CCI - Crown Castle: Take Advantage Of The Market's Short-Termism

2023-04-24 08:30:00 ET

Summary

- CCI suffers from two headwinds right now: Sprint lease cancellations and rising interest expenses from some floating rate debt.

- I argue that both of these headwinds are temporary rather than permanent.

- Mobile data demand is projected to continue growing at a 21% CAGR through at least 2028, and wireless carriers will need to continue steady infrastructure capex to meet that demand.

- If you look past the market's short-term pessimism about CCI, I think you will see a bright long-term future.

Thesis: Headwinds To Growth Are Temporary

Crown Castle ( CCI ) is a telecommunications infrastructure real estate investment trust ("REIT") focused entirely on the United States market, which the company believes to offer the most safety and highest risk-adjusted returns in the world.

Until recently, CCI has also been one of the most reliable and fastest growing compounders in the REIT space.

What happened? Why has CCI suddenly fallen headlong over a cliff?

CCI is facing two strong headwinds at the moment that are weighing down growth:

- Cancellations of certain leases to Sprint because of the carrier's merger with T-Mobile ( TMUS ) and the drop-off of lease cancellation fees after 2025

- Rising interest expenses from CCI's 15% of total debt with variable rates

The market seems to be valuing CCI as if these two headwinds will be permanent, and that AFFO per share and dividend growth will never return to management's target of 7-8% per year. I believe the market is wrong. The bond market is pricing in multiple Fed rate cuts by next year, which (if materialized) will ease the interest rate headwind. And CCI is investing heavily in small cells and fiber to offset the Sprint lease cancellations taking effect over the next few years.

Right now, CCI is valued at an AFFO multiple of 16.5x. By contrast, CCI entered 2022 at an AFFO multiple slightly over 27x!

Management attests that CCI will be able to return to 7-8% annual growth after 2025, and I believe them. In what follows, I'll explain why.

Crown Castle: A Unique Compounder

CCI owns the most extensive network of cell towers, small cell nodes, and fiber lines in the US. This size and scale give it enormous competitive advantages. The cost and time investment that would be involved in trying to build a competing set of infrastructure would be prohibitively high.

CCI Q1 Presentation

As I explained in a recent article highlighting CCI among other undervalued blue-chip REITs, CCI has a uniquely attractive business model that allows it to add multiple "tenants" onto its infrastructure for little to no incremental cost, which pushes up its yields on invested capital over time.

