PBE - CSL Limited: Market's Focus Is On Guidance And Recent Acquisition

- Both the FY 2022 top line and bottom line for CSL didn't meet the market's expectations, with the weakness associated with the core Behring business segment being a key factor.

- The FY 2023 outlook for CSL is better than management guidance suggested, taking into account one-off items.

- CSL stays as a Hold, as more information is needed to determine if the recent Vifor M&A deal was a good move.

Elevator Pitch

My Hold investment rating for CSL Limited's ( CSLLY ) [CSL:AU] shares stays unchanged.

I wrote about CSLLY's new license agreement and its short-term prospects in a prior May 21, 2021 article for the company. This current article is written with the aim of reviewing CSL Limited's recently announced full-year fiscal 2022 (YE June 30) financial results and other key developments.

CSL Limited's revenue and earnings missed consensus expectations slightly, but the company's FY 2023 management guidance (adjusted for one-offs in FY 2022) looks promising. However, CSL's current fiscal 2023 guidance has yet to include the impact of a key recent acquisition, Vifor. As such, I decide to retain my Hold rating for CSL Limited, pending the release of more relevant details on Vifor in the next few months.

Fiscal 2022 Results Were A Modest Miss

CSL Limited issued a press release disclosing its financial performance for fiscal year 2022 on August 17, 2022.

Headline revenue for CSLLY expanded by +2.4% YoY from $10,310 million in FY 2021 to $10,562 million for FY 2022, and this was just -1.1% lower than the sell-side analysts' consensus top line prediction of $10.68 billion based on data sourced from S&P Capital IQ . If one adjusts for the effects of foreign exchange, CSL Limited would have delivered a higher adjusted for constant-currency revenue growth of +3.5% YoY for fiscal 2022.

The company's core Behring business focused on plasma technologies saw its segment revenue decline by -0.8% from $8,428 million in fiscal 2021 to $8,360 million in FY 2022. This was more than offset by a +14.5% growth in segment sales for its Seqirus business engaged in influenza vaccines from $1,552 million to $1,777 million during the same period.

CSLLY highlighted at its FY 2022 earnings briefing on August 17, 2022 that "plasma products have a long manufacturing cycle between 9 and 12 months" and the sales of these products for FY 2022 were negatively affected by the lower-than-expected "volume of plasma collected in the previous year (FY 2021 or the period between July 1, 2020 and June 30, 2021)" due to COVID-19 lockdowns and restrictions. Therefore, it isn't surprising that the Behring segment delivered flattish top line growth for FY 2022.

On the flip side, CSL Limited revealed at the fiscal 2022 results call that "seasonal influenza vaccine sales" were "up 16%." This was a major factor which helped to drive the Seqirus business segment's overall revenue up by +14.5% in the recent fiscal year.

With respect to the bottom line, CSL Limited's after-tax net income decreased by -5.0% from $2,375 million for fiscal 2021 to $2,255 million in fiscal 2022. The company's bottom line for the most recent fiscal year fell short of the market's consensus earnings projection of $2,305 million (source: S&P Capital IQ ) by -2.2%.

The reduced profitability of the Behring business was the key reason for CSL Limited's bottom line contraction and earnings miss. While the Seqirus business' gross profit margin improved by +1.4 percentage points from 57.3% in FY 2021 to 58.7% in FY 2022, the gross margin for the Behring segment decreased by -320 basis points from 56.5% to 53.3% over the same period. Negative operating leverage and the increase in plasma collection expenses were a drag on Behring's gross profit margin in the recent fiscal year.

Fiscal 2023 Outlook Is Better Than What Guidance Implies

As part of the company's FY 2022 financial results release, CSL Limited also announced its guidance for FY 2023.

CSLLY expects to generate a constant-currency revenue growth of +7%-11% for full-year FY 2023, which will be a significant improvement as compared to its adjusted top line expansion of +3.5% for the previous fiscal year.

But CSL Limited's constant-currency net profit guidance of between $2.4 billion and $2.5 billion for FY 2023 appears to be relatively modest. On the surface, CSLLY's mid-point bottom line guidance of $2.45 billion only translates into a +9.6% increase in comparison with the company's constant currency earnings of $2,236 million for FY 2022.

But if one adjusts for the $70 million in one-off costs, CSL Limited's management guidance points to a much more attractive +13.1% adjusted net income growth for fiscal 2023. With plasma collection activity normalizing as COVID-19 eases, it is reasonable that CSL returns to higher top line and bottom line growth for FY 2023.

More importantly, CSL's current FY 2023 guidance has yet to incorporate the effects of a recently completed M&A deal, which I will discuss about in the next section.

