CCI - Crown Castle: Small Cells Are An Opportunity

2023-04-25 10:32:31 ET

Summary

- CCI's small cell business is a nice growth differentiator.

- However, the company faces headwinds in 2025 from the T-Mobile-Sprint merger.

- The stock looks like a solid "Hold" at the moment.

Crown Castle's ( CCI ) small cell strategy sets it apart, but Sprint-related headwinds will impact growth starting in 2025.

Company Profile

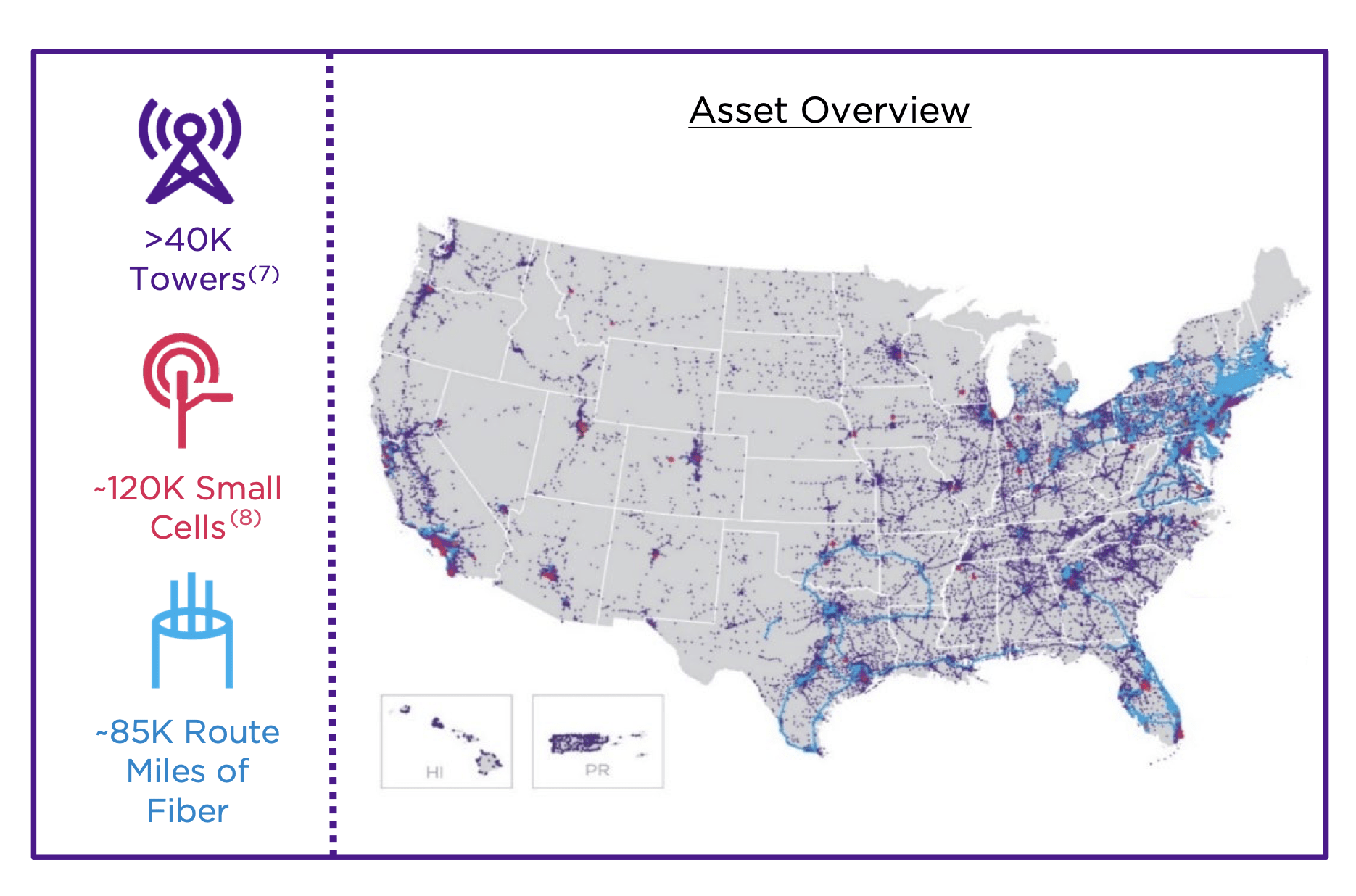

CCI is a real estate investment trust ((REIT)) that owns, operates, and leases shared communication infrastructure in the U.S. It has more than 40,000 cell towers, about 60,000 small cells on air and a similar number on backlog, and 85,000 route miles of fiber. The company operates in two segments: Towers and Fiber.

