CCI - Crown Castle: Downside Is Likely Limited

2023-11-10 14:29:51 ET

Summary

- Crown Castle has seen its share price drop due to two main headwinds.

- I discuss these headwinds and their implications.

- I also explain why the downside is likely limited and provide sensitivity analysis of potential upside in a number of scenarios.

Dear readers,

Crown Castle (CCI) is a U.S. cell tower REIT that has seen its share price plummet and its dividend yield rise to nearly 7%. This fall in price over the past two years has been mainly caused by two headwinds. Today, I want to discuss these headwinds and my realistic outlook for the REIT.

It's been a while since I last covered CCI in April at $124 per share. I was quite bullish on the stock then, but admittedly the stock price has declined much further than most (including myself) have anticipated and now trades at $95 per share.

CCI continues to face two headwinds

The first reason for the drastic sell-off was, of course, related to the rise in interest rates . And this is hardly a CCI-specific issue as nearly all REITs have suffered.

Interest rates impact CCI in two ways. The first is more important in the short term, while the second is in the long term.

REIT prices tend to be driven by the 2-year treasury yield in the short term. Consequently, a rise in yields is always going to likely result in a sell-off in REITs ( VNQ ), which is exactly what has happened over the past two years.

Since we cannot time the market, there's little we can do about these short-term fluctuations so we have to focus on the long-term.

And in the long term, fundamentals and cash flows drive most of the valuation. This is why REITs tend to outperform even in a high interest rate environment once rates stabilize.

High interest rates, impact cash flow by increasing their net interest expense. CCI is reasonably well positioned here. Their leverage is by no means excessive with a BBB+ rated balance sheet and a reasonable net debt/EBITDA of 5.4x. However they do have a relatively high floating debt exposure of 14% in addition to some near-term maturities.

Therefore, if interest rates stay higher for longer, their cost of debt will inevitably continue to rise from today's 3.8%.

