CSGS - CSG Systems: Navigating The Tech Wave For Growth But Profitability Reservations

2024-01-08 20:32:40 ET

Summary

- CSGS’ revenue growth has been impressive (+5%), with an improving trajectory in recent years following reinvestment in its services and industry tailwinds.

- Management’s expansion into new industries and the development of higher-quality services position CSGS well to maintain its existing trajectory.

- The company’s margin development has been disappointing, with dilution being a byproduct of its focus on growth.

- Relative to its peers, CSGS is underwhelming. The company is lacking in both growth and margins, although its commercial characteristics are not wholly reflected in its financial results.

- CSGS’ valuation does not imply sufficient upside in our view, particularly given that it is trading at a premium to its peers.

Investment thesis

Our current investment thesis is:

- CSGS is a solid business in our view, with a strong FCF yield and an attractive distribution strategy. When considered in conjunction with its positively developing business model, the company is set for a positive future.

- This said, its performance must be contextualized to consider if it is the correct investment relative to other available options. This is where the bull thesis weakens in our view. Its peers are performing better while being cheaper, making it difficult to view CSGS as a buy.

Company description

CSG Systems ( CSGS ) is a leading provider of business support solutions for the communications industry. With a focus on innovation, CSG enables its clients to monetize their products and services effectively. The company's solutions span the entire customer lifecycle, from acquisition to retention, offering a suite of services tailored to the dynamic needs of the telecommunications and media industries.

Share price

CSGS’ share price performance has been respectable, returning over 100% to shareholders during the last decade. This has been driven by healthy financial development, although not with perfect execution, contributing to it underperforming its peers.

Financial analysis

{kind=link}

Presented above are CSGS' financial results.

Revenue & Commercial Factors

CSGS’ revenue has grown well, with a CAGR of +5% during the last decade. EBITDA has failed to keep pace at a CAGR of +3%, despite initial gains.

Business Model

CSGS specializes in revenue management solutions, offering services that help businesses optimize their revenue streams. This includes billing and payment processing systems, subscription management, and revenue analytics.

In an increasingly digital world, CSGS enables businesses to monetize their digital services effectively. This involves providing platforms and tools for digital content delivery, including streaming services and digital products.

The company places a strong emphasis on enhancing customer experience, which is critical given the highly competitive environment in the digital space. CSGS solutions help businesses improve customer interactions, ensuring satisfaction and loyalty.

CSGS is increasingly leveraging advanced analytics to provide insights into customer behavior, market trends, and revenue performance. Data-driven decision-making is a key component of its services and growing in importance as we transition into a data era, enabling clients to make informed strategic choices.

The company has developed its capabilities globally, serving clients in different regions. This global presence allows CSG to tap into diverse markets, adapt to regional regulatory requirements, and understand the unique needs of clients worldwide.

Despite the well-structured business model and tailwinds from technological development, CSGS’ growth has been mild. This is primarily due to its focus on slow-moving industries, limiting CSGS’ scope for outperformance.

Management’s current growth strategy is based 4 pillars:

- Grow organic revenue faster: Management has invested in its capabilities to broaden its service offering ( Discussed in more detail later ). This has contributed to an uptick in its growth rate, which in conjunction with the following points, suggests it can be maintained.

- Add strategic operating scale: In conjunction with accelerating organic growth, Management is seeking to continue its M&A strategy in order to scale the business further. We are not completely convinced but are supportive of continuing this.

- Become the #1 SaaS provider for global telecom & cable: CSGS is leveraging its existing relationships to illustrate to global telcos it is positioned well to provide market-leading services. This is likely the pillar we are least convinced about, given the limited tangible examples of actions.

- Diversify revenue faster in exciting big new verticals: CSGS is seeking to grow outside of Telco and exploit growing industries such as Pharma, a shrewd decision in our view given the limitations of growth from the industry. This is progressing extremely well implying a fundamentally high-quality offering, with “Other” industries comprising 7% of revenue in FY17 (the remaining being telco/cable) and 27% in Q3’23.