{kind=link}

Approximately 71% of its towers are located in the 100 largest U.S. basic trading areas (BRAs), while 56% are in the top 50. Approximately 40% of its gross profit comes from towers on land it owns and 60% for land it leases, subleases, manages, or licenses. Most of its small cell and fiber assets are located in major metropolitan markets.

Approximately 69% of its 2022 revenue came from its Towers segment, and 31% from its Fiber segment. AT&T ( T ), Verizon Wireless, and T-Mobile ( TMUS ) accounted for about 75% of its site rental income. Its tenant contracts had a weighted-average remaining life of about six years.

Opportunities and Risks

Similar to American Tower ( AMT ), which I wrote about recently , CCI's business also has a lot of visibility with long-term, non-cancelable contracts. About 90% of its revenue in 2022 came from site rental revenue with fixed, non-cancelable terms, often with fixed or inflation based escalation clauses (generally about 3% annually). Its tower contracts are typically between 5-15 years, while fiber solution contracts range from 3-20 years. In addition, retention is very high, historically in the 98-99% range.

Like AMT, CCI is also greatly benefiting from increases in mobile data usage and the move to higher speeds through new technology standards such as 5G. The big 3 U.S. wireless providers continue to pour CapEx into what is essentially a mobile data arms race, which nicely benefits a company like CCI.

On its Q1 earnings call , CEO Jay Brown said:

"The need for substantial investment in networks has persisted from 2G through 5G. Since the early days of 4G to support mobile data demand that has increased by a factor of 62x since 2011. While industry-wide capital may vary year-to-year, particularly as new spectrum is acquired, wireless capital spending throughout the deployment of 4G was relatively consistent, averaging approximately $30 billion per year. During this time, priorities shifted back and forth between acquiring new spectrum and deploying that spectrum with the addition of new cell sites, with both being essential for our customers to keep up, with the increasing data demand. With our shared infrastructure model, we have helped our customers to maximize the benefits of these investments by lowering the cost of deployment. This value proposition has allowed us to generate significant growth in our tower's business throughout the 4G rollout, and we added to that growth with investment in small cells, which began to play a critical role in helping our customers keep up with the increasing demand in the later stages of 4G. Each new generation of wireless technology has provided expanded capacity for connectivity...

"As a result, we expect our customers' network and investment in the 5G era to exceed what they spent deploying 4G. Since we are still in the early innings of 5G, we believe these positive underlying demand trends will support our ability to sustain at least 5% organic tower revenue growth, and continue the acceleration in our small cell business. In the first 2 years of 5G deployment at scale, we led the industry with organic tower growth of greater than 6%. Additionally, we believe our current small cell backlog provides line of sight into doubling our on-air nodes over the next several years, which we expect will drive double-digit small cell revenue growth beginning in 2024."

At a conference in March, the company noted that wireless operators still haven't really gotten to the densification stage of the 5G cycle. Meanwhile, only 50% of its tower have mid-band spectrum infrastructure on them. This is similar to AMT, and shows the continued long runway it has with the steady 5G buildout.

