XBI - CTI BioPharma: Limited Cash Runway But Better Than Expected Commercial Launch

Summary

- CTI BioPharma has reported a better-than-expected Q3 print of 18.5M, which is a 40% growth QoQ, and we expect this growth to continue reaching close to USD60M in FY2022.

- CTIC’s Vonjo (Pacritinib) is a differentiated late-stage JAK2/IRAK4/FLT3/CSF1R inhibitor for the treatment of myelofibrosis in patients with severe thrombocytopenia (platelets <50,000/?L).

- Recent ASH data demonstrated that Vonjo is 4 times more potent in the anemia-reducing mechanism of action compared to competitor momelotinib; this could mean a larger market share in the future.

- The commercial print looks promising, and the company seems like it has a short cash runway with $81M cash (Q3 22) and a cash burn of around 130-140M.

- We upgrade to a hold rating (from a sell rating) due to the cash runway, although, we are net net positive about the commercial ramp.

Company background

CTI BioPharma ( CTIC ) is a commercial-stage (pre-cashflow positive) biotechnology company focusing on developing treatments for blood cancers. On Feb 2022, CTIC received accelerated approval for its lead clinical candidate, Vonjo (Pacritinib). Vonjo is a JAK2/IRAK4/FLT3/CSF1R inhibitor that received a label for the treatment of myelofibrosis in patients with severe thrombocytopenia defined as platelets <50,000/?L, which the current standard of care treatment such as Jakafi are not indicated in (patients under platelet counts <100,000/?L) due to its impact on anemia and thrombocytopenia. Anemia is a reduction in red blood cells, and thrombocytopenia is a reduction in platelet counts. The market launch started on March 2022. Seven months since the market launch, the company generated USD32M (7 months), and we expect this robust growth trajectory to continue during Q4 2022 and 2023 with i) Vonjo (Pacritinib) being included in NCCN guidelines (during Q2 2022), ii) new data around anemia presented during ASH 2022 conference, and iii) increase in covered lives >80% of the population.

New data published in ASH 2022 bodes well for Vonjo's commercial adoption

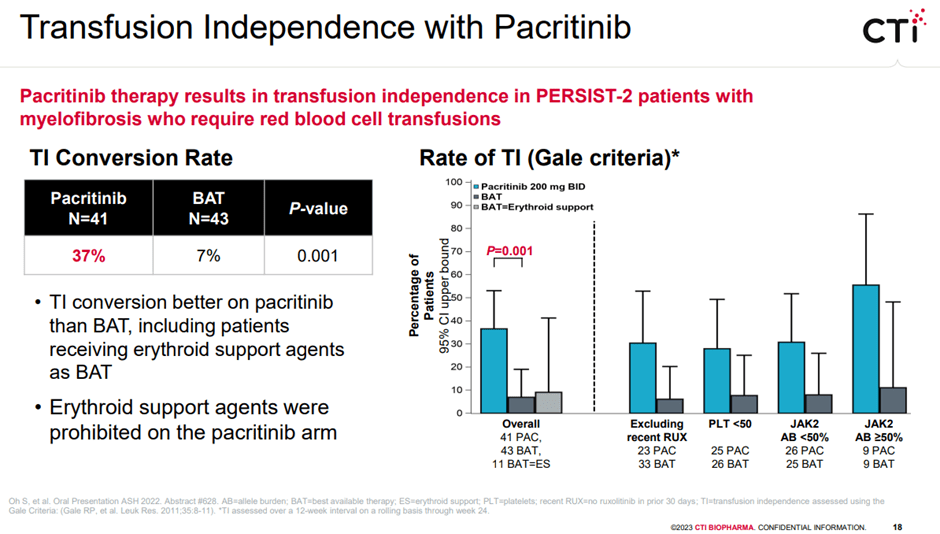

Last December , CTIC presented in-depth data from Vonjo's posthoc analysis that highlighted anemia benefits from the phase 3 PERSIST-2 trial and also presented PK/PD data during ASH 2022 annual meeting. The key takeaways from the presentation were i) Vonjo's anemia benefit in the myelofibrosis population, higher transfusion-independent patient population vs. baseline in PERSIST-2 trial vs. best available therapy (BAT), ii) OS survival trend data that highlights that patients who were not transfusion independent at baseline on Vonjo improved survival trend vs. BAT (HR=0.61, 95% CI), and iii) higher potency in ACVR1 inhibitor (4 times more potent than momelotinib from GSK ( GSK )). We highlight that both Gale and SIMPLIFY criteria showed 37% of patients turning transfusion independence vs. 7% in the BAT group between week 12 to week 24 (achieved during the first 12 weeks and leading into week 24), which we believe is comparable to momelotinib.

{kind=link}

According to the publication, anemia benefit seems to be driven by ACVR1 as ACVR1 reduces hepcidin production, which in turn increases iron available to erythropoiesis. Furthermore, RAK1 inhibition contributes to the reduction in downstream erythropoiesis, especially IL-6, which also impacts hepcidin expression. This data put momelutinib's market positing at risk as we believe this opens up the door for potential off-label prescribing of Vonju in MF patients with anemia, where physicians may prescribe Vonju over momelutinib due to its cleaner label without peripheral neuropathy concerns. Of note, momelutinib's PDUFA is planned for June 2023.

