CAPL - CrossAmerica Partners: A Favorable Outlook And Lower Fuel Costs Imply Undervaluation

2023-11-24 02:38:06 ET

Summary

- CrossAmerica Partners LP expects lower fuel costs and benefits from recent acquisitions, which could lead to free cash flow growth.

- Successful pricing strategies and merchandise offerings, as well as negotiation of fuel purchase orders, could contribute to the company's growth.

- While there are risks from higher interest rates and dependence on fuel costs, the stock appears undervalued.

CrossAmerica Partners LP (CAPL) recently delivered a beneficial outlook, including expectations about lower fuel costs and benefits from recent acquisition of assets. I believe that further successful pricing strategies, successful election of merchandise offerings, and negotiation of fuel purchase orders could bring significant FCF growth. There are some risks coming from higher interest rates, high dependence on fuel revenues, and volatility in wholesale costs, however in my view, the stock looks undervalued.

Product Analysis, And Recent Quarterly EPS Growth

Incorporated as a Delaware limited company in 2011, CrossAmerica is engaged in the wholesale distribution of motor fuel and the leasing of real estate for retail distribution. Controlled by the Topper Group, it operates via two segments: wholesale and retail. The following are figures reported in the last quarterly report.

Source: CrossAmerica Partners LP Reports Third Quarter 2023 Results

The wholesale business segment encompasses the wholesale distribution of motor fuels to tenant dealers and independent distributors. With exclusive distribution contracts, independent distributors own the property and all inventory, while tenant dealers lease the property and set prices and margins. The supply of brand-specific or unbranded fuel is facilitated, and contracts vary in duration. The wholesale business segment is obviously the most relevant in terms of revenue.

With that about the business activities, I believe that it is worth having a look at the company after revising the most recent quarterly report. The company did not release a surprising revenue, however the EPS GAAP was better than expected. Quarterly EPS stood at close to $0.31 per share with revenue close to $1.21 billion. Given the current market valuation, I believe that many in the market did not really react to the new information.

Source: SA

With that about the new figures reported, CrossAmerica Partners reported that even taking into account that fuel margins declined, the balance sheet and strong operating results position the company very well for the future.

CrossAmerica had another excellent quarter with continued strong operating results in fuel margins, fuel volume and store merchandise sales and margin. While retail fuel margins were down from the extraordinary quarter last year, the overall business still performed well for the current quarter. With our strong balance sheet and solid distribution coverage, the business is well positioned for the future. Source: CrossAmerica Partners LP Reports Third Quarter 2023 Results

Balance Sheet

As of September 30, 2023, the company reported cash and cash equivalents worth $5.79 million, accounts receivable of about $38.735 million, accounts receivable from related parties of $445 million, and inventory worth $53.609 million. Total current assets were equal to $123.261 million, below the total current amount of liabilities. The company seems to receive inventory in advance and sells to the clients. In order to finance these activities, CrossAmerica Partners uses some debt.

Property and equipment stood at $706.409 million, with goodwill worth $99.409 million and total assets close to $1.217 billion. The asset/liability ratio stands at more than 1x, so I believe that the balance sheet appears stable.

