PSA - CubeSmart: Performing Well But Too Expensive

2023-05-08 10:03:46 ET

Summary

- CubeSmart is the 3rd biggest self storage company in the US.

- It has delivered good results in the last quarter but is overvalued in terms of the implied cap rate and P/FFO.

- My analysis of the company leads me to a hold rating.

Background

Self storage REITs have been getting a lot more popular thanks to average home sizes getting smaller. Both because of rising real estate prices, which make people move to smaller apartments/houses, and urbanization, that forces people to move to cities where they simply cannot buy a house if they want to live in a reasonable distance from the center. I believe this has definitely made self storage companies grow and reach a peak in the last few years. These same trends should drive the performance of the sector going forward.

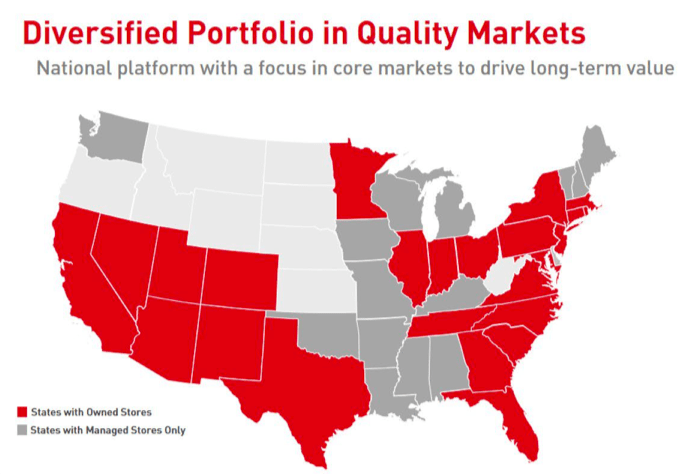

With 1279 properties CubeSmart ( CUBE ) is the 3rd biggest self storage REIT in the US. It is located in 39 different states with 89% of owed store NOI located in the top 40 top metropolitan statistical areas in the US. The biggest part of their portfolio, accounting for 22.3%, is located in the New York area where people tend to look for storage spaces more often as there are many people living in apartments rather than houses. At the same time though, as people started moving south during Covid, legacy markets including New York actually saw an outflow of people. Since it's usually new comers that tend to rent and look for self-storage this trend could result in a drop in demand.

CubeSmart Investor Presentation

{kind=link}

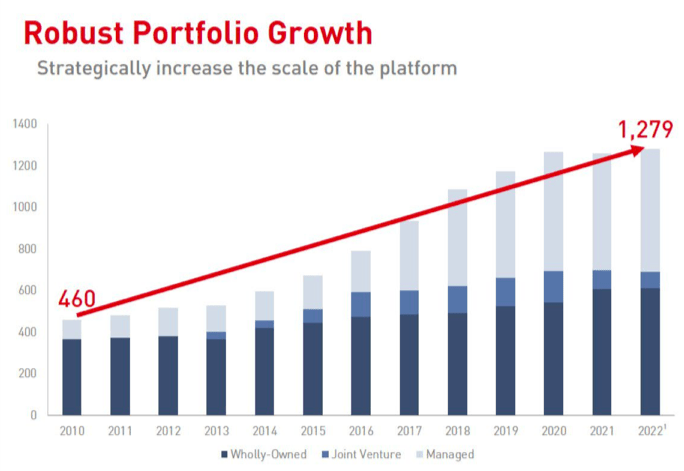

Their portfolio has grown a lot since 2010 mostly by acquiring properties that are now managed by a third party. They currently have 536 wholly-owned properties, 75 joined ventures from which the company acquired $900 million, and 668 third party managed properties with a $34 million management income fee. When we consider that about half of the portfolio is managed by a third party and that the REIT spends $43 Million in operating expenses to effectively manage the other half, it seems that they're actually getting a good deal and creating value by having the property management outsourced.

CubeSmart Investor Presentation

{kind=link}

Before diving into financials it's worth mentioning that the self storage space is quite competitive with a handful of major players that all offer the same product. This means that it's hard for any one of them to significantly increase prices and if demand slows in the future there's a potential risk of a price war as these major players try to compete for a limited number of tenants.

Financials

For Q1 of 2023, the company had an FFO of $147.5 million and an FFO per share of $0.65. During the first quarter, the firm performed really well. The revenues increased by 6.9% and NOI by 9.1%. While the operating expenses increased by only 1%. The occupancy went down by 1.5% but is still at a strong level of 91.9% so it seems that demand remains strong. Going forward management expects NOI to increase by 4-6% this year and has confirmed its guidance for 2023 FFO per share of $2.64-2.71. Which represents about a 3% growth at the midpoint.

Now I would like to look at the balance sheet of CUBE. The outstanding debt accounts for $3.06 billion, with 98% of the debt fixed and a 3.05% weighted average interest rate. The weighted average maturity is 6 years and very little debt matures before 2025. While they have basically no cash ($5 million) they have a credit facility which was recently amended for $850 million. So CubeSmart should not have a problem with maturities, at least not before 2025, when they will probably make use of their credit facilities and with essentially no interest rate exposure their interest expense should be very stable.

CubeSmart Investor Presentation

{kind=link}

CubeSmart's dividend has increased by 14% in the last year and currently stands at $1.96 per share with a 4.3% dividend yield. Considering the current payout ratio of 77% and a stable occupancy it should be pretty safe in the future, though I don't expect it to maintain the same level of growth.

Valuation

In terms of valuation, the company trades at an implied cap rate of 5.4%. The best way of evaluating whether that's a good deal is to look at the spread to long term treasury yields. Historically the spread has averaged around 300 bps and with 10-year treasury yields currently at 3.3%, the implied spread stands at just 210 bps. That feels too narrow a spread to justify the risk, likely meaning that the REIT is overvalued. Assuming the historical average is valid, there's an additional 16% downside.

The P/FFO for CUBE is 17.78x with a historical average of 18.31x. Peers trade at very similar multiples. Public Storage ( PSA ) at 18.26x, Extra Space Storage ( EXR ) at 18.36x. CubeSmart is therefore fairly valued compared to peers, but seeing as the current P/FFO is basically in line with the historical average and given the economic uncertainties we have today, I would argue that CUBE is quite pricy here at the price of $46 per share and I rate it as a HOLD for now.

{kind=link}

For further details see:

CubeSmart: Performing Well But Too Expensive