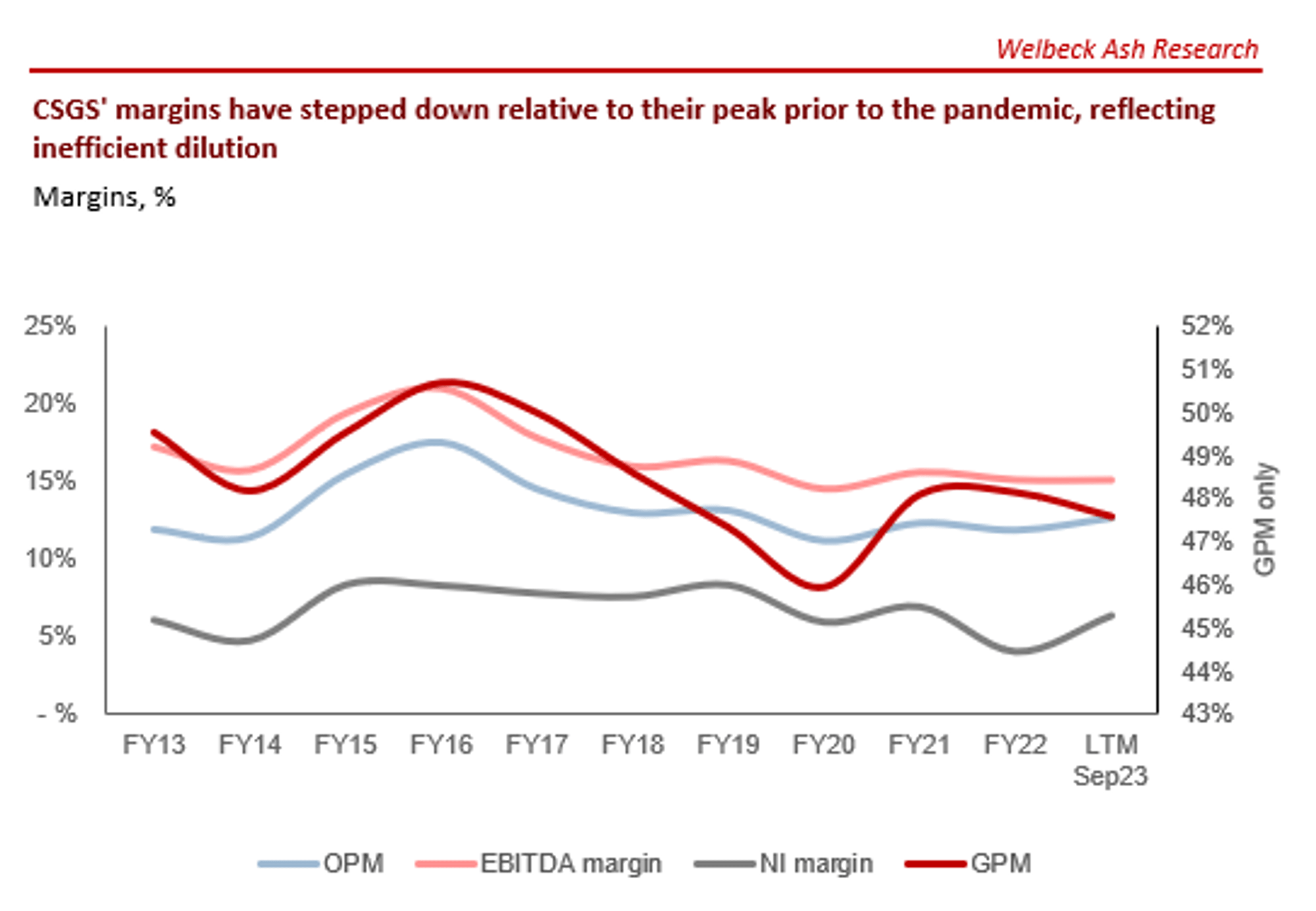

Margins

{kind=link}

CSGS’ margin development has been disappointing. Despite an initial improvement into FY16, the company has declined to a record low level (excl. the pandemic impacted year).

