CMI - Cummins: A Dividend Contender That Hasn't Been This Cheap In 3 Years

2023-12-20 07:30:00 ET

Summary

- Outside of the last few weeks, the last time Cummins traded for a P/E ratio of 12 was Summer 2020.

- The industrial posted respectable net sales and diluted EPS growth for the third quarter.

- Cummins enjoys an A+ credit rating from S&P on a stable outlook.

- Shares of the stock appear to be trading at an 11% discount to fair value.

- Cummins could triple the S&P 500 through 2025 and double it over the next 10 years.

In many ways, 2020 seems as though it was just yesterday, even though it was a full three years ago. I still vividly remember my accounting and paralegal roles at a disability and workers' comp law firm. At that time, I had just graduated with my BA in Accounting the year prior. I was also in my second full year of writing for Seeking Alpha on the side.

Who could forget the COVID-19 pandemic as well? Ever since that time, I have spent the vast majority of the last three-plus years working remotely.

Getting into the crux of this article, that was also the last time that the industrial juggernaut, Cummins ( CMI ), was this cheap. As I'll elaborate on with a discussion of the company's fundamentals and valuation for the first time in three months , I am maintaining my buy rating.

{kind=link}

Cummins' 2.7% dividend yield is nearly twice the 1.5% yield of the S&P 500 index ( SP500 ). That's also not all there is that I like about the industrial.

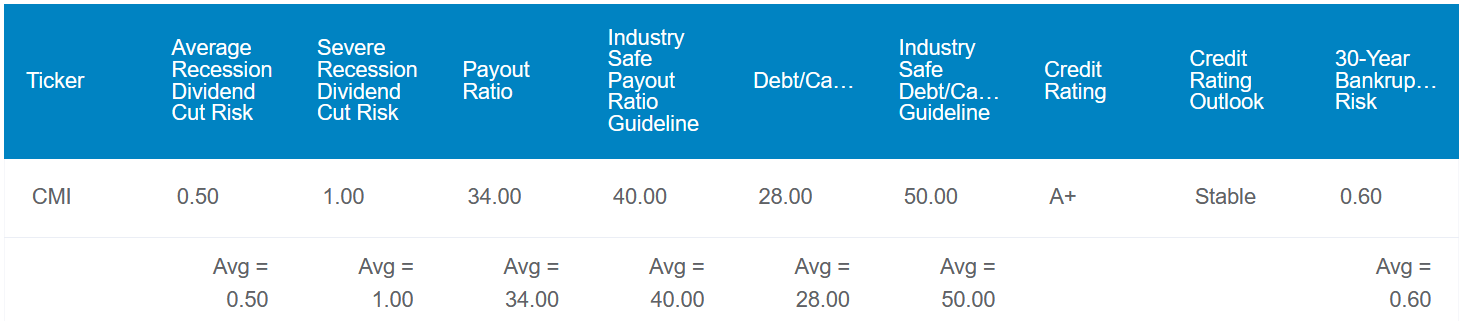

Cummins' 34% EPS payout ratio is below the 40% EPS payout ratio that rating agencies prefer from their industry. This builds a cushion into the company's dividend, which can protect it from a cut in an economic downturn.

Not to mention that Cummins' 28% debt-to-capital ratio is meaningfully less than the 40% that rating agencies like to see from a company in its industry. This explains how S&P has the conviction to rate Cummins' long-term debt an A+ on a stable outlook. That implies the probability of the company defaulting on its debt through 2053 is just 0.6%.

With these factors in mind, it makes sense that Dividend Kings estimates the risk of Cummins reducing its dividend in the next average recession is just 0.5%. That probability also only jumps to 1% in the next severe recession.

