In the trailing twelve months, 40% of Crocs brand sales were from international markets. Management believes a large opportunity is left in the international market . China is the main candidate, as the second largest foot apparel market worldwide. The Crocs brand ended 1st in sales on the Chinese version of TikTok (Douyin ??) and 2nd in sales on the Chinese Tmall app of Alibaba during the Mid-Season Festival. In the second quarter, revenue in the Asia Pacific market grew by 39%.

{kind=link}

Valuation

Following up with valuation, we can see that Crocs is valued the cheapest among peers based on a forward price-to-earnings ratio. V. F. Corp. ( VFC ) is the closest peer with a FWD PE of 9.3x. There are two stocks with quite a premium, Nike ( NKE ) at 26.5x FWD PE and Deckers Outdoor Corp ( DECK ) at 23x FWD PE.

Further, if we compare foot apparel peers on EV-to-Free cash flow, than only Steven Madden ( SHOO ) is priced below Crocs. The other peers are priced double as expensive with a few even showing negative free cash flow. EV stands for enterprise value and this takes into account the market cap combined with total debt minus cash and cash equivalents. The debt increase after the Hey Dude acquisition affected EV-to-Free cash flow to be temporarily higher.

More so, Crocs' free cash flow yield is exceptionally high at 12.5%. Wolverine World Wide has a slightly higher free cash flow yield following a sharp stock price drop after a disappointing earnings report and a management shake-up.

Since, Crocs is valued so discounted you might have thought that they have a lower margin business. Nonetheless, Crocs has the highest gross profit margins in the sector at 55%. Even while, the gross margins dropped from the 60% region due to the Hey Dude acquisition, which has slightly lower margins than the Crocs brand.

In the latest quarter, margins saw an increase again because of lower freight rates and the pricing power to push inflation further to the consumers.

In addition, Crocs' profit margins are again the strongest out there. Even topping that of the "premium businesses" Nike and Deckers Outdoor. Of course, I do understand that Nike does not only sell footwear apparel and might have higher margins on the shoes they sell. Still, very impressive how Crocs managed to go from lowest profit margin business to moving above and beyond the other peers.

Lastly, Crocs has been allocating capital excellently in the last 5 years with a median return on invested capital of 30% and an average ROIC of 24%.

Balance Sheet

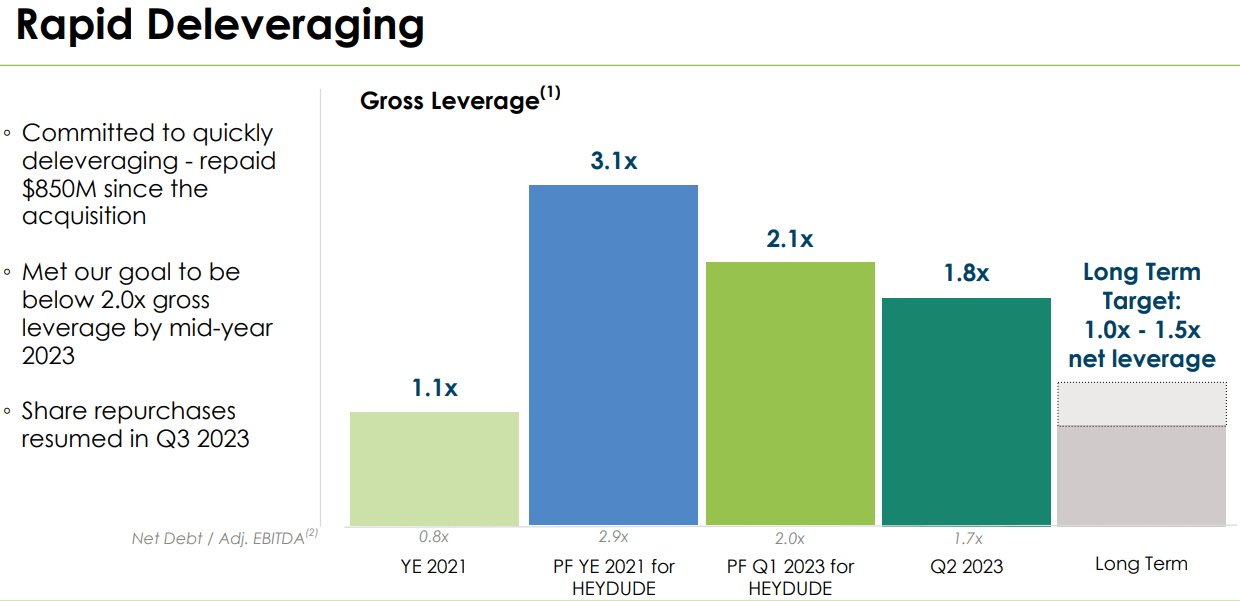

The S&P Global downgraded Crocs' business to negative after the $2.5 billion Hey Dude acquisition on concerns of integrating the business with its core assets. However, in January 2023 the S&P Global revised the outlook to stable. Although Crocs long term debt is still high at $2 billion, I do not think it will be a problem to pay it off. First of all, Crocs was able to get a refinancing of the loan, which decreased the interest rate by 0.5%. Secondly, in the trailing twelve months free cash flow was $750 million. If Crocs would allocate all their free cash flow to repaying the debt, it would only take 2.6 years to pay it off. In case, free cash flow drops to $500 million in the following years it would take around 4 years. The first maturity date on the borrowings is due to 2029, so the company has plenty of time to pay back the debt.

While Crocs shows up in the upper part of the graph in terms of Debt-to-Equity ratio, the management is laser-focused on deleveraging the balance sheet. Share buybacks were temporarily put on hold to accelerate the process to get the leverage below 2x. Now that gross leverage is below the minimum target of 2x, fueled by strong free cash flow generation, Anne Mehlman EVP and Chief Financial Officer mentioned in the refinancing press release:

Since acquiring HEYDUDE in February 2022, we have repaid $850M in debt and intend to methodically balance debt repayment and share repurchases as we approach our long-term net leverage target."

{kind=link}

Considering the low valuation compared to peers, buying back shares seems like the right thing to do in combination with paying down debt. Under the current buyback program, there is $1 billion left for share repurchases, which accounts for almost 17% of the market cap. In 2021, Crocs bought back for $1 billion in shares, which in hindsight might not have been very optimal, nevertheless this shows the commitment from management to give back to shareholders. Must we see the $1 billion of share repurchases in 2023 or 2024 at the current prices, than I am quite convinced we could see substantial upside from here.

Takeaway

When I look at Crocs, I see an underappreciated business that has the profitability and brand recognition for a premium valuation. Yet, the stock is trading by far as cheapest in the sector. There are clear paths to sustainable growth and deleveraging, while also focusing on shareholder value through share buybacks.

I rate Crocs a "Strong Buy" and have initiated a starting position at $96 a share. Consumer weakness in North America can temporarily pose a threat to a slowdown in sales growth, yet it should not endanger the repayments of debt, of which maturity is still a long way out. The Crocs brand is a perfect fit for the Asian market and should progress well in brand recognition going forward.

For further details see:

Crocs: Underappreciated Business, Ready To Buyback 17% Of Shares