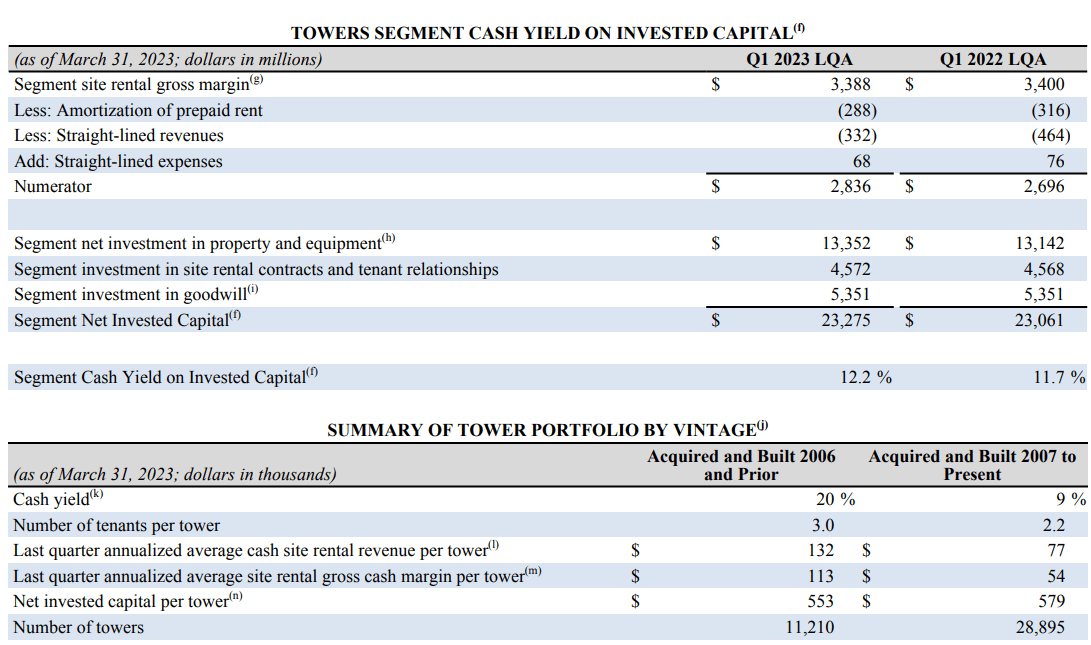

In the first quarter of this year, CCI had an average number of tenants per site of 2.4, which contributes to a weighted average cash yield on invested capital of 12.2% across the tower portfolio. That includes older towers with more tenants generating 20% yields on investment as well as more recently built or acquired towers with yields still in the high single digits.

{kind=link}

For the whole portfolio (towers, small cells, and fiber), the consolidated yield on invested capital actually fell year-over-year from Q1 2022's 9.9% to Q1 2023's 9.6%, but this is only because CCI is increasing the rollout of new small cell and fiber investments that start out with lower cash yields.

The organic tower revenue growth assumption of 5% annually comes almost evenly between contractual rent escalations and tenant densification (more tenants added to its towers).

Small cells (mini-cell towers placed in high-traffic areas that need additional capacity) and fiber work the same way. They start out with one tenant and initial yields in the mid-single digits, then returns gradually increase as new tenants are added and rent escalations accrue.

Towers typically feature annual rent bumps of 3%, while small cells and fiber feature rent bumps closer to 2%.

