CGEM - Cullinan Oncology: Playing 'Moneyball' In The Drug Development Sector

2023-06-28 09:08:05 ET

Summary

- Cullinan is an intriguing play in the biotech sector.

- The company hopes to have 6 assets in clinical studies by the end of 2023.

- Lead asset Zipalertinib recently entered a pivotal study in EXON-20 mutated NSCLC - potentially a $1bn per annum market.

- Recent data from a second candidate CLN-619 was encouraging, with a complete response in 1 patient - an approval in ovarian cancer is a possibility.

- Cullinan is well-funded and picks its targets based on what has worked well before as opposed to trying to reinvent the wheel. Shares are cheap and the risk/reward profile is marginally more positive than negative in my view.

Investment Thesis

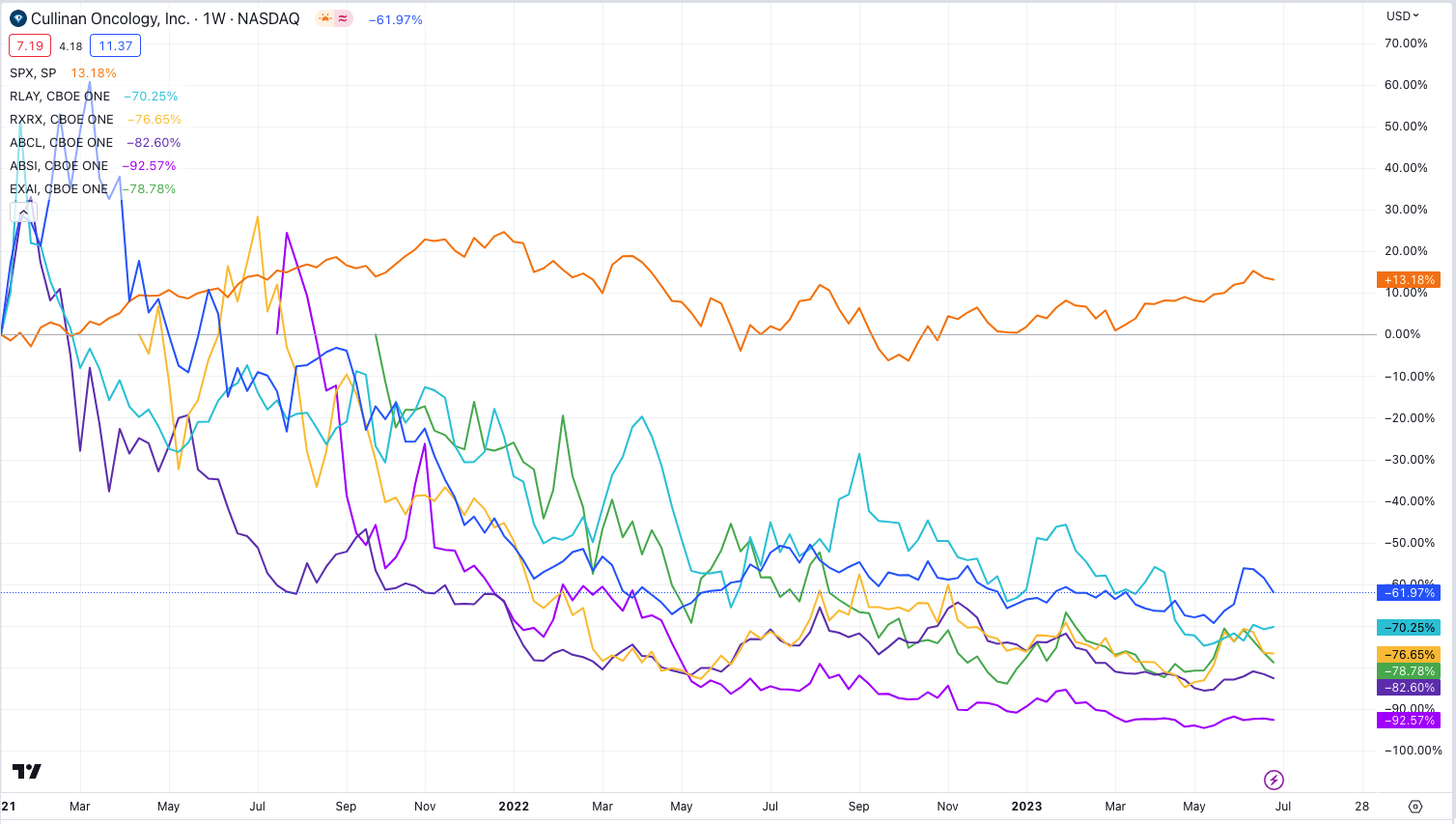

Over the past few years the biotech and pharmaceutical sectors of the stock market have witnessed the rise of AI driven drug discovery, with the likes of Relay Therapeutics ( RLAY ), Recursion Pharmaceuticals ( RXRX ), AbCellera ( ABCL ), Absci Corp. ( ABSI ) and Exscientia ( EXAI ) all completing lucrative IPOs and promising to revolutionise the space by evaluating billions, if not trillions of potentially druggable targets and compounds in double quick time using super-computers and bleeding edge 3D modelling.

