CCI - Crown Castle: Is This 5.5%-Yielding REIT A Buy Now?

2024-01-12 07:00:00 ET

Summary

- REITs can be an excellent way to generate sustainable passive income.

- Crown Castle's churn headwinds should dissipate soon and the company's change in direction could get it back on track.

- The infrastructure REIT maintains an investment-grade credit rating from S&P.

- Shares of Crown Castle may be undervalued by 14%.

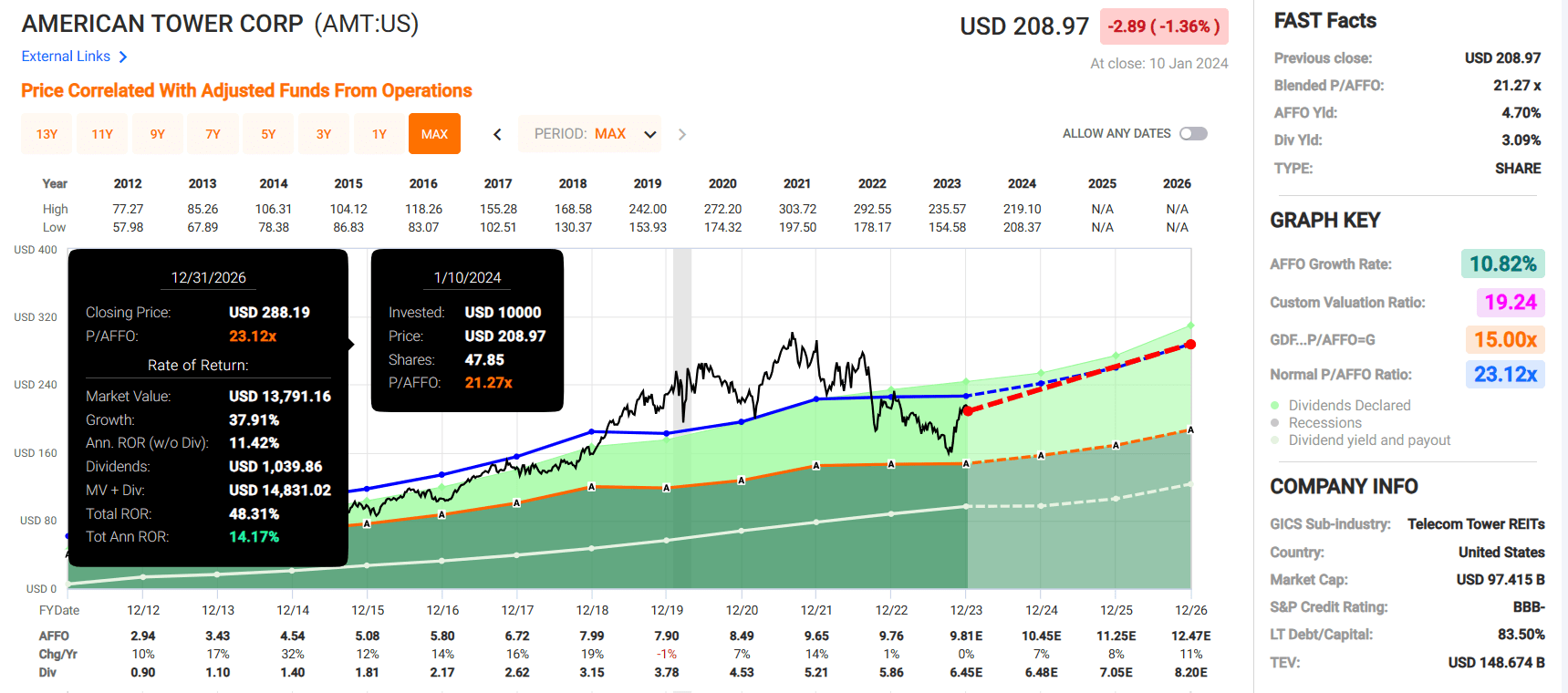

- I view American Tower as a better alternative for further investment at this time.

