CFR - Cullen/Frost Bankers: Texas Bank With Enviable Balance Sheet Strength And Sustainable Dividend Growth

2023-06-12 08:30:00 ET

Summary

- Cullen/Frost Bankers, the parent company of Frost Bank, is a conservatively managed regional bank focused solely on the Texas economy.

- Despite facing headwinds like rising deposit costs and exposure to commercial real estate, CFR's high customer satisfaction, strong financial management, and the robust Texas economy make it an attractive investment.

- With a 3.2% dividend yield, 29-year record of consecutive dividend growth, and a P/E ratio of 11.5x, CFR stock offers potential for both dividend growth and total return investors.

Cullen/Frost Bankers ( CFR ) , parent company of Frost Bank, is the largest and arguably the most conservatively managed regional bank based in Texas. Currently, the bank is focused solely on the state of Texas, which makes it a pure-play investment in the Texas economy.

Of course, there's nothing stopping the bank from expanding into other states if management deems it a good investment, but for now CFR is continuing to expand its presence and market share across multiple markets in Texas, including Houston, Dallas/Fort Worth, and Austin.

The issues weighing on regional banks generally -- rising cost of deposits, deposit flight from banks to money markets and bonds, and exposure to commercial real estate -- are also headwinds for CFR. But these issues appear to be less of a problem for CFR than for most other regional banks because of its high customer satisfaction, the underlying strength of the Texas economy, and strong financial management.

With a ~3.2% dividend yield and 29-year record of consecutive dividend growth, CFR looks attractive for both dividend growth and total return investors at its current price. Plus, at a P/E ratio of about 11.5x, CFR is significantly cheaper than its 5-year average of ~15x, giving it 30% upside to that recent historical average valuation.

Overview of Frost Bank

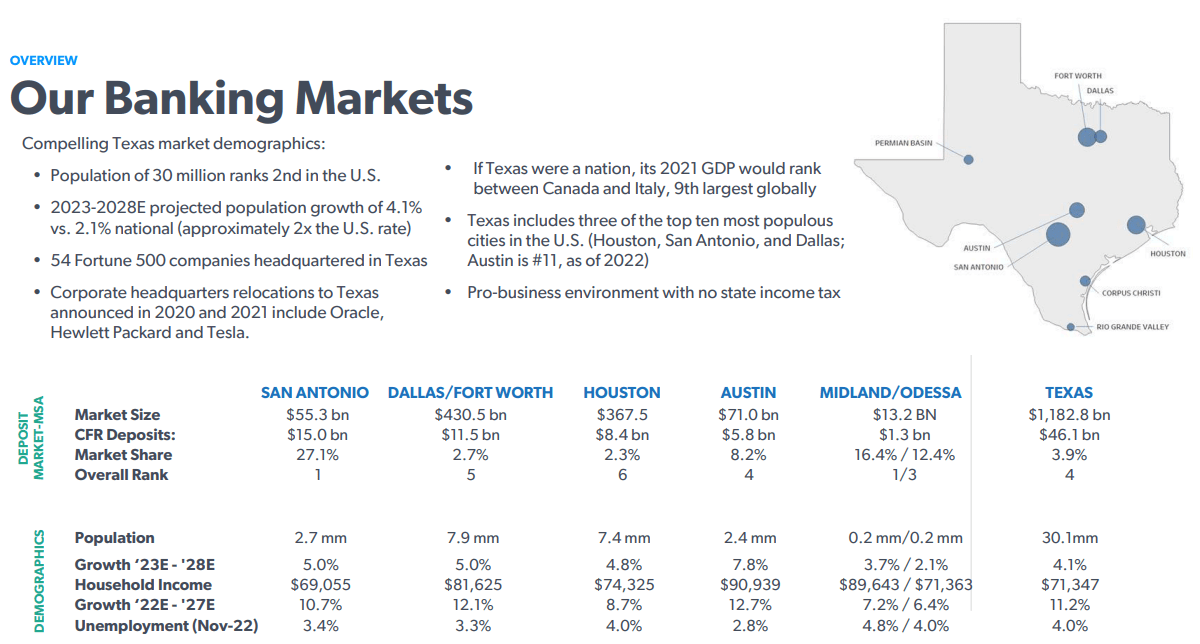

CFR operates exclusively in the large and fast-growing state of Texas. The bulk of its deposit base and loan portfolio are concentrated in San Antonio (where the company is headquartered), Dallas/Fort Worth, Houston, and Austin.