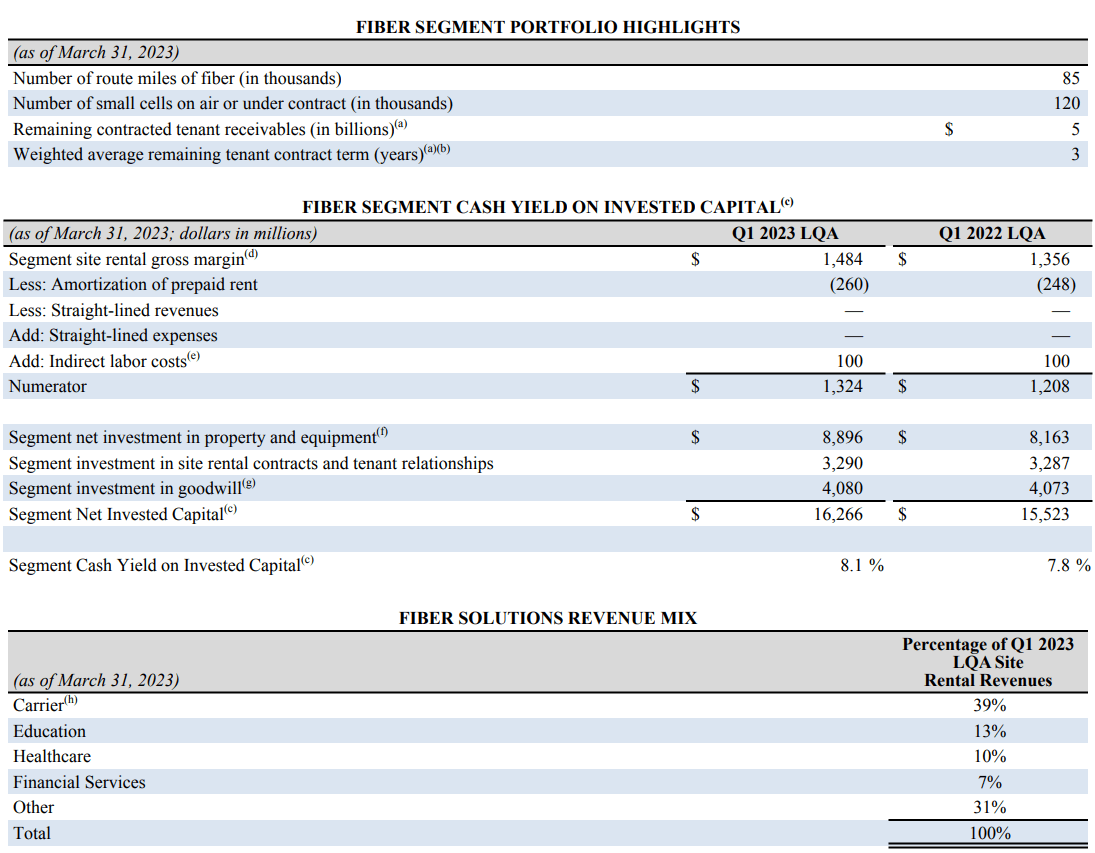

When it comes to CCI's fiber segment, it's useful to remember that CCI is not the user but the "landlord" or asset owner. Route miles of fiber are leased at a certain rent rate just like the towers and small cells, and in fact fiber is often used to put small cells on the air. Thus, as the small cell segment grows, so too should CCI's fiber segment.

And just as for the towers, CCI's fiber assets generate rising yields on invested capital over time, rising from 7.8% in Q1 2022 to 8.1% in Q1 2023.

{kind=link}

Due to the nature of most of CCI's fiber customer base, this segment is largely insulated from economic volatility. Most fiber revenue derives from tenants in the industries of telecommunications, education, healthcare, or government. This stability offsets the shorter weighted average remaining contract term of 3 years.

This business model not only results in higher yields on invested capital over time but also higher margins. In 2022, CCI's EBITDA margin came in at 69%, while its AFFO margin stood at 51%. Management's 2023 guidance assumes virtually identical margins.

CCI Q1 2023 Earnings Release

Management has stated that the combination of the Sprint lease cancellations should result in $350 million in revenue loss over the next few years. That's about $116.7 million per year spread across three years.

So, if not for the Sprint cancellations, CCI's site rental revenues would grow 5.4% this year instead of 3.5%, and AFFO per share growth would be about 5.5% this year instead of 3.4%.

In Q1 2023, organic contribution to rent billings came in at 6.8%, but adjusted for the Sprint cancellations, it was only 4.2%.

Could there be further consolidation in the wireless communications space that would lead to more lease cancellations?

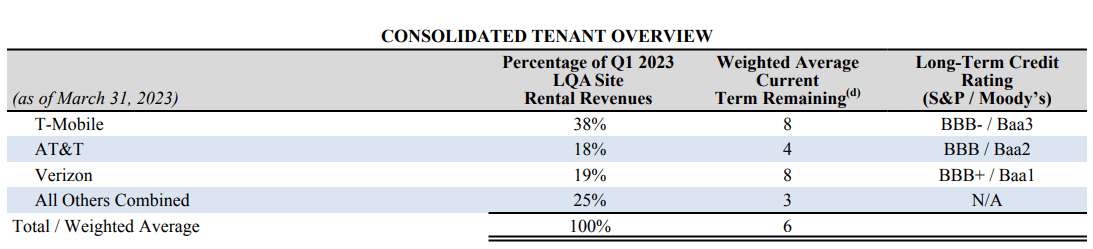

I find it highly unlikely. Already, wireless communications is effectively an oligopoly in the US, and 75% of CCI's revenue derives from these three major players.

{kind=link}

It seems unlikely that regulators would allow further consolidation in this space. Instead, there seems to be new entrants willing to pay for more space on CCI's towers, such as DISH Network ( DISH ).

