CTPTY - CTEEP: A Cautious Outlook On The Dividend Thesis In The Current Scenario

2024-01-20 00:00:19 ET

Summary

- Companhia de Transmissão de Energia Elétrica Paulista is a Brazilian utility company engaged in electric power transmission.

- CTEEP's investment thesis is supported by its focus on energy transmission, high cash generation, revenue indexed to inflation, and a robust track record in dividend payments.

- The company benefits from the resilience of the electricity sector, employing the RAP model for revenue, and has shown substantial growth in Annual Permitted Revenue over the years.

- While CTEEP has historically been a strong dividend payer, a substantial investment plan may impact dividends. Considering potential risks, a hold stance is recommended for investors.

Companhia de Transmissão de Energia Elétrica Paulista (CTPTY), also known as ISA CTEEP, or just CTEEP, is a Brazilian private-public utility concession company engaged in electric power transmission. The company constructs, operates, and maintains electric transmission systems and related infrastructure projects throughout Brazil through its subsidiaries.

CTEEP divides its operations into Infrastructure, Operation & Maintenance, and Concession Assets Remuneration business units. Most of the company's revenue comes from its Operation & Maintenance division, which oversees the nationwide electricity transmission system.

The company also plays a crucial role in transmitting a significant portion of Brazil's power production and more than half of the energy consumed in Southeast Brazil.

Key positive aspects supporting the investment thesis for CTEEP include:

- Operations focused on energy transmission, reducing exposure to fluctuations in electricity prices caused by factors like rainfall and reservoir levels.

- High cash generation with a degree of predictability.

- Revenues indexed to inflation, providing shareholders protection against systematic increases in price indices.

- Noteworthy track record in dividend payments, forming the basis of a bullish thesis.

However, it is essential to highlight the potential drawbacks of investing in CTEEP. The primary concern is the influence of the government in its sector of operation, leading to uncertainties about the company's shares. High charges in the energy segment and increased competition in future transmission auctions could also impact the return on lots won.

In 2023, CTEEP demonstrated exceptional performance among electricity stocks in Brazil. The company had a remarkable year characterized by a significant improvement in operating costs, the operational startup of lines ahead of schedule, and better-than-expected performance of investments according to ANEEL (Brazil's National Electric Energy Agency) expectations.

TRPL4 (Ibovespa) CTPTY (OTCMKTS) (TradingView)

{kind=link}

Despite the positive developments, 2024 appears less promising for the dividend thesis. The company's robust investment plan for the next five years raises uncertainty about its ability to maintain leverage below 3x net debt EBITDA while still paying out a minimum of 75% of its profits. Even if the company achieves this, the consensus suggests that the profits generated in 2024 may yield close to 5%. Considering the current share price and the expected return for an income stock like CTEEP, I find this less attractive.

CTEEP's Transmission Sector: Resilience and Robust Revenue Growth

The transmission segment in the electricity sector holds a significant competitive advantage, primarily due to its lower exposure to hydrological risks and fluctuations in electricity prices. CTEEP leverages this advantage effectively, positioning itself exceptionally well compared to other companies in the Brazilian sector. CTEEP exclusively operates in the transmission segment, further enhancing its competitive standing.

The resilience of companies in the electricity sector is fortified by the adopted remuneration model known as RAP. Under this model, the revenue for transmission companies is contingent on the availability of the service rather than the quantity of energy transmitted. When signing transmission contracts, ANEEL determines the RAP amount each transmission company will receive.

