CTEC - CTEC: Clean Tech Equities Are Undervalued But Volatile

2023-04-20 03:25:31 ET

Summary

- CTEC invests in clean technology companies.

- I think CTEC's portfolio is interesting and likely undervalued, with a strong IRR on offer for long-term shareholders.

- However, CTEC is still an unpopular, illiquid (costly to transact), and volatile fund. That makes CTEC potentially a risky proposition.

- Therefore, while I would be bullish on CTEC from a valuation standpoint, volatility-adjusted returns may not be so exciting; opportunistic purchases are recommended over immediate buys.

Global X CleanTech ETF ( CTEC ) is an exchange-traded fund designed to provide investors with exposure to companies expected to benefit from increased adoption of green technologies designed to reduce or inhibit negative environmental impacts. Per Global X : "This includes companies involved in renewable energy production, energy storage, smart grid implementation, residential/commercial energy efficiency, and/or the production and provision of pollution-reducing products and solutions."

The fund is concentrated, with 41 holdings reported as of April 18, 2023. The 30-day median bid/ask spread is also helpfully reported by Global X, being 0.51% at the time of writing, which is a hefty indirect fee of investing in this fund which evidently is not particularly liquid. That's materially higher than the 30-day SEC yield of 0.29%. Net assets as of April 18, 2023 were $117.42 million. The fund was set up in late October 2020, and has therefore since attracted only about $100 million. This is a fine start, but CTEC is not especially popular.

CTEC's top 10 holdings are listed below, which interestingly include plenty of companies engaged in the solar industry. This makes the fund interesting to me, at least, as solar has a promising future. Our sun is a star that essentially serves as a free nuclear fusion reactor "in the sky". It makes sense that solar will become increasingly relevant in the coming years and decades, especially as the technology (hopefully) improves, allowing us to capture and harness more of the energy provided by the sun.

{kind=link}

Enphase Energy, Inc. ( ENPH ) is the top holding. This is an American company based in California that develops and manufactures solar micro-inverters, battery energy storage, and EV charging stations primarily for residential customers. A solar micro-inverter is a small electronic device used in photovoltaic solar energy systems to convert DC (Direct Current) electricity produced by solar panels into the AC (Alternating Current) that can be fed into our electrical grid and used by households. First Solar, Inc. ( FSLR ) is another major holding; an American manufacturer of solar panels, utility-scale photovoltaic power plants, and provider of supporting services.

While CTEC is concentrated on the whole, its top 10 are actually fairly balanced. This is important to note, as it means that the single-name risk is not overwhelming. Plenty of smaller funds, if you look into their portfolios, are heavily dependent on single names, which is not really the case for CTEC.

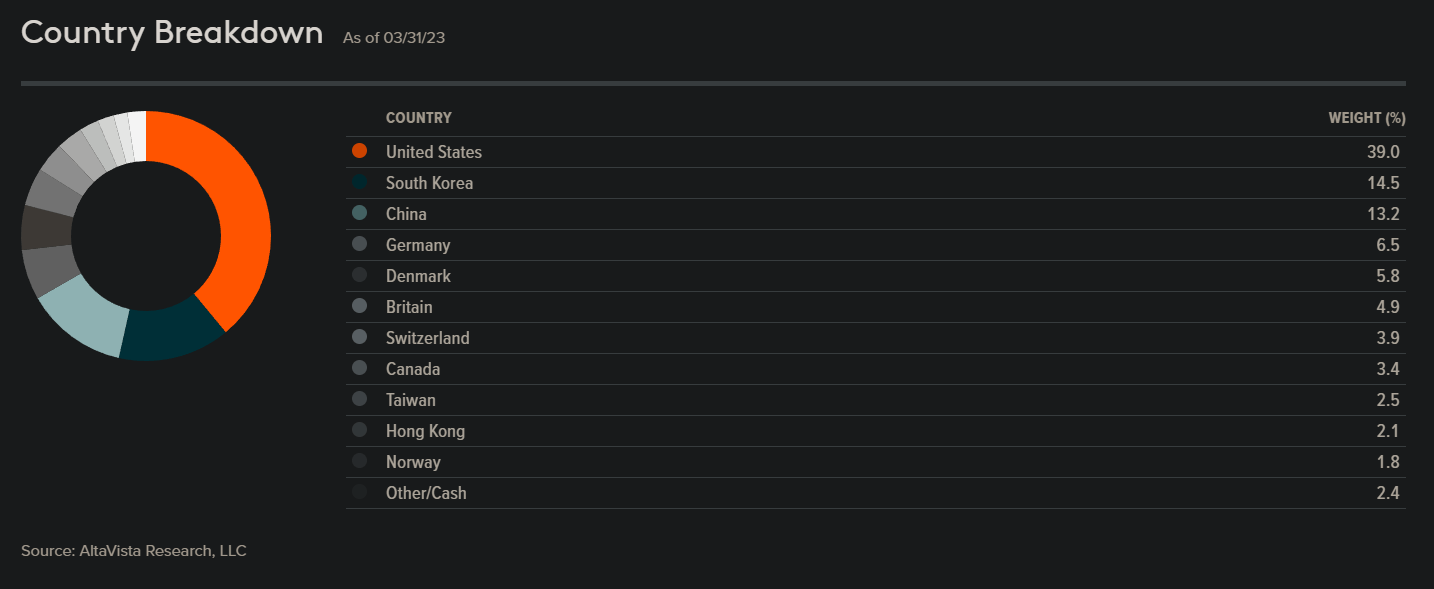

The fund is geographically diverse (see table below), with the United States representing 39% of the fund, followed by South Korea (14.5%), China (13.2%), Germany (6.5%), Denmark (5.8%), and others.