Previous data from PERSIST-2 trial

JAMA ONCOLOGY 2018 PERCIST 2 trial publication (Corporate Deck)

{kind=link}

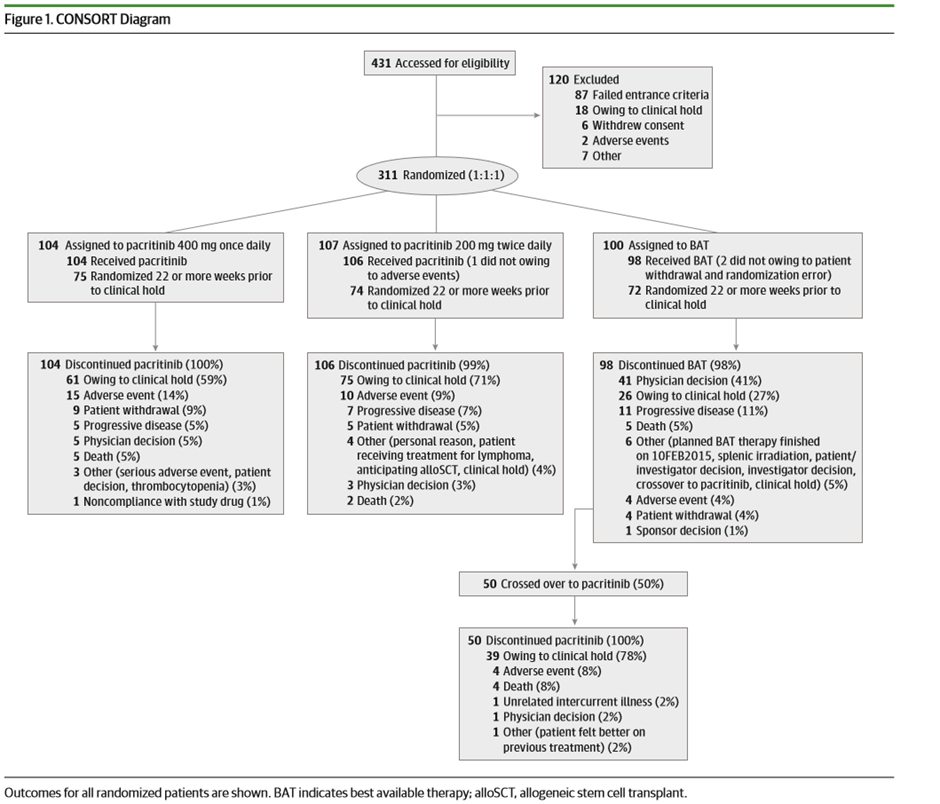

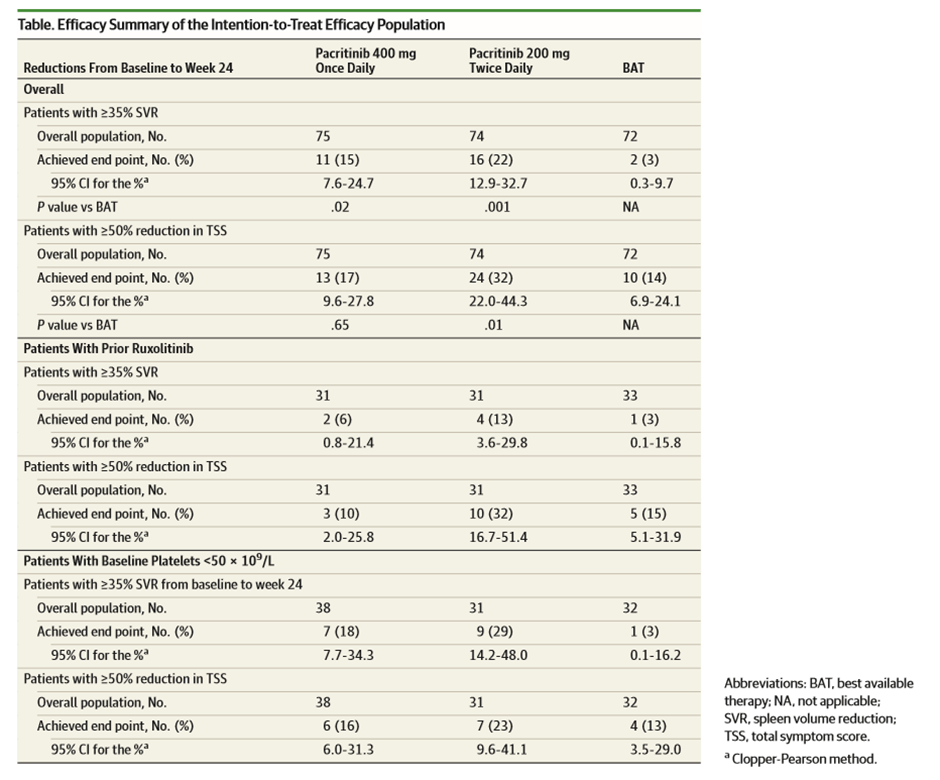

PERCIST trial was a phase 3 pivotal trial with 311 patients (>99% powered for SVR and TSS) that was designed to compare the efficacy and safety of JAK2 inhibitor Vonjo with the best-available therapy (BAT), including standard-of-care ruxolitinib, in a patient population with myelofibrosis and thrombocytopenia (platelet count <100x10^9/L). We highlight that in the BAT group, around 48% of the patients were on ruxolitinib, and 19% of patients received watchful waiting only. Key results were i) spleen volume reduction ((SVR)) of 35%, ii) 50% or more in total symptom score ((TSS)) at week 24, both endpoints were statistically significant, and iii) clinical improvement in hemoglobin and reduction in transfusion burden were greatest with pacritinib twice daily dosing. Regarding overall survival results, even though statistical significance was not met, the trial showed that the overall death rates were lower for those who crossed over to Vonjo from the BAT arm and the subgroup analyses for survival by risk factors showed that hazard ratios for pacritinib twice daily were less than 1 (with the exception of patients who were more than 1.5 years from diagnosis or secondary myelofibrosis).

JAMA ONCOLOGY 2018 PERCIST 2 trial publication (Corporate Deck)

{kind=link}

For the patient population under <50x10^9/L, all hematological adverse event rates were lower in the Vonjo arm vs. BAT. Interestingly for once-daily dosing, patients experienced a higher degree of thrombocytopenia, anemia, and discontinuation vs. BAT; this forms the basis for Vonjo's BID dosing regimen. Some limitations of the trial design were, due to clinical hold, efficacy endpoints collected at week 24 were limited, impacting the sample size and compromised time-to-event endpoints (including overall survival) by reducing follow-up times for assessment that would enable analyses that follow the intention-to-treat principle.

The competitive landscape looks favorable

Even though several combinations and monotherapy are being developed, except for momelutinib from GSK, we do not see potential competition with Vonjo as they are not specifically targeting their trials for the thrombocytopenia patient population.

Combination approach

- MorphoSys's ( MOR ) pelabresib (CPI-0610): phase 3 data coming out in 2024, and does not seem to enroll patients with platelet count <100x10^9/L. At best, we expect approval in 2025, which is couple of years down the road, and we do not believe it competes with Vonjo's market share.