{kind=link}

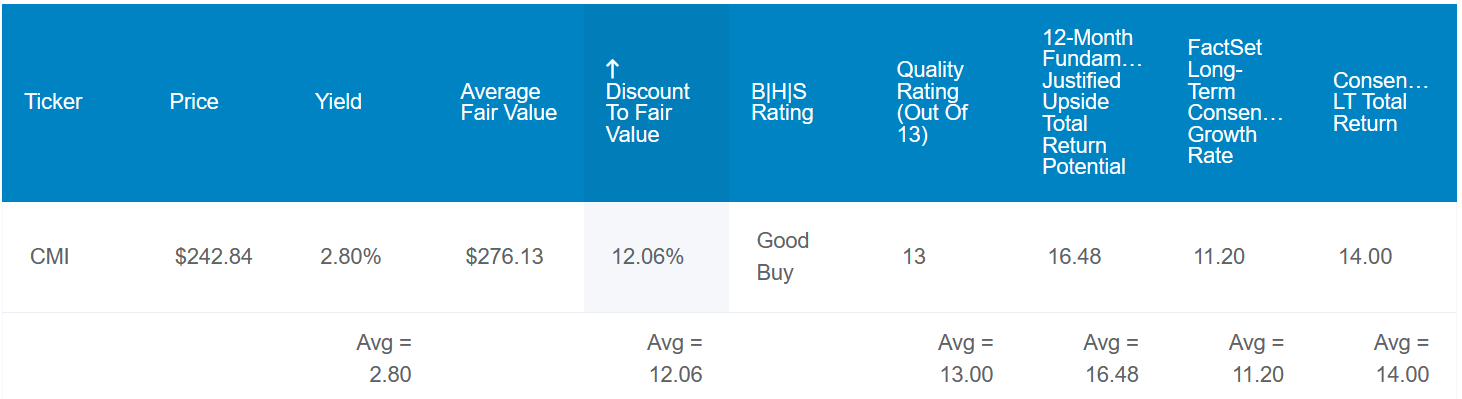

The appeal of Cummins doesn't end with its secure payout and rock-solid balance sheet, either. Shares of the industrial titan are currently priced at $244 each (as of December 19, 2023). Stacked against the historical fair value of $276 a share (using metrics like dividend yield and P/E ratio), this suggests Cummins' shares are 11% discounted.

Provided the company matches the analyst growth consensus and returns to fair value, here are the total returns that it could generate through 2033:

- 2.7% yield + 11.2% FactSet Research annual earnings growth consensus + a 1.2% annual valuation multiple upside = 15.1% annual total return potential or a 308% 10-year cumulative total return versus the 8.6% annual total return potential of the S&P or a 128% 10-year cumulative total return

