PINE - CTO Realty Growth: Reliable Yield Play With Upside Potential

2023-10-10 05:54:12 ET

Summary

- CTO Realty Growth is a unique REIT that originated from Consolidated-Tomoka Land Company, with a history in land development, oil and gas, agriculture, and forestry.

- In 2019, CTO took steps to refocus its business, including selling stakes in undeveloped land and spinning off net-lease properties.

- CTO converted to a REIT in 2020, leading to an increase in dividends and a focus on income-producing real estate.

Summary

CTO Realty Growth (CTO) is a retail-focused REIT with a portfolio predominantly located in the Sunbelt. Having a corporate history spanning >100 years, CTO has been through several major transformations. In its current form as a REIT focused on income producing properties, CTO has only been around for three years. I believe CTO's small size, confusing history, and remnants of its past have contributed to its obscurity. Having undertaken a critical overhaul of the business over the past three years, CTO is now positioned as a nearly pure-play retail and mixed-use REIT. However, the market has been slow to price it as such. At its current valuation, CTO offers investors the opportunity to acquire a steadily growing, well-managed REIT at an attractive going-in yield with a wide margin of safety and capital appreciation potential.

Background & Context

CTO is the successor entity to the Consolidated-Tomoka Land Company, which itself was the successor entity to the Consolidated Naval Stores Company. Consolidated Naval began operating in 1902 as a producer of turpentine and other pine derivatives. Consolidated Naval formed a subsidiary called the Tomoka Land Company in 1910. In 1961, Consolidated Naval rebranded as Consolidated Financial Corporation. In 1969, Consolidated Financial changed the name of the Tomoka Land Co. to Consolidated-Tomoka and listed a minority stake in the subsidiary on the AMEX. By 1998, Consolidated-Tomoka had divested its forestry assets to focus on its real estate business, which included residential, commercial, industrial, and golf course properties, predominantly in Florida. A detailed timeline of the Company's history can be viewed here .

In 2019, Consolidated-Tomoka began a significant corporate makeover. It took several major steps to refocus the Company, simplifying the story for investors and unlocking hidden value. First was the sale of a 66.5% stake in its 5,300 acre portfolio of undeveloped land in Daytona Beach to Magnetar (the remaining 33.5% stake was sold in 2021 to Timberline). Next was the spin-off of a portfolio of net-lease properties into Alpine Income Property Trust (PINE). The Company retained a 22% stake in PINE as well as the external management contract. Finally, it disposed of its remaining golf properties and changed its name to CTO Realty Growth, signalling the beginning of a new, refreshingly clean, chapter in the Company's history.

While the events of 2019 did much to set CTO on the path of shareholder value creation, there was still work to do. CTO was still structured as a corporation and held many assets incongruent with its focus on income-producing real estate (e.g., subsurface mineral interests , mitigation credits for losses of endangered species on land parcels, loan interests, etc.).

CTO converted to a REIT in December 2020, prompting an increase in the annual dividend from $0.12 to $0.91 and the payment of a special dividend of $11.83 per share in cash and stock (n.b., ~80% of the average VWAP from announcement to shareholder approval). Since the REIT conversion, CTO has increased its dividend ~67% to $1.52 per year.

As of Q2 2023, ~95% of revenue is generated from income producing real estate and management fee income from PINE, with the remainder coming from loan income and other activities. CTO still owns ~$2MM of mitigation credits, and $0.4MM of subsurface mineral rights (n.b., 352k acres), though it continues to sell these assets down consistently.