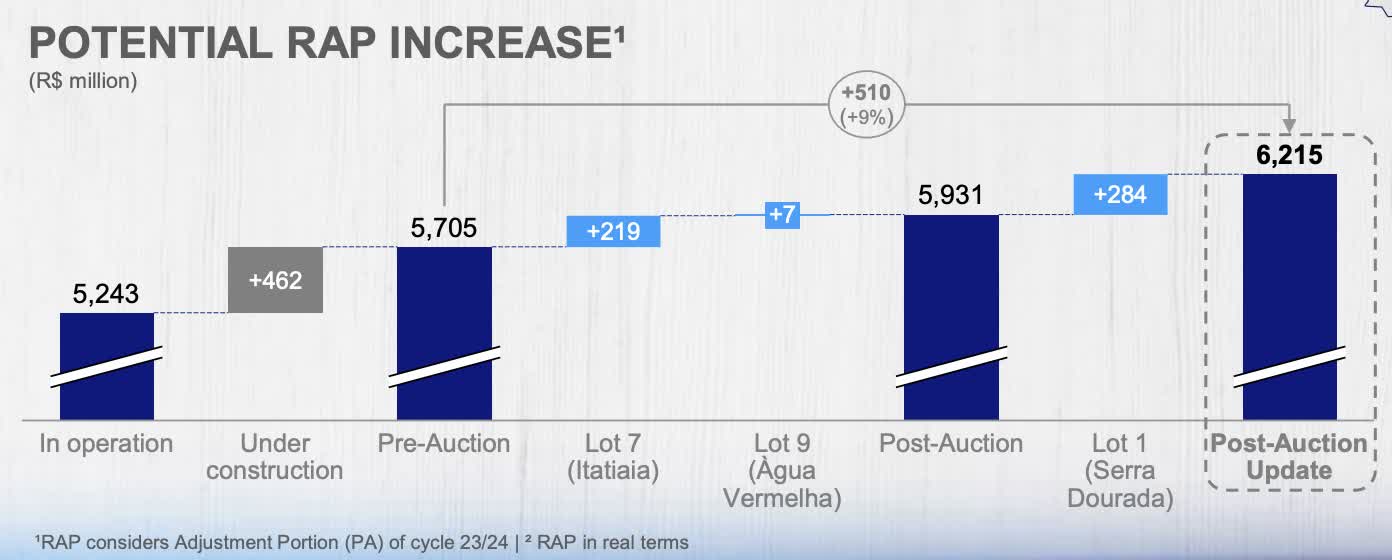

CTEEP emerges as one of Brazil's most prominent companies in Annual Permitted Revenue. Its extensive portfolio and strategic distribution of assets across various country regions contribute significantly to this privileged position. Despite its consolidated standing, the company remains proactive in seeking growth opportunities, participating actively in transmission auctions, and exploring new acquisitions. CTEEP's Annual Permitted Revenue ("RAP") has grown substantially, from R$800 million in 2013 to R$6.2 billion in 2023.

{kind=link}

The company's growth is primarily driven by the effective management of the renewed contract, specifically Contract 059/2001. With unique characteristics and involving assets in the state of São Paulo, this contract ensures predictable revenue, enabling continuous investment to maintain system reliability.

These investments contribute to the expansion of the asset base, consequently increasing revenue from the existing investment in São Paulo. Analyzing Contract 059/2001, a notable increase from R$539 million in the 13/14 cycle to R$1.3 billion in the 23/24 cycle indicates significant growth potential with a Compound Annual Growth Rate ("CAGR") of 9.2%.

In terms of new concessions, the company witnessed an increase from R$327 million in the 13/14 cycle to R$1.6 billion in the 23/24 cycle, reflecting substantial growth with a CAGR of 17.0%. The historical São Paulo contract (059/2001) accounted for 61% in the 13/14 cycle, while in the 23/24 cycle, this share diluted to 45% of the total RAP, illustrating diversification by contract type.

Lots Secured and Ongoing Projects: CTEEP's Expansion in the Electricity Transmission Sector

CTEEP strategically expands its presence in the electricity transmission sector through participation in auctions, where the company acquires lots, gaining the right to develop and operate power transmission projects associated with those lots. Regulatory agencies like the ANEEL in Brazil organize these auctions, where companies submit bids for infrastructure projects like transmission lines.

In 2023, CTEEP secured three lots:

-

Lot 01: Involving the Serra Dourada Project in Bahia and Minas Gerais, covering 1,116 km of transmission lines. The completion deadline is 66 months, with an estimated investment of R$3.1 billion. The project is expected to generate 5,739 jobs and an RAP of R$283.8 million.

