CCI - Crown Castle: I'm Stocking Up At These Prices

2023-10-24 08:10:00 ET

Summary

- Crown Castle Inc. is a compelling value for income investors who are focused on sectors and companies with low risk over the long run.

- It has a wide-ranging presence in all major US markets and is seeing accelerating growth in its small cell deployments.

- Despite near-term challenges, Crown Castle Inc. is well-positioned for long-term growth, with a solid dividend yield and strong revenue visibility.

There is a common misconception that you have to take on outsized risk to get outsized returns. Perhaps that’s what drives some to buy into highly leveraged income vehicles in search of high yield. On the contrary, I believe a better approach is to invest in sectors and companies with a high degree of uncertainty but low risk over the long-run

This brings me to Crown Castle Inc. ( CCI ), which I last covered here back in August with a Strong Buy rating, noting its undervaluation and strong income stream. In this article, I revisit the stock and discuss why it remans a compelling value for income investors so let’s get dive in!

Why CCI?

Crown Castle Inc. is one of the two largest cell tower owners in the U.S., and unlike peer American Tower ( AMT ), CCI is focused solely on the U.S., thereby removing currency risk from the equation. At present, CCI operates and leases over 40K cell towers covering 85K miles of fiber supporting small cells and fiber across every major U.S. market.

Investors familiar with CCI know that it hasn’t been easy holding onto the stock over the past 12 months, as the share price has declined by 29% during this time, and this includes the 17% drop in price since my last piece.

One of the contributing factors to the decline is the expectation of a higher for longer interest rate environment, as inflation is proving more difficult than expected for the Federal Reserve to tame. For REITs like CCI, this means higher interest expense when it comes to debt refinancing down the line, with the Fed not expected to cut rates anytime soon.

The market also may not have liked the 4.4% organic cash tower leasing growth, which was lower than previous years due to lower spend by top customers like AT&T ( T ), Verizon ( VZ ), and T-Mobile ( TMUS ). However, lower capital investment and higher free cash flow this year was something that was well-communicated by the CEOs of the major telcos earlier this year.