The decline in EBITDA-M is primarily due to a reduction in GM%, which has fallen from 51% in FY16 to 48% in the LTM. S&A spending as a % of revenue has also increased by 3ppts.

This is due to a combination of factors. Firstly, Management has sought to reinvest in its product offering to attract more lucrative services, which based on its growth improvement post-FY16 implies success. Secondly, the business has experienced dilution as it has scaled its operations, illustrating a willingness to trade margin for growth. Finally, Management began acquiring businesses in FY18, contributing to dilution.

Looking ahead, we do believe there is scope for margin improvement through greater weighting toward SaaS revenue, as well as optimization of its operations. This said, the limited improvement in recent years implies Management is unable to execute.

Quarterly results

CSGS’ recent performance has been strong, with top-line revenue growth of +5.4%, +13.0%, +9.2%, and +5.0% in its last four quarters. In conjunction with this, margins appear to have stabilized, although there is scope for a further decline short-term based on trends.

The company’s clients have inevitably been negatively impacted by the current macroeconomic conditions, as businesses turn defensive and consumers soften spending. This said, its target market of telcos and related media businesses positions it well to be resilient, owing to consistent consumer demand due to its inelastic nature.

When considering this in conjunction with its strategic focus on improving its pipeline and scale, CSGS has managed to win notable contracts and expand its remit, such as with Chater and Comcast in the US and M1 Singapore.

Looking ahead, we suspect CSGS can maintain its current growth trajectory, particularly if it can meaningfully expand into new industries that are currently being targeted.

