SBAC - Crown Castle: Good Time To Pick Up This High Quality Player

2024-01-16 08:10:00 ET

Summary

- With plenty of economic uncertainties that remain, investors may do well to pick up high quality names with moat-worthy assets.

- Crown Castle Inc. is a strong investment choice due to its durable business model and history of strong returns.

- CCI remains undervalued with a respectable dividend yield. With growth expected to resume in 2025, the stock remains an appealing choice.

It’s a strange world we live in these days, where you now have to pay extra for a streaming subscription just to watch a select NFL playoff game . I had once thought that so long as you’re willing to sit through commercials, then you could watch for no extra cost beyond a cable subscription or a TV antenna!

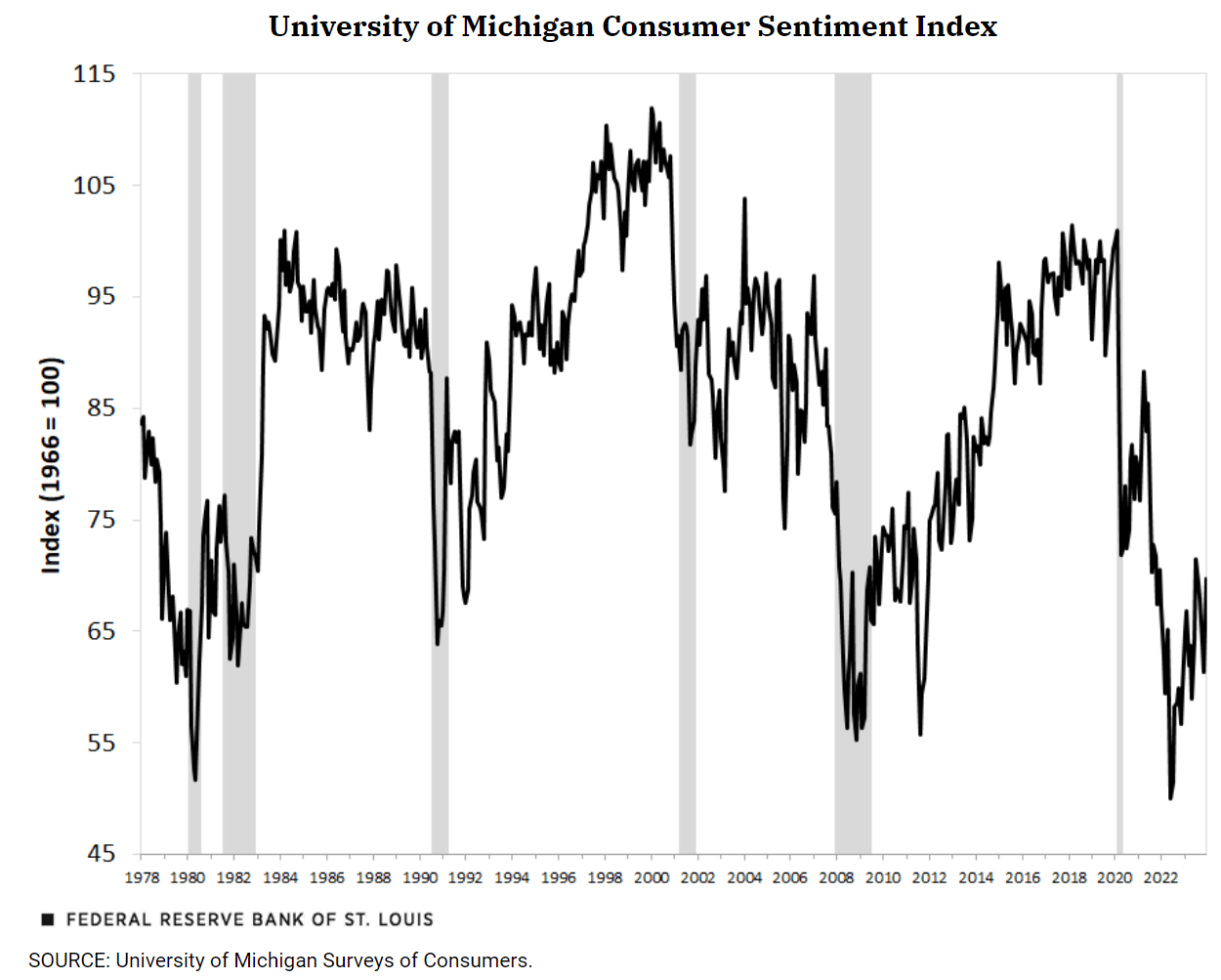

But I digress, turning to the economy, unemployment is low in the U.S. and in many parts of the world, and yet consumer sentiment remains rather low despite that fact. As shown below, consumer sentiment is even lower than where it was in 2010, when the U.S. was coming out of the Great Recession.

{kind=link}

In these confusing times, it’s anybody’s guess where the economy will land by the end of the year, and that’s why investors may be well served to layer into durable names that are economically essential for all market environments.

This brings me to Crown Castle Inc. ( CCI ), which I believe fits that mold. I last covered CCI here back in October with a ‘Strong Buy’ rating, noting its compelling value and accelerating growth in small cell deployments.

It appears that the market had agreed with my thesis, as the stock has given investors a 32% total return since then, besting the 13% rise in the S&P 500 ( SPY ) over the same timeframe. In this article, I provide an update and discuss why CCI remains a compelling buy at present for its dividend and value, so let’s get started!

Why CCI?

Crown Castle is one of just one of three large cell tower REITs that dominate the landscape, alongside peers American Tower ( AMT ) and SBA Communications ( SBAC ). It has over 40K cell towers and 85K route miles of fiber that touches every major U.S. market.