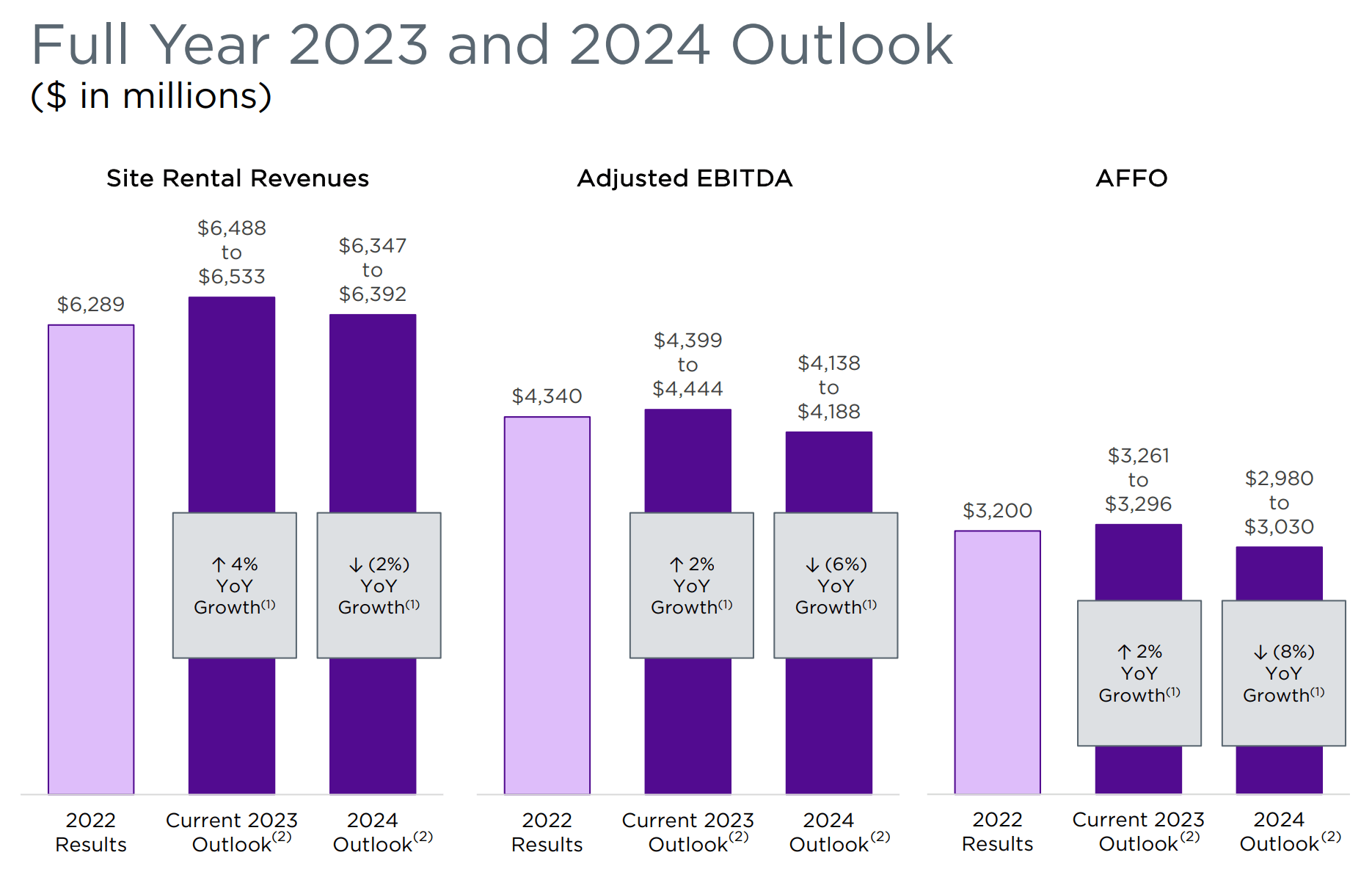

Other near-term challenges include the impact of Sprint-related churn (since it was acquired by T-Mobile), and management expects the AFFO/share trough to happen during the first half of 2024 before returning to growth in AFFO in the second half of next year and beyond. As shown below, AFFO is expected to decline by 8% next year after rising by 2% this year, driven by lower site revenue and higher interest expense.

{kind=link}

Notably, I wouldn’t expect any meaningful dividend raises between now and 2025, considering that dividend-to-AFFO payout ratio estimate of 91%, based on the midpoint of management’s 2023 AFFO/share estimate of $6.91. Despite the near-term headwinds from lower customer spend, I see the long-term growth thesis as being intact, as management expects to maintain its $6.26 per share dividend resume bottom-line and dividend growth beyond 2025.

CCI is already taking steps to secure the company for near-term headwinds and position it for the long-term, by having achieved $105 million of annual run-rate savings driven in part by workforce reduction and organizational efficiencies. CCI is also positioned for long-term top-line growth as it plans on deploying $1.2 billion of discretionary capital without the need to issue equity through 2024

Moreover, CCI is well positioned for future densification buildouts by its customers no matter where they plan deploy equipment, given CCI’s already wide-encompassing presents in major markets. The market may also be overlooking CCI’s potential with small cells, of which it already has 115K on air and under contract, and management expects them to see 13% organic revenue growth next year.

Small cells are discreet, fiber-connected antennas, usually located on existing structures like utility poles, and work in conjunction with CCI’s tower infrastructure to provide greater wireless coverage and capacity. This strategy was elaborated upon during the recent earnings call :

In 2024, we expect to deploy a record 14,000 small cell nodes. Our ability to capture the accelerating growth in small cell demand is driven by the assets and core capabilities that we have built as the largest operator of shared infrastructure in the United States. Our 85,000 route miles of fiber include high strand counts in heavily populated areas where the density of data demand is the highest, which makes them the most desirable locations for small cell deployments.

Risks to CCI include a tighter dividend coverage than I would like in the near term, leaving less retained funds for capital expenditures. This means that CCI is expected to go over its target net debt to EBITDA ratio of 5x next year to achieve its growth spending plan. This risk is mitigated by management taking steps in since 2015 to extend its weighted average debt maturity from 5 to 8 years, and percentage of fixed rate debt from 68% to 86%, thereby buffering some of the impact from higher rates in the current environment.