So far however the reality has not yet matched the hype - no AI-discovered drugs have yet been approved (although that could change if Relay's bile duct candidate RLY-4008's pivotal study in bile duct cancer is successful) and share price performance has been poor - as shown in the table below.

{kind=link}

All five of the companies mentioned above have seen their share prices decline by >70%, and two of five by >80%.

What this may indicate is that AI-driven drug discovery is still in its infancy, and that companies that take a slightly more pragmatic approach, and work with well-established druggable targets as opposed to trying to find new ones, still have a significant role to play in the drug discovery process - and may offer investors a less cash intensive, more financially viable business model to buy into.

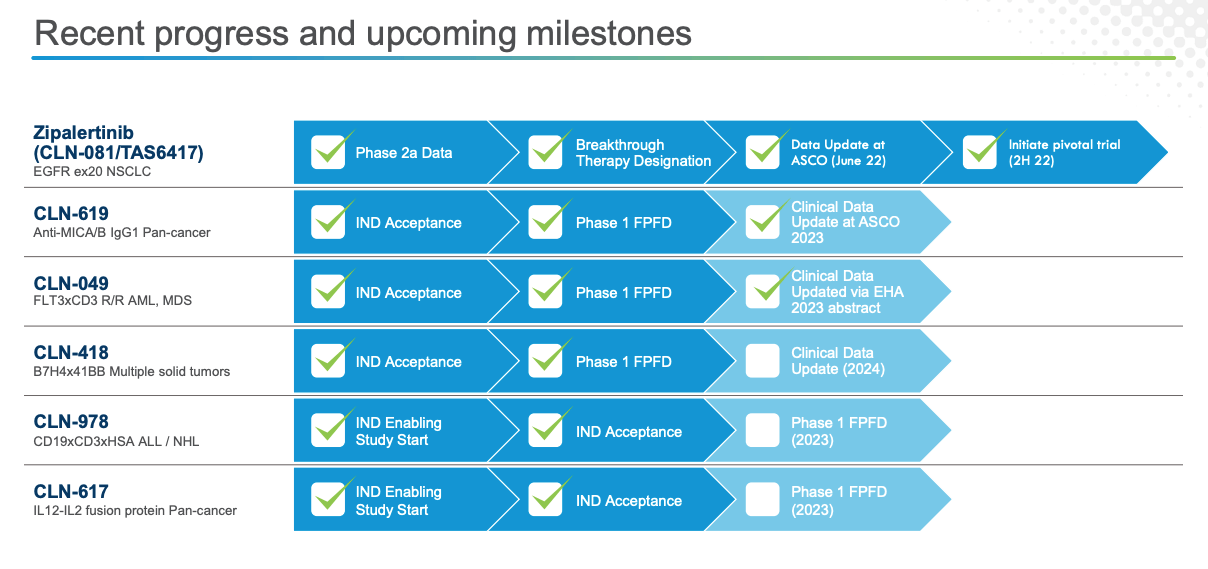

Cullinan Oncology ( CGEM ) - the subject of this post - is one such company in my view. I have included the company in the chart above, and although its 5-year performance is not much better than the AI-driven stocks - down >60% - it has been able to successfully develop a proprietary, clinical stage pipeline consisting of 6 assets, one of which has entered a pivotal study in non-small cell lung cancer ("NSCLC") in 4Q22.