Cummins Is A Fundamentally Thriving Company

Cummins Q3 2023 Earnings Presentation

{kind=link}

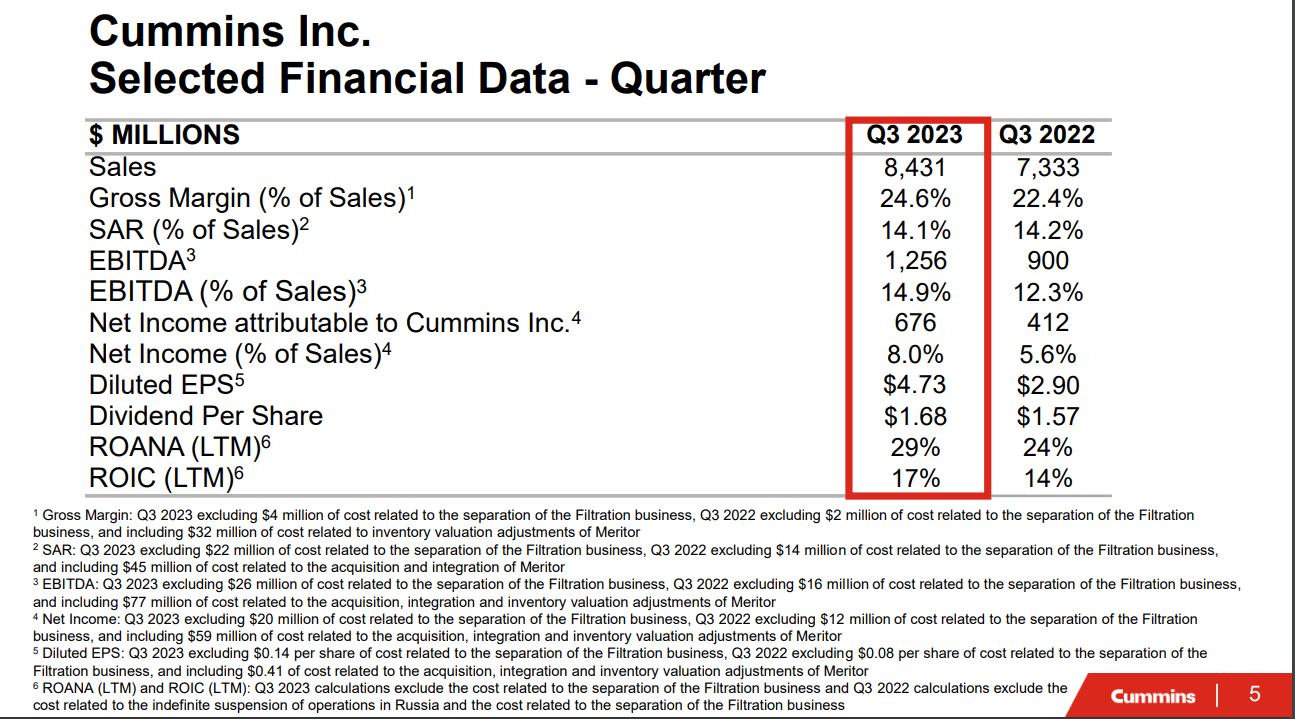

Cummins' results for the third quarter ended September 30 were what I have come to expect. The company's total net sales climbed 15% year-over-year to $8.4 billion in the quarter. This topped the analyst consensus by $250 million .

As I noted in my previous article, the automobile components producer Meritor acquisition was again primarily responsible for this growth. That is because Cummins anticipates that the company will account for $4.8 billion in midpoint net sales in 2023. On an annualized quarterly basis, that's $1.2 billion of net sales contributions. Steady demand for the company's base business was the other factor that helped net sales to grow at a double-digit rate during the third quarter.

Cummins' diluted EPS soared 63.1% over the year-ago period to $4.73 for the third quarter. For perspective, that beat the analyst consensus by $0.04. The higher net sales base from the completion of the Meritor acquisition helped diluted EPS grow in the quarter. Also, a swing in tax items from unfavorable in Q3 2022 to favorable in Q3 2023 played a role. Finally, $77 million in acquisition and integration costs in Q3 2022 relating to the Meritor acquisition lowered the bar for Q3 2023.

Cummins maintained its commitment to innovation in the third quarter, spending $376 million or 4.5% of its net sales on research, development, and engineering expenses. These costs are driving new product launches, which should propel both the top line and the bottom line higher over time.

Cummins is also still financially sound. This is supported by the company's interest coverage ratio of 11.1 through the first nine months of 2023 (details sourced from Cummins' Q3 2023 Earnings Press Release ).

Ride The Dividend Higher

Cummins has proven itself to be an excellent dividend grower over the last decade. Since 2013, the company's quarterly dividend per share has compounded by 168.8% to the current rate of $1.68 . That equates to a 10.4% compound annual growth rate. I would contend that at least high- single-digit annual dividend growth can continue in the years ahead.

This is because Cummins generated $1.8 billion in free cash flow through the first nine months of 2023. Compared to the $683 million in dividends paid during that time, this works out to a 37.7% free cash flow payout ratio (page 6 of 78 of Cummins' recent 10-Q filing ). That comfortably leaves Cummins with the capital to grow the dividend, repurchase shares, and fund acquisitions.

Risks To Consider

According to Dividend Kings' quality rating, Cummins is a perfect 13/13 ultra SWAN. This doesn't mean the company is perfect and without its risks, however.

As of just two weeks ago, the spread between the 3-month U.S. treasury and the 10-year U.S. treasury was more than -0.9. Predicting U.S. recessions by treasury spreads, the New York Fed estimates the risk of the economy entering into a recession in the next 12 months at 51.8% . If this were to occur, Cummins' operating and financial results could be unfavorably impacted temporarily.

I would also reiterate the risk that the majority of Cummins' current business mix is still diesel and natural gas engines and components. If the company's investments in R&D don't yield the products that will be in demand tomorrow, it could lose market share and growth prospects could suffer.

Summary: A Superior Business With Market-Beating Potential

FAST Graphs, FactSet FAST Graphs, FactSet

{kind=link}

{kind=link}

On every front, Cummins is an exceptional business. The company's growth prospects are robust, its market-topping payout is secure, and the balance sheet is strong.