- Incyte ( INCY ) is evaluating its own BET inhibitor that can be used in combination with Jakafi, which is only going through phase 1 at the moment.

- Incyte also has a phase 3 asset, PI3K inhibitor parsiclisib, that is being studied as a combo therapy with ruxolitinib in patients who are inadequate responders to ruxolitinib. We expect the data to come out in 2023. For this candidate, we believe the classwide safety overhang is a key concern, as we have seen with Incyte withdrawing NDA in Marginal zone lymphoma, Follicular lymphoma, and Mantle cell lymphoma.

- AbbVie ( ABBV ) has also released phase 2 data of navitoclax, Bcl-2 inhibitor, that is being combined with ruxo in JAK naïve myelofibrosis patients. The trial data was fairly robust (63% of patients with SVR >35% at week 24). Interestingly, the drug has demonstrated a reduction in i) symptom burden, ii) bone marrow fibrosis, and iii) benefit in anemia.

- Roche is developing a PRM-151, a recombinant pentraxin-2 molecule, that is currently going through phase 1 and being studied in combination with ruxo.

Mono therapy under development

- Geron Corporation's Imetelstat, a first-in-class Telomerase inhibitor, has shown impressive symptom response and overall survival benefit in the phase 2 Imbark trial in the moderate to a high-risk patient population who have relapsed after JAK inhibitor. Phase 3 ImpactMF trial of this drug is targeting 2L patients who relapsed after JAK and have a BAT arm that excludes JAK inhibitors.

- A phase 2 asset Bomedemstat, LSD1 inhibitor, has shown robust data across symptom volume, bone marrow fibrosis, and anemia in the second-line myelofibrosis patient population.

Risks

Clinical risk: potential unknown side-effects can emerge during post-market surveillance, competitive risk: GSK's momelutinib may come out with long-term efficacy and safety data superior to Vonjo, potentially diluting Vonjo's market; capital raise risk: if Vonjo's sales don't ramp up enough, there could be more stock dilution hurting the stock price.

Conclusion

We continue to like Vonjo's clinical profile and better than expected sales ramp that the company has demonstrated during the last seven months of launch. However, due to a limited cash runway and increased valuation, we remain on the sidelines until we see a few more months of data and a clear sign of profitability. That being said, we continue to believe that CTIC will trend higher during the next 12-24 months, with an increase in the adoption of Vonjo and an increase in off-label prescribing. Furthermore, we believe a potential interesting BD deal could be a possibility, either the company buying other early-stage assets (i.e., BET inhibitors) or the company getting bought.

For further details see:

CTI BioPharma: Limited Cash Runway, But Better Than Expected Commercial Launch