{kind=link}

As far as demographics go, you couldn't ask for a much better profile than the one CFR enjoys in Texas. That's the first notable strength of the bank.

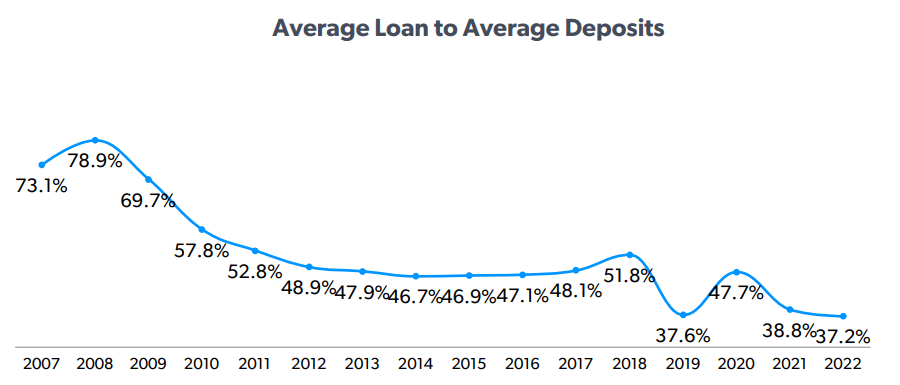

The second notable strength is CFR's extremely conservative loan-to-deposit ratio.

{kind=link}

As of Q1 2023, the LDR ticked up a bit to 0.41x, or 41%, as total deposits slightly decreased while total loans slightly increased.

CFR is at no risk of its LDR becoming worrisomely high anytime soon. Although the bank did not itself get into too much trouble during the Great Recession of 2008-2009, management certainly seem to have learned from some of the mistakes of the banks that did, one of those being too high of LDRs.

One of the market's primary concerns about regional banks generally and CFR specifically is the exposure to office property loans.