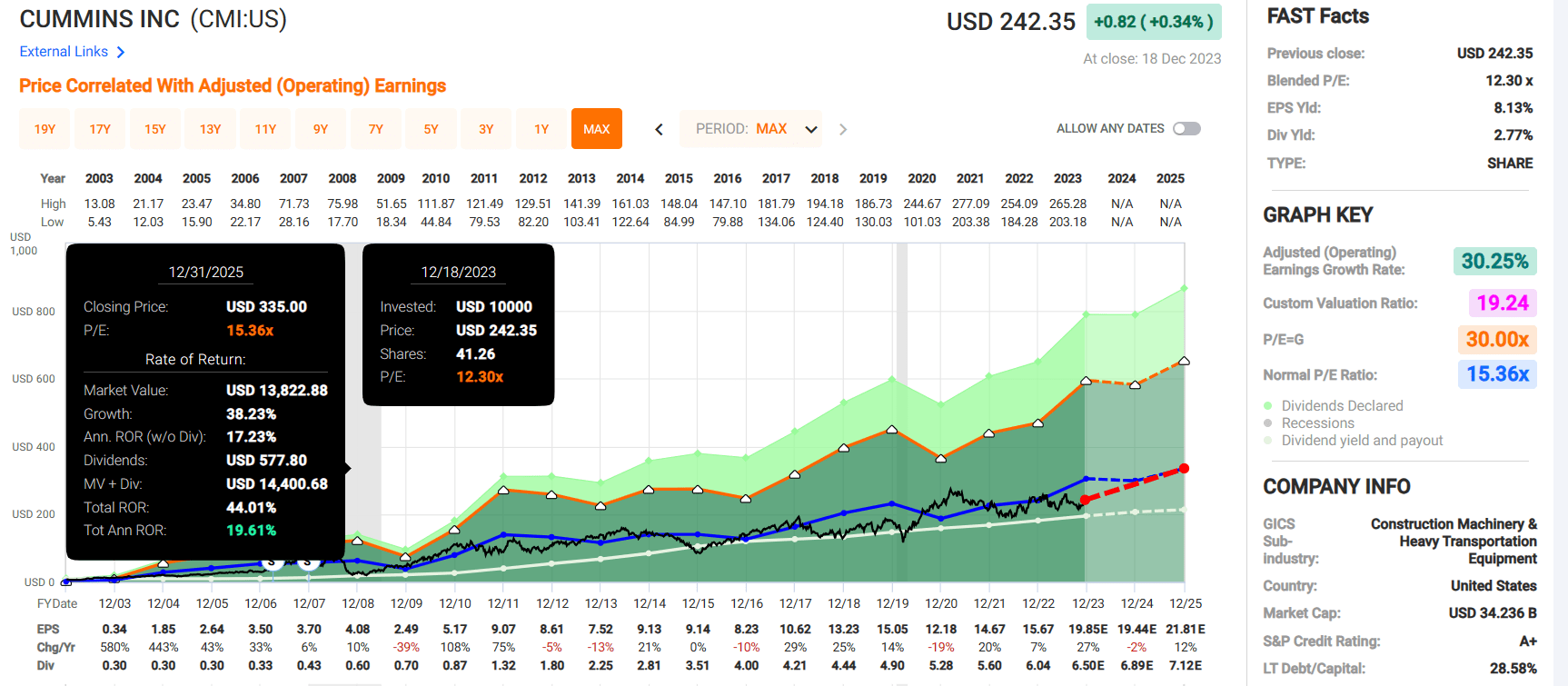

Surprisingly, the underlying stock of the business is also attractively valued. Besides recent weeks, the last time Cummins was this cheap (based on the P/E ratio) was June 2020. The stock's blended P/E ratio of 12.3 is substantially below its normal P/E ratio of 15.4. Since I believe that Cummins' fundamentals are intact, I also believe that this is a compelling valuation.

If Cummins matches growth projections and reverts to fair value, its cumulative total returns through 2025 could be 44%. That's more than triple the 14% cumulative total returns through 2025 that are expected from the SPDR S&P 500 ETF Trust ( SPY ) currently. Thus, I still rate the shares of Cummins a buy.

For further details see:

Cummins: A Dividend Contender That Hasn't Been This Cheap In 3 Years