Cullinan Oncology pipeline and progress (Cullinan presentation)

{kind=link}

A key point of difference in Cullinan's approach to drug development versus the AI companies is outlined in the company 2022 10K submission ( annual report ) as follows:

Our strategic focus is on what we call “modality-agnostic targeted oncology”: We first identify high-impact cancer targets and then select what we believe is the optimal therapeutic modality for those targets. As a result, we are not dependent upon a singular technological platform or product.

We define “high-impact” biological targets as those that play key roles as either oncogenic drivers or immune system activators. From there, we advance only molecules that we believe have first- and/or best-in-class potential and that can generate a robust anti-tumor response as a single agent in vivo.

Through this disciplined approach, we believe we will bring forward differentiated molecules with the potential to create new standards of care for patients with cancer. Key objectives we aim to achieve with our strategy are as follows:

In short, Cullinan selects targets that are known to work, and picks the mechanism of action ("MoA") likely to work best for that target. It makes sure the candidate has activity as a monotherapy, and it is prepared to license-in promising candidates rather than create new ones from scratch. Overall it may represent a cheaper, faster route to finding better-performing drugs.

Of course, that does not necessarily mean that Cullinan's pipeline is made up of 6 slam dunk approval shots with blockbuster (>$1bn per annum) revenue potential. Far from it. But another positive about Cullinan for investors looking for exposure to promising biotechs is that its market cap valuation is a fraction of most of the AI-driven drug developers mentioned above. Cullinan's market cap is $448m at the time of writing, compared to Relay Therapeutics - $1.44bn - Recursion - $1.42bn - AbCellera - $2.1bn, and Exscientia - $785m.

As such, where many drug developers are struggling to justify their price tag, Cullinan looks potentially undervalued. In fact, the company is trading at less than its cash position, reportedly $504m as of Q321. Cullinan says its funds will last until 2026, which is plenty of time to make significant progress with all 6 of its assets, and perhaps secure a first approval for lead asset Zipalertinib.

In the remainder of this post I'll take a deeper dive look at Zipalertinib, and a brief look at the company's other assets, before speculating about what price the company's shares may trade at in 3-5 years time, or when the current funding is exhausted.

Zipalertinib - Mechanism of Action, Current Progress, Market Opportunity

According to research quoted in Cullinan's 2022 10K submission:

Lung cancer is by far the leading cause of cancer deaths among both men and women, comprising almost 25% of all cancer deaths. The American Cancer Society estimated that in 2023, there will be approximately 238,340 new cases of lung cancer and approximately 127,070 deaths from lung cancer in the U.S. The most common subtype of lung cancer is NSCLC, which represents approximately 80% to 85% of all lung cancers.

According to it Q321 10Q submission:

Zipalertinib (CLN-081/TAS6417), which we are co-developing with an affiliate of Taiho Pharmaceutical Co., Ltd ("Taiho"), is an orally-available small-molecule, irreversible epidermal growth factor receptor ("EGFR") inhibitor that is designed to selectively target cells expressing EGFR exon 20 insertion mutations with relative sparing of cells expressing wild-type EGFR.

EGFR is "a receptor tyrosine kinase ("RTK"), that normally functions to trigger cell division when growth factors bind to the receptor, but it can be susceptible to oncogenic mutations that lead to the development of NSCLC. Cullinan believes that EGFR mutations:

Are present in approximately 15% to 25% of U.S. and Western European NSCLC patients and approximately 30% to 50% of Asian NSCLC patients...

Exon 20 insertions, which account for 7% to 13% of all EGFR mutations in NSCLC patients, are the most prevalent after the classical EGFR mutations. We estimate an incidence of approximately 2,000 to 5,000 NSCLC patients in the U.S. and approximately 1,000 to 3,000 patients in France, Germany, Italy, Spain, and the United Kingdom (the "UK") with EGFRex20ins mutations.