-

Lot 07: Encompassing Rio de Janeiro and Minas Gerais, this lot includes 1,044 km of double-circuit transmission lines (522 km for each circuit). The completion deadline is 66 months, with ANEEL's CapEx at R$2.3 billion. The project is expected to create 4,182 jobs and achieve a RAP of R$218.9 million.

-

Lot 09 : Involving the Água Vermelha project in Minas Gerais, with a 36-month execution period. Aneel estimates the investment at R$94 million, contributing to 313 jobs and providing a RAP of R$7.8 million.

CTEEP's ongoing project portfolio includes seven units totaling 2,700 kilometers of transmission lines and 7,100 MVA in transformation capacity. It also encompasses the construction of eight substations. As per Aneel, the planned investment in CapEx is R$10.6 billion, with an RAP of R$972 million.

In total, CTEEP is committed to 257 projects, representing a total investment of R$15.6 billion ($3.2 billion).

CTEEP has distinguished itself by implementing pioneering technologies in the Brazilian basic grid, including the country's first digital substation in 2021, the first large-scale battery storage project in 2022, and Brazil's first 4.0 substation in 2023. As part of its new business focus, CTEEP concentrates on battery energy storage, offering operational flexibility, reduced dependence on hydroelectric plant reservoirs, quick implementation, lower operating costs, optimized investments, and reduced greenhouse gas emissions.