Balance sheet & Cash Flows

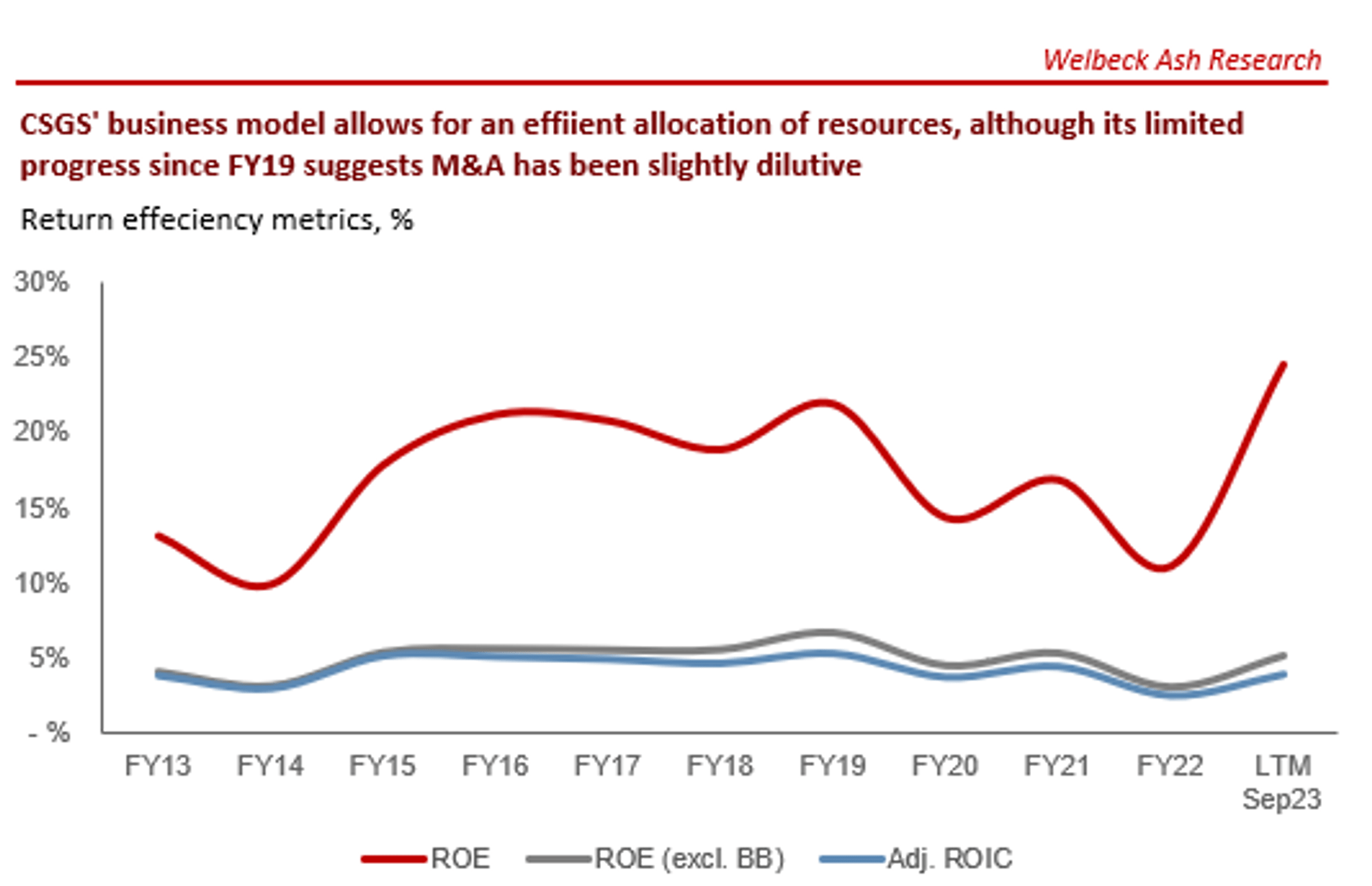

CSGS is conservatively financed, with an ND/EBITDA ratio of 2.4x. This is a reflection of its cash-generative nature, with highly consistent FCF generation, which has been kept elevated despite declining margins due to lower Capex spending.

This has allowed Management to initiate an aggressive capital allocation strategy, with both consistently growing distributions and M&A. We are hesitant to suggest the M&A strategy is completely successful, given the margin erosion experienced, although we note ROE has been broadly flat and so investors are not negatively impacted.

Distributions have grown impressively, with buybacks growing at +26% and dividends at +9%. Given FCF is in the region of ~$75m, the current levels are not sustainable. This is particularly unusual given Management has raised debt to deliver this. We expect buybacks to fall noticeably in the coming year for this reason.