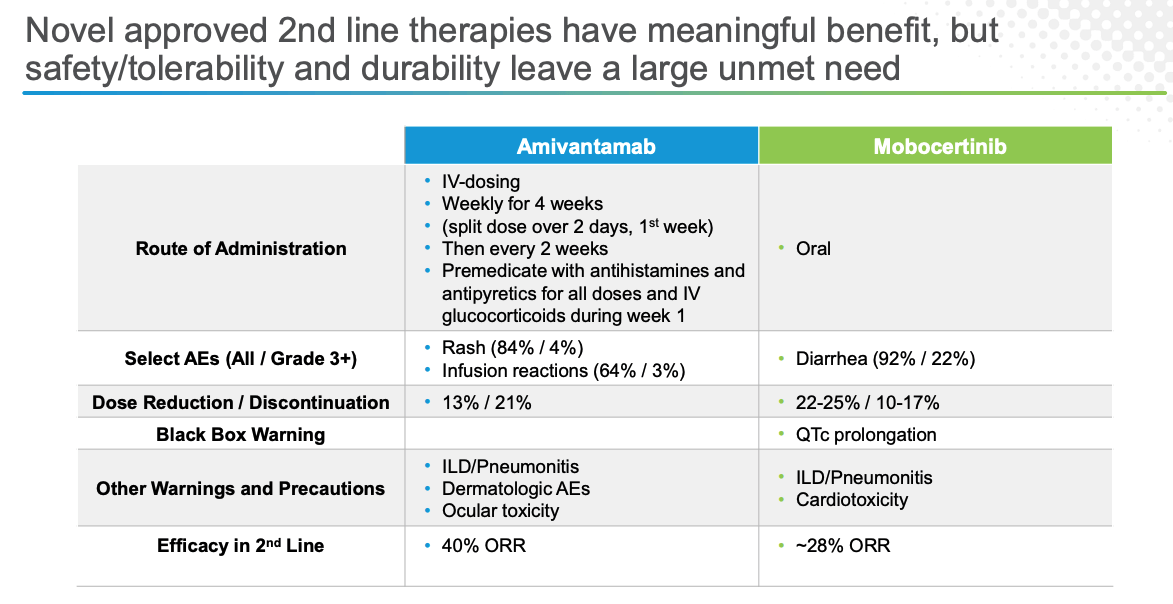

Ultimately, despite its indication for NSCLC, Zipalertinib does not have a large addressable market, and it also has 2 already approved rivals, drugs that also target EXON 20 mutation in NSCLC, in amivantamab, marketed and sold as Rybrevant by Johnson & Johnson ( JNJ ) and mobocertinib, marketed and sold by Takeda ( TAK ) as Exkivity.

Rybrevant was approved in May 2021, and Exkivity in September 2021 - Takeda has forecast peak sales of $300 - $600m for its drug, which likely represents a 50% market share - although Exkivity was rejected for approval in Europe in July last year, and based on study results, Rybrevant arguably has the superior safety and efficacy profile.

Given that 2 Pharma giants are already marketing drugs in this niche NSCLC indication, can investors really pin their hopes on Zipalertinib establishing a significant share of this market? The Cambridge, Massachusetts based biotech compares the 2 approved drugs as follows in a recent investor presentation:

amivantamab / mobocertinib comparison (Cullinan presentation)