As a dividend-oriented investor, REITs are an important part of my portfolio. Overall, I own 12 REITs within my portfolio, and they contribute 13.8% of my overall dividend income.

It shouldn't come as a surprise that REITs are prominently featured in my portfolio. After all, they are required by law to pay at least 90% of their taxable income to shareholders to maintain their legal classification as a REIT. That often means they offer an enticing income with some growth to boot.

One REIT that is part of my portfolio is Crown Castle ( CCI ), which comprises 1.1% of my annual dividend income. But would I consider adding to my portfolio now? For the first time since April 2022 , I will revisit the company's fundamentals and valuation to provide an answer to that question.

{kind=link}

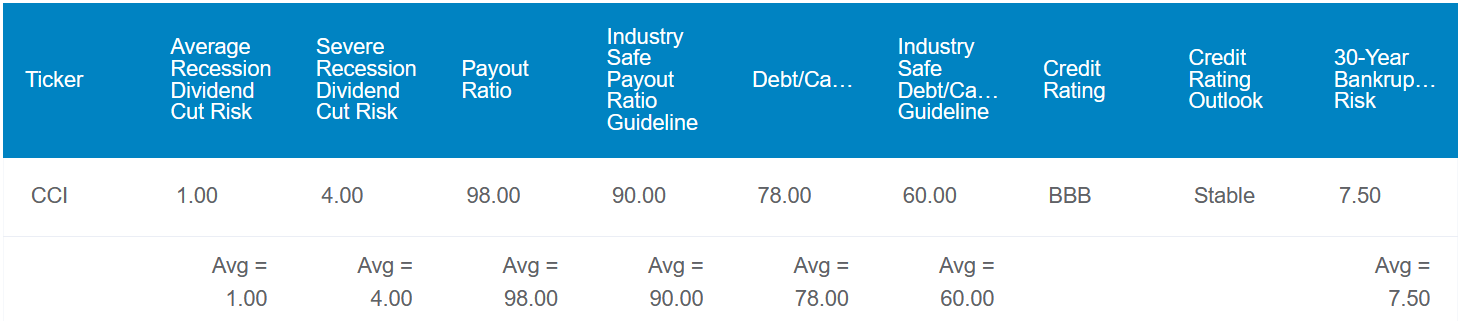

Crown Castle's 5.5% dividend yield comes in at nearly four times the 1.5% yield of the S&P 500 ( SP500 ).

The company's 98% payout ratio is elevated a bit beyond the 90% payout ratio that rating agencies like to see from REITs. As is the 78% debt-to-capital ratio relative to the preference of 60% or below from rating agencies.

However, Crown Castle has earned a BBB credit rating from S&P on a stable outlook. That puts the REIT at a non-zero but still reasonable 7.5% probability of defaulting on debt in the next 30 years.

For these reasons, the risk of Crown Castle cutting its dividend in the next average recession is just 1%. In a severe recession, that chance shoots up to 4%.

Whether the company ends up cutting its dividend in the foreseeable future will depend on the ability to execute a turnaround.