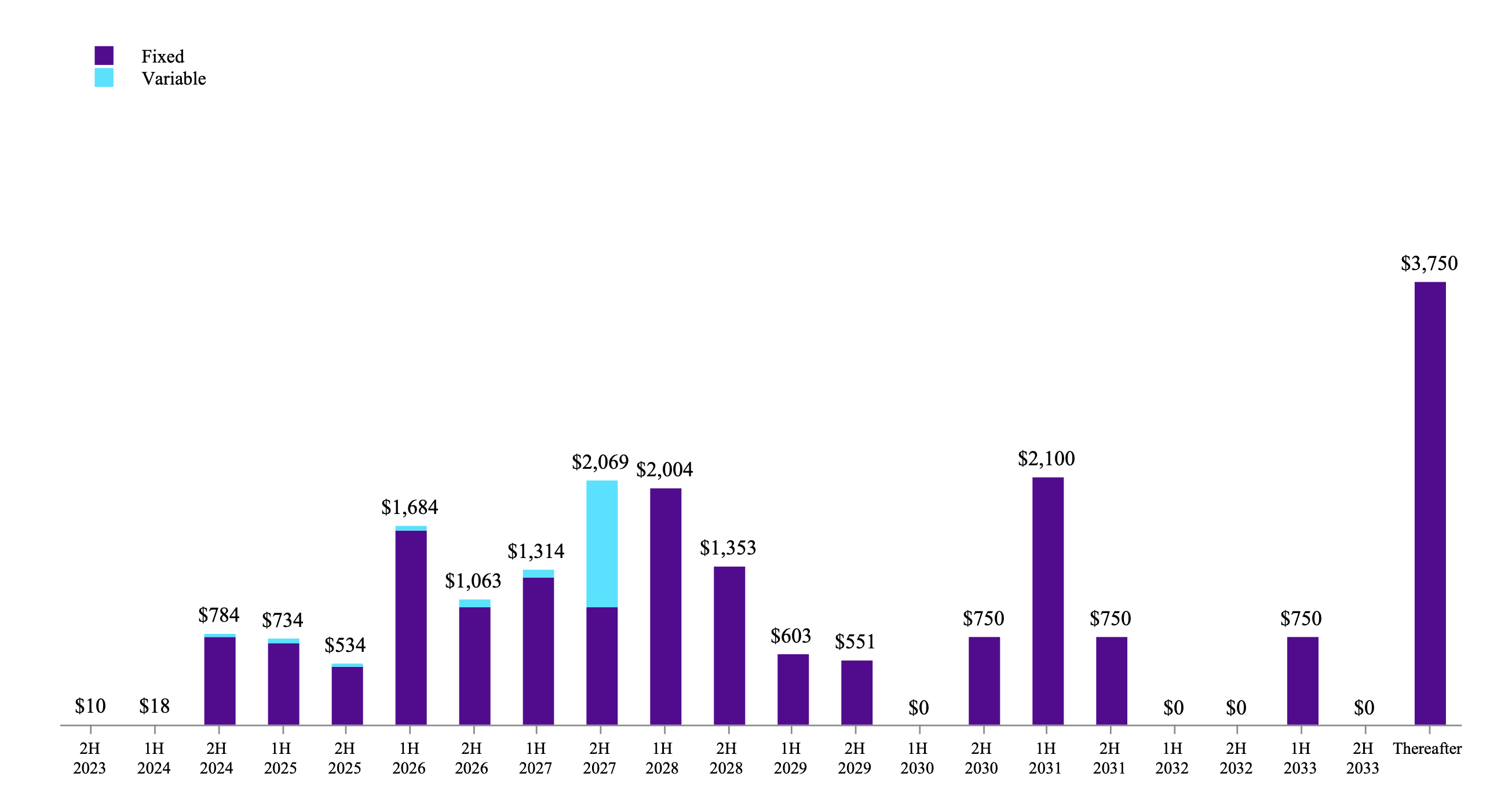

An example of this, is management's recent (poor?) decision to refinance a $750 Million maturing bond by their revolving line of credit which accrues interest at 6.2%. As a result, their interest expense in Q3 increased by 22% YoY to $213 Million. For the full year, management expects interest expense of $850 Million and for 2024, guidance calls for an additional 12% YoY increase.

{kind=link}

While a $100 Million in additional interest expense per year is significant, it's important to put things into context. CCI expects to receive annual rent of $5.6 Billion next year, so the increase in interest expense accounts for just 1.8% of revenues. Normally, that could be easily offset by 2-3% rent escalators which CCI has.

But this is where we get to the second headwind - the Sprint terminations .

Cell tower REITs have a unique advantage in their ability to lease space on a single tower to multiple tenants. But recently, when Sprint merged with T-Mobile ( TMUS ) this worked against CCI. Post merger it didn't make sense for T-Mobile to pay twice the rent for the same technology which is why Spring leases have been terminated and resulted in a rather significant drop in revenue for CCI.

These terminations will continue to affect the REIT until 2025 when they culminate. Lower revenue over the next two years has been largely priced in at this point, but the problem is that this also makes dividend coverage quite slim.

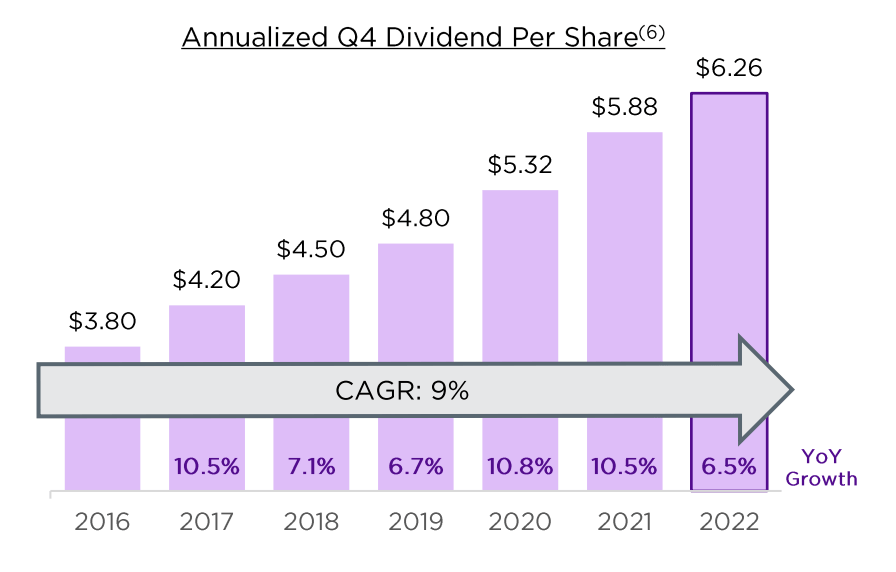

Management has stated on their earnings call that given the transitory nature of this problem and their expectation to return to 5% growth post-2025, it makes sense to keep the dividend where it is. The dividend currently stands at $6.26 per share and yields 6.5%. But with 2024 forecasted AFFO of $6.85-6.97, it's obvious that coverage will be tight.

{kind=link}

CCI's management has proven very competent over time, which is why I would give them the benefit of the doubt at this point. However income investors should be aware of the fact that the dividend will likely not be covered by free cash flow at some point next year or in 2025 and consequently might get cut.