{kind=link}

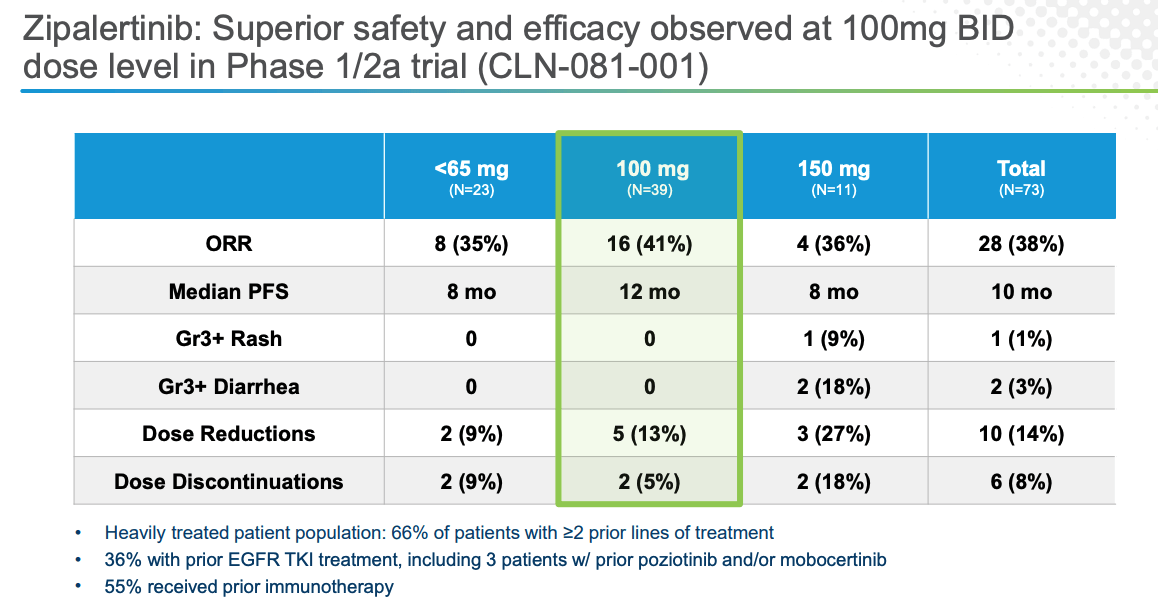

Cullinan believes that Zipalertinib has "best-in-class" potential, thanks to its HER-2 sparing and highly selective to mutant vs wild type EFGR "distinct chemical scaffold", and it has the - early stage - data to support this assertion from a Phase 1/2 study.

{kind=link}

A mantra of biotech investing is not to compare clinical studies because no two studies are ever exactly alike, but given the absence of other ways of comparing drugs before they are approved, the market frequently does anyway.

As we can see above, Zipalertinib's 41% ORR compares favourably with its rivals, although it is barely more than Rybrevant, whilst the 12m progression free survival is less that the duration of response ("DoR") recorded by Exkivity of 17.5m and more than the 11.1m DoR recorded by Rybrevant in studies. These measures are not directly comparable (a primer explaining the different clinical trial endpoints can be found here ), although apparently Exkivity patients extended their lives by a median 24 months, and Rybrevant patients by 22.8m.

Zipalertinib's safety profile appears to be reasonably strong, with no grade 3 of above rash or diarrhea cases reported below the 150mg dose level, although 4 patients experienced treatment related pneumonitis.

