CMI - Cummins: Forget The AI-Rally Buy The Heat Rally

2023-07-20 08:05:00 ET

Summary

- Cummins stock price has rallied since the start of June, with its power generation solutions being a possible catalyst in a warming environment.

- CMI's strong performance is supported by a robust balance sheet, a 2.6% dividend yield, and positive long-term outlook driven by electrolization and truck fleet modernization.

- Risks include potential slower-than-expected demand from China and competition from alternative power generation sources, but CMI's A+ credit rating and strong financials provide a safety net.

Lots of focus has been put on AI stocks in recent months, with many names now far surpassing their previous all-time highs. With this sector now appearing to be way too expensive, those investors seeking the next big thing may want to consider the 'heat rally', which includes names that remain reasonably priced and which are well-positioned to benefit from warmer temperatures globally.

This brings me to Cummins ( CMI ), which I last covered here back in April of last year. It appears that my bullish take has paid off, with the stock giving investors a 33% total return since then, far surpassing the flat performance of the S&P 500 ( SPY ) over the same timeframe.

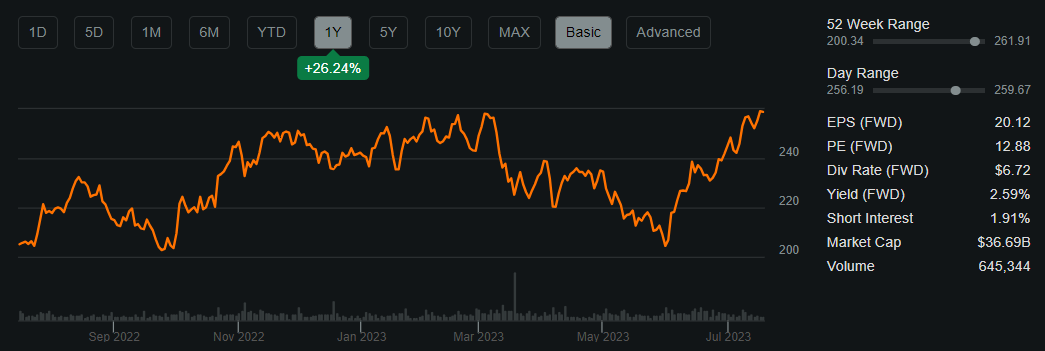

As shown below, CMI's share price has picked up momentum since the start of June and is now near its 52-week high. In this article, I provide an update and discuss why CMI remains a good value at present.

{kind=link}

CMI Stock (Seeking Alpha)

Why CMI?