Robust Cash Generation and Dividend Distribution

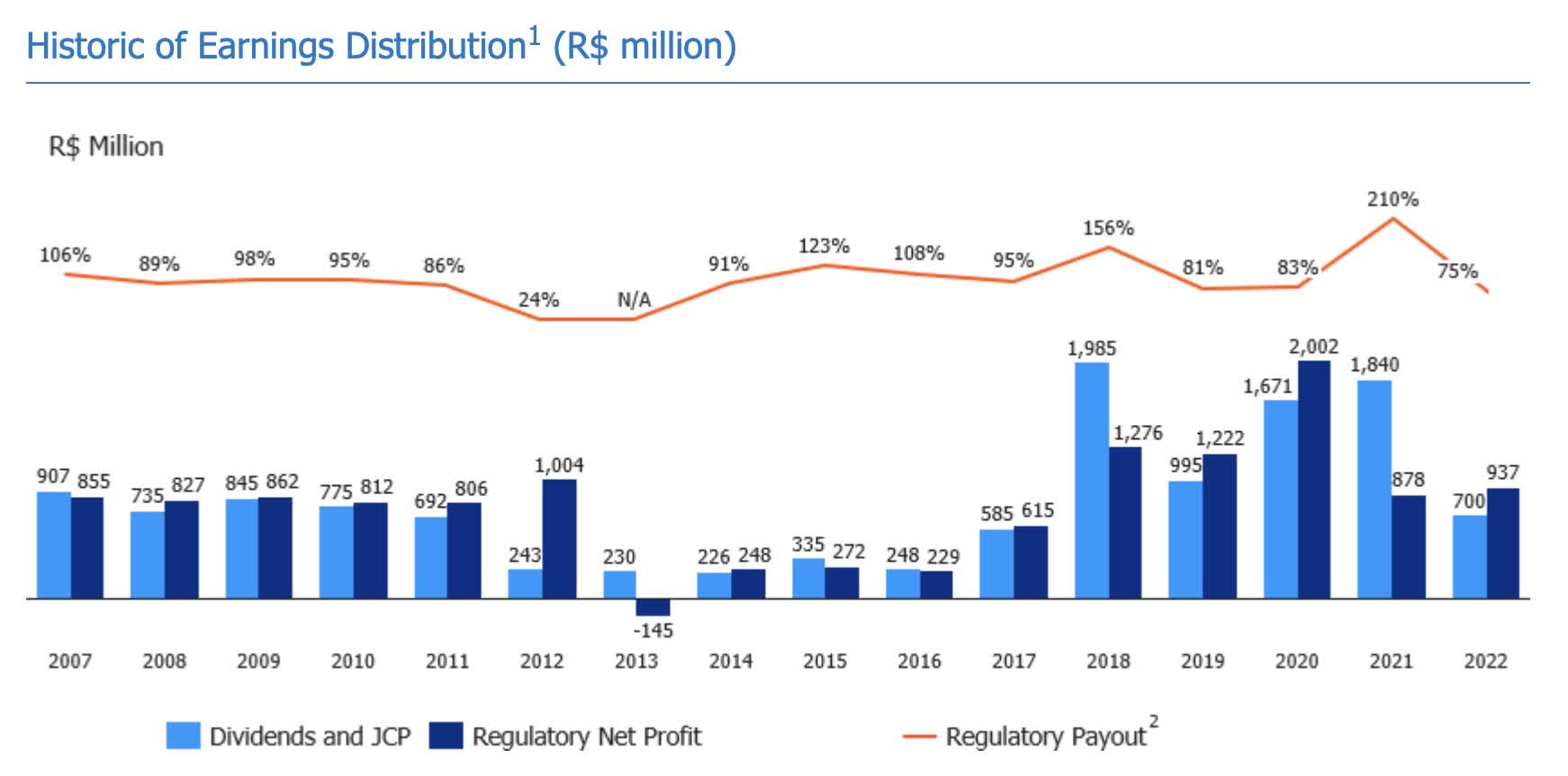

One of the critical elements of CTEEP's investment thesis lies in its strong corporate governance, robust cash generation, and a significant record of distributing dividends. Even during economic recessions, CTEEP's results have demonstrated resilience, attributed to a predictably high cash generation stemming from its robust business model.