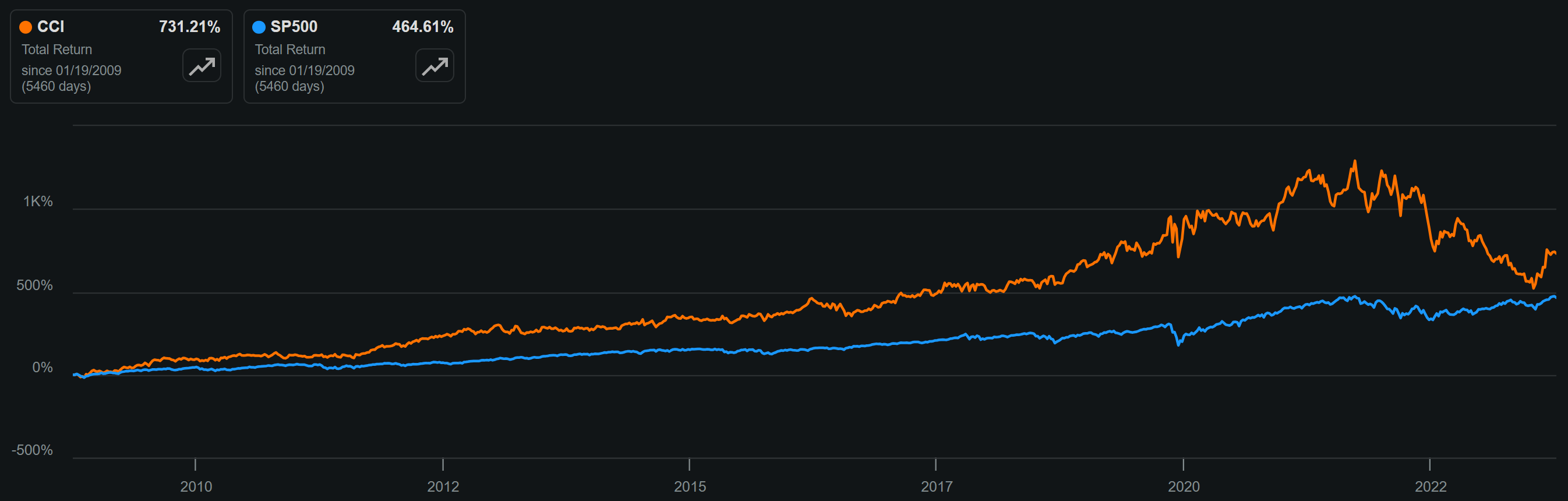

CCI has grown to its current size from humble beginnings. Due to its durable business model of leasing out much needed space in a growing wireless market, CCI has produced outsized returns over its history. This includes the prior 15 year period, in which CCI has given investors a 731% total return, far surpassing the 464% of the S&P 500, as shown below.

{kind=link}

Those who follow the stock closely know that CCI has seen some challenge over the past year, as reflected by its 25% decline in share price over the trailing 12 months. That’s because after years of aggressive expansion, the top wireless names Verizon ( VZ ), AT&T ( T ), and T-Mobile ( T MUS ) have pulled back their capital spending, especially as it relates to their 5G investments.