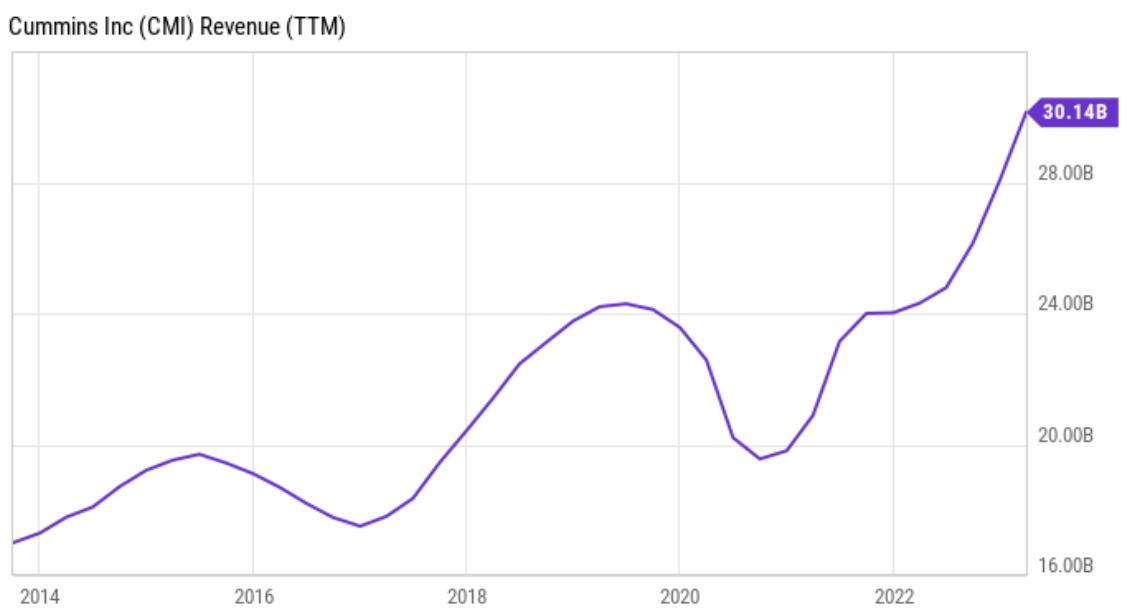

Cummins is a global power leader that designs, manufactures, and distributes diesel, natural gas, electric and hybrid powertrains around the world. It was founded over a century ago in 1919 and over the trailing 12 months, generated $30.1 billion in total revenue. CMI has demonstrated a fairly strong track record with revenue nearly doubling over the past 10 years, as shown below.

{kind=link}

YCharts

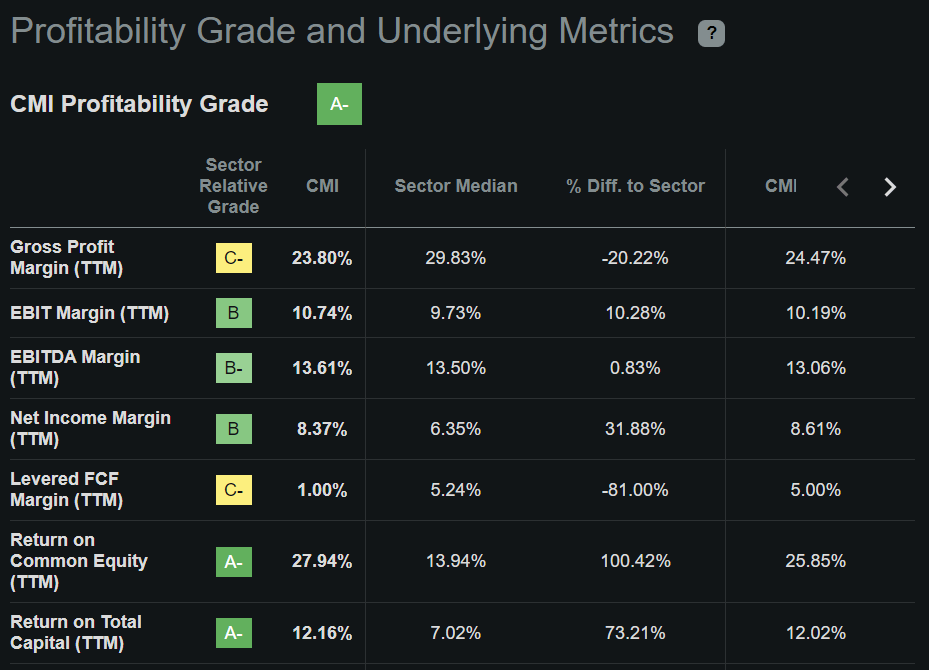

The company is also shareholder-friendly, having reduced its share count by 13% over the trailing 5 years. This has resulted in a boost to the return on equity, which sits at 28% and is well above the 14% sector median. As shown below, CMI also generates a healthy net income margin of 8.4%, which is 200 basis points higher than the sector median.