{kind=link}

I have calculated, at the time of writing, a fund-weighted 10-year yield (as a proxy for the fund's geographically weighted risk-free rate) of 2.90%. I also use data from Professor Damodaran to assign a weighted equity risk premium of 5.09%.

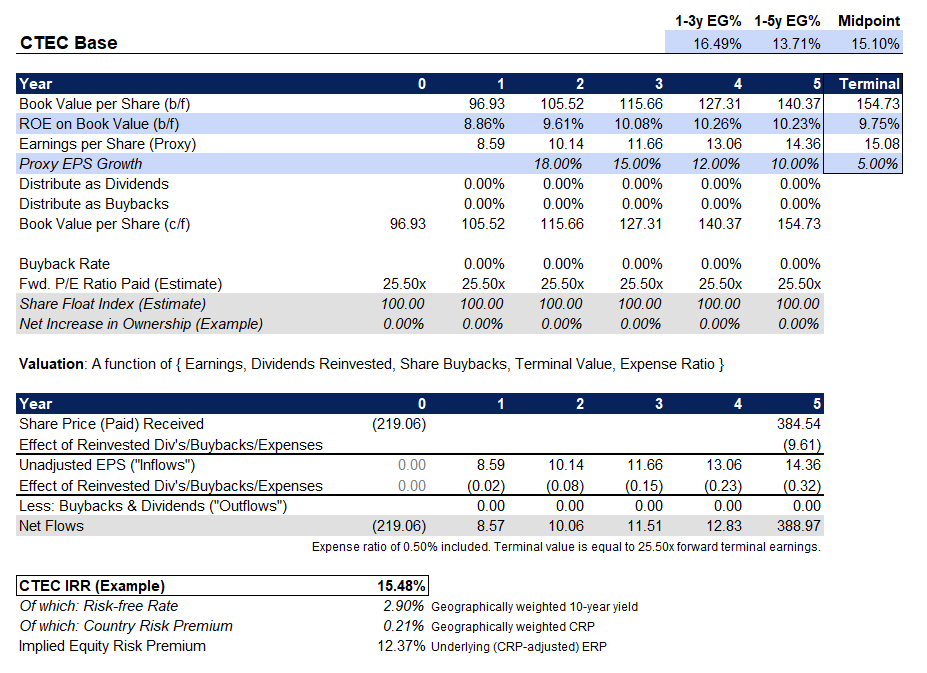

There are several conflicting sources for price/earnings ratio for CTEC's portfolio. I am therefore going to focus on forward earnings, and use a less flattering estimate of 25.50x reported by Global X (the ETF provider) themselves (not paying attention to trailing earnings). Dividend data is also mixed. I am going to make no substantial assumptions, but use the somewhat rosy consensus three- to five-year earnings growth rate from Morningstar of 21.17% as a basis. I will assume no dividends or share buybacks, and a slightly improving return on equity from 8.86% (currently estimated) to circa 10% over the next few years. This means my average earnings growth rate is closer to 15% than Morningstar's consensus of over 20%.

All considered, this provides me with a headline IRR estimate of 15.48%, which is strong, with an implied net equity risk premium of 12.37% (which is generally speaking very high).

{kind=link}

I think the long-term future of CTEC is probably quite good, so it perhaps makes some sense to use a longer forecast time horizon than I have used here. Nevertheless, this does in some way enable me to take a more conservative approach, with a lesser average earnings growth rate (tailing off somewhat harshly toward the end), and keeping only a relatively modest return on equity of 10% (or less) for the fund. I have kept the forward price/earnings multiple the same, though, which is probably not unfair given the longer-term potential of CTEC's portfolio's technologies and the likely longer-term time horizon (in respect of earnings growth potential and trajectory).

The beta of the fund is approximately 1.4x relative to the S&P 500. So, we could in theory take the 15.48% IRR implied above, subtract the 2.90% weighted risk-free rate, and adjust the gross balance (ERP: 12.58%) for 1.41x beta as reported by Global X. This would land a tighter adjusted ERP of 8.92% vs. our CRP-adjusted ERP of 12.37% (presented at the bottom of the chart above). An adjusted ERP of 8.92% sounds closer to reality, but it is still high in relation to what I would consider a fair adjusted ERP of 4.2-5.5% for equities. So, all considered I think CTEC is probably undervalued.

On the other hand, historical data for CTEC since inception indicates a standard deviation of some 41%, and still some 38% on a 20-day basis. So, CTEC continues to trade in an erratic way. It could be the case that volatility will be suppressed later as the fund becomes more popular, which is certainly possible, but an IRR of circa 15% is therefore not likely to come without volatility. This makes CTEC fairly unattractive in relation to its trailing volatility; timing therefore becomes a bit more important, potentially.

CTEC is down year-to-date by about -6% at the time of writing. I reckon that CTEC could be undervalued with the potential for perhaps 20-40% upside based on valuation alone (with perhaps an IRR of at least 15% to fall back on for a longer-term hold). With under-valuation and recent downside, forward volatility may well benefit shareholders. Therefore, I would take a bullish outlook, but not very bullish: even with an IRR of 20%, for example, the large volatility involved in this still unpopular fund (with a high bid-ask spread) makes CTEC not for the faint of heart.

For further details see:

CTEC: Clean Tech Equities Are Undervalued But Volatile