{kind=link}

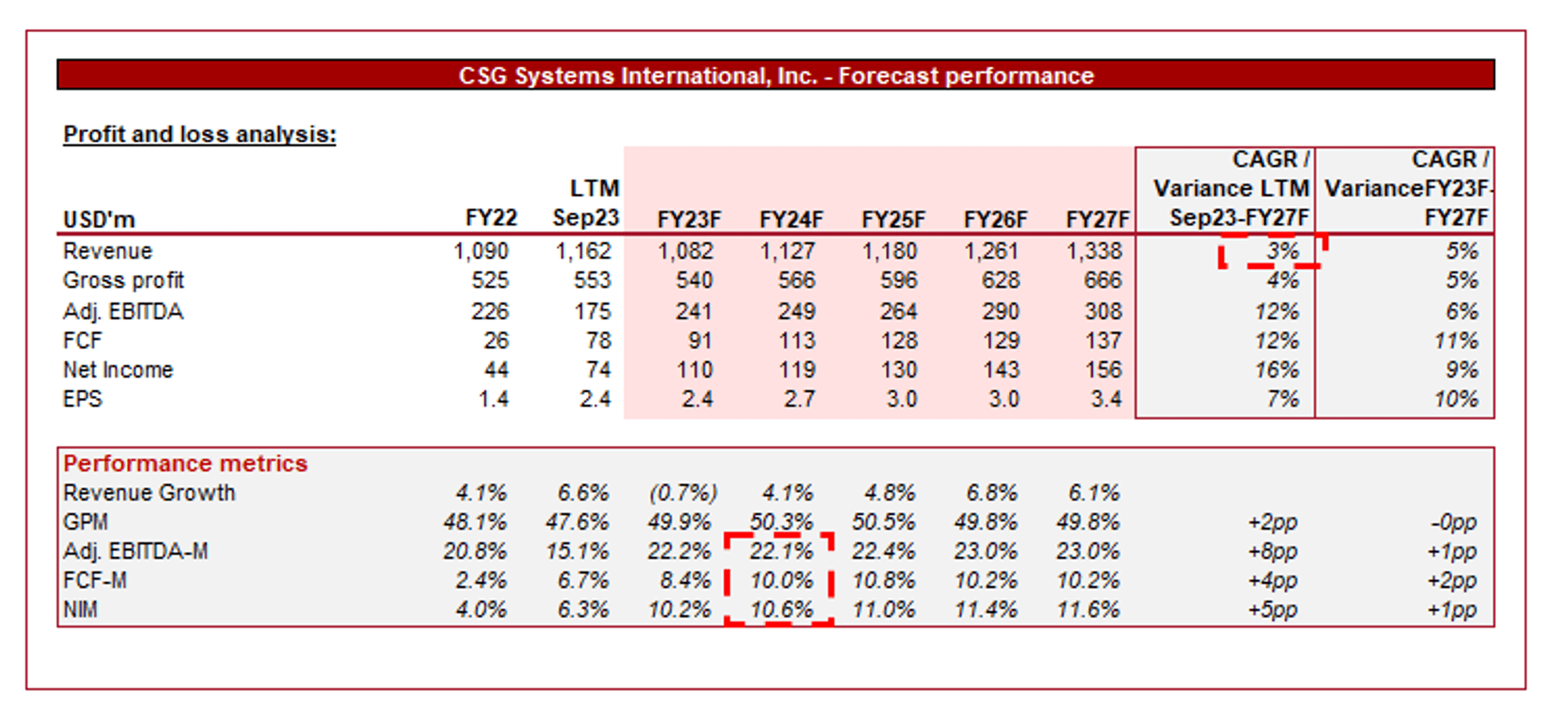

Outlook

{kind=link}

Presented above is Wall Street's consensus view on the coming years.

Analysts are forecasting revenue growth to soften in the coming years, with a CAGR of +3% into FY27F. In conjunction with this, margins are expected to improve slightly relative to FY22, although not materially so.

We broadly consider these assumptions to be conservative, suspecting revenue could exceed these levels given its recent trajectory. In its last five quarters, CSGS has beat on revenue and EBITDA every time, suggesting analysts are currently underestimating the company.