{kind=link}

Seeking Alpha

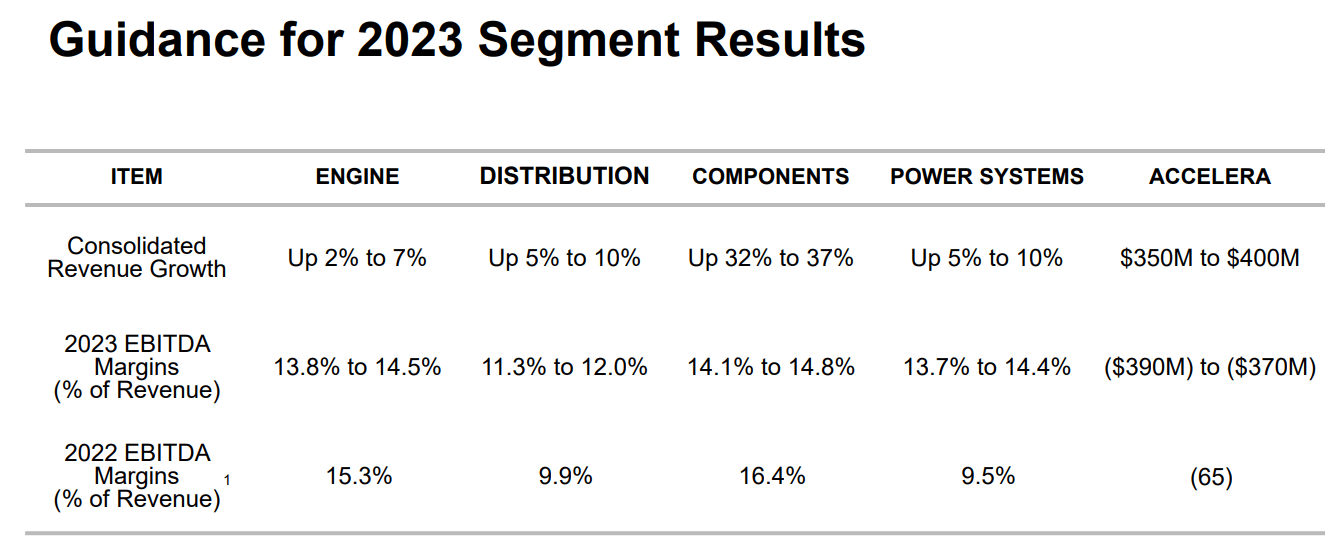

Meanwhile, CMI has executed strongly amidst economic uncertainty, with revenue reaching a record $8.5 billion during the first quarter. This combined with a positive outlook resulted in management raising full-year revenue growth guidance to 18% and EBITDA margin to 15.4% at the midpoint. This is driven by strong North American truck and aftermarket demand. As shown below, 2023 growth is expected to be driven by growth in all segments across the company, particularly in components and power systems.

{kind=link}

Earnings Presentation

Looking ahead, near-term growth is supported by the current labor shortage, with trucking companies continuing to modernize their fleets to attract the best drivers, as management noted during a recent industry conference. Also, the current heat wave experienced around the world is showing no signs of letting up. This could result in more than expected demand for CMI's generators that deliver power to HVAC systems, as they deliver cooling to areas and regions that previously did not need them.

Also hydrogen remains a secular tailwind for the company, as it ramps up its electrolyzer business. According to the IEA, the number of countries with polices that directly support investment in hydrogen technologies is increasing, along with the number of sectors they target, and there are around 50 targets, mandates and policy incentives in place today that direct support hydrogen, with the majority focused on transport.

Management sounded bullish around the long-term prospects around electrolyzers and near-term opportunities, including one that is 4.5x the size of its last biggest electrolyzer project, as noted during the recent industry conference :

We have been excited about the electrolyzer business for some time. In our Analyst Day last year, on Hydrogen Day, we talked about building towards a backlog and then getting the business to breakeven by 2027 overall, but building towards kind of a 400-megawatt backlog kind of a number.

There’s been all kinds of challenges in getting projects off the ground, and of course, the IRA [Inflation Reduction Act] is a very different incentive driver and so lots of interest, all of a sudden really fast. We did the biggest electrolyzer project in 2021 at 20 megawatts and we have just closed our first 90-megawatt plant.

Risks to CMI in the near term include potential for slower-than-expected demand from China, as its recovery since emerging from lockdowns has been underwhelming, with consumers holding back on spending. In addition, alternate sources of power generation, such as battery power and storage may impede on hydrogen-related growth for CMI, although it does have electrification solutions of its own.

Importantly, CMI carries a strong balance sheet with an A+ credit rating to deal with whichever challenges that may arise. This is supported by $2.4 billion in cash and short-term investments on hand, and a low net debt to TTM EBITDA ratio of just 1.4x, sitting far below the 3.0x level that most ratings agencies consider to be safe.