More Clarity On Recent Acquisition Required

CSL Limited announced on August 10, 2022 that the takeover of Vifor Pharma AG or Vifor has concluded successfully. Earlier towards the end of last year, CSLLY disclosed that it proposed to "launch an all-cash public tender offer to acquire all publicly held Vifor Pharma shares," and it referred to Vifor as a "pharmaceuticals company" with a focus on "Nephrology, Dialysis and Iron Deficiency."

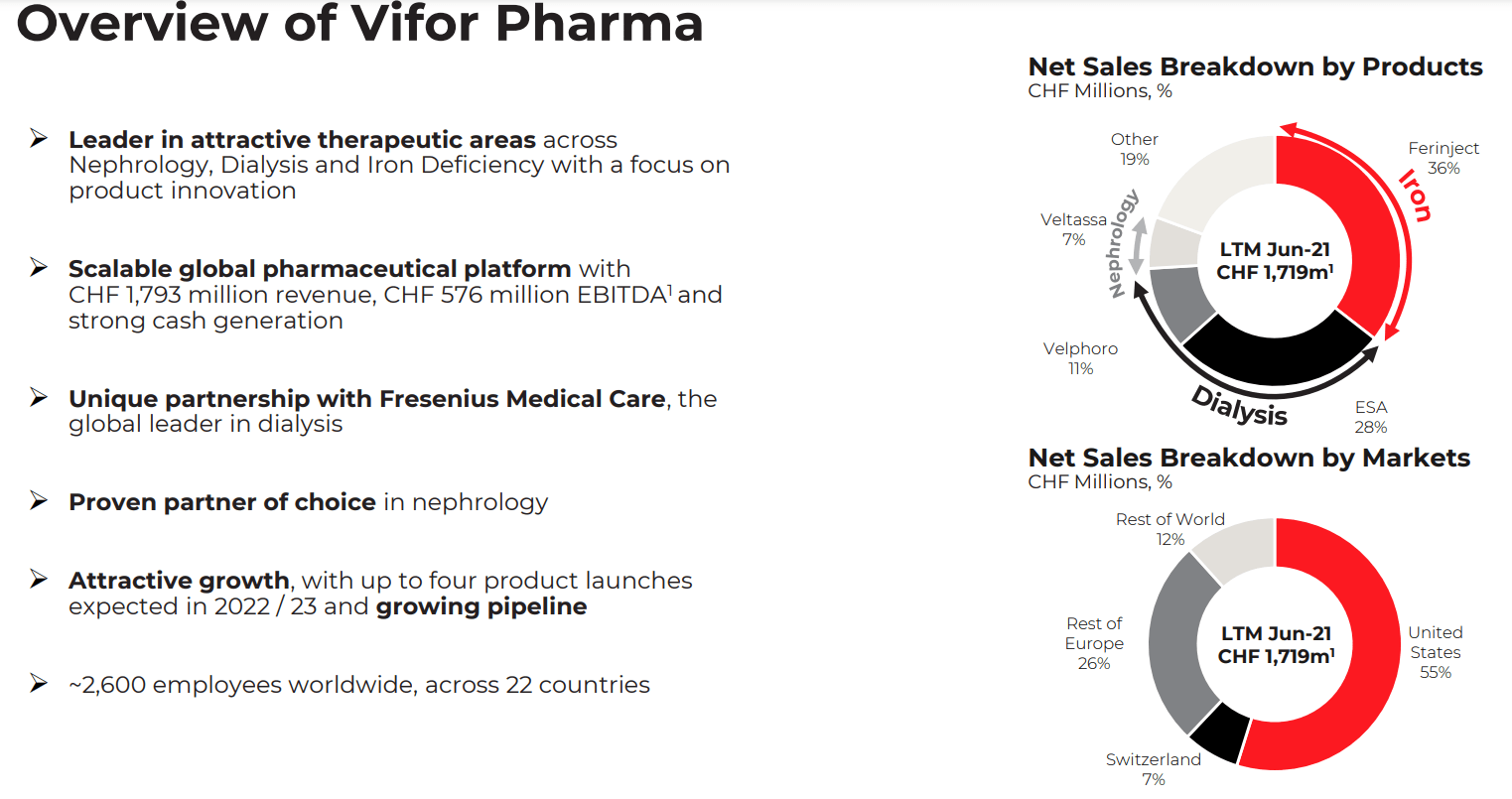

Vifor's Corporate Background

{kind=link}

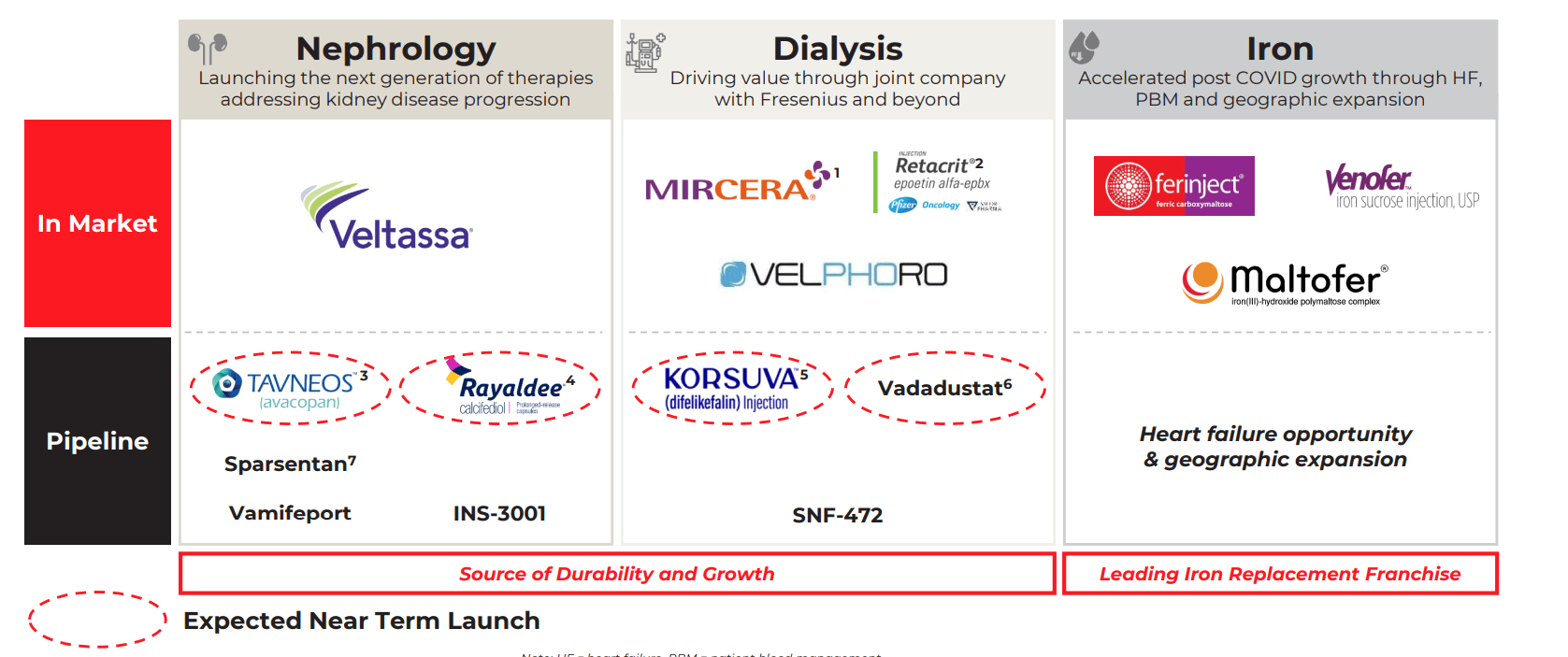

Vifor's Current And Future Products

{kind=link}

There are two key factors that might lead to certain investors viewing CSL Limited's acquisition of Vifor in a slightly negative light. Firstly, the deal isn't exactly cheap, with the implied price-to-sales multiple being in excess of 4 times based on my calculations. Secondly, CSLLY has chosen to acquire a company which focuses on therapeutic areas that are different from that of its core Behring business.

At this point of time, it seems too early to judge the Vifor transaction. At its FY 2022 investor call, CSL Limited has committed to updating its FY 2023 guidance to "include CSL Vifor at the first practical opportunity", and discussing "more about the strategic merits of the deal at a dedicated CSL Vifor briefing in October."

I choose to reserve judgment on the Vifor acquisition till the point when more quantitative (new FY 2023 guidance) and qualitative information (October 2022 management briefing for Vifor) on the transaction are provided in due course.

Closing Thoughts

I continue to rate CSL Limited as a Hold. It is tough to have a Buy or Sell call on the name, when critical details with regards to the company's recent key M&A deal aren't known yet. On the financial side of things, CSL's FY 2022 financial performance was reasonably decent despite a slight miss. Looking forward, the company's FY 2023 performance, excluding the impact of the Vifor deal, is expected to be better than of FY 2022.

For further details see:

CSL Limited: Market's Focus Is On Guidance And Recent Acquisition