REIT Overview

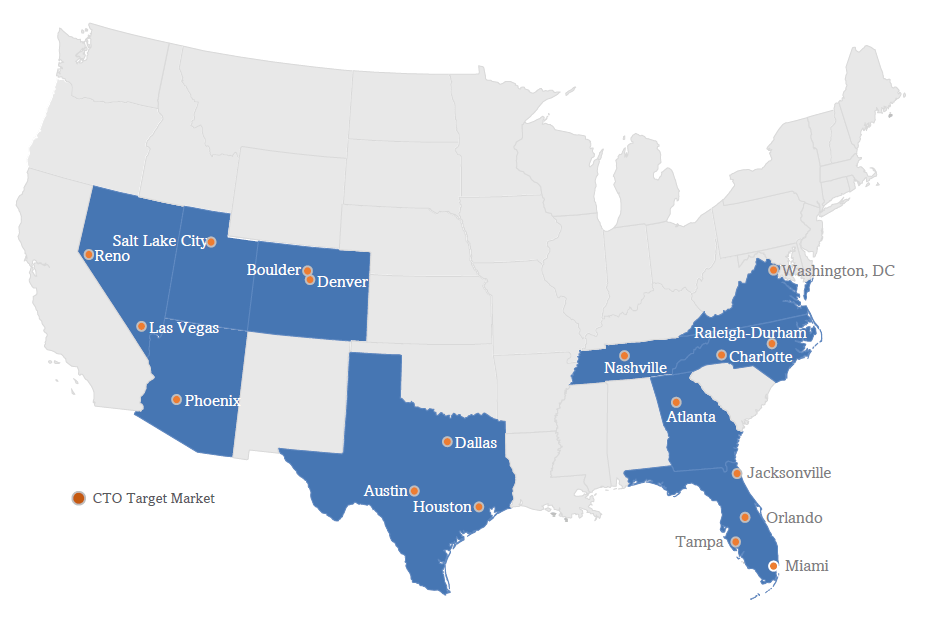

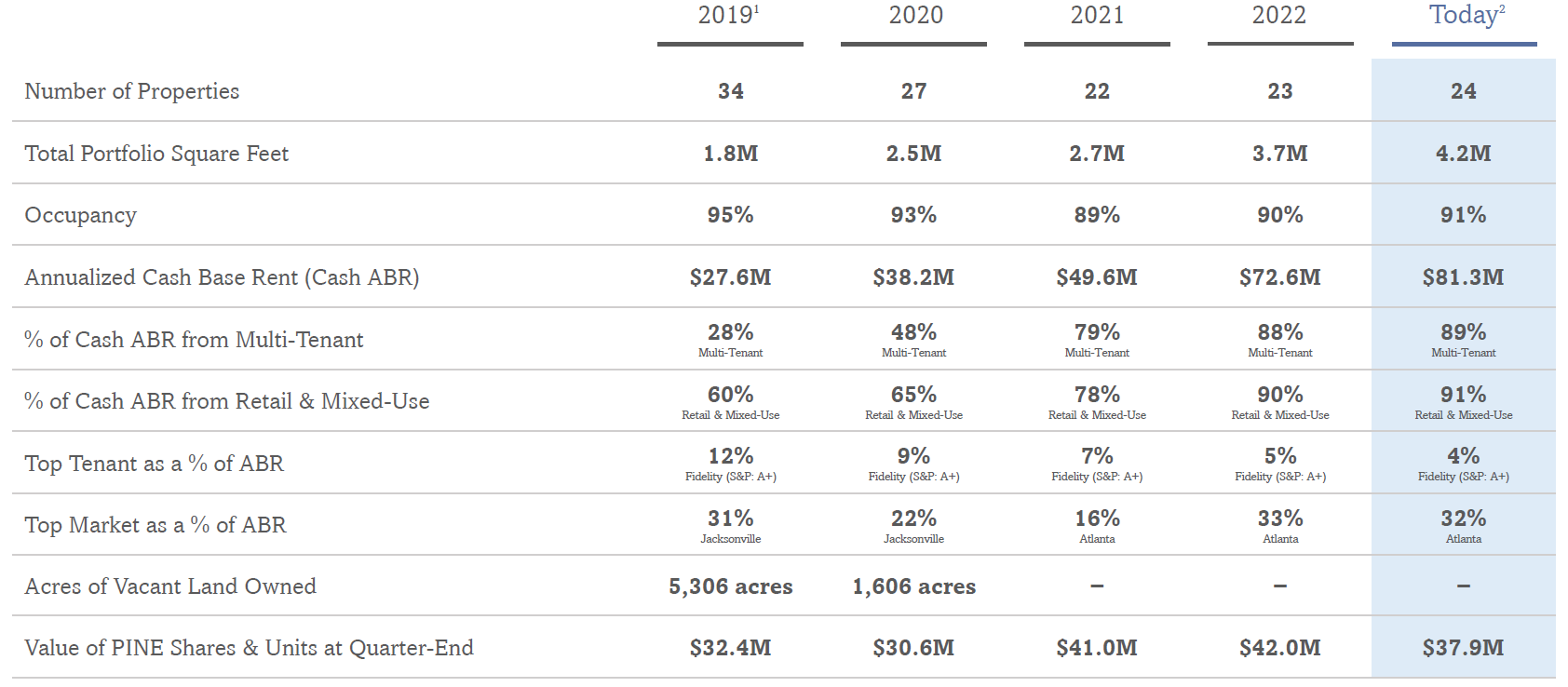

The income producing portfolio is comprised of 23 properties (n.b., 16 retail, 5 mixed-use, and 2 office). Retail contributes ~55% of cash base rent, mixed-use ~36%, and office ~9%. The highly attractive markets of Georgia, Texas, Florida, Arizona, and Nevada represent ~74% of cash base rent. Atlanta is CTO's top market, with ~32% of cash base rent. The total portfolio is ~91% occupied with a WALT of 5.3 years. It still owns ~15% of PINE (n.b., implied market value of ~$40MM, or ~11% of CTO's current market cap).

Geographic Breakdown (Company filings) Portfolio Summary (Company filings)

{kind=link}

{kind=link}

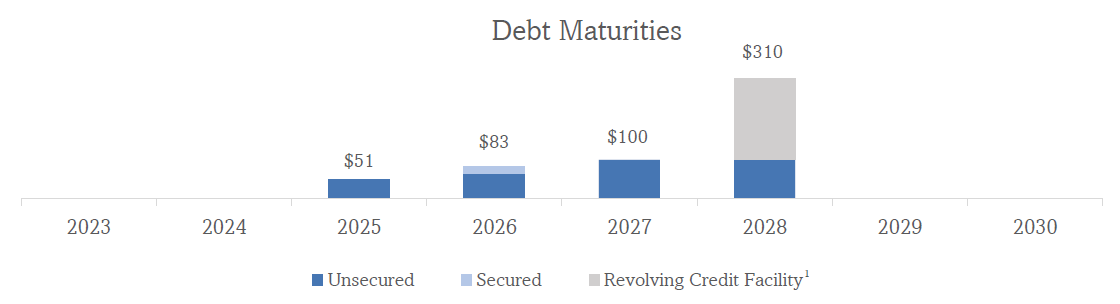

CTO's balance sheet and liquidity position are clean and healthy, with no debt maturities until 2025 and only ~20% of its debt subject to variable rates.

Debt Maturities (Company filings)

{kind=link}

Valuation

CTO Net Asset Value ("NAV")

Given the relative complexity of the REIT's portfolio and the fact that it follows U.S. GAAP, CTO's balance sheet requires a bit more scrutiny than other REITs (e.g., Northview Residential REIT ).

Note that under U.S. GAAP, the reported book value of CTO's investment properties reflects its depreciated cost basis and not a mark-to-market value, as a REIT would report under IFRS. This makes metrics such as book value and tangible book value almost meaningless.

As a result, I began by adjusting the value of the investment properties to reflect a stabilized NOI and average cap rate for the portfolio.

I also updated the carrying value of CTO's stake in PINE based on the latest market price and the estimated market value of the management contract (n.b., 3x fee revenue, in-line with management and comparable internalization transactions).

