CSWI - CSW Industrials: Waiting For Further Value-Creating Acquisitions

2023-10-31 23:10:36 ET

Summary

- CSW Industrials manufactures and distributes a wide range of industrial products.

- The company's strategy revolves around acquisitions that benefit from CSW's large distribution network.

- CSW has achieved both organic and acquisition-driven growth, with a CAGR of 14.0% from FY2013 to Q1/FY2024.

- The stock seems to be priced correctly when considering CSW's organic performance - further acquisitions could still create further excess shareholder value.

CSW Industrials ( CSWI ) manufactures and distributes products for industrial and other use cases. The company has a very wide range of products as a result of numerous amounts of acquisitions; CSW’s strategy includes acquiring businesses and improving the acquired products’ distribution with CSW’s extensive network of distributors. The company’s strategy seems to have worked very well as the company’s stock has performed very well after an IPO in 2015. To analyze the stock’s valuation, in this article, I constructed a discounted cash flow model with organic estimates.

The Company & Stock

CSW operates in three segments – Contractor Solutions with 66% of revenues, Specialized Reliability Solutions with 20% of revenues, and Engineered Building Solutions with 14% of revenues. The Contractor Solutions segment produces and sells products for heating, ventilation, air conditioning, refrigeration, plumbing, electrical, and industrial applications with products such as pipe sealants, switches, grilles, drain pans, water & gas connectors, and refrigerant fittings. The Specialized Reliability Solutions segment includes products for B2B markets such as rail transport, energy, mining, and other industrial purposes. Lastly, the Engineered Building Solutions segment manufactures railings and other products for smoke & fire detection, safety railings, and other end markets.

{kind=link}

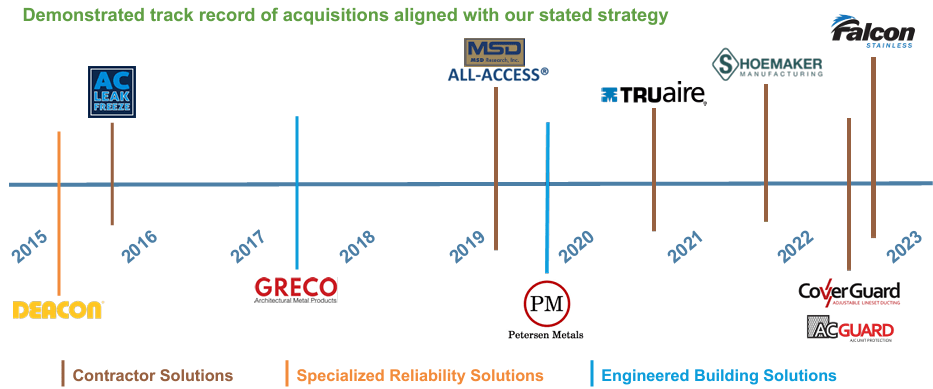

Of the segments, Contractor Solutions has the clearly best EBITDA margin in addition to the majority of revenues. The segment has also experienced a good amount of growth, as CSW has had four acquisitions for the segment from 2020 forward:

{kind=link}

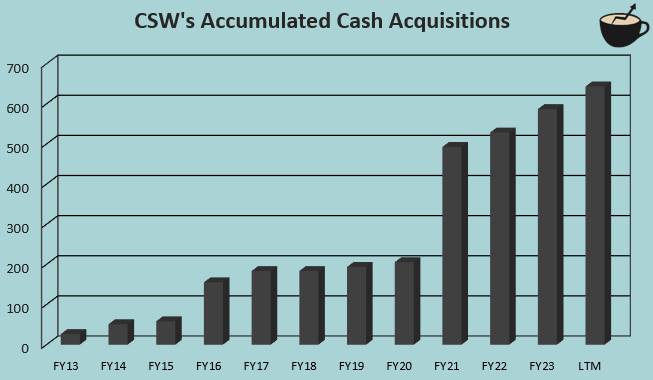

As can be seen, CSW’s strategy includes a good amount of acquisitions to fuel constant growth. The company aims to achieve growth in the acquired businesses, as CSW’s distribution channels are a powerful way to expand a product’s reach. In total, CSW has had $644 million in cash acquisitions from FY2013 into the current moment as of Q1/FY2024:

{kind=link}

The stock has performed exceptionally well after CSW had an IPO in late 2015, the stock has appreciated by around 426%:

{kind=link}

In addition, CSW pays out a very small dividend. Currently, the dividend yield stands at 0.43% ; most of CSW’s cash flows are used in share repurchases and acquisitions, which seems to have worked well for CSW’s shareholders.