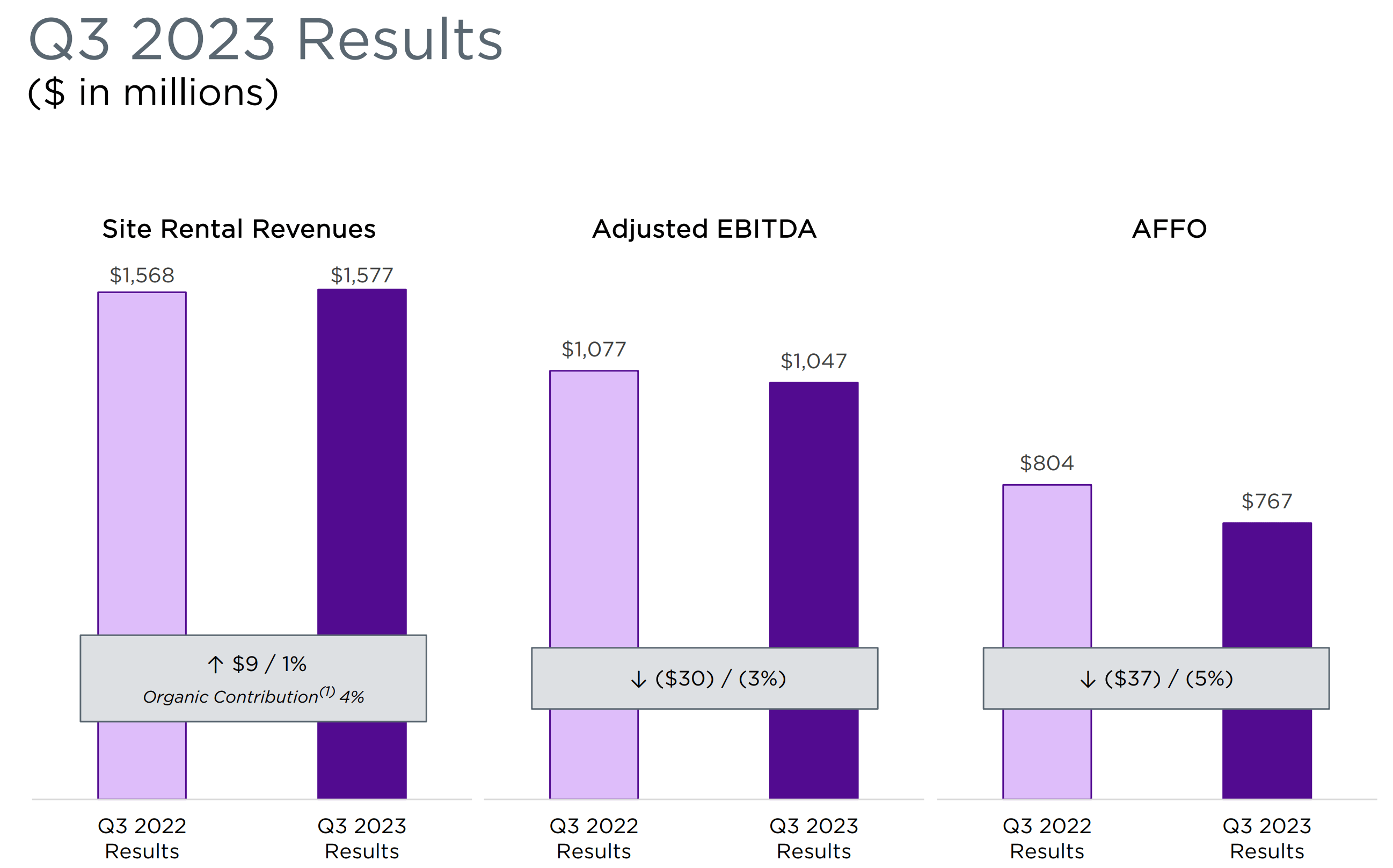

This has resulted in a slowdown in leasing activity, which management’s guidance implies that it will continue into the current year. As shown below, Site rental revenue grew by just 4.4% YoY on an organic basis (slowest since 2020), and both adjusted EBITDA and AFFO declined by 3% and 5%, respectively, during the third quarter.

{kind=link}

While these headline figures may be less than impressive, there are underlying trends that support a growth story beneath the surface. This is supported by the fact that after years of investment into the small cell space, this segment appears ready to turn the corner. This is reflected by management’s expectations that small cells will see 13% organic growth in 2024, driven by an estimated $60 million in core leasing activity and the addition of 14,000 new nodes this year, after adding 10,000 in 2023.

The market may have only recently begun to warm up to CCI’s small cell strategy, which is based on the value proposition they add to its existing infrastructure. Small cells are added to structures like utility poles and work with CCI’s towers to provide expanded wireless capacity and coverage.

Expansion of small cells could also be valuable to CCI’s customers like Verizon and T-Mobile which are aggressively expanding their fixed wireless customer base. For example, Verizon alone is seeing around 400K net fixed wireless adds per quarter, and ended its last reported quarter with 2.7 million fixed wireless connections. CCI’s management recently gave an update on its small cell strategy as follows:

We are consistently finding ways to build small cells and fiber more efficiently. These efficiencies allow us to provide the most cost-effective and reliable network solutions for customers. We look to deliver the highest risk-adjusted returns for our shareholders through continuously building on the core capabilities that I just mentioned that generate unique value in the businesses we own and operate. These capabilities reduce the overall cost of deploying and operating communications networks, which becomes even more compelling for our customers in times of increasing capital costs.

Risks to CCI include the recent activist involvement from Elliot Investment Management, which has built a $2 billion stake in the company, calling for a CEO change and a re-evaluation of its fiber business, implying that it wants for CCI to spin-off the unit. It appears that Elliot got its wish, as CCI announced the retirement of its CEO effective on January 16 th , with interim CEO Melone, who has served as CTO of Verizon in the past to step into the role. Elliot’s involvement introduces a level of uncertainty in the near term.

Also, CCI’s leverage ratio is currently elevated with a net debt to TTM EBITDA ratio of 6.8x, exceeding management’s long-term target of around 5x. This is, however, due in part to the Sprint-related churn and management expects to organically reduce the leverage ratio to be in line with its BBB investment grade credit rating from S&P. In the meantime, CCI has plenty of liquidity, with $5 billion in available capital under its revolving credit facility, against $750 million worth of debt maturities in 2024.

Importantly for income investors, CCI currently yields a respectable 5.6% and the dividend coverage ratio is somewhat elevated at 85%. However, management expects the first half of 2024 to be a trough for AFFO, with annual growth resuming in the 7% to 8% range in 2025, with dividend growth to resume next year as well. This is based on expectations that leasing will improve in the second half of this year and beyond, as customers continue to build out 5G.

