CCRN - Cross Country Healthcare: YOY Earnings Decline Low Valuation Sketchy Chart Seen

Summary

- Healthcare stocks have struggled mightily in 2023 after a strong relative return last year.

- Healthcare Providers have done better, but one name remains significantly below its 2022 peak.

- I see earnings uncertainty with Cross Country and the chart warrants some caution.

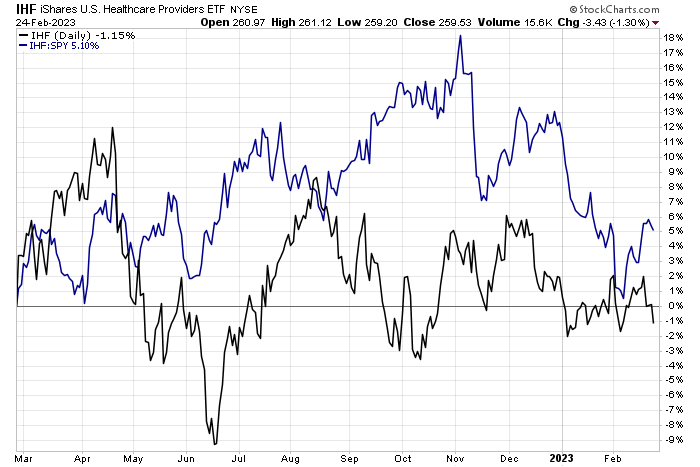

The Healthcare sector has lagged lately. The group as a whole is down a stunning 9 weeks in a row, but one niche has fared a bit better this year. U.S. Healthcare Providers, as measured by the iShares U.S. Healthcare Providers ETF (IHF), are actually about even with the S&P 500 in 2023.

One name within the industry, Cross Country Healthcare (CCRN), has endured similar bearish price action, falling about 40% from its November peak to a recent high-volume low. But are shares now a value play? I see about balance risks and rewards here on valuation and in the charts.

XLV: Health Care ETF Down 9 Weeks Straight

Stockcharts.com

Healthcare Providers Somewhat Better

{kind=link}

According to Bank of America Global Research, Cross County Healthcare is a healthcare staffing company, which sources and recruits nurses, physicians, and other allied healthcare professionals to work on temporary assignments in healthcare facilities in the U.S. The company also provides talent management software as well as recruitment, processing, and consulting services.

The Florida-based $958 million market cap Healthcare Providers & Services industry company within the Healthcare sector trades at a low 5.2 trailing 12-month GAAP price-to-earnings ratio and does not pay a dividend, according to The Wall Street Journal. CCRN beat its Q4 earnings estimate and reaffirmed 2023 guidance, but revenues may turn negative sequentially from Q1 to Q2 ahead. AMN voiced similar concerns in its quarter.

The firm cited declining rates on open orders nearing double-digit percentages which may hit hardest in Q2 ahead. Upside potential stems from Cross Country being able to cut costs more effectively related to staffing and labor, but obviously the downtick in COVID-related demand will hurt from a year ago and on the 2-year stack.

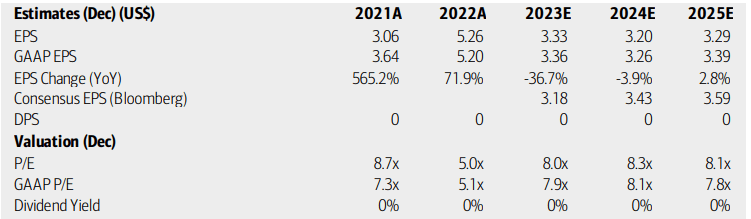

On valuation , analysts at BofA see earnings falling big this year and declining once more in 2024. Modest per-share bottom-line growth is seen by 2025. The Bloomberg consensus forecast is a bit more sanguine compared to BofA when looking ahead several quarters. No dividends are expected, though. Shares remain priced cheap with high-single-digit earnings multiples.

Hence, Seeking Alpha rates the stock with an A+ on valuation, but growth is tepid with a D-. Even if we allow the stock a 12 multiple using $3.40 of 2025 earnings, that is $41 at least a year from now with CCRN sporting a low forward PEG ratio of 0.8. A high near-term discount rate and industry uncertainty cast shadows on the hypothetical valuation. Overall, while I like the valuation, earnings uncertainty remains high.