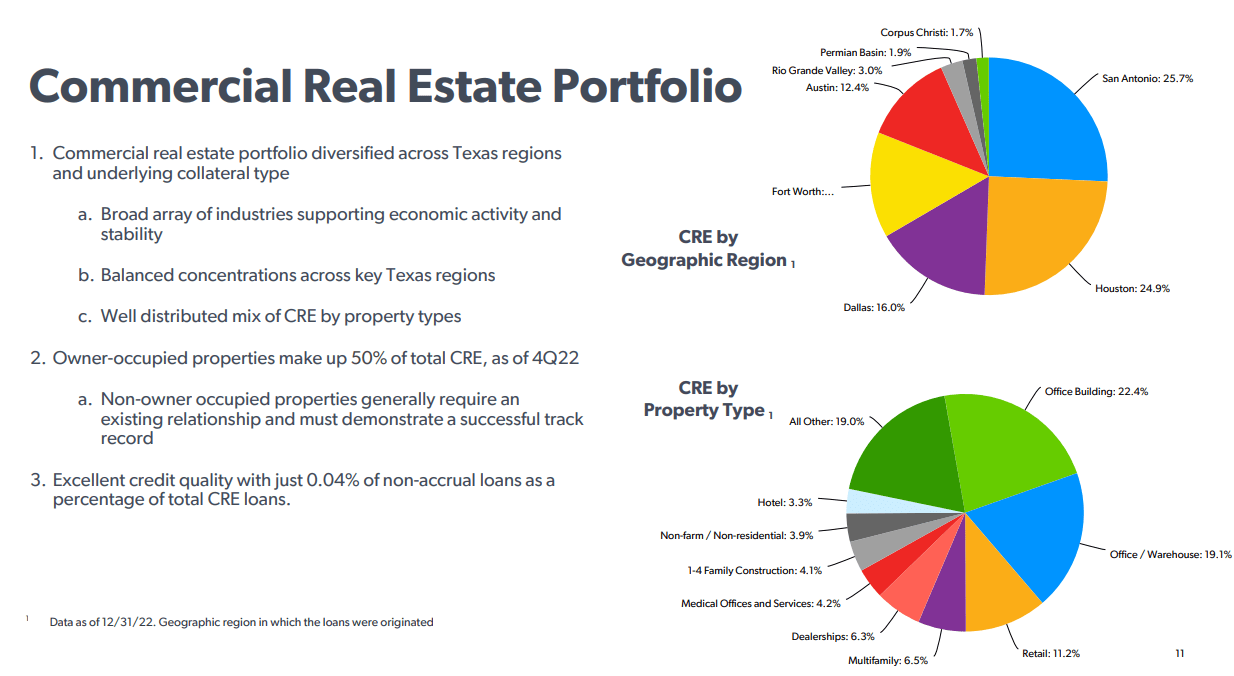

At the end of Q1, CFR had $10.9 billion in commercial real estate loan commitments, with $8.3 billion of that already funded. That amounts to about 48% of CFR's total loan portfolio.

{kind=link}

As of the end of March 2023, 100% of commercial real estate loans were current (no delinquencies or past due payments). And the overall average loan-to-value for its CRE portfolio stood at 55%, which strikes me as fairly conservative.

To be fair, it is unclear to me how recent that 55% LTV assessment is. Year-to-date, most CRE segments have seen property price declines, which should cause LTVs to rise. The point here, though, is that a 55% LTV is conservative enough to allow for some drop in price without wiping out the borrower's equity.

As for the office building loans specifically, they make up 26.5% of the CRE portfolio and 12.8% of total loans. A significant portion of these loans mature in the coming years. For example, 36% of office loans mature in less than a year, but most of that is owner-occupied office buildings.

About half of all CFR office loans are for investor-owned properties, which are generally considered to be riskier than owner-occupied properties.

According to CEO Phillip Green from the Q1 2023 conference call , 27% of investor-owned office loans mature within 12 months, 19% in 12-36 months (1-3 years), 21% in 36-59 months (3-5 years), and 33% in 60 months or more (5+ years).

Here are the rest of Green's comments on the office loan portfolio from the conference call:

Specifically, in the office building portfolio, which is top of mind in the current environment and including medical office, we have about $2.4 billion committed and $2.2 billion outstanding, with about half of that being owner-occupied buildings.

We consider owner-occupied properties to have a lower risk profile due to reliance on our C&I borrowers operating cash flow rather than income generated from underlying real estate. And borrowers in our C&I portfolio have held up very well as we operate in some of the strongest markets in the United States.

The investor office portfolio exhibited an average loan-to-value of 55% and an average debt service coverage ratio of 1.35 at current interest rates. Again, starting from a strong position with cushion for potential valuation declines.

Our comfort level with our office portfolio continues to be based on the character and experience of our borrowers and sponsors, the predominantly Class A nature of our office building projects and the fact that 83% of the exposure is associated with stabilized projects that are 87% leased. It also helps to be operating in Texas.

So, in short, there are several mitigating factors that should ease investors' concern about CFR's office exposure:

- Some of it is medical office.

- Half of it is owner-occupied and therefore significantly less likely to experience distress.

- The loan-to-value is fairly low, discouraging borrowers to walk away.

- Most office buildings (the collateral) are Class A properties.