Lastly, I continue to see value in CCI at the current price of $112.71 with a forward P/FFO of 15.3, which I believe to be highly reasonable for a long-term growth story with moat-worthy assets. This is based on expectations that CCI could reasonably achieve AFFO/share growth in the mid- to high-single digit over the long run, which when combined with the current dividend yield, could produce annual returns in excess of 10%. As shown below, CCI also trades at a material discount to its normal P/FFO of 21.8.

{kind=link}

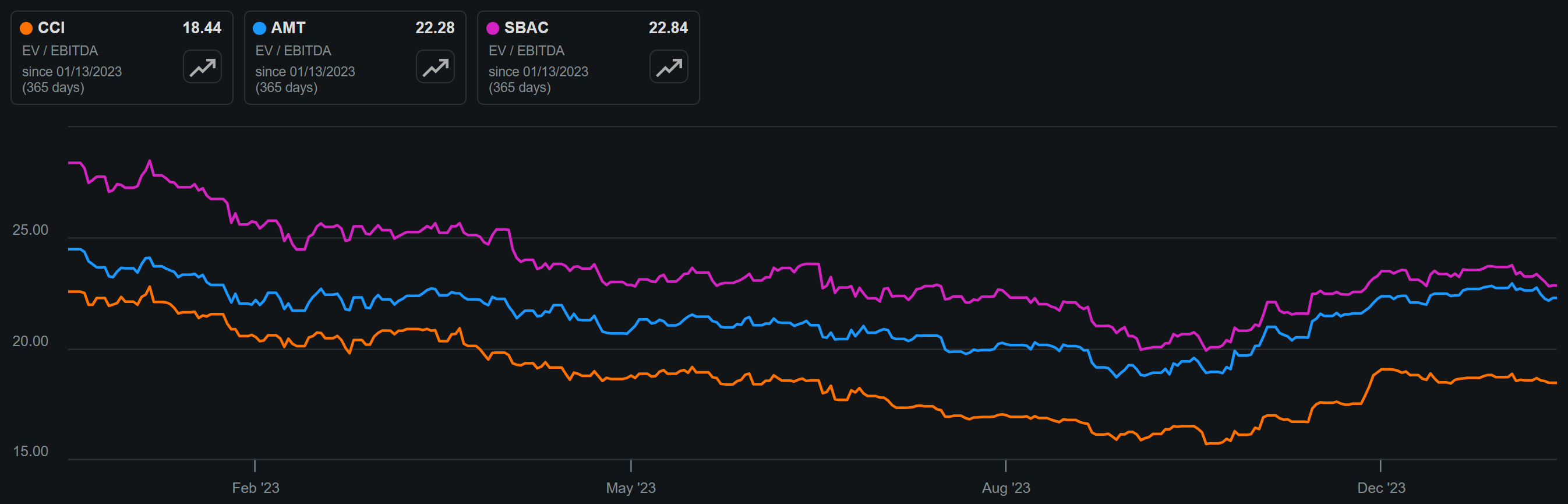

As shown below, CCI also trades at a substantial discount to its peers AMT and SBAC, with an EV/EBITDA of 18.4 while giving a higher dividend yield than its two peers.

{kind=link}

Investor Takeaway

Despite the recent slowdown in leasing activity, Crown Castle remains a long-term growth story with its strong portfolio of assets and focus on growing small cells. While there are risks to consider such as Elliot's involvement and elevated leverage ratio, I believe that CCI's long-term potential for AFFO growth and dividend income make it an attractive investment opportunity. Additionally, its current discount to its peers and historical valuation metrics further support its value proposition.

As 5G deployment continues to ramp up and the demand for wireless infrastructure increases, I believe that CCI will continue to see strong growth in the years ahead. While I remain bullish on CCI, I am downgrading it from a 'Strong Buy' to a 'Buy' based on the share price having made up for its substantial losses since the last time I visited the stock.

For further details see:

Crown Castle: Good Time To Pick Up This High Quality Player