{kind=link}

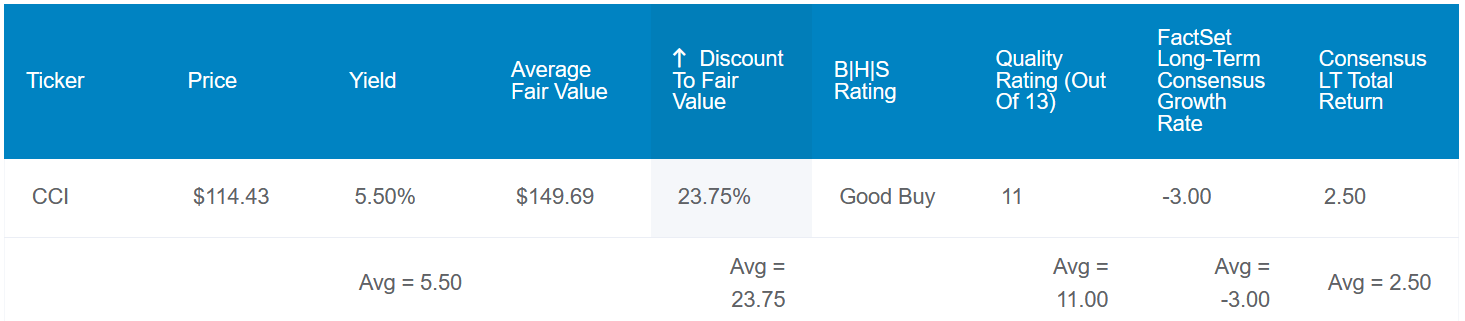

Crown Castle's valuation appears to be at least somewhat attractive at this time. Using historical dividend yield and P/AFFO, its shares could be worth $150 each. Now, I would split the difference between the current $112 share price and the $150 fair value estimate for my estimate of approximately $130. That's because, until the turnaround is complete, I don't believe the company is worthy of the valuation multiples that it fetched in the past.

If Crown Castle grows as anticipated and returns to my fair value in the next 10 years, here are the total returns that it could generate (assuming mixed success with the turnaround):

- 5.5% yield - 3% FactSet Research annual growth consensus + 1.5% annual valuation multiple expansion = 4% annual total return potential or a 48% 10-year cumulative total return versus the 8.6% annual total return potential of the S&P or a 128% 10-year cumulative total return

Churn Headwinds Will Fade And The Right Moves Are (Starting To) Be Made

{kind=link}

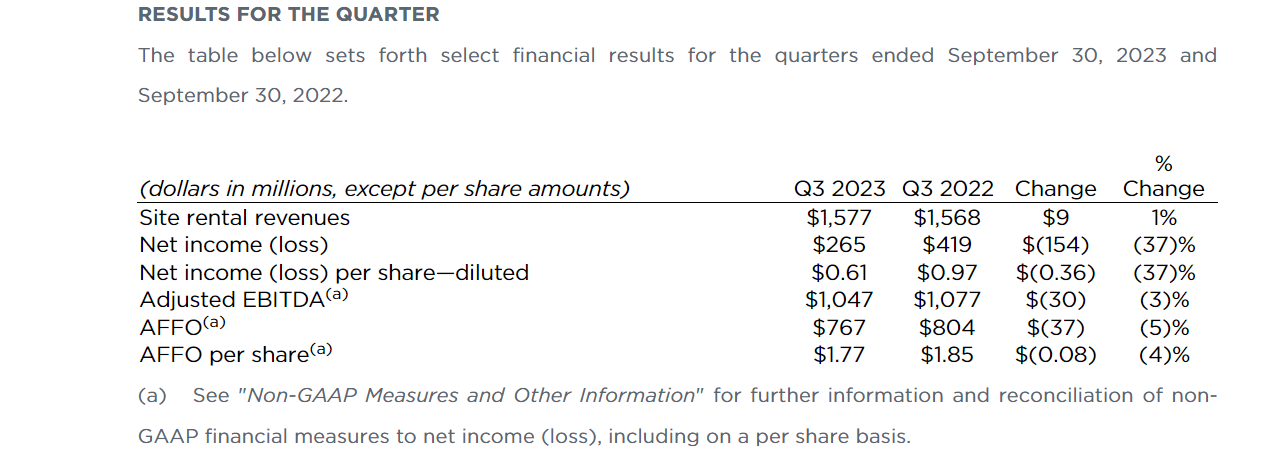

Crown Castle's total revenue dipped 4.6% year-over-year to $1.7 billion in the third quarter ended September 30, which missed the analyst consensus by $20 million . Site rental revenue edged 0.6% higher over the year-ago period to $1.6 billion during the quarter. This was driven by $53 million in additional organic contributions to site rental billings, but was mostly offset by Sprint churn due to its merger with T-Mobile ( TMUS ).

