CCI - Crown Castle: The Market Is Still Not Getting This Right Buy The Dip

2023-07-20 10:20:11 ET

Summary

- Crown Castle, a leading infrastructure REIT, owns and leases critical communications assets in the US, playing a key role in the transition to 5G technology.

- The 4% fall in the company's shares after its 2Q23 results is a market overreaction and represents a buying opportunity, as the results were generally positive.

- I assign a BUY rating to Crown Castle stock, and any dip following Q2 results will represent an opportunity to add exposure at a steep discount to fair value.

Investment thesis

Crown Castle ( CCI ) is a leading infrastructure REIT that owns and leases critical communications assets in the United States. CCI owns more than 40.000 towers, 120.000 small cells, and 85.000 route miles of fiber networks. CCI plays a pivotal role in supporting the growing demand for mobile data and the transition to 5G technology, and its key strength lies in being one of the few providers supporting wireless carriers to expand their networks cost-effectively.

The company benefits from long-term contracts with $39 billion residual value in lease payments and a weighted average of 6 years, providing excellent cash-flow visibility. Towers represent about 70% of CCI’s site rental revenue. With tower costs largely fixed and only rising marginally, but rents usually including 3% escalators, Crown Castle has enjoyed increasing operating leverage and profit margins. The proliferation of smartphones, IoT devices, and data-hungry applications should give investors confidence that CCI infrastructure will be, for the foreseeable future, an integral part of the long-term mobile network, allowing the company to drive growth.

2Q23 results

The company fell over 4% post-market after releasing its 2nd quarter results. However, in my opinion, the reported results were quite good. The headline that probably freaked out longs (and unleashed the algo trading) was the AFFO guidance trim : CCI lowered its FY23 baseline range from $7.58-$7.68 to $7.50-$7.58, or a $0.09 cut at the midpoint from $7.63 to $7.54 (-1.2%). While the news is disappointing, the new guidance still represents a 2.1% increase over the FY22 result of $7.38, which leads me to believe that the market overreaction represents a buying opportunity.

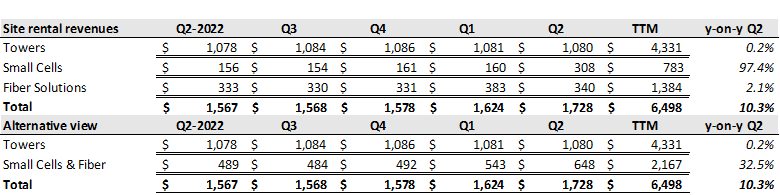

The remaining data points were, in fact, all quite positive. Q2 adjusted FFO of $2.05 was a beat against analyst estimate of $2.01 and an increase of almost 14% vs. the year-ago period ($1.8). AFFO continues to accelerate faster than revenues, as I like to see, as site rental revenue increased 10.3% to $1.73 billion in the quarter vs $1.57 billion in 2Q22.

{kind=link}

And Value For All

All segments reported positive y-on-y trends, although towers were essentially flat. CCI already explained that carriers have lowered their spending budget for the moment. Still, eventually, the upgrade cycle will inevitably resume as network densification continues to support data-hungry customers.

With CCI breaking down fiber solutions and small cells into two separate elements, the lion’s share of growth was taken by the small cells, with a robust 97.4% increase vs. 2022 and 92.5% sequentially. By looking at fiber and small cells separately, one could also be concerned by the $43 million q-on-q decline in fiber solutions. However, because the fiber optic network effectively enables CCI to install small cells, it is difficult to analyze the two independently. When the two were combined, the broader fiber segment growth was impressive at 32.5% vs. last year, somehow vindicating the management’s stance that fiber investments are conducive to growth for CCI.

Small cells deployment and growth

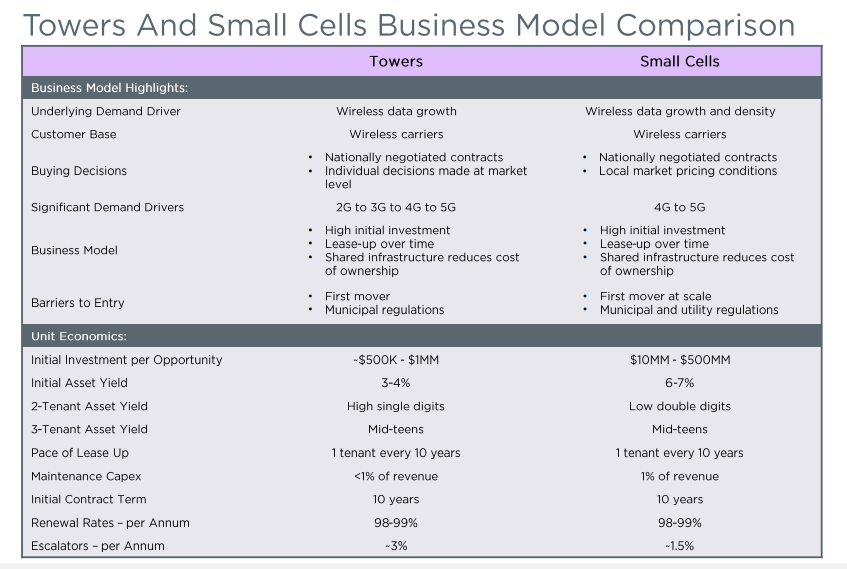

Crown Castle continues steadily deploying new small cell nodes, with 10,000 new cells forecasted for the year. Since 2020, CCI has essentially doubled the number of small cells deployed. With a backlog of new deployments still reaching 60.000, I think management has some visibility to support its claim that it can return to 7%-8% growth once the Sprint ( TMUS ) churn is completed by 2025.