Financials

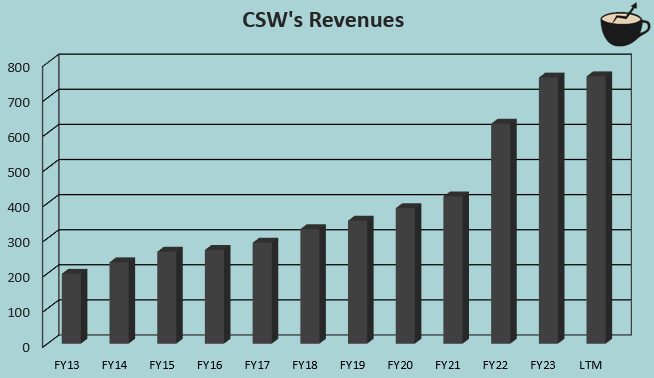

As CSW has had a significant number of acquisitions in the past, the company has been able to grow at a good pace. From FY2013 to LTM figures as of Q1/FY2024, CSW’s compounded annual growth rate has been 14.0%:

{kind=link}

Although acquisitions have fueled the growth, CSW has also achieved a good amount of organic growth. The company’s total revenue CAGR has been 18.4% from FY2018 to FY2023, most of which has been organic even with $403 million of cash acquisitions in the period – the organic CAGR in the period was 11.4% according to CSW’s Q1 investor presentation.

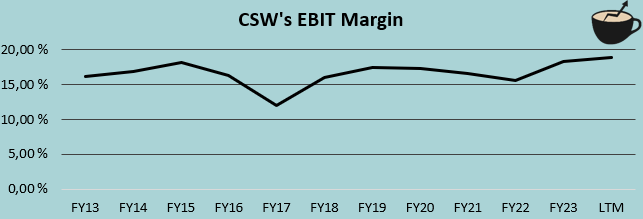

CSW’s margins have been mostly stable. From FY2013 to FY2023, the company’s average EBIT margin has been 16.6%, with the margin currently standing at 18.8% with trailing figures:

{kind=link}

The higher margin seems to be a result of operating leverage in SG&A – CSW’s gross margin has decreased from a level of 48.4% in FY2014 into a current level of 42.6%, but the company’s operating margin has still scaled in the same period of time.

Valuation

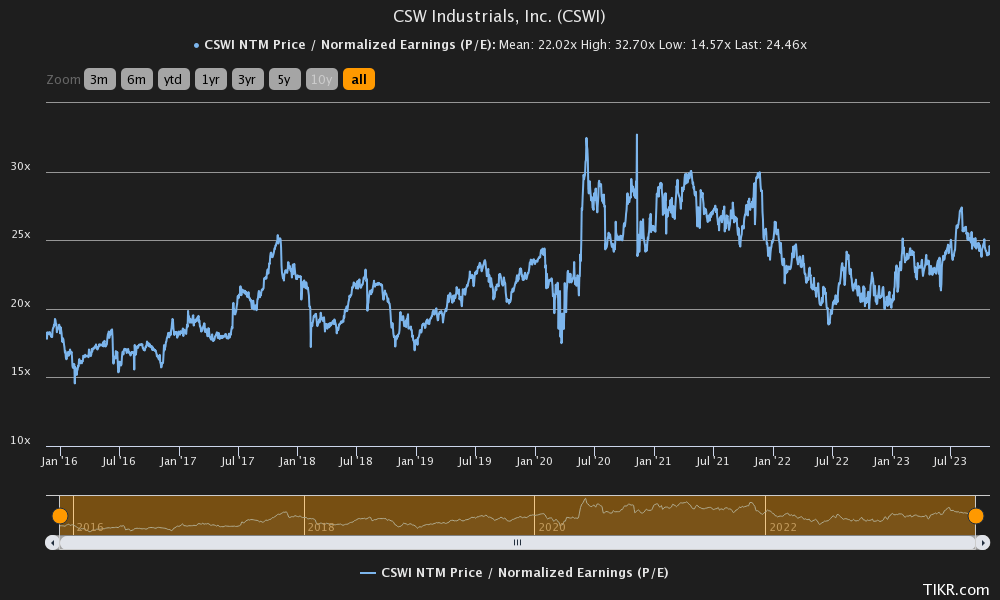

CSW doesn’t seem very cheap. Currently, the stock trades at a forward P/E ratio of 24.5, above the company’s historical average of 22.0 from CSW’s IPO:

{kind=link}

As CSW’s acquisitions create value and the company has some organic growth, the P/E ratio could be justified. To estimate a rough fair value for the stock and to contextualize the price tag, I constructed a discounted cash flow model as usual. I only model in an organic performance from the company, as cash flows from acquisitions are challenging to estimate.