{kind=link}

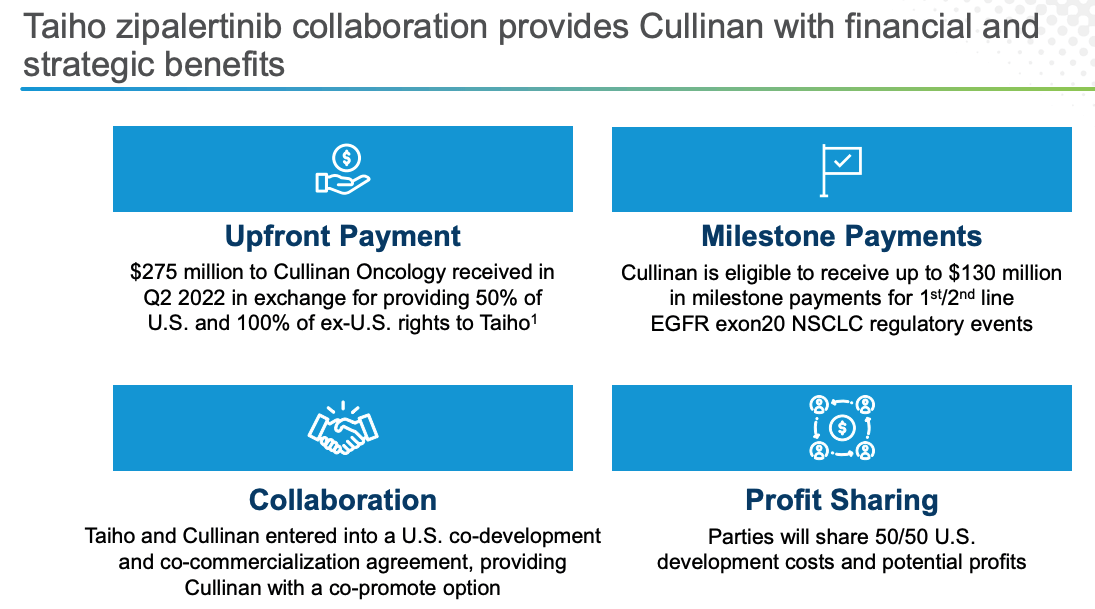

Shown above are the terms of agreement - shared in a recent investor presentation - with Taiho Pharmaceuticals. In exchange for a $275m upfront payment, Cullinan agreed to split development costs and any profits from the drug, if approved, 50/50, whilst Cullinan is also in line for up to $130m in additional milestone payments, often referred to as "biobucks". In effect, if Zipalertinib were to be approved and grab a 50% market share, Cullinan's revenues per annum would be ~$150 - $300m, based on Takeda's forecast for Exkivity, which are regarded as optimistic.

Nevertheless, provided Cullinan costs of sales were not too high - which should not be the case given the co-marketing arrangement with Taiho - revenues of >$100m per annum ought to push the market cap valuation above $500m, based on a rule of thumb that commercial stage pharmaceutical companies typically trade ~5x sales.

At present, Cullinan hasn't provided any timeline regarding the pivotal study data and when it may be shared, which is a slight worry for investors, as biotech valuations typically drift downward when there are no data or regulatory / approval catalysts in play - although thankfully, the progress of other assets has seen Cullinan's share price begin to trend upwards - by 20% in the past months.

Cullinan Pipeline ex-Zipalertinib - CLN-619 ASCO Data Impresses

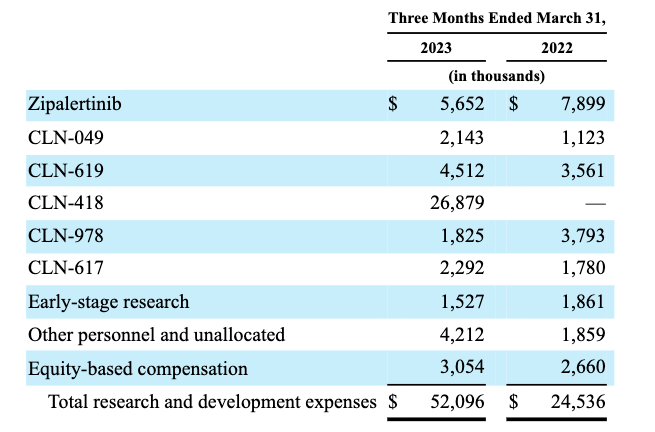

Often, a <$500m market cap biotech will be reliant on just a single asset - although that is not the case with Cullinan, it is equally worth bearing in mind that a large pipeline can be misleading if management is not committed to every asset. Looking at Cullinan's R&D expenditure in Q123, however, it seems the company is prepared to allocate significant funding to every one of its programs.

{kind=link}

Cullinan paid $25m in February to acquire the Phase 1 stage bispecific drug developed by Harbour BioMed - a deal which also includes ~$550m of biobucks / milestone payments based on progress with the asset. In a press release, Nadim Ahmed, Chief Executive Officer of Cullinan Oncology commented:

CLN-418 is a strong strategic fit for Cullinan, building on our expertise with bispecifics, and placing us at the forefront of bispecific antibody development in solid tumors

The press release discussed the bi-specific as follows:

B7H4 is an attractive tumor associated antigen (TAA) highly expressed on multiple tumor types, including triple negative breast cancer, ovarian cancer, and lung cancer, while expression on normal tissue is low. A coinhibitory immune checkpoint with PD-L1 in the B7 family, B7H4 has minimal overlap with PD-L1 expression. Targeting B7H4 has the potential to address tumor types for which PD-L1-based immunotherapies have exhibited limited efficacy.