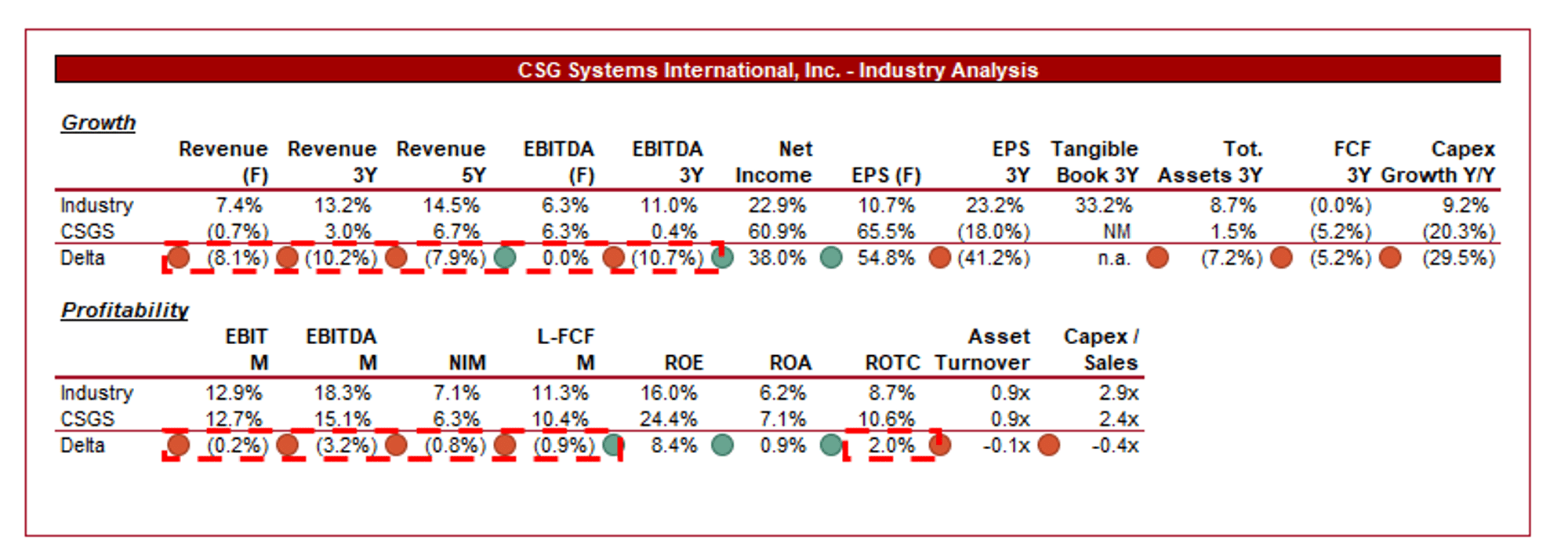

Industry analysis

{kind=link}

Presented above is a comparison of CSGS' growth and profitability to the average of its industry, as defined by Seeking Alpha (16 companies).

The company performs relatively poorly when compared to its peers. Revenue growth is noticeably below the average, with this forecast to continue. This is driven by a less aggressive approach to investing in expansion, alongside its niche focus on a mature industry. CSGS is inherently tied to the growth of the industries it serves.

Further, its margins are below the average, although not materially so, boasting a superior ROTC. This is an issue of execution in our view, given the dilution experienced during the last few years. Management has needed to invest in its capabilities to create a more well-rounded, broader service offering,