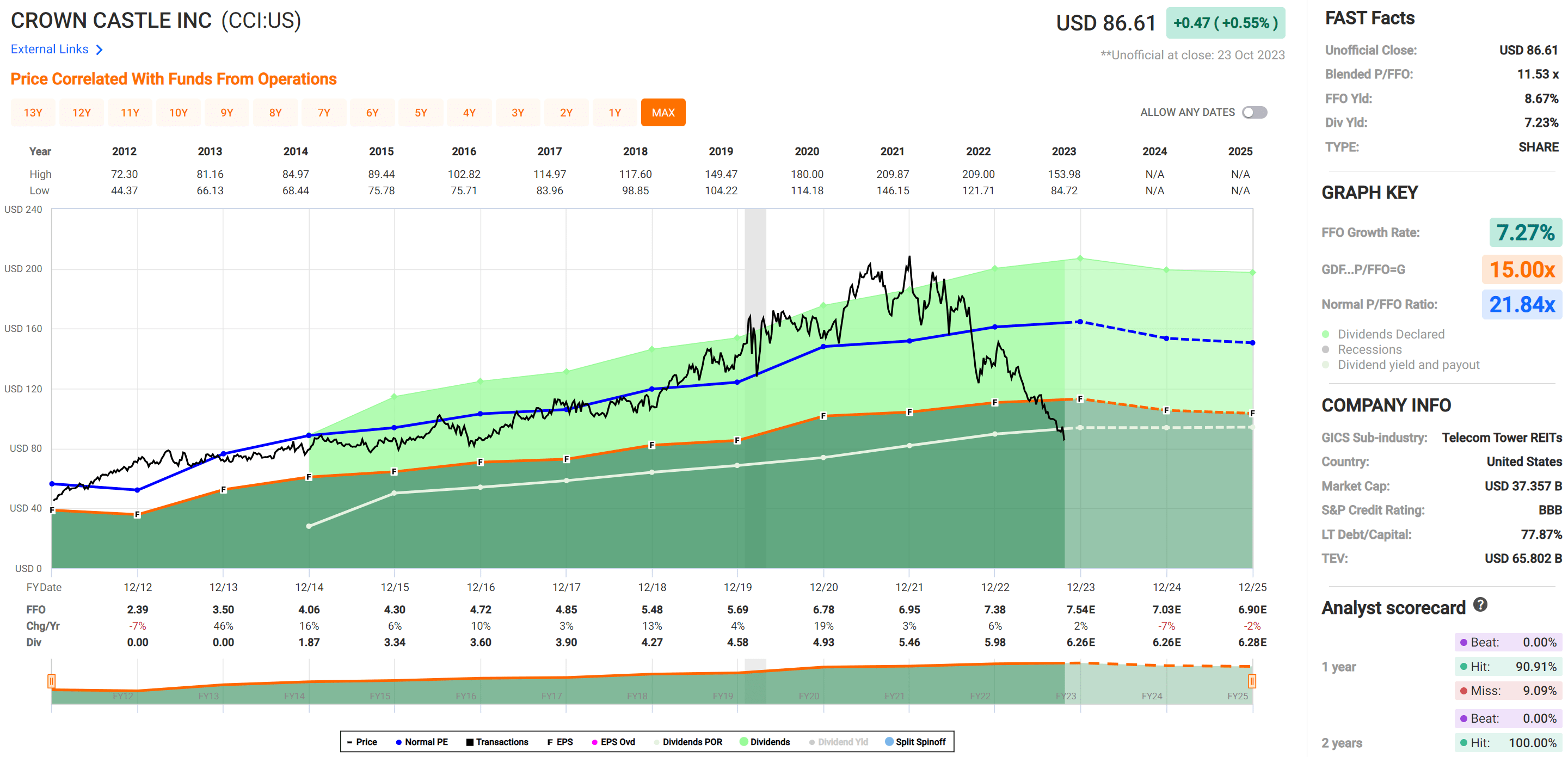

Turning to valuation, CCI is currently is solid value territory with a 7.2% dividend yield and forward P/FFO of 11.7, sitting far below its normal P/FFO of 21.8, as shown below.

{kind=link}

Based on my NPV analysis below, I arrive at a fair value estimate of $123. This is based on a modest 5% annual growth rate over the next 15 years, which I believe is a fair period considering the durability of the business model. The model also factors in a 3.5% discount rate to account for near-term headwinds related to lower customer spend and higher interest rates. This discount rate is higher than the 2% inflation rate target by the Federal Reserve for the aforementioned reasons. The fair value is calculated based on the sum of the annual cash flows over the 15 year period with the 5% exponential growth and 3.5% exponential discounting factored into the equation.

NPV Analysis (Produced by Author)

{kind=link}

Investor Takeaway

While there are near-term headwinds facing CCI, the company is taking steps to position itself for long-term growth and remains a strong player in the wireless infrastructure market, especially considering its small cell strategy. With a solid dividend yield and strong revenue visibility, CCI offers investors an attractive investment opportunity at its current discounted valuation.

As such, I've taken the opportunity to add to my CCI position at current prices amidst market uncertainty. While I fully expect more volatility in the stock price in near-term with potential for further downside, I reiterate my 'Strong Buy' rating for long-term investors.

For further details see:

Crown Castle: I'm Stocking Up At These Prices