CSWI - CSW Industrials: Significant Premium For What Could Be Muted Growth

2023-11-04 01:43:31 ET

Summary

- CSW Industrials Inc. has seen increased optimism in the residential industry due to construction projections and high demand for housing.

- The company's share price has increased by 38% in the last 12 months, but its high valuation and sector premium make it a hold rather than a buy.

- CSW Industrials specializes in manufacturing mechanical products for various sectors and has experienced revenue growth through acquisitions.

Investment Rundown

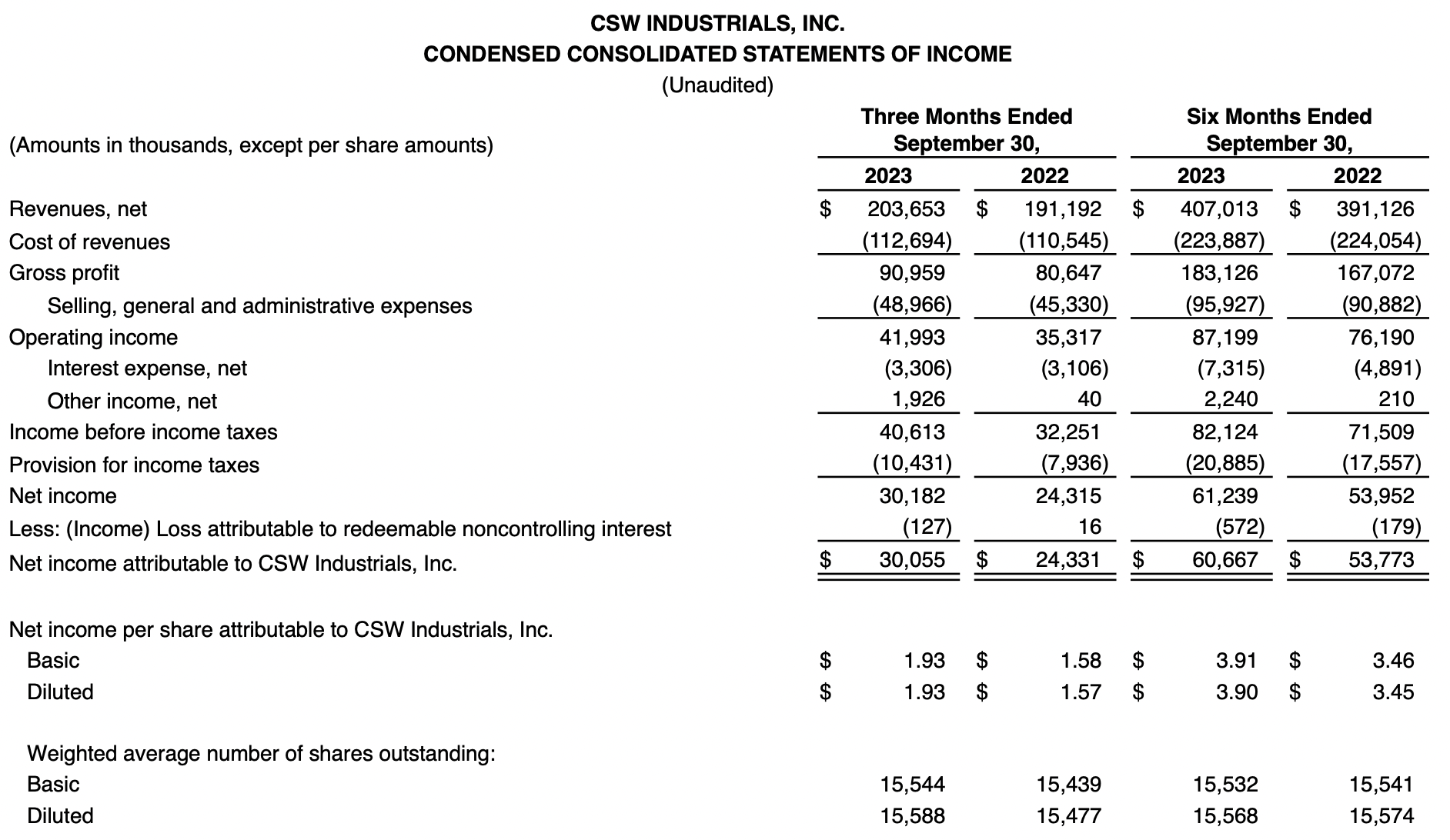

In recent months, or in some cases the better part of 2023 there has been an increased optimism around companies in the residential industry mostly focusing on construction projections and buildings. CSW Industrials Inc (CSWI) has no expansion when it comes to the increased optimism as real estate prices have shown resilience as there is still a quite large deficiency in terms of housing and people in the US, which is bolstering the demand and resulting in higher prices. Over the last 12 months, the share price has increased by around 38% for CSWI but it has unfortunately reached a level where I can't say it a reasonable buy by any valuation standards. The p/e is over 25, which is incredibly high for a company in the sector and more or less indicates that CSWI should be able to grow the bottom line by double digits consistently. Last quarter saw revenues reach record levels at $203 million which puts CSWI at a TTM p/s of 3.6, a 187% premium to the sector.