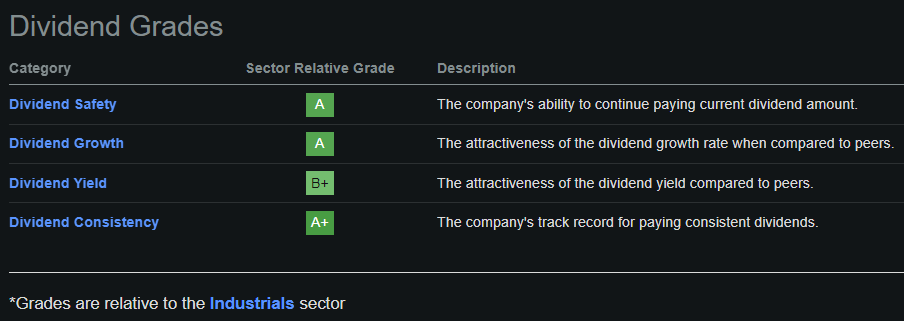

This lends support to the 2.6% dividend yield, which is well-covered by a 33% payout ratio and has a 5-year CAGR of 8%. As shown below, CMI carries mostly A grades among its dividend metrics that include safety, growth, yield, and consistency relative to the industrials sector.

{kind=link}

Seeking Alpha

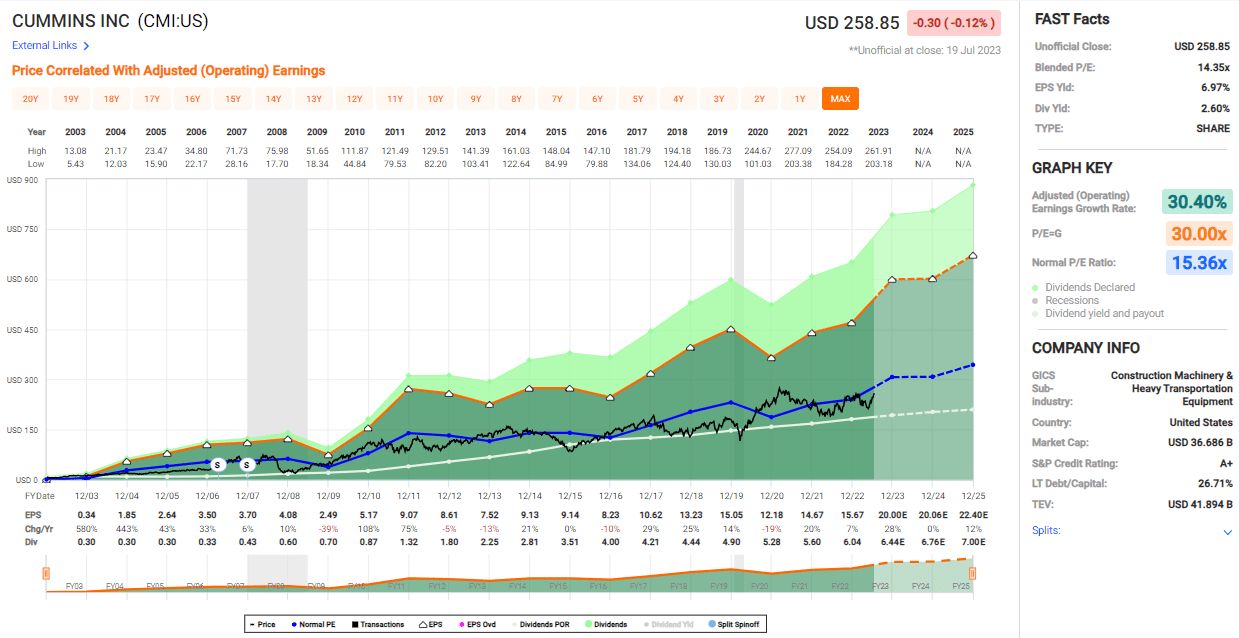

Lastly, while CMI is no longer cheap at the current price of $259, it's not expensive either with a forward PE of 12.9, sitting below its normal PE of 15.4. I believe that CMI warrants a higher PE valuation of 15+, considering its trailing 5-year annual EPS growth of 9.8%, and the expectation that it could reasonably deliver mid to high-single digit annual EPS growth going forward.

{kind=link}

FAST Graphs

Investor Takeaway

Cummins remains a good value at present given its strong balance sheet and positive long-term outlook that is supported by the current heat wave and truck fleet modernization. The company carries an attractive dividend yield of 2.6%, which has been increasing at a strong clip over the past five years, while also providing solid capital gains potential as the stock remains priced below its normal valuation. All in all, CMI is a buy at current levels and offers long-term investors an attractive total return opportunity despite the recent rally in the share price.

For further details see:

Cummins: Forget The AI-Rally, Buy The Heat Rally