Source: 10-Q

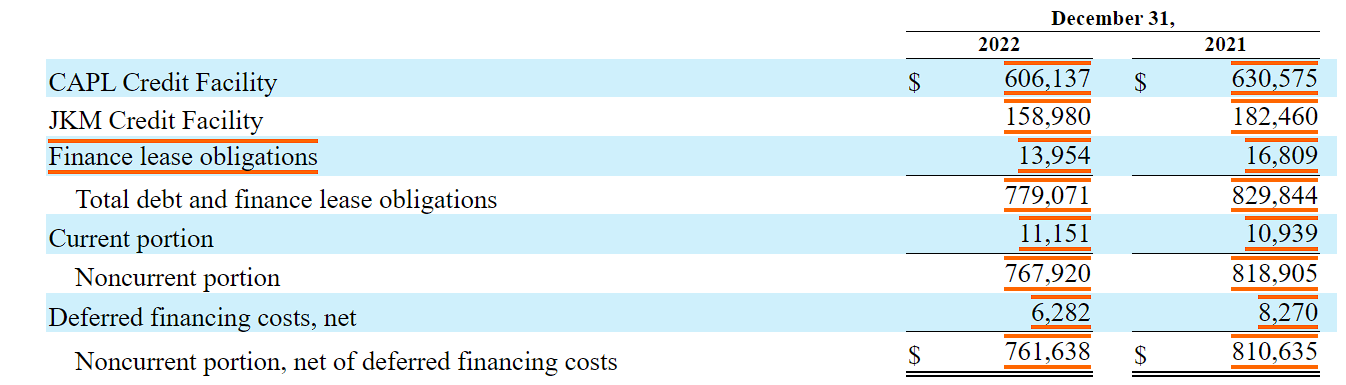

I am not really worried about the total amount of debt because CrossAmerica Partners appears to have a solid business model with long term generation of FCF. With that, investors may want to study carefully the leverage, which is not small.

Source: Investor Presentation

Current portion of debt and finance lease obligations stands at $3.034 million, with accounts payable worth $80.21 million, debt and finance lease obligations of $760.688 million, and asset retirement obligations close to $47.506 million. Total liabilities stood at close to $1.167 billion.

Source: 10-Q

CrossAmerica Partners has a $750 million Senior Secured Revolving Credit Facility due April 2024, subject to increase upon request. Loans bear interest based on LIBOR or base rate, with adjustable margins depending on the leverage ratio. The facility is secured by assets, including an interest in a subsidiary. Financial covenants must be followed, and a violation could result in termination and loan expiration. In 2022, the effective rate was 4.2%. Additionally, there is a $200 million JKM Credit Facility, secured by assets of Holdings and subsidiaries, maturing in July 2026 . With these figures in mind, I believe that the cost of capital would most likely be above 4%.

{kind=link}

{kind=link}

Successful Merchandise Selection And Pricing Strategies Could Bring Further Gross Profit Margins

Given the recent merchandise gross profit percentage increases reported in the last quarter, CrossAmerica appears to be making smart offerings. Perhaps, management successfully increased prices, and clients are at the moment accepting the changes. I believe that we may see further gross profit margins increase, if CrossAmerica continues to develop smart pricing strategies.

Source: Investor Presentation

The Acquisition Of CSS And New Acquisitions Could Also Bring FCF Margin Increases

The most recent outlook offered to investors includes expectations about gross profit margins derived from the acquisition of assets from CSS.

Our results are anticipated to be impacted by the acquisition of assets from CSS, which is anticipated to increase gross profit within the wholesale segment. Source: 10-Q

I believe that management may have to lower its leverage in order to make more acquisitions. However, if CrossAmerica Partners finds new assets at a beneficial valuation, deb investors may approve new transactions. As a result, I would expect FCF margin growth.

Maintaining strong relationships with oil companies, CrossAmerica also seeks to optimize the operations of the acquired assets. With strengths in stable cash flows, a history of successful acquisitions, and prime locations, in my view, the company is positioned to capitalize on strategic opportunities. In this regard, it is worth noting that CrossAmerica does have significant expertise in the acquisition of assets and targets. In the last 9 years, goodwill increased significantly.

Source: Ycharts

Lower Fuel Costs Could Also Bring FCF Margin Improvements

In the last quarter, CrossAmerica noted beneficial expectations about fuel costs as the company signed new purchase contracts. In the long term, further successful negotiations with fuel sellers and new contracts could bring gross profit margin increases and FCF growth.

In addition, we anticipate that we will continue to realize reductions in our fuel costs as a result of new or amended fuel purchase contracts. We continue to consider the highest and best use class of trade for each of our properties, which may result in the conversion of sites from one class of trade to another and ultimately increases or decreases in the gross profit for the wholesale and retail segments. Source: 10-Q