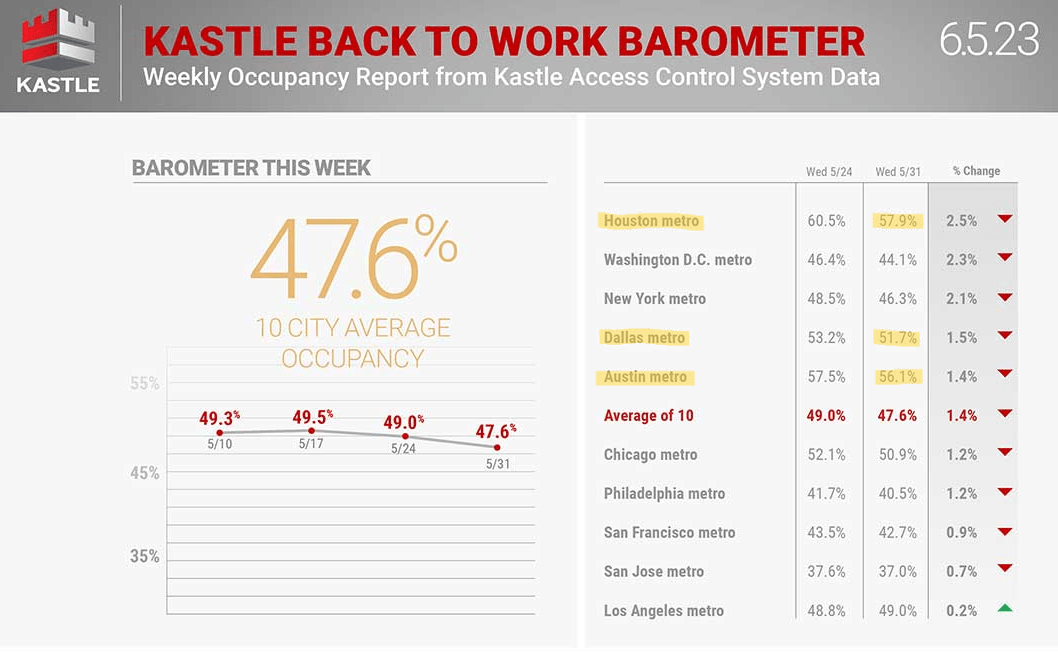

- Texas office markets tend to enjoy higher-than-average worker utilization.

Whether for cultural reasons or issues related to commute times or something else, Sunbelt office markets tend to exhibit higher worker utilization of offices. In Kastle Systems' most recent reading of weekly office occupancy from late May, Houston, Dallas, and Austin continue to show the highest worker occupancy among the top ten.

{kind=link}

Granted, occupancy declined across the board in the second half of May, but that could be a result of increased summer travel or broad-based economic weakening and layoffs. In either case, the Texas office buildings continue to be the most utilized among large metros. This should minimize distress among Texas office landlords and thus also CFR.

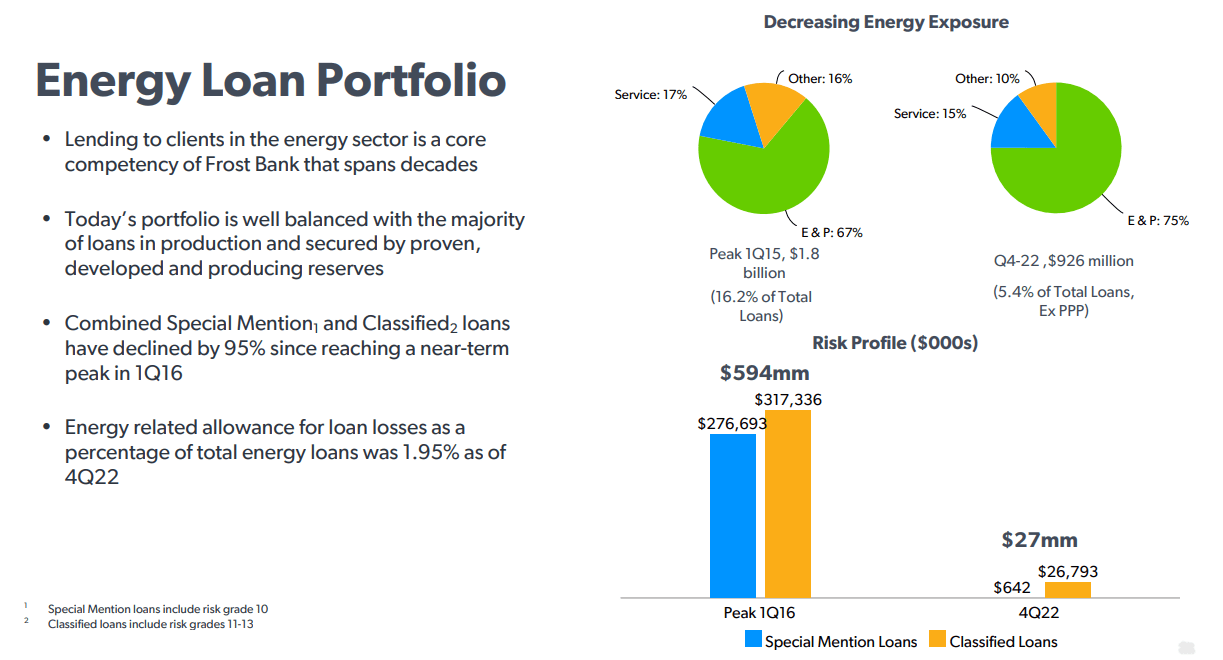

And, of course, CFR would hardly be a Texas bank if it didn't have some exposure to the energy sector. The bank does have some exposure, but it is small (less than 5% of total loans). Since the beginning of 2015, CFR has halved its exposure to energy companies.