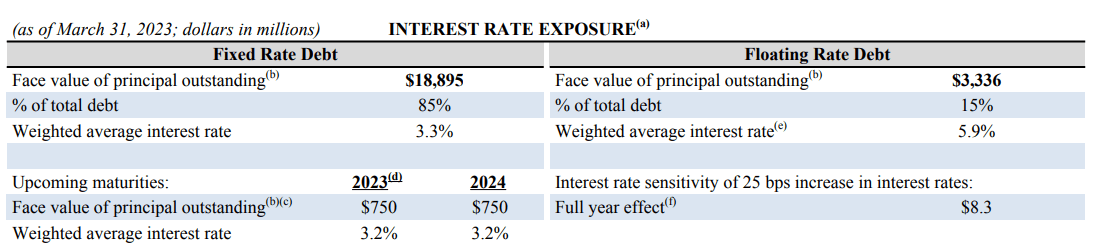

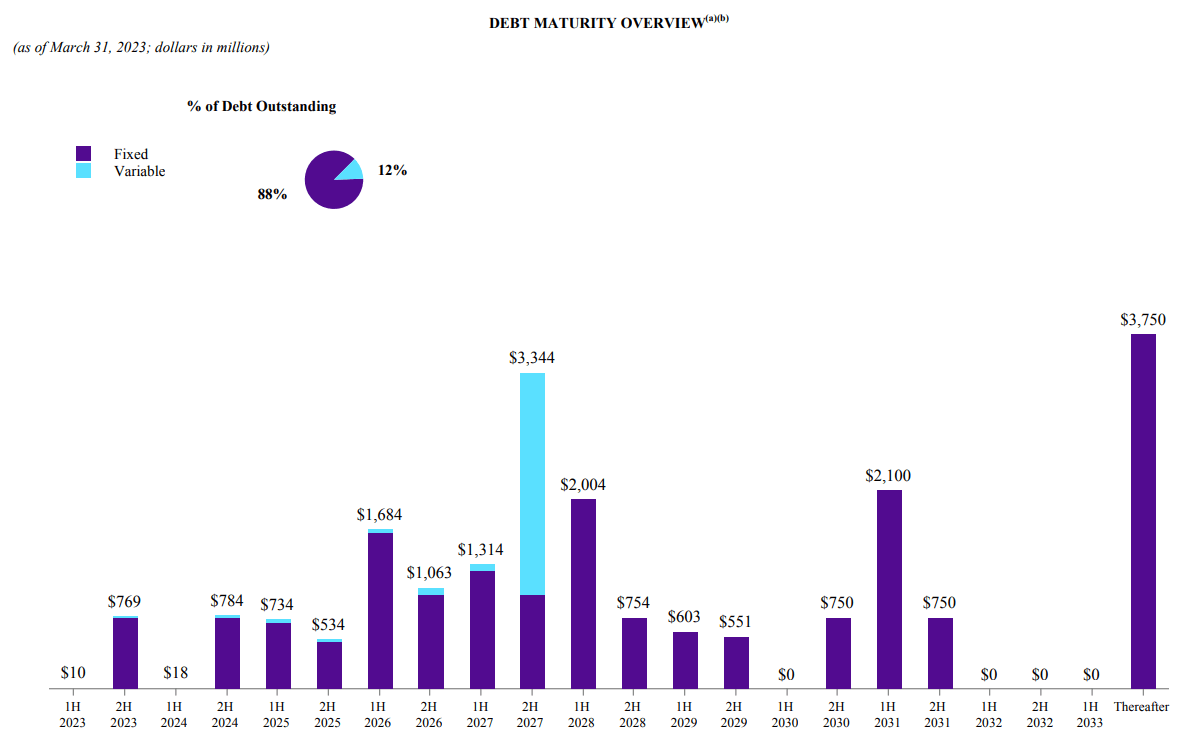

Rising interest rates are also a significant headwind right now. In Q1 2023, CCI's interest expenses soared 24% year-over-year and a little under 5% quarter-over-quarter. This is due to the 15% of floating rate debt the REIT carries on its balance sheet.

{kind=link}

As you can see above, CCI enjoys a weighted average interest rate of 3.3% on its fixed rate debt, which is undoubtedly a result of its strong, investment grade credit ratings of BBB/BBB+.

However, it does have $750 million in fixed rate debt maturing in each of 2023 and 2024, both of which feature 3.2% interest rates. Management will likely tap the floating rate credit facility to pay off the $750 million maturing this year (unless interest rates fall meaningfully soon), which means that the interest rate on that debt will jump from 3.2% to at least 5.9% - more if the Fed raises rates again this year.

This increase in interest expenses certainly seems to be the primary culprit of CCI's recent selloff. But keep in mind that:

- Debt maturities this year represent only 6.5% of CCI's total debt outstanding

- Total debt to enterprise value is quite low at only 28%

- Net debt to EBITDA is fairly low at 5.0x

- 2023's guidance for adjusted EBITDA covers estimated 2023 interest expenses at a 5.3x coverage ratio

- The market implicitly forecasts that the Fed will cut rates by next year

- The vast majority of CCI's debt remains fixed-rate, with no major refinancing hurdles until 2026