Crown Castle's increased site rental revenue was more than countered by a 49.4% decline in services and other revenue to $90 million for the quarter. This was driven by the announcement of a 15% reduction in the company's total employee headcount back in July (page 18 of 56 of the most recent 10-Q filing ).

Crown Castle's AFFO per share dipped by 4.3% year-over-year to $1.77 in the third quarter. That came up $0.03 shy of the analyst consensus. A lower revenue base and higher interest expenses due to elevated interest rates were to blame for AFFO per share contracting faster than revenue during the quarter.

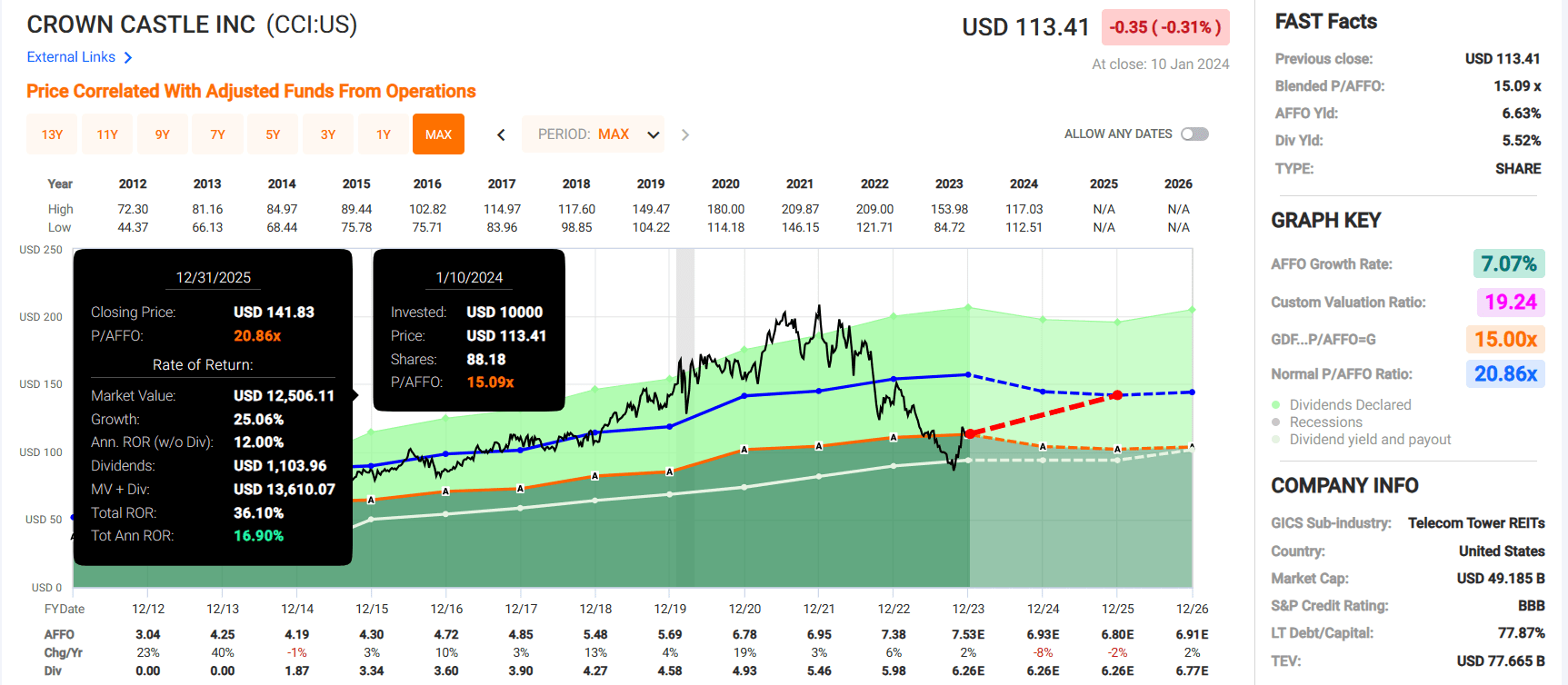

Based on current guidance for 2024, Crown Castle predicts it will generate $6.91 in midpoint AFFO per share. From the current $7.54 midpoint for 2023, that would represent an 8.4% decline. Two factors primarily play a role in this dip in AFFO per share. For one, an $85 million to $130 million uptick in interest expenses for 2024 will weigh on AFFO per share. Secondly, Crown Castle expects to receive $165 million less in rent from Sprint in 2024 due to the latter eliminating redundancies in its network following the merger with T-Mobile.