The carrying values for the subsurface interests and mitigation credits were updated to reflect the present value of these assets, assuming they are sold at a pace and value in-line with historical averages assuming a 12% discount rate. This results in a ~$0.7MM (n.b., 25%) increase from the carrying value of these line items, driven by the fact that the subsurface interests are generally well-above their carrying value.

I also considered cases including and excluding the intangible assets and liabilities, which largely consist of above or below-market leases, as these values should be implicitly included in the value of the investment properties.

My central case assumes a stabilized NOI of ~$72MM, in-line with management, a 7.25% cap rate, the high-end of management guidance and slightly above recent dispositions, and $5MM of common share repurchases. Based on the foregoing, I estimate CTO's NAV at just under ~$22 per share (n.b., +36% higher than current share price, and 12.7x FFO / ~11x adjusted AFFO, 7% implied yield). Due to its smaller size, and diversified holdings (i.e., subsurface, mitigation, mortgages, loans, etc.), I do not expect CTO to trade exactly in-line with NAV. I would consider trimming my position around $20 per share, but would likely retain a smaller holding given my low cost basis and high yield.

My bear case assumes stabilized NOI of ~$65MM (n.b., ~10% lower than the central/management case), a 7.5% cap rate, and no share repurchases. This case results in a $16.3 NAV per share, ~2% higher than the current price.

Risks

1) Bad Debt & Tenant Bankruptcy

In the first two quarters of 2023 , CTO has faced FFO/AFFO headwinds (n.b., FFO and AFFO per share are down ~13% and ~8% YoY YTD, respectively) primarily due to bad debt expense related to The Hall at Ashford Lane, reduced rent associated with the bankruptcy of Regal at Beaver Creek Crossings and negative effects from 2022 CAM reconciliations at The Strand in Jacksonville and Crossroads Towne Center. Based on the Q2 '23 earnings call, it appears that the worst is behind us, and management has indicated it is conversations with multiple potential tenants to backfill these spaces by early '24.

2) Variable Rent

YTD, ~21% of CTO's rental revenue is considered variable. The variable component of rental revenue consists of percentage rent and tenant recoveries (CAM, insurance, tax, etc.). Charging tenant recoveries is an industry standard and not a common source of significant risk. However, the percentage rent, presumably tied to certain tenants' sales volumes (e.g., QSRs), is subject to material economic risk. CTO does not disclose the breakdown of the sub-categories of its variable rent, so I cannot quantify this risk. However, in the Q2 '23 earnings call, management noted that it had benefited from elevated percentage rents from restaurant tenants in Daytona Beach (n.b., +$250k). This is a key line item to watch in the next few quarters as we enter a likely recession or economic/consumer slowdown.

3) Lack of Coverage

Due to CTO's non-traditional history and small size, it is poorly covered with no major banks or equity research houses covering it. This may increase the amount of time required for the market to price CTO appropriately, or prevent it from trading exactly in-line with comps or NAV.

4) Inability to Sell Subsurface Rights & Mitigation Credits

At the rate CTO has sold subsurface interests and mitigation credits over the past 6 quarters, it will take CTO approximately 1 year to divest its mitigation credits and 30 years to divest its subsurface interests. Retaining the subsurface interests, even in such small quantities, may deter investors. While I don't view this as rational, it is somewhat understandable.

Catalysts

1) Replacement of Nonperforming Tenants

As discussed in the risks section above, the resolution of the issues CTO is facing at The Hall at Ashford Lane, Beaver Creek Crossings, The Strand in Jacksonville, and Crossroads Towne Center will be supportive of SP NOI, and FFO and AFFO per share recovery into '24.

If these issues prove more widespread and difficult to address, I would reconsider my thesis and potentially reduce my position sizing.

2) Dividend Increase

CTO has paid dividends for 47 consecutive years and has increased the dividend in each of the last 12 years under its current management.

