CGEM - Cullinan: Trading Way Below Cash

2023-04-05 01:28:51 ET

Summary

- Cullinan has one partnered lead asset and other early stage programs.

- The company is trading way below cash, which often means the market thinks the company lacks growth prospects.

- This fact, contrasted with the strong data, makes Cullinan complicated.

Cullinan Oncology ( CGEM ) is a cancer focused drug developer with a mid stage pipeline. Their approach is to develop differentiated molecules with first-in-class potential, and one of the ways they approach this is to test their molecules as monotherapies in early stages in order to “avoid uncertainty of early-stage clinical combination studies.”

On the other hand, the company has more cash than the market values its pipeline for, so that’s something we need to understand. A negative enterprise value is almost never a good sign. There is, after all, some sense in the idea that if something is too cheap, it may be because it is not worth buying. That applies here as well. A company trading below cash may sometimes mean that the market does not believe there are growth prospects to the company. This needs to be figured out.

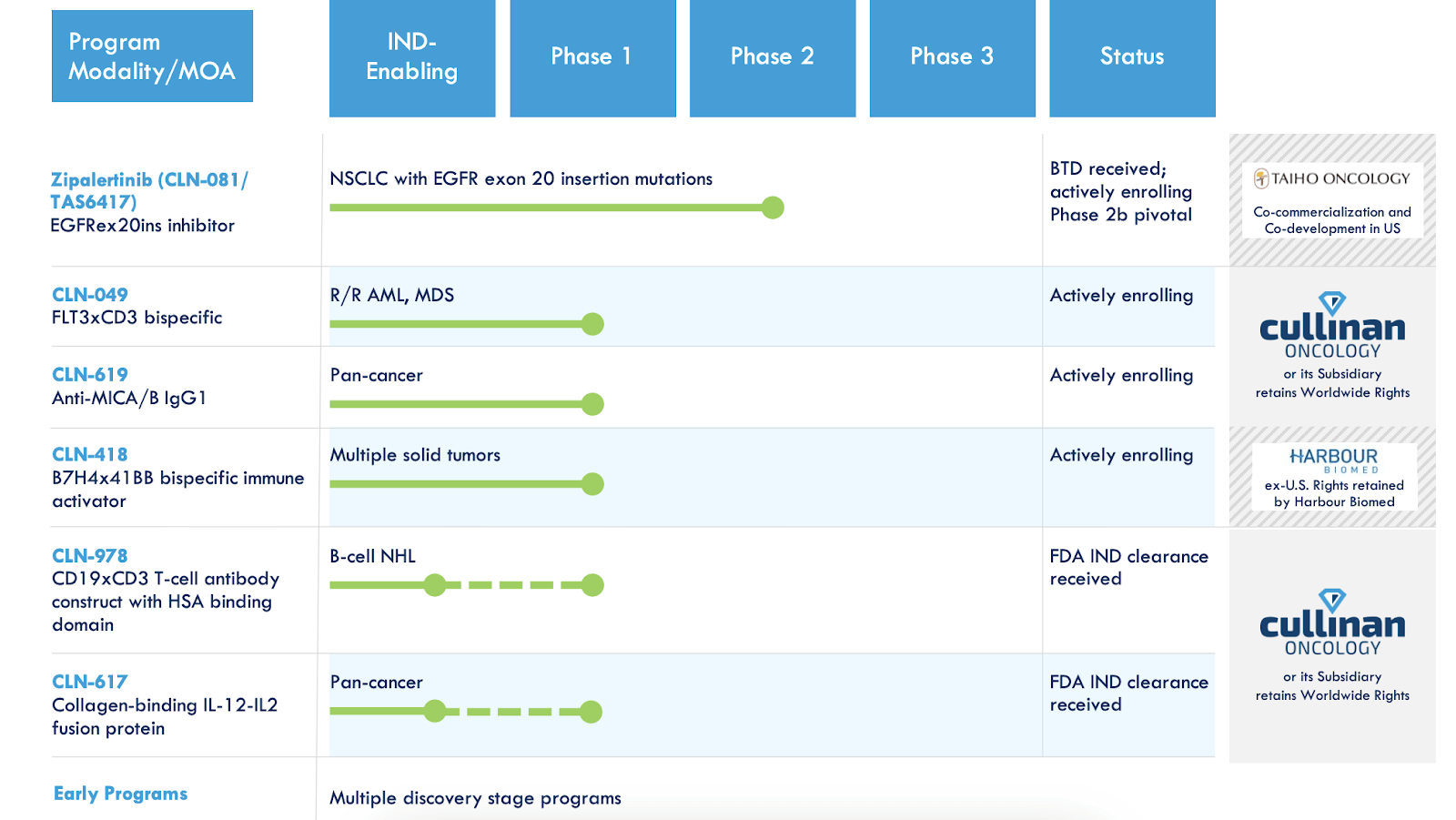

Now, Cullinan’s pipeline looks like this:

{kind=link}

Lead asset Zipalertinib (CLN-081/TAS6417) is a novel, orally bioavailable, irreversible EGFR inhibitor. This asset was in-licensed from an Otsuka subsidiary, who have recently bought back from Cullinan all rights except US and China. The molecule was designed for specificity, and in preclinical models it has shown highly selective inhibition of EGFRex20ins mutations while relatively sparing cells expressing wild-type EGFR. This is intended to avoid the toxicities associated with inhibiting wild-type EGFR.