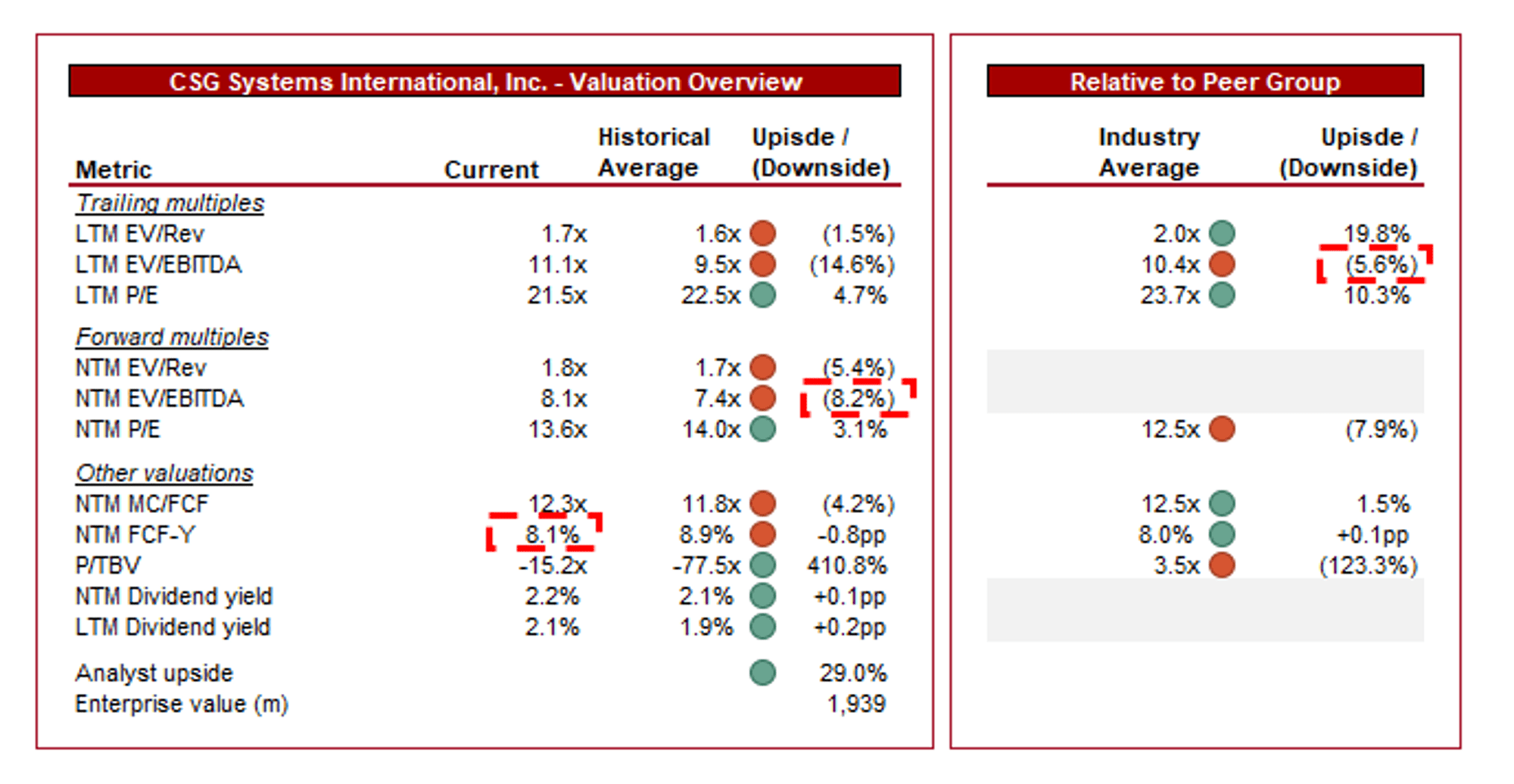

Valuation

{kind=link}

CSGS is currently trading at 11x LTM EBITDA and 8x NTM EBITDA. This is a premium to its historical average.

A premium to its historical average is warranted in our view, primarily due to the improvements in its business model. The company is far better placed to target a wide range of industries, while continuing to develop its telco/media capabilities, contributing to a widening of its competitive position and thus growth potential. The decline in margins is an offsetting impact, and so we do not expect the premium to be significant.

Further, CSGS is trading at a small premium to its peers, with a LTM EBITDA premium of ~6% and a NTM PE premium of ~8%. This is far more difficult to rationalize given the clear outperformance relative to CSGS. Even if growth can sustainably accelerate, the gulf to its peers is unlikely to sufficiently close. Investors must be expecting margin improvement alongside growth to justify this valuation.

Based on this, we believe CSGS is likely slightly overvalued. Its FCF yield of 8% appears attractive but this is below its historical average (~9%), further implying a premium.