With CTO guiding to 1-4% SP NOI growth, a demonstrated ability to accretively recycle capital, 8-9% leasing spreads YTD, a ~79% AFFO payout ratio, and no debt maturities until 2025, CTO is well-positioned to continue delivering dividend increases. Given the near-term FFO headwinds and management's stated desire to prioritize debt repayment through the balance of the year, I see any potential dividend increases likely coming in '24 when the aforementioned tenant issues are resolved.

3) Repurchase of Pref and/or Common

Management has demonstrated willingness and ability to repurchase common and preferred shares. In Q2 2023 , they repurchased preferred shares for the first time, buying 746 shares at $18.82, 25% below par. While this represented only a small fraction of the 3MM outstanding preferred shares prior to the repurchase, it is reflective of a keen focus on capital allocation. Based on CTO's current marginal cost of borrowing (n.b., SOFR + 10 bps + [1.2% - 2.2%]) I estimate that repurchasing all the outstanding preferred shares with debt would generate ~$0.03 per share of incremental run rate savings, which could support a ~2.3% dividend increase.

When it comes to repurchasing common shares, management has been much more active over the years. In the first three quarters of 2022, management issued ~203k shares at an average price of ~$22 per share, while repurchasing ~92k shares at an average price of ~$19 per share (n.b., all figures are split-adjusted). This demonstrates management's flexibility to take advantage of market conditions to improve liquidity when prices are high and accretively repurchase shares when prices are low. In Q4 2022, management made a massive ~3.5MM share issuance through its ATM program at an average price of $19 per share (n.b., 8.0% forward yield). On the surface, this seems like a bad move. However, it may have been necessary and prescient. This issuance allowed CTO to raise +$60MM, giving it the capacity to deploy ~$20MM at an 8.5% going-in yield and repurchase ~303k shares at an average price of ~$16.5 per share the following quarter. YTD, CTO has repurchased ~307k shares at an average price of ~$16.5 per share.

My model indicates that every $1MM CTO uses to repurchase common shares at today's prices would be +$0.01 per share accretive to its NAV. My central case assumes $5MM of share repurchases (n.b., ~$26MM of cash on the balance sheet as of Q2 2023, pro forma for disposal on Oct. 2, excluding restricted cash).

4) PINE Re-Rating

CTO's ~15% stake in PINE is likely to benefit disproportionately from future rate cuts. Being a pure-play triple-net REIT, PINE's portfolio is extremely bond-like and thus exhibits high convexity to interest rates. If the fed cuts rates, PINE should re-rate significantly.

5) Disposal of Subsurface Rights and Mitigation Credits

CTO still owns ~28 mitigation credits, and 352,000 acres of subsurface interests, though it continues to sell these assets down consistently. Divesting these obscure assets may simplify the story for investors and should help reposition CTO as a pure-play retail and mixed-use REIT.

Quick Note on the Preferred

In addition to CTO's common, I had a quick look at the preferred. Obviously, I believe the prefs are well-covered with the common equity cushion. Currently, the prefs trade at ~$18.8 (n.b., 25% below par, ~8.6% implied yield).

I view the prefs are more of a macro play, as the only way they will trade at par (aside from CTO being acquired) is for rates to fall materially. In that case, one could expect a ~40% total return. I would view this as a more attractive way to play CTO, as the yields are similar, and the prefs rank senior to the common. However, I do not want to make a pure macro call on rates and the prefs are far less liquid than the common. Therefore, I would prefer to stick to the common. Though I give the prefs a Buy rating given the low business risk and depressed pricing.

Conclusion

At its current valuation, CTO offers investors the opportunity to acquire a steadily growing, well-managed REIT at an attractive going-in yield with a wide margin of safety and capital appreciation potential. The 9.5% current yield and presence of several near and medium-term catalysts warrant my current Buy rating.

For further details see:

CTO Realty Growth: Reliable Yield Play With Upside Potential