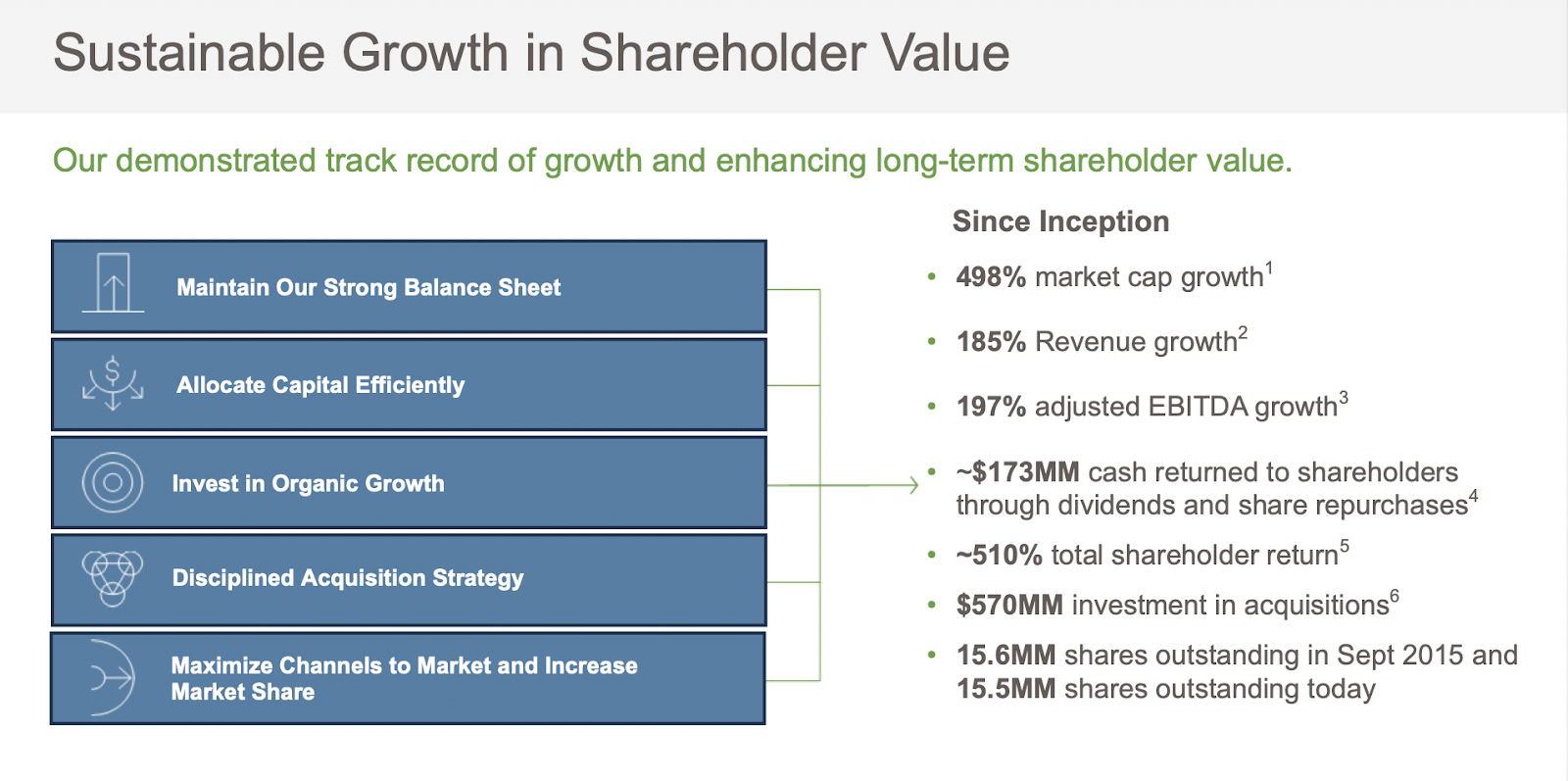

The growth has since listing on the Nasdaq been quite solid and in the last 5 years, the revenues have compounded at 18.4% annually. This is impressive and I think the market is betting it will continue this way. I lean more towards that CSWI maybe delivering a decent top and bottom line growth in the 7 - 8% range over the next decades. This would not equate to the current multiples it receives and even if eventually the results catch up to the valuation, then I think it's a long time until investors will be seeing any significant returns on their investments. This brings me to rate CSWI as a hold rather than a buy. Buying should be done when the price is at a far more reasonable level, which is something I will outline further down in the article.