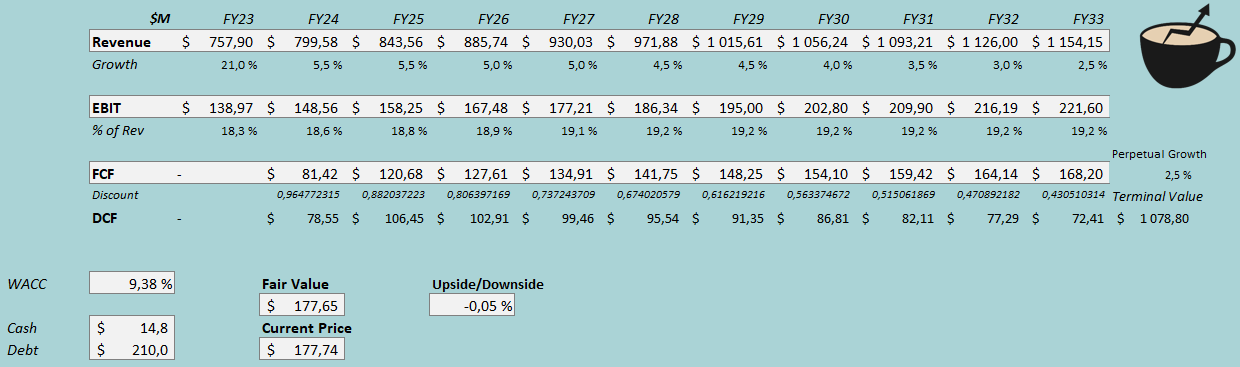

In the model, I estimate CSW’s revenues to grow by 5.5% organically in FY2024. I estimate the same growth to carry onto FY2025 with the same growth rate in the year. After FY2025, I estimate CSW’s growth to start slowing down in steps into a perpetual growth rate of 2.5% from FY2033 forward. The estimated growth corresponds to a CAGR of 4.3% from FY2023 to FY2033.

I believe that CSW’s margin stability should be quite similar going forward. For FY2024, I estimate the company’s EBIT margin to be very slightly above the achieved FY2023 level at a figure of 18.6%. As a result of operating leverage, I estimate the margin to eventually scale very slightly into a figure of 19.2%, with the level being achieved in FY2028. CSW has a good cash flow conversion, as the company’s capital expenditure needs are quite low. The mentioned estimates along with a weighed average cost of capital of 9.38% craft the following DCF model with a fair value estimate of $177.65, with the estimated price being incredibly close to the stock price at the time of writing:

{kind=link}

The used weighed average cost of capital is derived from a capital asset pricing model:

CAPM (Author's Calculation)

In Q2, CSW had $4 million in interest expenses. With the company’s current amount of interest-bearing debt, CSW’s interest rate comes up to an annualized figure of 7.64%. The company uses debt quite moderately – I estimate a long-term debt-to-equity ratio of 10%, quite near the current figure.

On the cost of equity side, I use the United States’ 10-year bond yield of 4.88% as the risk-free rate. The equity risk premium of 5.91% is Professor Aswath Damodaran’s latest estimate made in July. Yahoo Finance estimates CSW’s beta at a figure of 0.77 . Finally, I add a small liquidity premium of 0.35%, crafting a cost of equity of 9.78% and a WACC of 9.38%.

Takeaway

CSW’s acquisition strategy seems well thought-out as the company’s distribution network increases the acquisitions’ value. My DCF model currently estimates CSW’s stock to be priced correctly when considering the company’s organic performance. It is important to note that the DCF model doesn’t factor in acquisitions; historically, CSW’s acquisitions have created a significant amount of shareholder value. Further acquisitions could prove the DCF model’s estimated fair value as too low. For the time being, though, I don’t see further acquisitions as too large of a catalyst for a buy rating. For the time being, I have a hold rating for the stock.

For further details see:

CSW Industrials: Waiting For Further Value-Creating Acquisitions