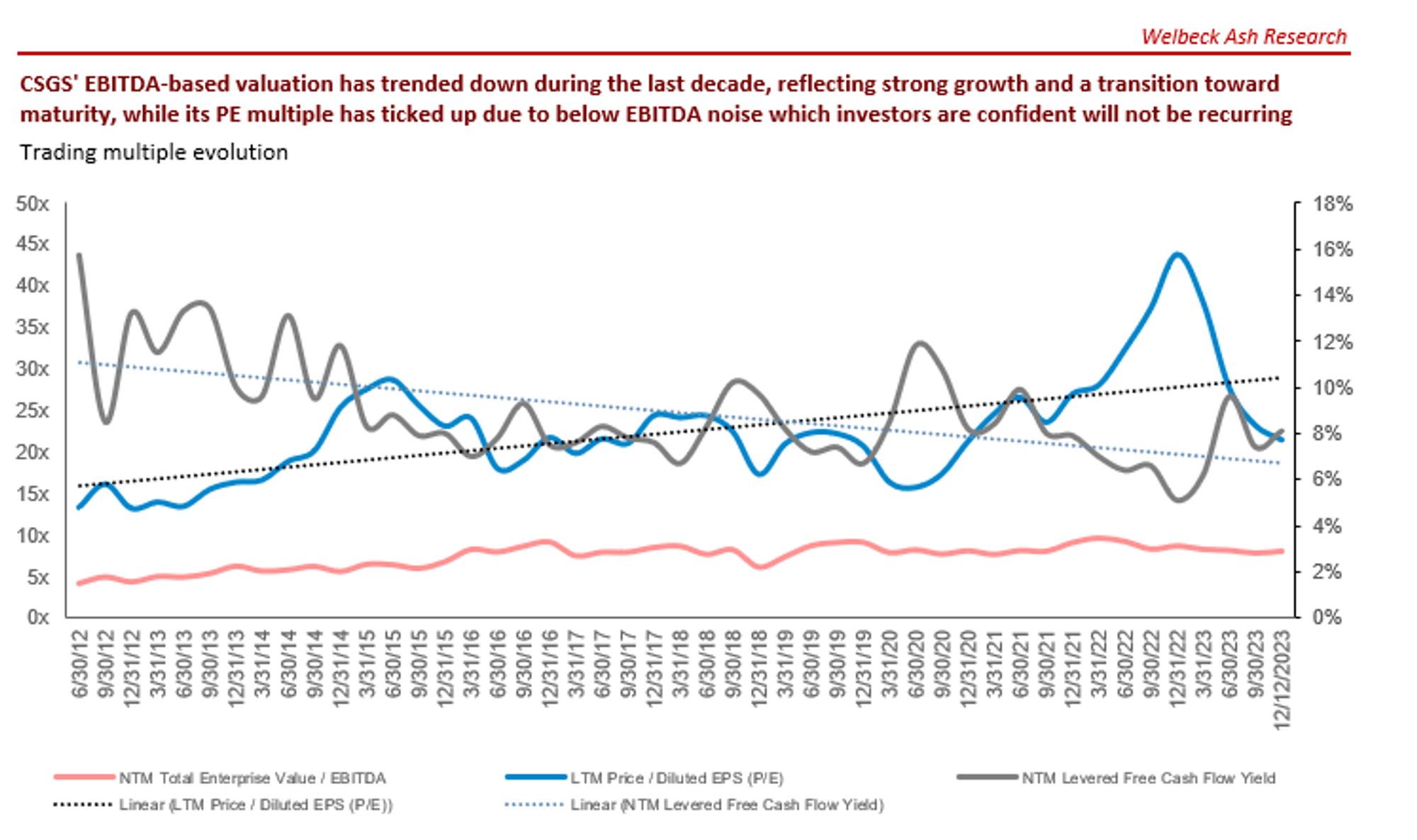

Valuation evolution (Capital IQ)

{kind=link}

Key risks with our thesis

The risks to our current thesis are:

- [Upside] Successful integration of emerging technologies and new trends.

- [Upside] Effective response to industry trends that contribute to an uptick.

- [Upside] Transformational M&A.

- [Downside] Failure to adapt to technological changes.

- [Downside] Increased competition impacting market share, particularly if price-driven.

Final thoughts

CSGS is a high-quality business that is positioned well to achieve healthy long-term growth, particularly if industry tailwinds are maintained and CSGS continues to gain traction in new industries. We do not see sufficient attractiveness relative to its peers, however, considering this the biggest issue currently. At its current valuation, we await the scope for margin improvement.

For further details see:

CSG Systems: Navigating The Tech Wave For Growth But Profitability Reservations