What's beyond these headwinds

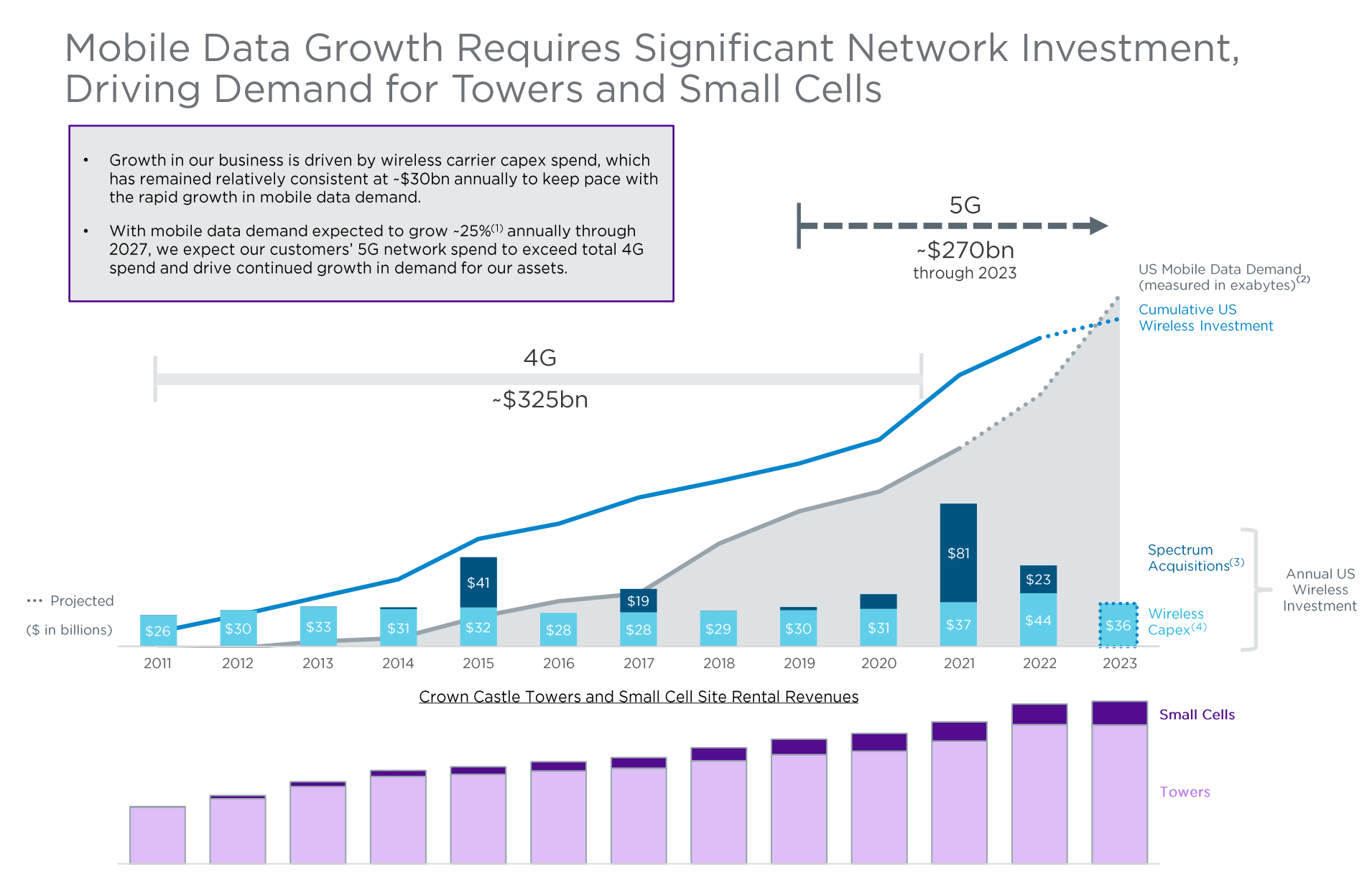

The business model works. Cell towers and fiber optics are absolutely key to telecommunication infrastructure and aren't going anywhere. Moreover, CCI's model is not CAPEX intensive at all and allows for very high EBITDA margins of 65%.

Demand for data is very likely to continue on its growth trajectory. To capture this demand, telco providers will have to continue to invest in their infrastructure which will directly benefit CCI.

{kind=link}

Consequently, I believe that once CCI works through the Sprint termination, it will be back to business as usual and the REIT will continue to grow its AFFO per share at 5% through a combination 2-3% rent escalators, putting additional technology on existing towers and expanding their portfolio. Note that management claims that 75% of this growth is already contracted and therefore very visible.

The REIT currently trades at an implied cap rate of 6.9% which is about 200 bps above 10-year treasury yield. That's a healthy spread for a company like CCI.

