CCRN - Cross Country Healthcare: Earnings Beat And Price Retreat

2023-08-05 07:50:54 ET

Summary

- Cross Country Healthcare reported strong Q2 earnings, beating expectations with revenue of $540.7M primarily driven by physician staffing and education sectors.

- The company showed improved gross margin and decreased SG&A expenses, indicating a positive operational strategy.

- Despite a promising quarter, there are headwinds to consider, including a projected downturn in the next quarter, warranting a "hold" rating on the stock.

Thesis

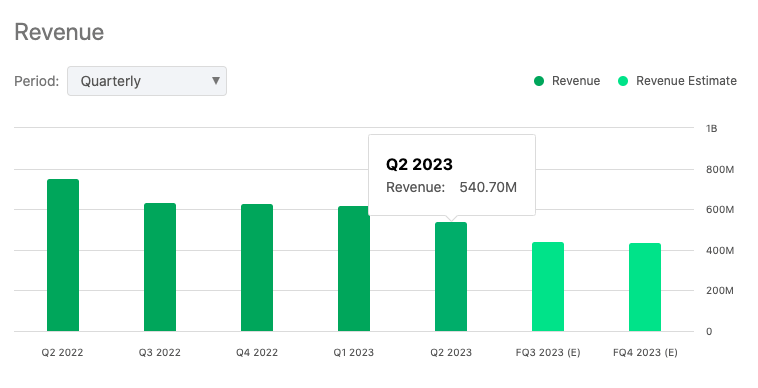

In the second quarter of 2023, Cross Country Healthcare (NASDAQ: CCRN ) reported non-GAAP EPS of $0.69 that beat by $0.08, and revenue of $540.7M that beat by $9M, primarily due to strong performances in the physician staffing and education sectors. However, this analysis argues that despite a promising quarter, there are headwinds to consider, including a projected downturn in the next quarter which warrant a "hold" rating on the stock.

Company Profile

Cross Country Healthcare, Inc., based in Boca Raton, Florida, is in the American healthcare services landscape, primarily operating within Nurse and Allied Staffing and Physician Staffing.

With its comprehensive suite of services in the Nurse and Allied Staffing division, the firm offers not just traditional staffing and recruiting, but an assortment of enhanced talent solutions, accommodating temporary and permanent placements for a diverse set of healthcare professionals.

The firm's Physician Staffing division further diversifies its portfolio, supplying a wide range of healthcare facilities with specialty physicians and other practitioners. Since its inception in 1986, Cross Country Healthcare's extensive reach, evidenced by a broad clientele spanning public and private hospitals, government facilities, and outpatient clinics, among others, underscores its position as a significant contributor in the sector.

Cross Country Healthcare's Q2 Earnings Highlights

Cross Country Healthcare, in the second quarter , exceeded the upper limit of their revenue guidance, delivering a performance that has surpassed expectations. With a consolidated revenue amounting to nearly $541 million, the company’s progress can be attributed to the performance in two major sectors: physician staffing and education.

{kind=link}

Investigating further into the company's financials, we see an improvement in the gross margin by 40 basis points when compared to the first quarter. This increment has been largely ascribed to the annual payroll tax reset.

The company demonstrated judicious management of selling, general and administrative (SG&A) expenses which saw a decrease of 6% sequentially, and 8% year-over-year. Factors contributing to this decline include lower variable compensation and reductions in costs related to salaries and benefits, further indicating an operational strategy that's moving in the right direction.

When we turn our focus to the top line, it's evident that the company's performance not only met but exceeded expectations. This was further magnified by tight cost management, culminating in earnings that manifested in an adjusted EBITDA of $44 million.

Strategically, Cross Country Healthcare has been purposefully aligning its investments with the prevailing market conditions. According to management, the goal is to ensure profitability is maintained while there is room for future growth. While it may be important to note the reduction in the company's internal headcount by over 10% since the start of the year, the firm continues to channel resources into areas with high growth potential and technology-driven initiatives. For instance, CEO John Martins highlighted the use of their propriety vendor system "Intellify", which, according to him:

...will save us millions of dollars annually in tech fees paid to third-parties.

Within the Nurse and Allied segment, the education business experienced substantial growth, exceeding 40% on a year-over-year basis. The Physician Staffing segment also surpassed expectations, realizing $45 million in revenue. This constitutes an upsurge of 12% sequentially and more than double the revenue from the prior year, largely due to a recent acquisition.

Assessing the financial position of the company at the end of the quarter reveals it to be holding its own. The company reported cash holdings of $673,000 and an outstanding debt of $31 million under their ABL facility. The firm's performance coupled with a positive cash flow has brought down total leverage to less than 0.2 times.

Furthermore, Cross Country Healthcare's cash flow from operations has remained high, with the company generating $119 million. This figure represents the second-highest quarterly performance on record for the company thanks to a steady pace of collections, and a reduction in Days Sales Outstanding (DSO) to 63 days.