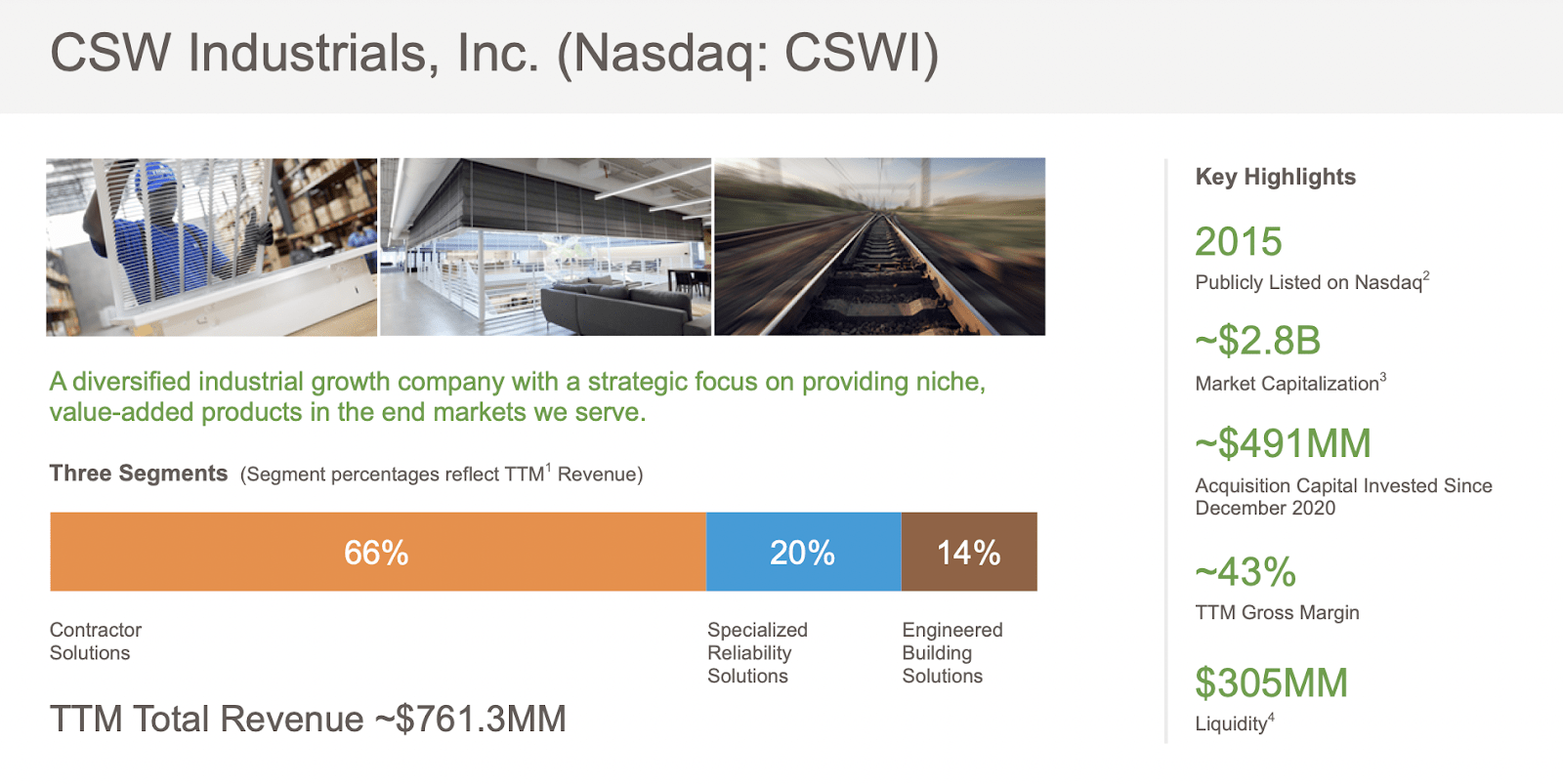

Company Segments

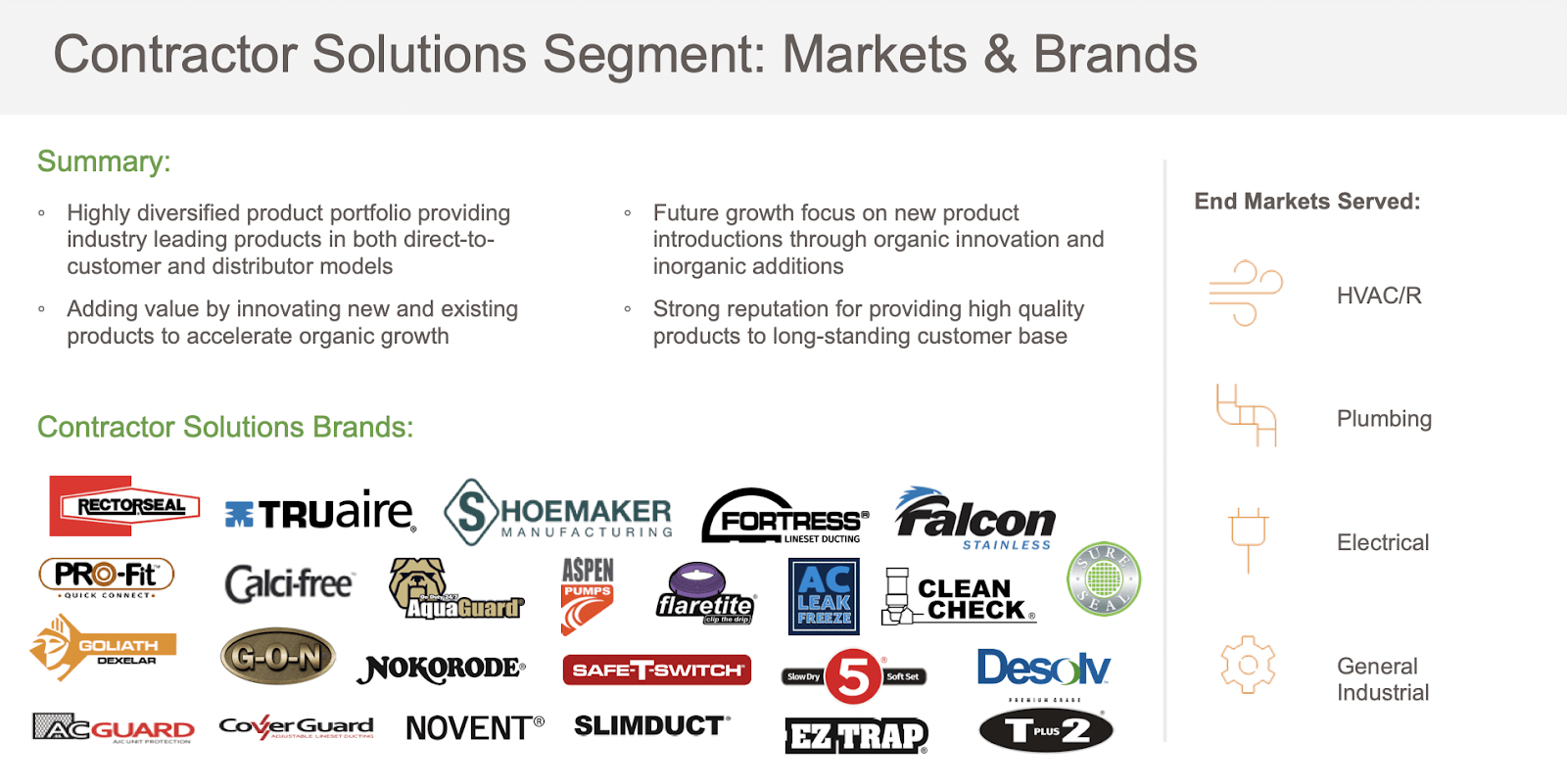

CSW Industrials specializes in the manufacturing of mechanical products utilized in various sectors, including HVAC/R, plumbing, as well as grilles, registers, and diffusers ((GRD)). Additionally, the company is a key player in the realm of building safety solutions and high-performance specialty lubricants and sealants. These diverse product offerings cater to an array of industries and applications.