{kind=link}

It's notable that, even with the highly publicized distress in the office sector as well as the strong profitability of the energy sector, allowances for loan losses remains higher for energy loans than for CRE.

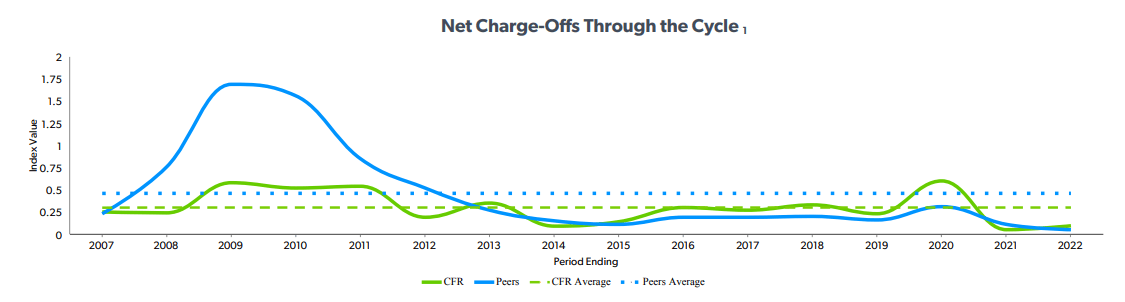

But across the board, CFR's loan book continues to perform with extremely little non-performance. Net charge-offs are at extremely low levels, and they remained significantly more muted than the peer average during the Great Recession.

{kind=link}

NCOs did spike a bit higher than the peer average during 2020 as a result of CFR's energy exposure, but that particularly bad scenario for oil & gas companies appears highly unlikely to play out again anytime soon.

Perhaps the strongest aspect of CFR is its conservative financial management. The balance sheet enjoys A-/A3 credit ratings as a result of this conservatism. Since the bank employs very little debt on its own balance sheet, it's important to note that the company has very high customer/depositor loyalty. That's pertinent to balance sheet strength when a huge percentage of your liabilities are in the form of deposits!

But CFR also enjoys among the largest cash cushions in the entire banking sector, which provides both cushion during periods of deposit outflows as well as dry powder when investment opportunities become extraordinarily attractive. Cash & equivalents as a percentage of total assets stood at 18.2% in Q1 2023, down from 22.7% in Q4 2022.

CFR has a general policy of maintaining around 20% of total assets in cash/equivalents but will allow that to dip lower when attractive investment opportunities are abundant. Recently, management has been deploying some of that cash into relatively high-yielding securities, which strikes me as a great way to lock in safe, 5%+ yields for multi-year periods.

As a result of where interest rates stand, CFR's net interest margin reached 3.56% in Q1 2023, up from 2.87% in FY 2022.

Also, the bank is extraordinarily efficient, with an efficiency ratio of 53.7%, down from 56.9% in FY 2022. (When it comes to the efficiency ratio, lower is better, as it indicates less expenses per dollar of income.)