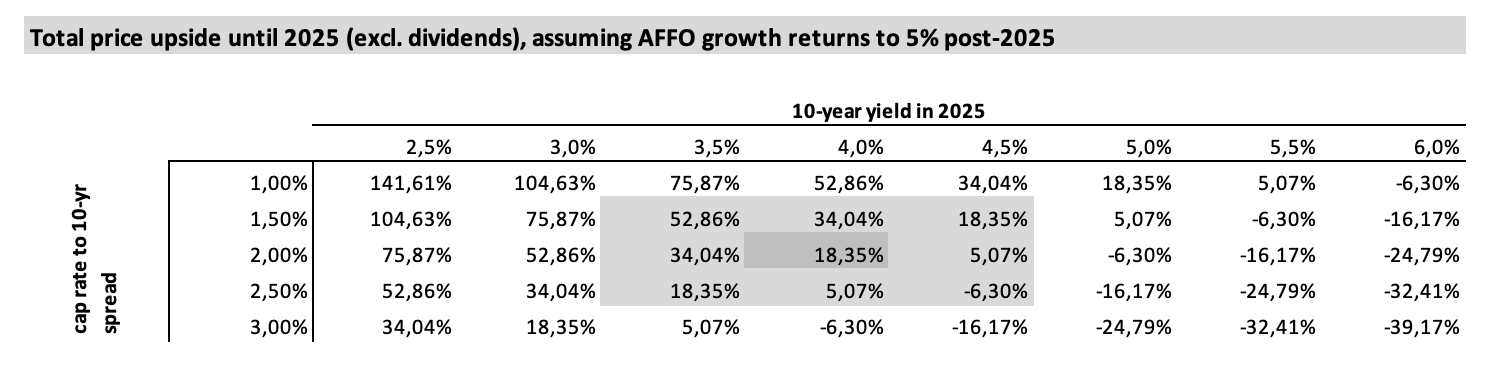

My base case assumes that management will deliver on their target. I expect NOI to decline by 7% next year due to Sprint terminations and a higher interest expense. Then, in 2025 I expect flat NOI, and post-2025 I expect growth to return to 5% per year. Since my upside calculation looks out to the end of 2025, at that point forward AFFO will already be growing at 5% per year.

I take this set of assumptions, keep the spread to treasuries constant at 2%, and look at a number of potential upside scenarios depending on the 10-year treasury yield in 2025. At a 4% yield, my upside would be 18% from price appreciation + 13% in dividends over the two years. That's a combined 31% over two years. And frankly, I could see the spread contracting as low as 1.5% which would increase the upside even more.

{kind=link}

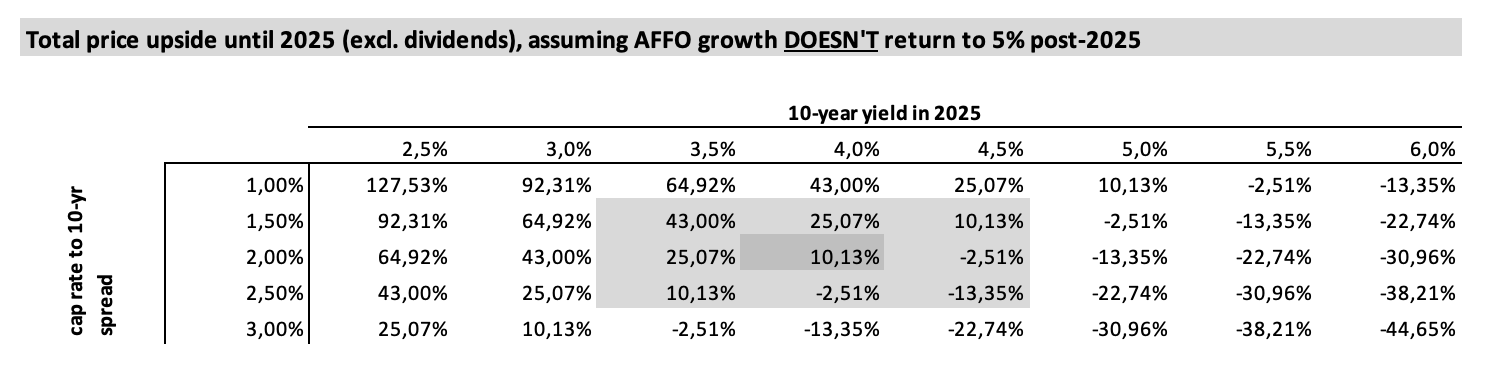

My bear case assumes that AFFO stays flat from 2025 onwards. In this scenario, I also assume that the dividend gets cut to a payout ratio of 75%. That would correspond to about a 20% dividend cut and the stock would yield about 5.5%. With an expected upside of 10% and 11% in dividends, we're looking at 21% over two years. That's still not bad for a bear case.

As far as additional risks, I don't think the spread is likely to widen further. CCI is too high a quality to trade at a 3% spread. But, of course, 10-year yields could be higher than 4% in 2025. In that case, the investment is likely to break even. It would take 10-year yields above 5% in 2025 to lose money on CCI. I think that's unlikely and see the downside as quite limited at this point.

{kind=link}

For further details see:

Crown Castle: Downside Is Likely Limited