Lead indication is NSCLC with EGFR exon 20 insertion mutations. About the unmet need, the company says:

In the U.S., approximately 16% of non-small cell lung cancer (NSCLC) cases harbor epithelial growth factor receptor (EGFR) mutations, with insertions at exon 20 (EGFRex20ins) accounting for 12% of those mutations. Patients with EGFRex20ins mutations have poorer outcomes than those with more common EGFR mutations, such as exon 19 deletions. There remains a significant unmet need for therapies targeting EGFRex20ins mutations in NSCLC that are safer and more effective.

There are approximately 238,000 US patients who will be diagnosed with NSCLC in 2023. Thus, the target population for Zipalertinib is roughly 4500 patients. Taking a ballpark estimate of $100k per patient per year (based on prices of random NSCLC molecules , really), this gets us a $450mn market for the molecule.

Coming to trial data, on checking the federal registry, I see only one phase 1 and 2 trial for this molecule. The trial is run by Cullinan, and is ongoing. The molecule is partnered with Taiho Pharmaceuticals, from which Cullinan licensed ex-Japan rights in 2019, but which were last year bought back by Taiho for $275mn. These trials begin as phase 1 and then become phase 2 as things progress. Data from the phase 1 portion has been made available. The company says the following about this data:

In ongoing Phase 1/2a study, zipalertinib (CLN-081/TAS6417) demonstrated promising efficacy in heavily pretreated patients, including patients who progressed on treatment with EGFR tyrosine kinase inhibitors (TKIs), with favorable safety and tolerability profile. Results are encouraging in heavily pretreated patients, including those who progressed with other EGFR TKI. The safety profile is amenable for long-term treatment at doses <150mg BID. Zipalertinib (CLN-081/TAS6417) demonstrates the potential to become a new standard of care to treat NSCLC harboring EGFRex20ins mutations.

Granular data from last year from the two cohorts, together and individually, is as follows:

Results indicated that the best response to treatment with CLN-081 in the overall population (n = 70) was a confirmed partial response (PR') in 36% of patients, an unconfirmed PR in 10% of patients, and stable disease in 49% of patients. Four percent of patients experienced disease progression.

Among the 36 evaluable patients who received CLN-081 at the recommended phase 2 dose (RP2D) of 100 mg twice daily, 39% achieved a confirmed PR and 1 additional patient (3%) had a PR that was pending confirmation at the time of data cutoff, which was December 1, 2021. Moreover, 8% of patients experienced an unconfirmed PR, 47% had stable disease, and 3% had progressive disease.

In the cohort of 11 patients who received CLN-081 at a twice-daily dose of 150 mg, the confirmed PR rate was 27%, the unconfirmed PR rate was 18%, the stable disease rate was 45%, and 9% of patients experienced disease progression.

What we see here is that the 100mg dose cohort did better than the 150mg cohort, so this is probably going to be the dosage of choice. Indeed, in terms of safety as well, 100mg did better. There was a grade 4 liver enzyme elevation at 150mg, and those patients were switched to 100mg. The FDA asked for a food effect study with the 150mg dose after this AE. Other than that, these are very heavily pretreated patients so PR is perhaps the best response we can hope for.

Last year, a research report noted :

Currently, none of the internationally approved EGFR tyrosine kinase inhibitors (TKIs) have demonstrated adequate antitumor activity as frontline therapy for the treatment of EGFR ex20ins NSCLC. A real-world study showed that NSCLC patients with EGFR ex20ins mutations had lower overall survival (OS') and progression-free survival (PFS') than those with common EGFR mutations (EGFR ex19del and EGFR L858R).

Thus, there is an unmet need, however, the paper goes on to cite numerous trials where OS, PFS and ORR were tested. This molecule, too, needs to bring out such data before it can be adequately compared with the existing molecules (that don’t work well). There are two other drugs approved in the exact indication, Takeda’s small molecule Exkivity, and Johnson & Johnson’s mAb Rybrevant. CLN-081 has an ORR of 41%, while Exkivity and Rybrevant have 28% and 40% respectively, so this is good news for Cullinan. Another potentially positive aspect is that both approved drugs have safety issues like rash and diarrhoea, while the wild type EGFR sparing CLN-081 has so far not seen any grade 3 or higher AEs of these two types. Dizal’s sunvozertinib/DZD9008 is a competing pipeline candidate with strong data.

Other assets are in early stages. There are 3 programs in phase 1 trials, and the rest are in discovery stages. In February, Cullinan paid Harbour BioMed $25mn for a fourth clinical stage asset, CLN-418, the only bispecific in development targeting B7H4 and 4-1BB antigens.

Financials

CGEM has a market cap of $402mn and a cash balance of $550mn. Research and development (R&D) expenses were $21.3 million for the fourth quarter of 2022, while General and administrative (G&A) expenses were $11.3 million. At that rate, the company has a cash runway extending till 2026.

Bottomline

I hope it is a little clearer why this company has more cash than its market cap. Last year, the company made a large amount of money from Taiho. CGEM stock had been trading below cash even earlier, but the difference is now stark. This, coupled with the early stage pipeline apart from the licensed lead asset, is a worry and keeps me firmly on the sidelines.

For further details see:

Cullinan: Trading Way Below Cash