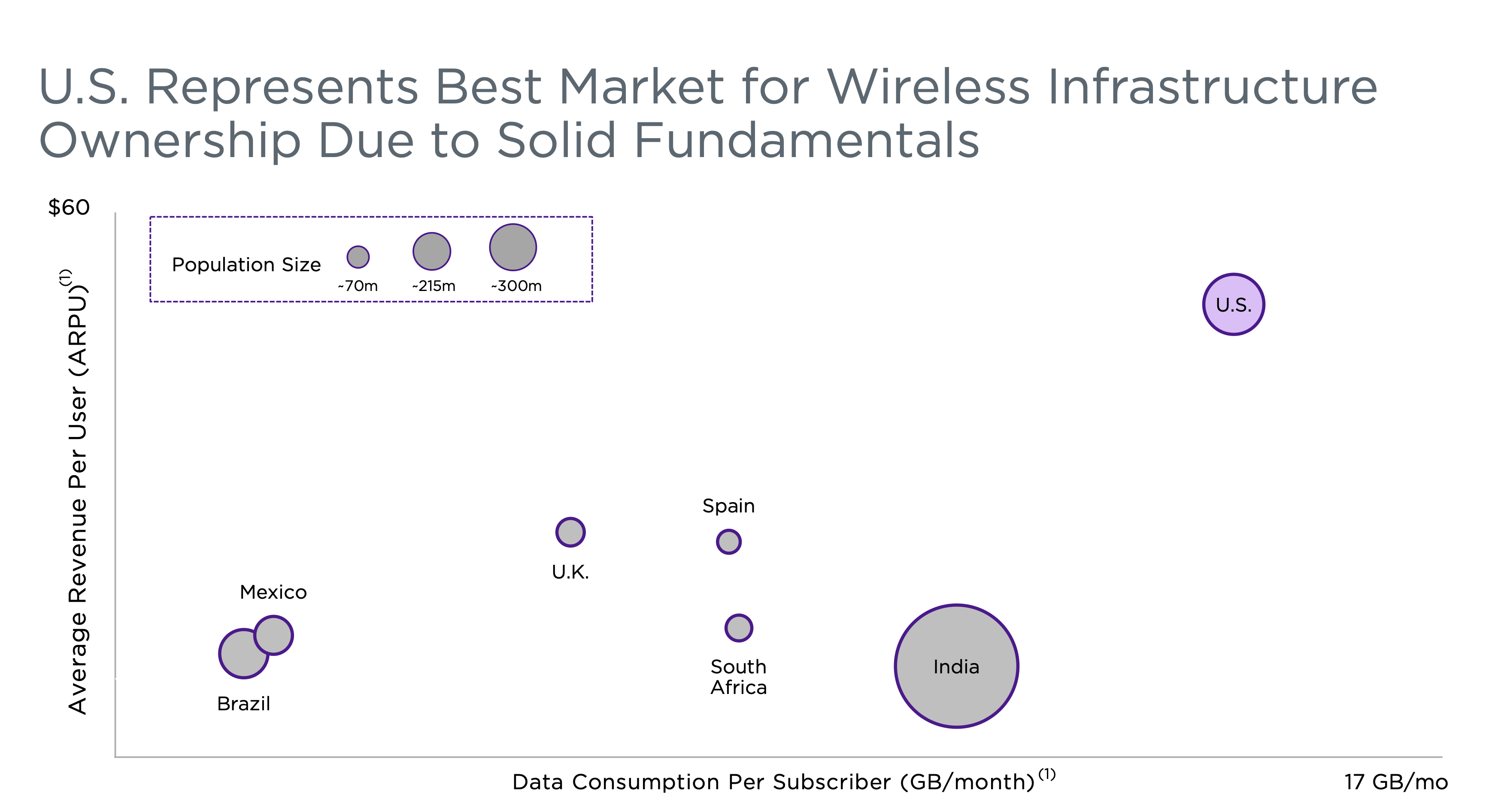

Unlike AMT, CCI primarily focuses on the U.S. As noted earlier, AMT has run into some churn and customer payments in international markets. The company believes the U.S. is the best market to be in because U.S. spends the most of its wireless network than any other country.

{kind=link}

Another way in which CCI differs from AMT is with its small cell business. Small cells are much smaller than towers, standing around 25 feet tall versus between 50-300 feet with towers. They are meant to be situated in places that towers can't reach and fill the gaps where towers are not capable of delivering all the wireless demand. Towers cannot be too close to each other, or they will interfere with each other, so small cells help pick up the load.

Currently, small cells is the larger revenue growth driver for CCI. The company isn't currently building any new tower, just leasing them up. For small cells, it has about 60,000 built and then 60,000 in its backlog. It takes about 18 to 36 months from the time a contract is signed to get it up and running due to permitting and zoning, as they are generally built in the right of way owned by the municipalities. The company has a nice first mover advantage in this area, and is the leader in the small cell space.

With its visible business model and small cell growth, CCI is looking to grow its dividend by 7-8% a year. The stock currently yields about 5%, and it's grown its dividend 9 years straight.

Like other tower operators, CCI carries a fair amount of debt. With 85% of its $22 billion in net debt is fixed, it has $3.3 billion in variable debt and commercial paper, where higher interest rates have increased its interest payments. Its leverage is about 5x.

Another headwind the company will face is with the merger of T-Mobile and Sprint. Currently, CCI is getting a benefit from termination payments, but it will see about $200 million in Sprint tower rent churn off in 2025, as well as $45 million in small cell churn and $30 million in fiber churn over the next 3 years.

Like most telecom service and equipment companies, CCI faces spending cycle risk. Telecom spending is in a solid upcycle, but it isn't always a straight line-up, and the 3 big providers sometimes will cut back. Its largest customer, T-Mobile, represented 38% of revenue last year, so it also has some pretty big customer concentration risk as well. AT&T and Verizon Wireless were both 18% customers.