According to CCI’s management, the economics of small cells are similar to towers, which means CCI’s leadership will be able to drive growth using the same business rulebook. Regarding small cells, initial asset yields are even higher than towers, although lower escalators compensate for that.

{kind=link}

CCI - Investor presentation May23

Debt profile

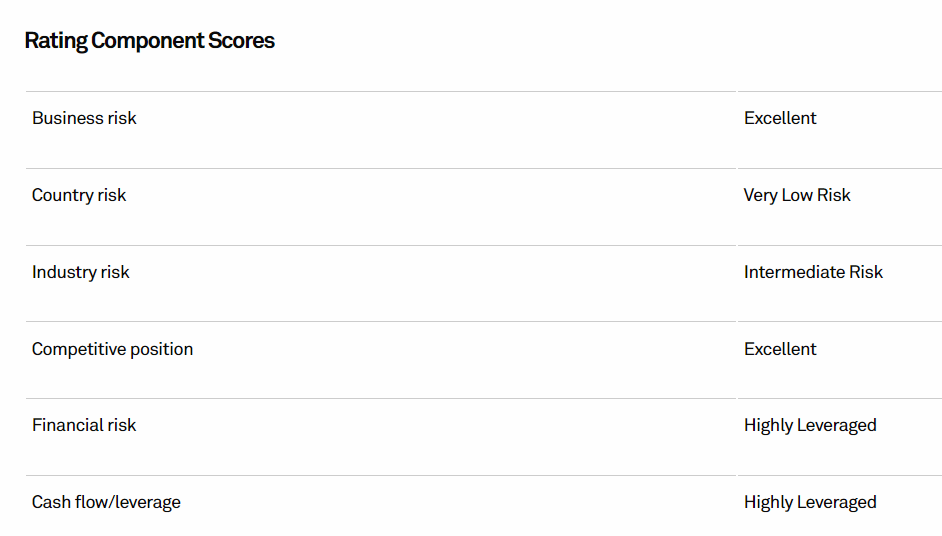

Crown Castle has a BBB (stable) credit rating from S&P and BBB+ from Fitch. S&P completed its annual review just a few days ago, and the main risk highlighted was related to the amount of leverage employed by CCI.

{kind=link}

S&P

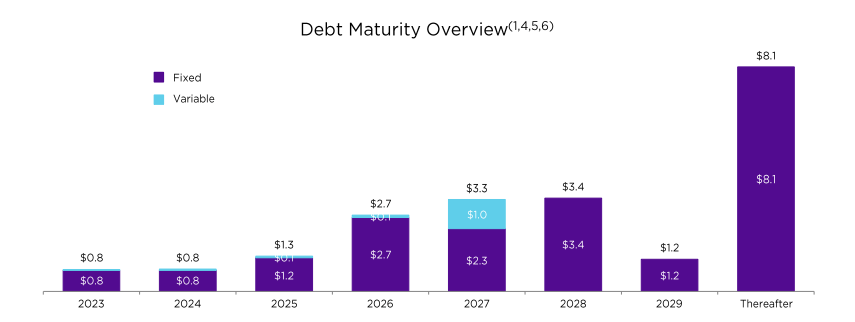

However, as a REIT, I don’t perceive CCI’s positioning as overly stretched. While the company has approximately $22 billion in debt against a $48 billion market cap, 91% of the total debt is fixed-rate, and maturities are well distributed, with a weighted average life of 8 years and a whopping $8.1 billion maturing in 2030 or afterward.

{kind=link}

CCI - Investor presentation May23

Valuation

With shares trading below $110, the company trades at less than 15x FY23 AFFO multiple. The multiple is below historical levels and appears pretty cheap for a business that enjoys steady cash flows with high visibility into the future.

With a dividend rate of $6.26, the yield is now pushing toward 6%. With a well-established track record of growth (5Y CAGR of 8.5%), the stock could appeal to DGI and income investors.

The stock has a median price target of $144 and a fair value of $140 by Morningstar, suggesting approximately 30% potential upside from current levels. By solving the dividend discount model ((DDM)) for growth using a $140 fair value and 10% required return rate, the market’s implied growth is 5.5%, well below management’s future target and historical results. FFO of $7.5 supports a valuation above $180 per share compared to historical valuation trends, and according to the below graph, CCI is by far the most undervalued it has ever been for the past ten years.

Seeking Alpha

Investor takeaway

I am assigning a BUY rating to Crown Castle and adding CCI shares to my DGI portfolio. I believe any irrational dip following Q2 results will represent an even more compelling opportunity to add exposure to a leading owner of vital communications infrastructure.

2Q23 results were not bad, the FY23 guidance trim was minimal, and CCI will still modestly grow AFFO over its 2022 base. The known problem related to the Sprint churn is a one-time issue that will likely be fully solved by 2025, and while AFFO growth got effectively stalled for a few years, CCI’s business model is alive and well. The Sprint/T-Mobile merger effectively dealt a blow to tower REITs by reducing the number of carriers from 4 to 3, but from here, the risk of further consolidation is negligible.

My expectations align with the consensus, and we should see 2025 through at about $7.4 AFFO per share. Afterward, the company should return to a 5%-7% AFFO growth. Buy & Hold investors who patiently wait for the uncertainty to sort out should be awesomely rewarded. Even by accounting for essentially zero growth through 2025 and about 6% after (well below management’s targets), I expect a total IRR of approximately 13% through the decade’s end.

For further details see:

Crown Castle: The Market Is Still Not Getting This Right, Buy The Dip