CMI - Cummins: A Dividend Growth Stock That Can Keep Your Portfolio Trucking Along

2023-09-27 22:07:35 ET

Summary

- Cummins' diluted EPS payout ratio is poised to improve from the high 30% range in 2022 to the low 30% range in 2023.

- The company logged double-digit net sales and diluted EPS growth through the first half of the year.

- Cummins' admirable financial positioning earns it solidly investment-grade credit ratings from S&P and Moody's.

- My inputs into the dividend discount model imply the stock is priced at a 6% discount to fair value.

- Cummins' 2.9% dividend yield and strong earnings growth potential could make it a buy for dividend growth investors.

Dividend growth investing doesn't have to be complicated. Achieving success with this investing strategy can be as simple as picking leading businesses in industries that are crucial to the economy.

Well, few industries are as essential to the modern economy as transportation. The transportation system in the U.S. alone moves 49 tons of freight worth over $53 billion each day . The American Trucking Associations estimates that nearly three-quarters (72.5%) of that freight by weight is moved by trucks.

Ask yourself this question: As the economy grows, do you think that consumption of freight is going to decrease or increase over time? If you expect the latter as I do, the diesel, hybrid, and electric engines, transmissions, and batteries company Cummins ( CMI ) is a dividend growth stock worth considering for your portfolio. For the first time since November 2021 , let's dig into the company's fundamentals, risks, and valuation to lay out the buy case for the stock.

Delivering Nice Dividend Growth To Shareholders

Cummins is an all-around great dividend stock. The company's 2.9% forward dividend yield is materially greater than the industrials sector median forward yield of 1.6%. Thanks to this significantly higher starting income, the Seeking Alpha Quant system awards Cummins a B+ grade for dividend yield.

This starting income becomes especially attractive when also considering that the company's 10-year annual dividend growth rate is 11.6% - - more than the industrials sector median of 8.1%. This is good enough for a dividend growth grade of A-.

Cummins should also be able to support healthy dividend growth moving forward. This is because the company generated $15.12 in diluted EPS in 2022. Against the $6.04 in dividends per share that were paid during this time, that works out to a 39.9% diluted EPS payout ratio.

Looking at the current year, analysts believe Cummins will post $19.96 in diluted EPS. Compared to the $6.50 in dividends per share that will be doled out in 2023, this is a diluted EPS payout ratio of just 32.6%.

Finally, it is projected that Cummins' EPS will rise by 10.9% annually for the next three- to five years. Along with the low payout ratio, this should help the company extend its 18-year dividend growth streak. This is also why I believe Cummins' annual dividend growth rate should be 7.25% annually over the long haul.

Cummins Is Firing On All Cylinders

{kind=link}

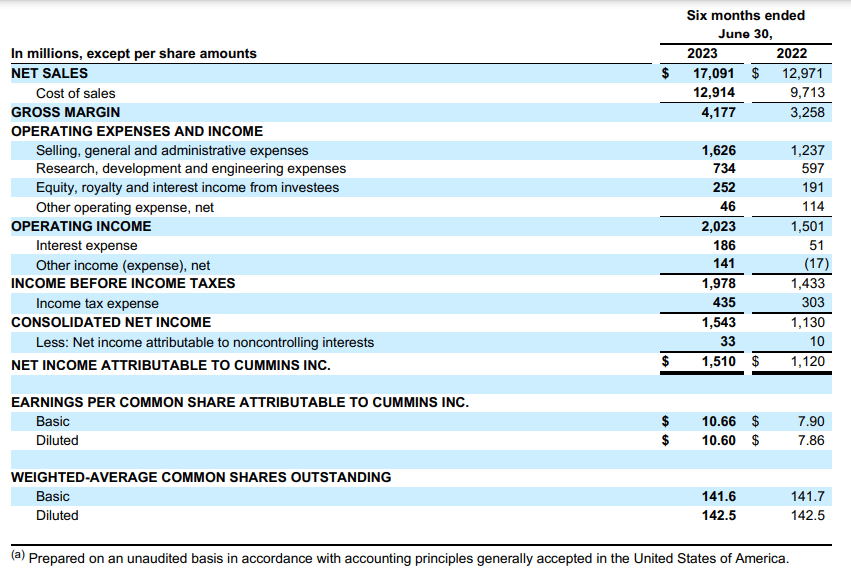

If its financial results are any indication, Cummins is off to a roaring start to 2023. The company's net sales surged 31.8% higher year over year to $17.1 billion in the first half ended June 30. How did the company put up such amazing topline growth during this time?

Cummins anticipates that its acquisition of the automobile components manufacturer Meritor will contribute between $4.7 billion and $4.9 billion in revenue for the year. That would imply that about $2.4 billion of revenue year to date or nearly 60% of growth was the result of the acquisition that closed in August 2022 . The remainder of Cummins' net sales growth was derived from robust demand and improved pricing throughout its businesses.

The company's diluted EPS soared 34.9% over the year-ago period to $10.60 for the first half of 2023. Cummins' total expenses grew at a slower rate than net sales during the first half. That is what led the company's profit margin to expand by 20 basis points to 8.8% in the first half. This fueled faster growth in diluted EPS than in net sales for the period.

Cummins isn't just a growing business. The company's interest coverage ratio was 11.6 during the first half of 2023. This rock-solid interest coverage ratio is precisely why Cummins enjoys respective investment-grade credit ratings of A+ and A2 from S&P and Moody's (unless otherwise linked, all info sourced from Cummins Q2 2023 earnings press release and page 53 of 159 of Cummins 10-K filing ).

Risks To Consider

Cummins posted record second-quarter revenue. But even with that being the case, investors need to know some of the risks before becoming a shareholder in the stock.

As a company operating in the cyclical industrial sector, Cummins isn't completely immune to the risk of a looming recession. This would negatively impact demand for its products temporarily, which would weigh on net sales and profits.

Another risk to Cummins is that its core business is still diesel and natural gas engines/components. The company is working on electrified powertrains and fuel cells. But there is no guarantee that these efforts will translate into market-leading share in newer technologies. If Cummins can't win top market share in these technologies, that could put a damper on future growth. That is especially the case if the shift away from diesel and natural gas engines/components accelerates.

A Sensible Valuation For A Blue Chip Dividend Stock

Cummins has shed 5% of its value so far in 2023. This looks to have positioned the stock as a buy for dividend growth investors based on my inputs into a valuation model.

Investopedia

The valuation model that I am referring to is the dividend discount model or DDM. This includes the following three inputs.

The first input into the DDM is the annualized dividend per share. The company's annualized dividend per share is $6.72 at this time.

The next input for the DDM is the cost of capital equity or annual total return rate. I target 10% annual total returns, so that is what I will assume for this input.

The final input into the DDM is the annual dividend growth rate. As noted above, I will use a 7.25% annual DGR.

These inputs for the DDM give me a fair value output of $244.36 a share. This suggests that the shares of Cummins are trading at a 6.1% discount to fair value and offer a 6.5% upside from the current price of $229.49 a share (as of September 27, 2023).

Summary: Buy Cummins Stock Now And Add On Weakness

Cummins is an excellent pick for dividend growth investors for a variety of reasons: These include the company's low payout ratio, respectable growth prospects, and proven reputation as a dividend grower.

Cummins doesn't leave a sizable margin of safety for investors around $230 a share. That is why I believe the stock is a marginal buy at the current share price and that investors should add more aggressively to their positions on any dips moving forward.

For further details see:

Cummins: A Dividend Growth Stock That Can Keep Your Portfolio Trucking Along