My Income Statement Expectations

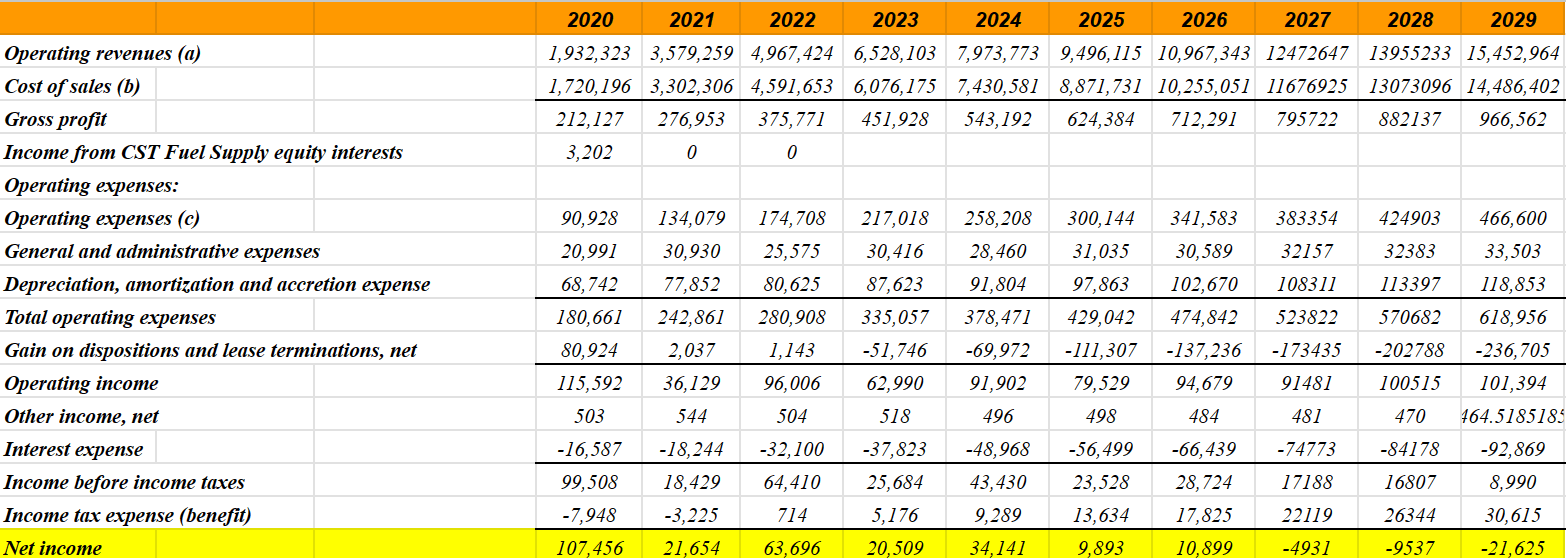

Under the previous assumptions, I included declining operating revenue growth, including a median net sales growth of 19% with a minimum growth of 10.7%. Given the net sales growth reported in 2021 and 2022, I think that my numbers are conservative.

{kind=link}

Also, with declining gross profit margin from 10% in 2020 to around 6% in 2029, I believe that my financial model appears likely and close to reality.

{kind=link}

More in particular, I included operating revenues of $15.452 billion, with cost of sales close to $14.486 billion, gross profit worth $966 million, operating expenses close to $466 million, and general and administrative expenses close to $33 million.

Besides, with depreciation, amortization, and accretion expense of about $118 million and total operating expenses worth $618 million, 2029 operating income would be close to $101 million. Finally, using 2029 interest expense close to -$93 million, 2029 net income would stand at -$22 million.

{kind=link}

My Cash Flow Expectations Taking Into Account Previous Assumptions And Previous Results