{kind=link}

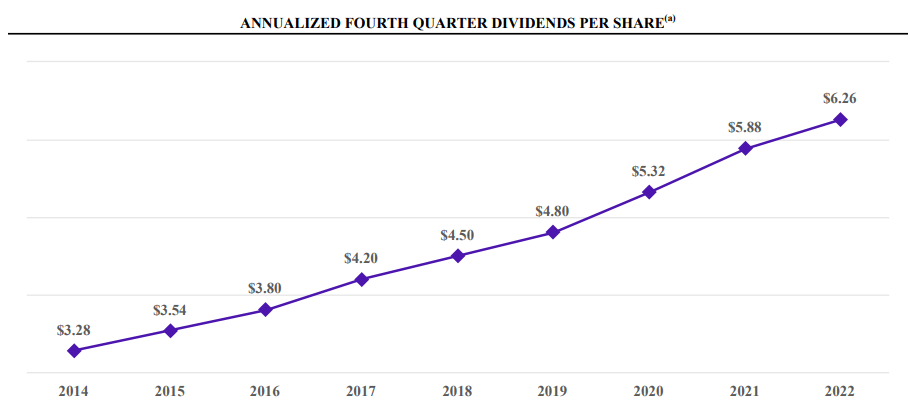

This interest rate and refinancing headwind goes a long way in explaining why management says CCI's dividend growth should be slower than its 7-8% long-term target range in the next few years.

But, again, it is important to keep this in perspective. Since the implementation of CCI's 7-8% annual dividend growth target in 2017, the REIT has averaged dividend growth meaningfully higher than that (9% per year on average).

{kind=link}

A few years of low single-digit dividend growth should not fool investors into thinking that CCI's era of high single-digit or low double-digit growth is over forever.

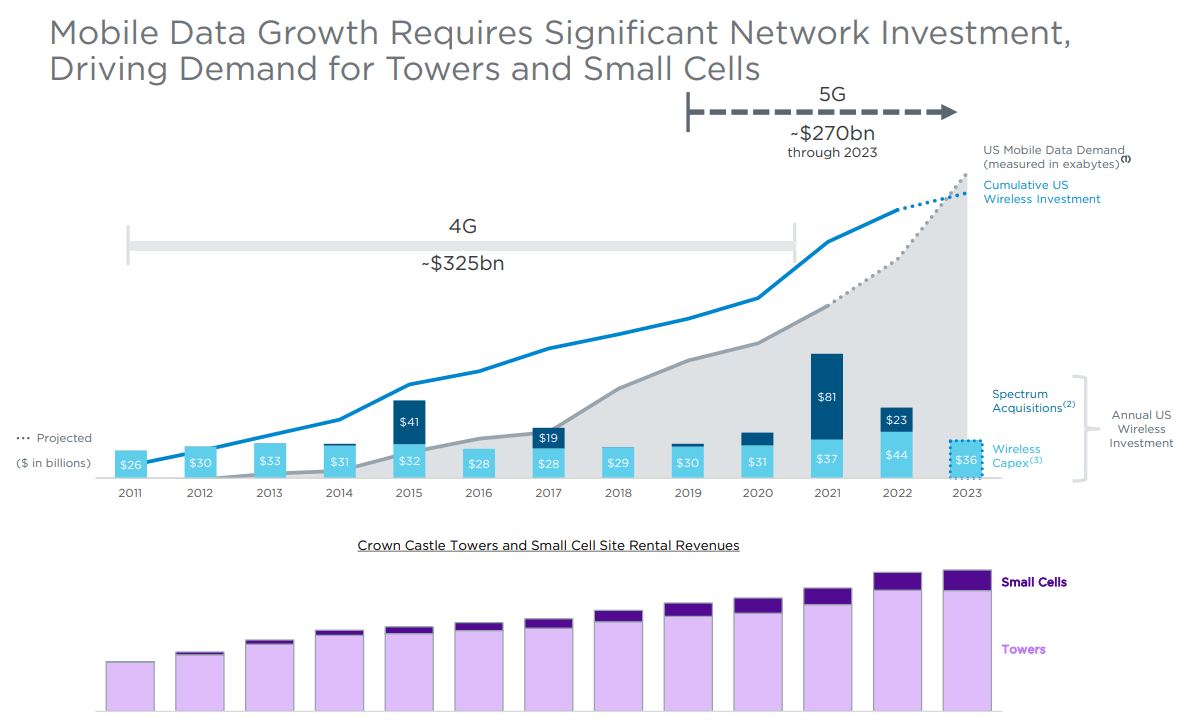

In 2021, mobile data demand was about 62 times higher than its level in 2011, and data usage continues to increase at a rapid rate.