There is good news if one can look out to the horizon. According to opening remarks from outgoing CEO Jay Brown during the Q3 2023 earnings call , the impact of Sprint churn should be done as the first half of 2024 closes. Also, Elliott Investment Management's $2 billion stake in Crown Castle and the resulting review of its fiber business could take the company in a new and improved direction to unlock shareholder value .

Little To No Dividend Growth Likely For The Next Few Years

Crown Castle's quarterly dividend per share has surged 39.1% higher in the last five years to the current rate of $1.565 . Of course, past dividend growth often has minimal bearing on future dividend growth potential. This is especially the case when a company's payout ratio is on the high end and it's executing a turnaround like Crown Castle.

As much as a frozen dividend pains me, the company appears to be taking the responsible route. CEO Jay Brown noted in his opening remarks during the Q3 2023 earnings call that the dividend will be maintained in 2024. Compared to $6.26 in dividends per share that will likely be paid during the year, Crown Castle's $6.91 AFFO per share midpoint would represent a 90.6% AFFO payout ratio.

As the company works through the ongoing Sprint cancellations related to the latter's merger with T-Mobile and implements its turnaround, Crown Castle expects to resume dividend growth beyond 2025.

Risks To Consider

Crown Castle is a quality REIT, but it has risks that must be weighed before opening or adding to a position.

The completed merger of T-Mobile and Sprint in 2020 and the fallout from it (cancellations as the two eliminate redundant leases) is a reminder that telecom consolidation remains a risk. If more M&A activity occurs within the space, this could negatively impact Crown Castle. That's especially the case with its big three tenants comprising roughly three-quarters of site rental revenue in 2022 (page 4 of 144 of Crown Castle's 10-K filing ).

Another risk to Crown Castle is the potential that it ends up overbuilding its infrastructure. If this were to happen, the company's growth prospects could be diminished and the total returns for shareholders could further languish.

Crown Castle's debt load is also reasonably elevated. As of September 30, the company had $22.6 billion in debt. Compared to the $4.2 billion in adjusted EBITDA that it is guiding for in 2024, that's a debt-to-adjusted EBITDA ratio of around 5.4. If the company fails to right the ship and fundamentals deteriorate any further, such a significant debt load could become an issue. Fortunately, Crown Castle has upped its proportion of fixed rate debt from 68% in 2015 to 86% as of Sept. 30. The company's weighted average coupon remains low at 3.8%. Also, Crown Castle only has $2.1 billion in debt coming due between now and the end of 2025 ($800 million in 2024 and $1.3 billion in 2025 pr slide 18 of 19 of Crown Castle's November 2023 Investor Presentation ).

Summary: There Is A Better Option Right Now

{kind=link}

{kind=link}

Crown Castle isn't a bad REIT by any means. It just faces challenges that will take some time to work through, which will require patience. Thus, the FAST Graphs analyst consensus anticipates -8% AFFO per share growth in 2024 and -2% AFFO per share growth in 2025 from Crown Castle.

In a vacuum, now may not be a bad time to buy for those who have faith in the turnaround. But with American Tower ( AMT ) expected to deliver far superior AFFO per share growth without being in a turnaround, Crown Castle is a less attractive option in my opinion. That's why the former is 1.2% of my portfolio value while the latter is just 0.8%. It also explains my rationale for assigning a buy rating to American Tower while rating Crown Castle as merely a hold currently.

For further details see:

Crown Castle: Is This 5.5%-Yielding REIT A Buy Now?