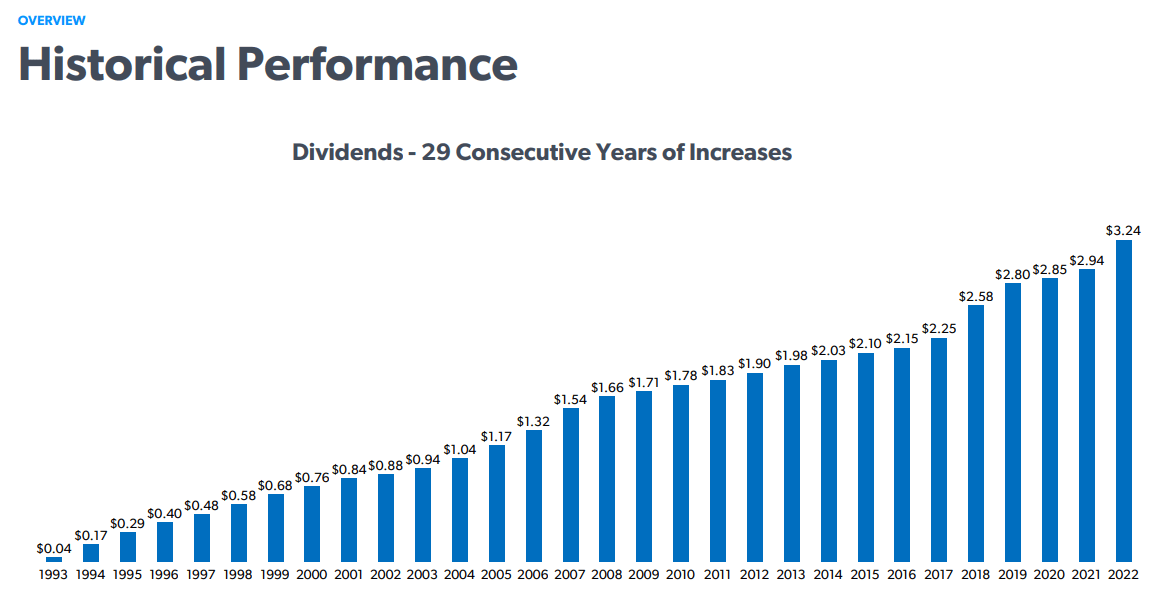

All of the above flows through to strong and sustainable earnings growth over time, and in turn CFR has been able to continuously raise its dividend over the past several decades -- 29 consecutive years, to be exact.

{kind=link}

After four quarters in a row at the same dividend, CFR is due for another raise in the next declared dividend. The next dividend increase could be lower than its typical 6-8% hike because of the headwinds facing the banking sector right now, but I do not believe this would be an indication of a slowing long-term dividend growth rate.

In fact, given CFR's ample liquidity, ability to pounce on great long-term yields, and strong market position in the fast-growing state of Texas, the bank's growth rate may actually be faster in the next five years than it was in the last 10 or so.

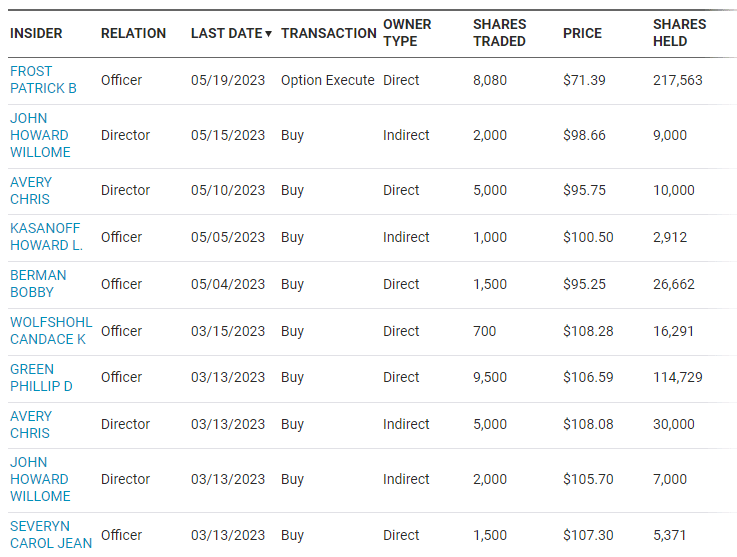

There is one last relevant point to mention in CFR's favor, and it is that insiders have been buying shares hand over fist in recent months.

{kind=link}

Notice, for example, that CEO Phillip Green recently purchased over $1 million of CFR at a price of $106.59.

Bottom Line

CFR is among the most conservatively managed US banks with a skilled, long-tenured, shareholder-aligned management team. The balance sheet and liquidity position are top-notch, providing ample optionality during tricky periods like the current one.

And, finally, the loan book, which accounts for only ~40% of deposits, is much stronger than the market seems to give it credit for. Its office loans are showing no signs of distress as of yet, and its energy exposure is minimal. The primary factor weighing on the stock price seems to be negative investor sentiment rather than degrading fundamentals.

Meanwhile, the bank enjoys a very strong and focused market position in the economically robust state of Texas.

With an attractive dividend yield of ~3.2%, recession-resistant loan book and balance sheet, and promising growth prospects for the years to come, CFR looks like a great bank stock to buy today.

For further details see:

Cullen/Frost Bankers: Texas Bank With Enviable Balance Sheet Strength And Sustainable Dividend Growth