{kind=link}

The company's operations are organized into three distinct operating segments, each of which plays a crucial role in delivering innovative solutions and contributing to the broader landscape of mechanical and safety products. As CSW Industrials continues to expand its product portfolio and explore growth opportunities, its commitment to quality and innovation remains a hallmark of its presence in these diverse markets.

Investor Presentation

One of the key drivers behind the company's ability to grow revenues at a fast rate in the last few years has been extensive acquisitions and M&A opportunities. In the last 12 months, nearly $60 million has been going towards acquisitions, which is around 8% of the total revenues. That is a substantial amount and perhaps something the market is looking towards for CSWI to continue to deliver the value that the share price is valued at right now.

Earnings Highlights

{kind=link}

Last report the company published they managed to grow the revenues at a slight YoY increase, reaching $203 million, a $12 million increase. The positive factor for the quarter was that gross profits increased at a faster rate seeing as the cost of revenues declined following lower materials costs and prices. This is a short-term tailwind for the company and something that could lead to further EPS growth in both Q3 and Q4 of FY2024 for the company. The latest report I don't think was enough to justify 24 p/e. For CSWI to climb down to a p/e of 16 given the current price it would need to provide annual EPS of $11 at least, or $2.75 every quarter. Last quarter saw an EPS of $1.93 which means a 40% increase is necessary. I don't see falling materials prices as a sufficient driver of such EPS expansions. The management sees positive on the latest results and seems positive as well in the coming quarters that some growth will be seen, I just don't think it's enough to justify the current valuation the company has.

{kind=link}

With such a broad set of markets that CSWI is serving, I think it will eventually see revenues pick up once again as interest rates potentially go down and companies are left with more capital available for spending and expansion endeavors. This would lead to sales growth for CSWI I think. However, I do also think that could take some time as expecting the interest rates to go down to around 1 or even lower is not likely to happen this decade honestly. We have seen the results of having very low interest rates, which pumped up inflation numbers and eventually, quantitative tightening which is hurting some industries.

Setting a price target for CSWI I think as long as it remains over the sector average p/e it will be a hold. With the sector p/e in mind, I get a price target of $112 with a $7.07 FY2023 EPS in mind. In December of last year, CSWI was trading around those levels and a broader market sell-off paired with weaker fundamentals in the condition sector could lead to us revisiting those levels and making CSWI a buy perhaps.

Risks

The company's revenue outlook for FY24 remains contingent on the successful completion of inventory destocking at channel partners during the latter half of 2023. The timing and effectiveness of this destocking process will play a pivotal role in shaping the revenue trajectory for the next fiscal year.

{kind=link}

Furthermore, it's important to note that the costs associated with specific raw materials and freight are showing a downward trend, which could bode well for the company's cost structure. However, the market dynamics are subject to change, and if a scenario of material shortages and tight freight conditions materializes, the costs of both raw materials and freight could experience an upswing. Such an increase in costs would inevitably impact the company's profit margins, making it essential to carefully monitor these variables and adapt strategies to navigate the evolving economic landscape effectively.

{kind=link}

Apart from the risk of significant material increases, I see the high valuation as a risk as well to investors. Should CSWI see a lack of growth numbers in not just the next earnings report, but also in several ones afterward I think we are heading quickly down to a p/e of 12 - 14 for the company, which leaves a significant drop. What is supporting it right now is resilient real estate prices I think as it has reassured investors about the fundamental prospects of investing there. The largest segment for CSWI is the contractor solutions at around 66% of total sales. Demand there is more or less a direct reflection of strong market optimism for construction and real estate in general.

Final Words

The construction industry has seen some pretty resilient demand as the lack of housing is driving prices upwards seeing as there is still a shortage. Even if CSWI isn't necessarily solely relying on strong housing prices, it still gains from positive trends here and improved prices. The share price has however run up far too much for my liking and I don't think it's reasonable to be buying right now. Investors are better or holding shares and waiting for the price to come down instead.

For further details see:

CSW Industrials: Significant Premium For What Could Be Muted Growth