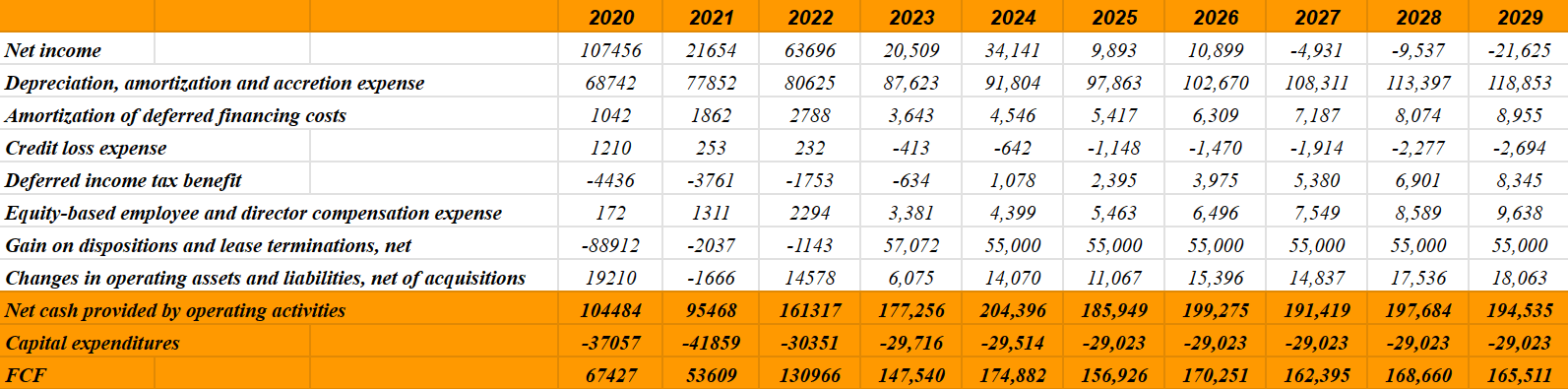

For the assessment of future FCFs, I took a look at previous results, and also included my previous assumptions. In the past, CrossAmerica Partners reported a maximum FCF of more than $120 million, and FCF growth seemed positive since around 2012.

Source: Ycharts

In the past, the company traded between 20x and 17x, however I tried to be as conservative as possible. I used a lower EV/FCF than what the company reported.

Source: Ycharts

My cash flow expectations included 2029 depreciation, amortization, and accretion expense close to $118 million, 2029 amortization of deferred financing costs worth $8 million, and credit loss expenses of about -$3 million.

Besides, with equity-based employee and director compensation expenses close to $9 million and changes in operating assets and liabilities, 2029 net cash provided by operating activities would be about $194 million. Finally, taking into account capital expenditures of -$30 million, 2029 FCF would be close to $165 million.

{kind=link}

I also included a WACC ranging from 4% to 6.5%, EV/FCF between 9x and 13x, cash and cash equivalents of $5.79 million, current portion of debt and finance lease obligations of $3.034 million, current portion of operating lease obligations of $35.085 million, and debt and finance lease obligations less current portion of $760.688 million. Finally, with a shares count of 37.971 million, the implied forecast price would be between $24 and $44 per share with a median close to $33 and $34 per share.

{kind=link}

Also, taking into account the current stock price, the internal rate of return would stand between 2% and 20% with a median IRR close to 10%-11%.

Source: My Expectations

Risks

The company faces significant risks due to high dependence on motor fuel revenues. Volatility in wholesale fuel costs, influenced by political, economic, and supply factors, can negatively impact gross profit. Seasonal fluctuations, changes in demand, and unpredictability in the transmission of changes from wholesale prices to retail prices add complexity. In addition, the inability to anticipate and adapt to changes in these factors could materially affect the company's financial performance and distribution capacity.

Besides, it is worth noting that increases in the interest rates could lower future EPS growth as CrossAmerica's debt is not small. In the last quarterly report, management noted that it is expecting higher interest expenses.

Lastly, given increases in interest rates, we also anticipate higher interest expense. Source: 10-Q

Competitors

In the wholesale segment, the company competes with other motor fuel distributors, standing out in customer service, price, quality of service, and product availability. In the highly competitive and fragmented convenience store industry, it faces competition from various chains and independent establishments.

Key competitive factors include location, accessibility, variety of products and services, fuel brands, pricing, customer service, store appearance, and cleanliness. The company adapts to constant changes in the retail offering, and seeks to excel in these factors to maintain its competitive position in the market.

My Opinion

CrossAmerica Partners LP operates in the wholesale distribution of fuels, showing strength in revenue and expansion strategies. Its focus on cash flows and well-managed acquisitions, backed by strong relationships with oil companies, is a key asset. In my view, successful pricing strategies, lower fuel costs thanks to successful negotiation of purchase agreements, and benefits from previous acquisitions like that of CSS could bring FCF growth. The company faces significant risks due to its high dependence on fuel revenues and volatility in wholesale costs, however I believe that the stock remains undervalued.

For further details see:

CrossAmerica Partners: A Favorable Outlook And Lower Fuel Costs Imply Undervaluation