Performance

Seeking Alpha

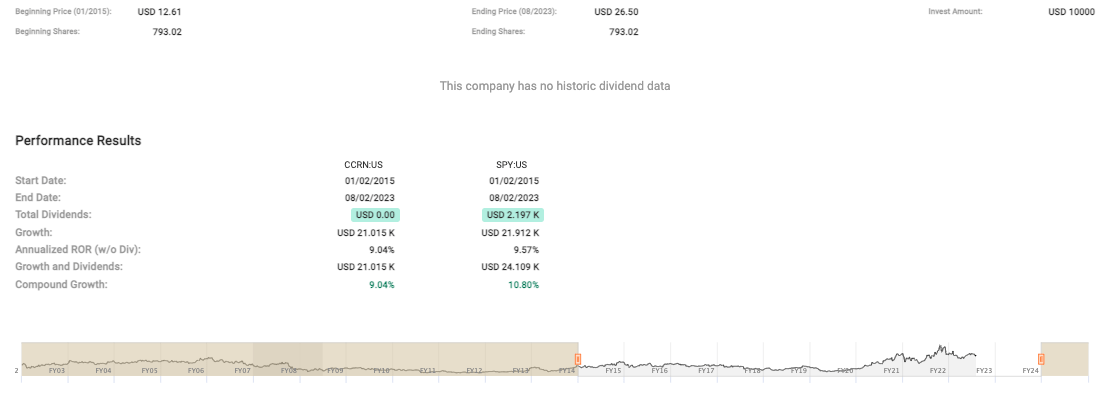

Unfortunately, at the time of this analysis, Cross Country Healthy is trading down -3.47 or -13.70% before the midday mark. With that in mind, its medium-term performance (see data below) from the beginning of 2015 to August 02, 2023, has seen the stock nearly double from $12.61 to $26.50, representing an annualized rate of return (ROR) of 9.04%.

{kind=link}

When we compare Cross Country Healthcare's performance to the S&P 500 Index , we see a slightly different narrative. The S&P delivered an annualized ROR of 9.57% without dividends, which slightly edges out CCRN. But let's not forget the impact of dividends. Including those, S&P's Compound Growth Rate jumps to 10.80%.

Valuation

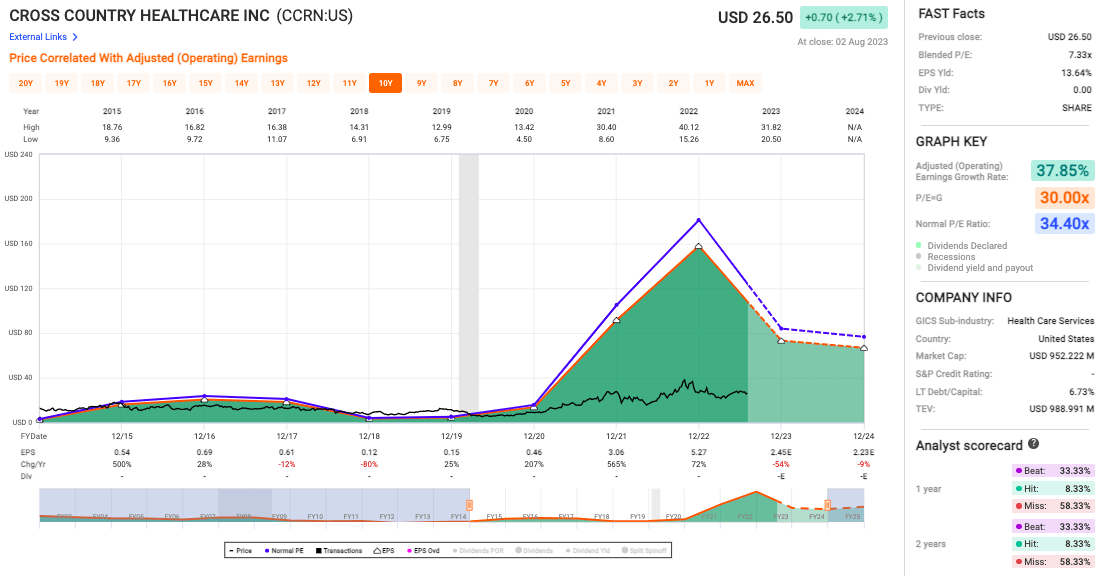

Cross Country Healthcare's Adjusted Operating Earnings Growth Rate of 37.85% (see chart below) suggests that the company's operations had been firing on all cylinders and generating robust earnings growth.

{kind=link}

Meanwhile, the Blended P/E ratio at 7.33x, significantly below the normal P/E ratio of 34.40x indicates that the market is undervaluing the stock, given the substantial earnings growth rate. However, prior to yesterday's earnings report and today's intraday selloff, it also raised the question of why the market was pricing the stock so cheaply; perhaps now we know why.

Risks & Headwinds

Even with an apparent upbeat performance, Cross Country Healthcare's revenue suffered a decline of 28% YoY and 13% sequentially. Analyzing the company's nurse and allied segment deeper, including the Travel Nurse and Allied business, we see a revenue drop of 15% sequentially and 32% YoY. The primary drivers of this downturn are reduced bill rates for travel and fewer billable hours. Demand significantly eased off at the beginning of the year and, while orders are making a slow recovery, average bill rates persist in their softening trend. This has resulted in a discrepancy in clinicians' pay expectations and, consequently, a softer Q3 than was initially projected. Moreover, the local or per diem business experienced a dip in revenue due to a decrease in demand.

As Cross Country Healthcare sets its sights on the third quarter, it expects its revenue to fall within the boundaries of $440 million to $450 million. This prediction signals a sequential tumble of 17% to 19%. The primary contributors to this projected decline are attributed to that softening in travel bill rates as well as a decrease in volumes.

Adjusted EBITDA forecasted for the forthcoming quarter is estimated to range between $27 million and $32 million, or an adjusted EBITDA margin between 6%-7% compared with previous quarter.

Parallel to this, Cross Country's adjusted earnings per share are also anticipated to experience a downturn in the next quarter. Specifically, these are predicted to descend into a range of $0.35 to $0.45.

Final Takeaway

I would rate Cross Country Healthcare's stock as a "hold." The company demonstrated significant revenue growth, tight cost management, and promising innovation, including the new "Intellify" system, but is facing concerning headwinds. The decline in revenue and the forecasted decrease in the next quarter due to lower travel bill rates and volume decreases require careful observation, even though it currently appears to be undervalued according to its P/E ratio.

For further details see:

Cross Country Healthcare: Earnings Beat And Price Retreat