Cross Country: Earnings and Valuation Outlook

{kind=link}

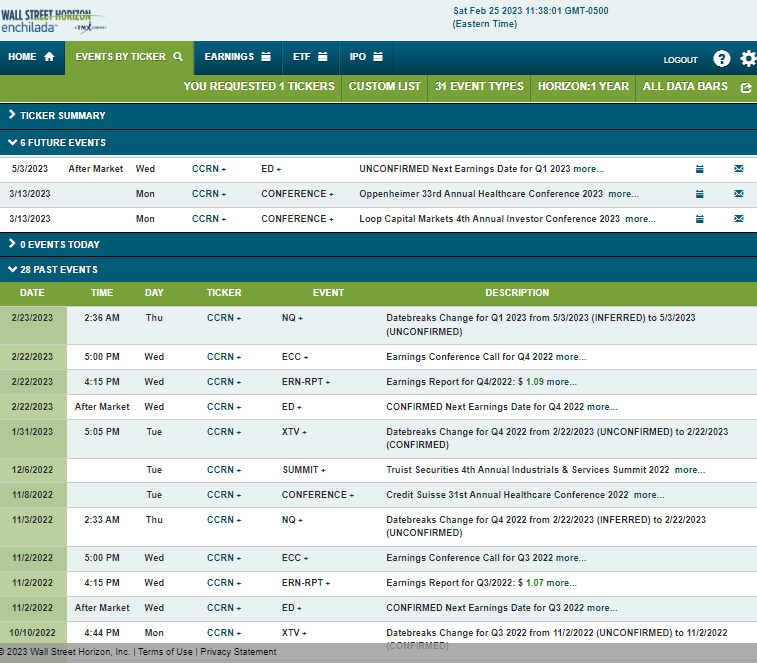

Looking ahead, mid-March is key for Cross Country. Its management team is expected to present at the 32 nd Annual Healthcare Conference put on by Oppenheimer from March 15 to 17. Just before that, CCRN is slated to speak at the Fourth Annual Loop Capital Investor Conference on March 13 and 14. So expect some possible volatility that week should new information about the company or industry cross the wires.

Corporate Event Risk Calendar

{kind=link}

The Technical Take

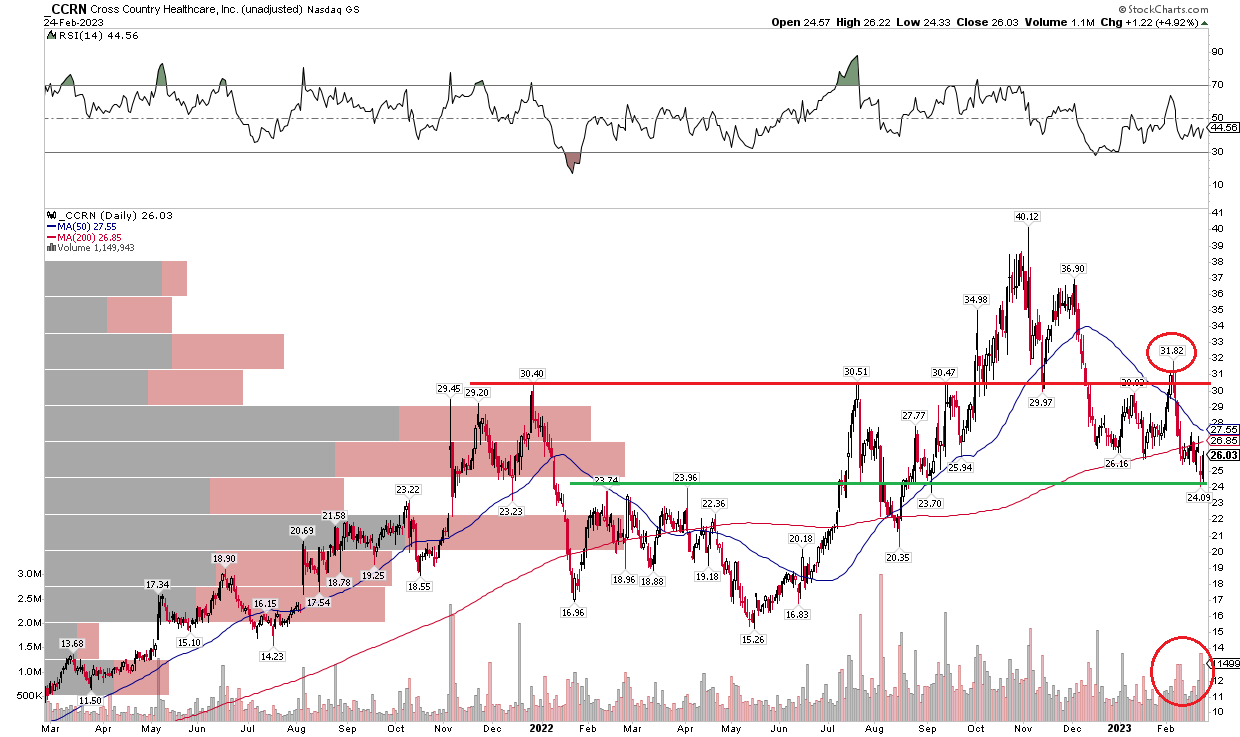

CCRN looks a bit better on the charts versus the valuation, but once again, it is not a clear path higher. Notice in the chart below that shares dipped to my initial support call of $24 and have bounced. But a broader topping pattern may be unfolding, so I fear that the green support line below might yield to the bears.

There was indeed a bearish false breakout a few weeks ago before the approach to support. That dip occurred on high volume, too. The stock is now back below its 200-day and 50-day moving averages, and I would like to see CCRN rise above $32 to help support the bulls’ cause here. A long play with a stop under $23 could work, but I do not see it being a great value until it gets into the teens again.

CCRN: Shares Dip to $24 Support, Still Vulnerable

{kind=link}

The Bottom Line

Cross Country is a hold on both valuation and technicals. The P/Es and PEGs are attractive, but there are industry headwinds and weak earnings ahead. The chart also shows its own set of risks.

For further details see:

Cross Country Healthcare: YOY Earnings Decline, Low Valuation, Sketchy Chart Seen