4-1BB is a key costimulatory molecule for both T- and NK-cell engagement and is being studied in multiple clinical programs. However, safety concerns such as hepatic toxicity remain despite the biological validation of the 4-1BB pathway. Conditional activation of 4-1BB in the tumor microenvironment that is dependent on B7H4 expression presents a novel approach to harness the potential of both targets. CLN-418/HBM7008, with strict TAA crosslinking dependent T-cell activation, can potentially translate to better safety and a more favorable therapeutic window.

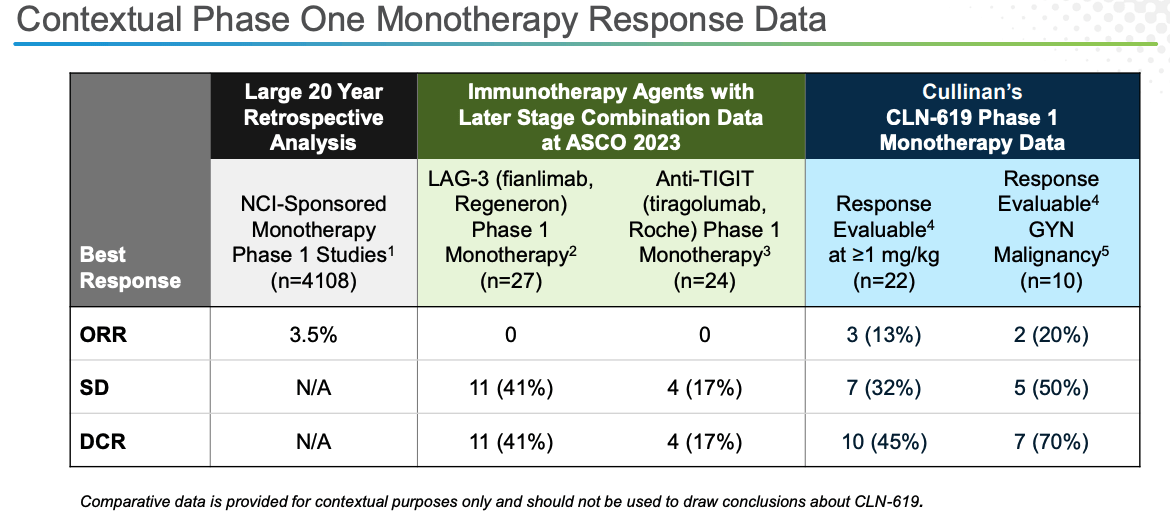

Meanwhile, data shared by Cullinan at ASCO 2023 from a Phase 1 study of CLN-619 - a novel, anti-MICA/B antibody, revealed 1 complete response ("CR") from a patient with parotid gland cancer, out of a patient population of 37, and 2 partial responses. Stable disease was observed in 7 other patients - all patients had been heavily pre-treated. Cullinan compares the data favourably with Regeneron's LAG-3 targeting ( REGN ) fianlimab and Roche's ( OTCQX:RHHBY ) TIGIT targeting tiragolumab in its presentation as below.

CLN-619 monotherapy data vs anti-LAG3, anti-TIGIT drugs (presentation)

{kind=link}

Cullinan plans to target endometrial, cervical and ovarian cancers with CLN-619 -areas where unmet need is high, with respective patient populations of 66k, 14k, and 20k.

Newly acquired CLN-418 is designed for solid tumors, and has already entered Phase 1 studies, joining a second bispecific, CLN-049, in the clinic, although the latter drug is designed to treat hematological cancers, CLN-978 and CLN-617, targeting CD19 x CD3 T-cell antibodies and IL-12 -IL2 cytokines respectively, now have their Investigational New Drug applications approved by the FDA, meaning in-human studies can begin.