{kind=link}

It would be helpful here to quote CEO Jay Brown from the Q1 2023 earnings conference call at length (bolded text is done by me):

Growth in our business has consistently been driven by our customers investing in their networks with the deployment of more spectrum and cell sites to keep pace with the rapid growth and mobile data demand. The need for substantial investment in networks has persisted from 2G through 5G.

... While industry-wide capital may vary year-to-year, particularly as new spectrum is acquired, wireless capital spending throughout the deployment of 4G was relatively consistent, averaging approximately $30 billion per year.

... Each new generation of wireless technology has provided expanded capacity for connectivity and over time, it also created a platform for innovation that expanded how we use and rely on our mobile devices, driving ever-increasing demand for data and connectivity . As a result, we expect our customers’ network and investment in the 5G era to exceed what they spent deploying 4G. Since we are still in the early innings of 5G, we believe these positive underlying demand trends will support our ability to sustain at least 5% organic tower revenue growth and continued acceleration in our small cell business.

You might argue that the CEO of a tower infrastructure REIT is of course going to say bullish things about the REIT's core asset base. But, at the same time, given CCI's industry leadership in this space, the top executives of CCI also have the most expertise and insight into the future of their industry.

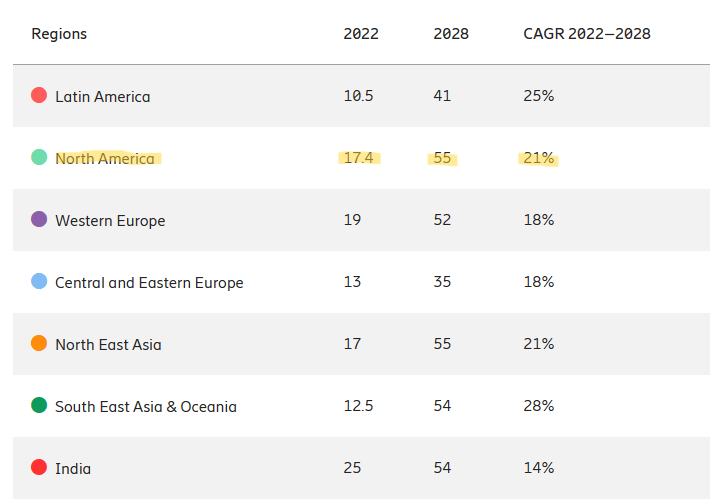

Swedish telecom giant Ericsson ( ERIC ) recently put out a forecast corroborating Brown's optimism. In Ericsson's view, North American mobile data demand should grow at a compound annual rate of 21% from 2022 through 2028, ending that year with among the highest GB per month at 55 (tied with Northeast Asia).

{kind=link}

Will carriers' infrastructure capex need to grow as fast as data usage? No, almost certainly not.

But will they be able to handle the significantly greater traffic without continuing to invest in upgrading their infrastructure networks? Again, no, almost certainly not.

As such, it seems safe to assume that CCI's infrastructure assets will continue to be necessary to the functioning of modern telecommunications systems for decades to come. And, indeed, these assets should only grow in value as carriers expand their number of locations, thereby increasing CCI's tenants-per-asset and yields on invested capital.

Bottom Line

I think the market has overreacted to temporary bad news about CCI. The market is either shortsighted in its inability to envision a world beyond 2025 that requires further wireless infrastructure spending, or it believes CCI will not be able to revive growth again even after the headwinds of Sprint cancellations and rising interest expenses are behind it.

In either case, I think the market is incorrect. I believe that the Fed will be cutting rates within a year or so, which will bring down interest expenses and allow CCI to term out its revolver debt by issuing new bonds, and I also believe that there are many more years of organic revenue growth to come from continued 5G capex.

As such, I continue to happily buy CCI and its 5% dividend yield. Assuming a few years of low single-digit dividend growth and then 7-8% annual dividend hikes thereafter, I think CCI will be able to deliver average dividend growth of around 6% over the next 10 years. That should render a 10-year yield-on-cost in the neighborhood of 9%.

That strikes me as an excellent dividend growth opportunity.

For further details see:

Crown Castle: Take Advantage Of The Market's Short-Termism