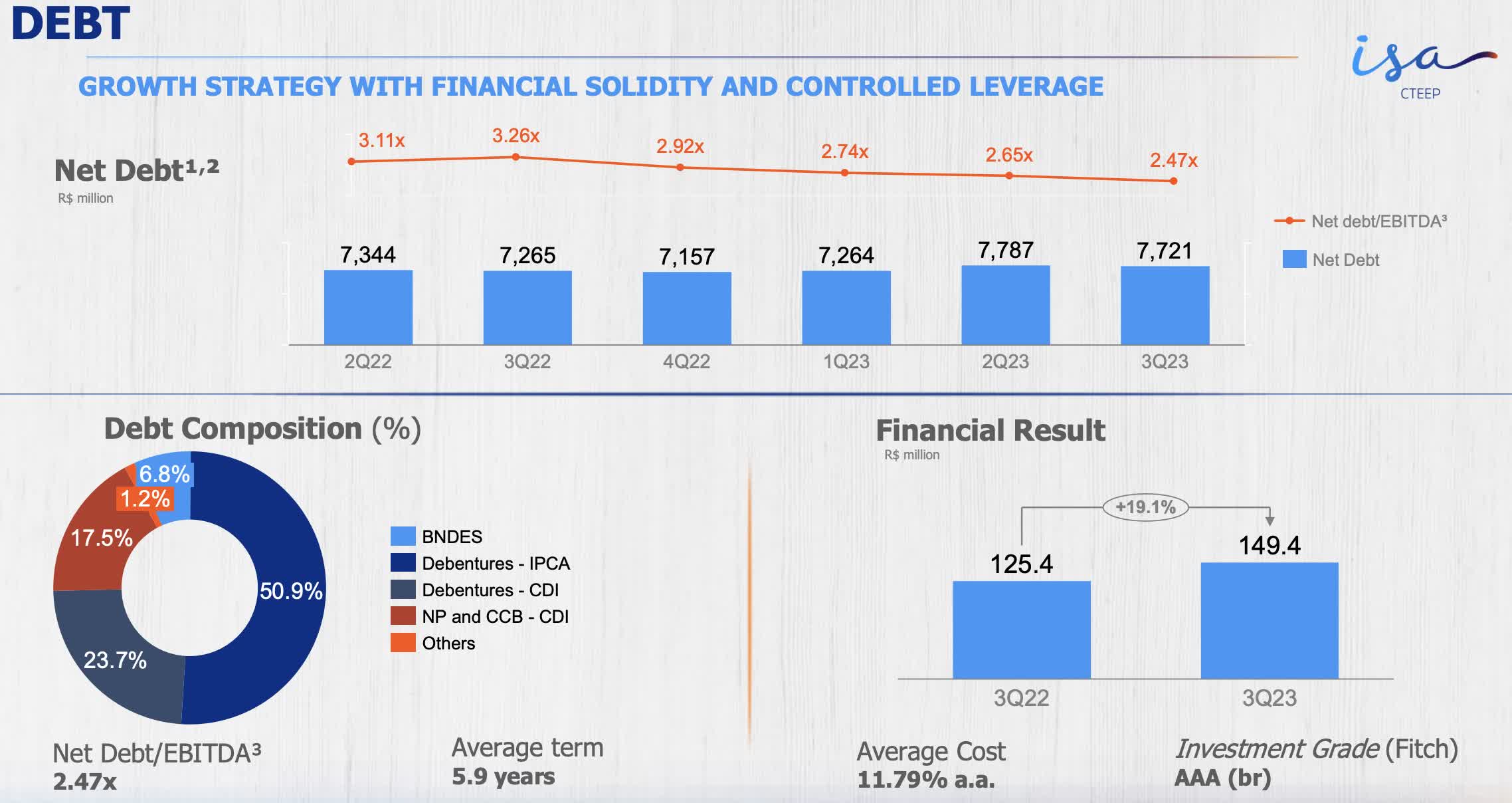

The upcoming years will likely be characterized by a substantial investment of R$15 billion over the next five years, exerting pressure on CapEx. This, in turn, could impact the company's leverage and potentially lead to more conservative dividend payouts.

The level of financial leverage holds significance in light of the current dividend policy, which dictates a distribution of 75% of regulatory net profit as long as leverage remains below three times Net Debt/EBITDA.

Presently, CTEEP maintains controlled leverage, with a net debt/EBITDA ratio of 2.47x. This metric has progressively decreased since 2022, with an average cost of debt at 11.7%.

{kind=link}

Considering the dividend outlook, the likelihood of extraordinary dividend payments seems improbable. Nonetheless, considering that the company refrained from distributing dividends only in 2013, a year marked by financial losses, it is reasonable to expect that CTEEP will uphold a resilient dividend payout for 2024.

{kind=link}

If the company maintains leverage below or close to 3x and adheres to the 75% payout policy, CTEEP could potentially achieve a yield of 5% in 2024. This projection is derived from the Koyfin platform, which considers the S&P Global Intelligence consensus. The consensus anticipates a net profit of $295 million for the year.

{kind=link}

The Bottom Line

CTEEP's investment thesis, anchored in its robust cash flow and consistent revenues from the energy transmission segment, positions it as a valuable income stock for portfolio inclusion. Despite concentrated risks related to government decisions and potential sector interference, the indirect nature of transmission companies with the end consumer helps mitigate direct impacts even amid changes.

However, with CTEEP currently navigating a cycle guided by a substantial investment plan that may impact liquidity, there is an anticipation that, while still positive, dividends may not reach the levels observed in recent years.

Considering a Return on Investment ("ROI") of 6%, seen as an attractive benchmark for dividends, and a 75% payout, the calculated target price for CTEEP is $5.60. This figure is 16% below the current ADR trading price of $6.50 as of January 17th.

Nevertheless, by incorporating the average P/E ratio of 8.8x over the last ten years and a P/B ratio of 1.17 for the same period and adapting it according to the Graham valuation method, the fair value for CTEEP's ADR should be $6.38. This suggests a margin of safety that is practically negligible or essentially non-existent.

Given the uncertainties and potential risks leading to a minimum payout in 2024, there seems to be little reason for immediate enthusiasm about CTEEP as an income stock. Consequently, I recommend a hold stance for investors contemplating the addition of CTEEP to their dividend portfolios, at least for the time being.

For further details see:

CTEEP: A Cautious Outlook On The Dividend Thesis In The Current Scenario