Its intriguing to look at Cullinan's competitors in each space - the biotech states (in its 2022 10K) for example that CLN-049, which targets a protein called FLT3, is up against a drug candidate developed by Pharma giant Amgen ( AMGN ), whilst Japanese Pharma Astellas has secured approval for XOSPATA (gilteritinib), and Swiss Pharma Novartis ( NVS ) has secured approval for RYDAPT (midostaurin) - both drugs also target FLT-3. Acute Myeloid Lymphoma ("AML") is treated in a variety of ways by as many as 6 different drugs, with likely many more prescribed off-label.

Meanwhile, Novartis, Bristol Myers Squibb ( BMY ) and Roche are all working on drugs similar to CLN-619, and as for CLN-978, rival drug developers include AstraZeneca ( AZN ), MorphoSys AG ( MOR ), Novartis, Gilead Sciences ( GILD ) Bristol-Myers Squibb, Allogene Therapeutics ( ALLO ), Century Therapeutics, Inc., Nkarta Inc., Autolus Therapeutics ( AUTL ), ADC Therapeutics, and Amgen.

CLN-617 and CLN-418 appear to have novel MoAs - on the one hand being in a competitive development market means you are looking in the right place, while on the other, having a novel MoA gives a biotech a significant first-mover advantage in the event Proof of Concept is established.

Concluding Thoughts - Cullinan Plays The Percentages With Moneyball Approach To Drug Development - A Company Worth Following For Those With An Appetite For Risk

The truth is that I have fallen for Drug Developers with apparently diverse pipelines and even an approved drug before, believing they looked undervalued based on the opportunities in play.

A good example of this is MacroGenics ( MGNX ), I company I wrote a bullish review of for Seeking Alpha readers a couple of years ago - shares are down >80% since that note.

Drug development is a very tricky business characterised by a failure rate somewhere between 75 - 100%, and there is an argument it should be left to the Big Pharma industry, who have billions of dollars of R&D funds to invest. Then again, there is an argument that says Pharma's buy in their best drug candidates by acquiring the small biotech firms that developed them.

When that happens, biotech companies are bought out at massive premiums to their traded price - there is probably no other sector that provides as many overnight, triple digit gains as the biotech sector - one good data set can add >$1bn to a company's valuation in a matter of hours.

Where AI-driven drug discovery is trying to reinvent the wheel and start almost from scratch, chasing targets formerly regarded as undruggable, which could take a decade while burning through billions of dollars of investors' money, Cullinan's approach is more pragmatic - almost a "moneyball" approach based on opportunistic in-licensing of pre-identified targets.

There are plenty of reasons why Cullinan's valuation could rise - a pivotal study stage drug with a safety and efficacy profile that suggests it can compete in a >$1bn market. Encouraging data from another candidate CLN-619 - data that is better than that provided by giants like Regeneron and Roche, despite their incomparably larger R&D budgets. Management's ability to find the targets it is looking for and bring them in-house. >$500m of cash, set to last until 2026.

Balanced against that, the Zipalertinib is competitive but far from a guarantee the drug will be approved, let alone take on Takeda and Roche in the NSCLC markets. The remainder of the pipeline is very early stage and it is long odds that any will succeed, as carefully chosen as they are. The pace of development in drug discovery is rapid - Cullinan may not be able to develop assets fast enough even if they deliver positive data.

When I tipped MacroGenics 2 years ago, the company had a market cap valuation of $1.75bn, which is >4x the current valuation of Cullinan, however, and when compared with the AI-driven developers, again Cullinan is several multiple cheaper, despite being further along in the clinic with a key asset.

As such, my conclusion would be that Cullinan does offer investors with an appetite for risk some a decent risk / reward opportunity. EXON-20 mutated NSCLA is still an unproven market - peak sales expectation may be significantly exaggerated - but Cullinan appears to a genuine "shot on goal" in that indication, with expansion opportunities in play.

The stock may be a little discounted due to a lack of momentous recent catalysts, and management is casting nets in many of the right places. As with many biotechs, the stock price could easily double, and it could easily fall by half. I slightly favour the former scenario based on my analysis of the pipeline and the strong cash position.

For further details see:

Cullinan Oncology: Playing 'Moneyball' In The Drug Development Sector