Valuation

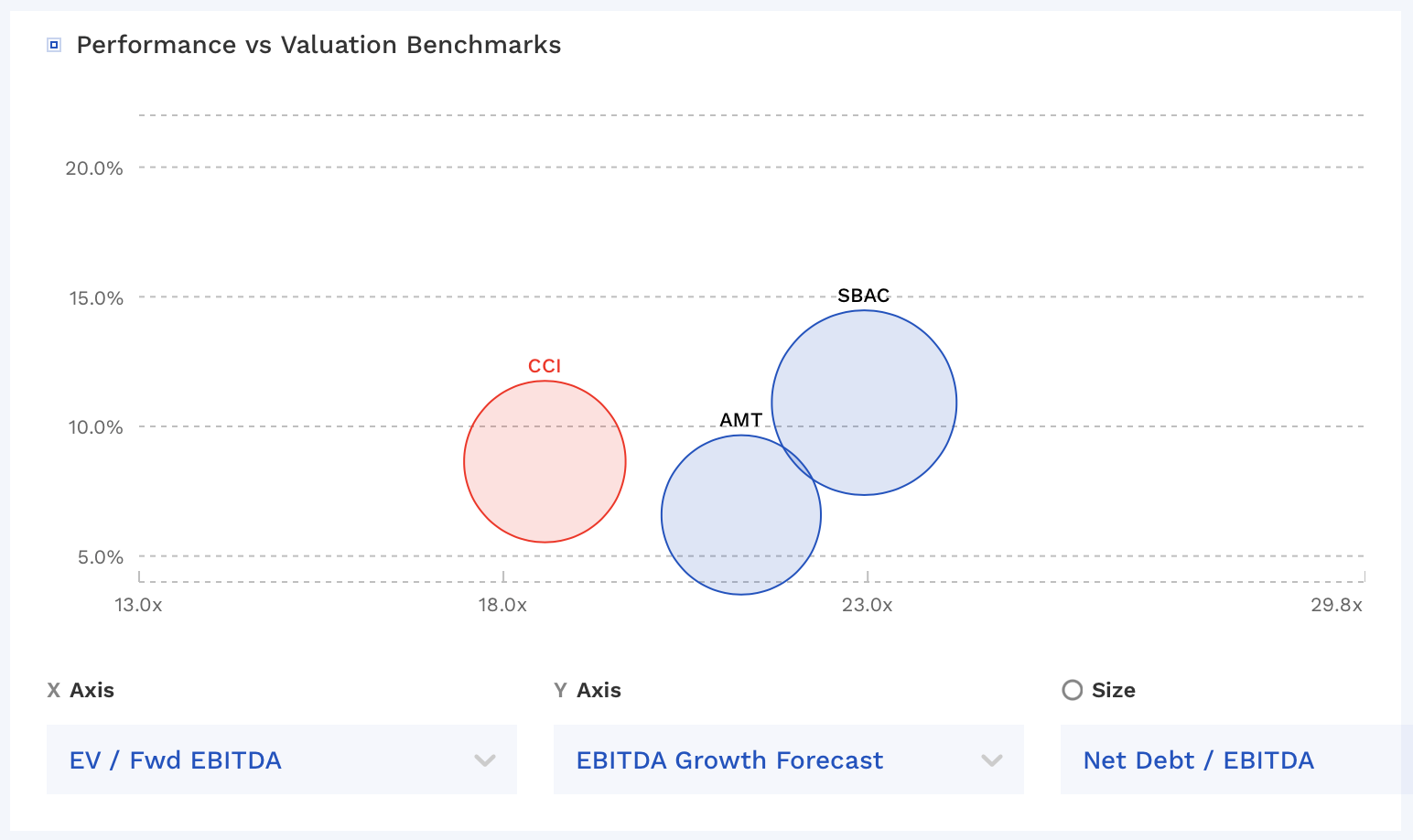

CCI trades at 18.6x EBITDA based on 2023 analyst estimates of $4.47 billion. Based on the 2024 consensus of $4.4 billion, the stock trades at an 18.9x multiple.

Based on an AFFO forecast of $7.64, it trades at a 16.6x price-to-AFFO ratio.

The stock trades at the lowest valuation of its two closest peers, AMT and SBA Communications ( SBAC ).

CCI Valuation Vs Peers (FinBox)

{kind=link}

Conclusion

Overall, I like CCI's focus primarily on the U.S. market and its foray into the faster-growing small cell market. However, the company has more Sprint-related headwinds ahead of it compared to the other tower operators. At the time of the merger, CCI was getting about 20% of its revenue from T-Mobile and 13% from Sprint, and last year the combined company was about 38% as it got cancellation payments.

CCI is the cheapest of the tower operators, as its growth will be limited in a few years due to the Sprint headwinds. That said, the stock still is not cheap. I think with the current yield and planned dividend growth, however, that the stock is a solid "Hold." I'm just not a new buyer at these levels.

For further details see:

Crown Castle: Small Cells Are An Opportunity