CMI - Cummins: Navigating Challenges With Resilience And Record Revenues

2023-08-14 07:00:00 ET

Summary

- Cummins reported strong earnings with record revenues and organic growth, despite economic challenges.

- The company hiked its dividend by 7% and maintained its full-year guidance.

- Cummins hinted at potential headwinds in the future but remains well-positioned for growth and innovation.

Introduction

Cummins ( CMI ) is one of my favorite machinery dividend stocks. The only reason why I don't own it is because I own Caterpillar ( CAT ) and Deere & Company ( DE ). Owning three machinery companies in a 22-stock portfolio is a bit too much.

The reason I'm writing this article is because the company reported its earnings earlier this month, which showed tremendous strength. Despite economic challenges, the company achieved record revenues and strong organic growth.

It also hiked its dividend by 7% last month and stuck to its full-year guidance.

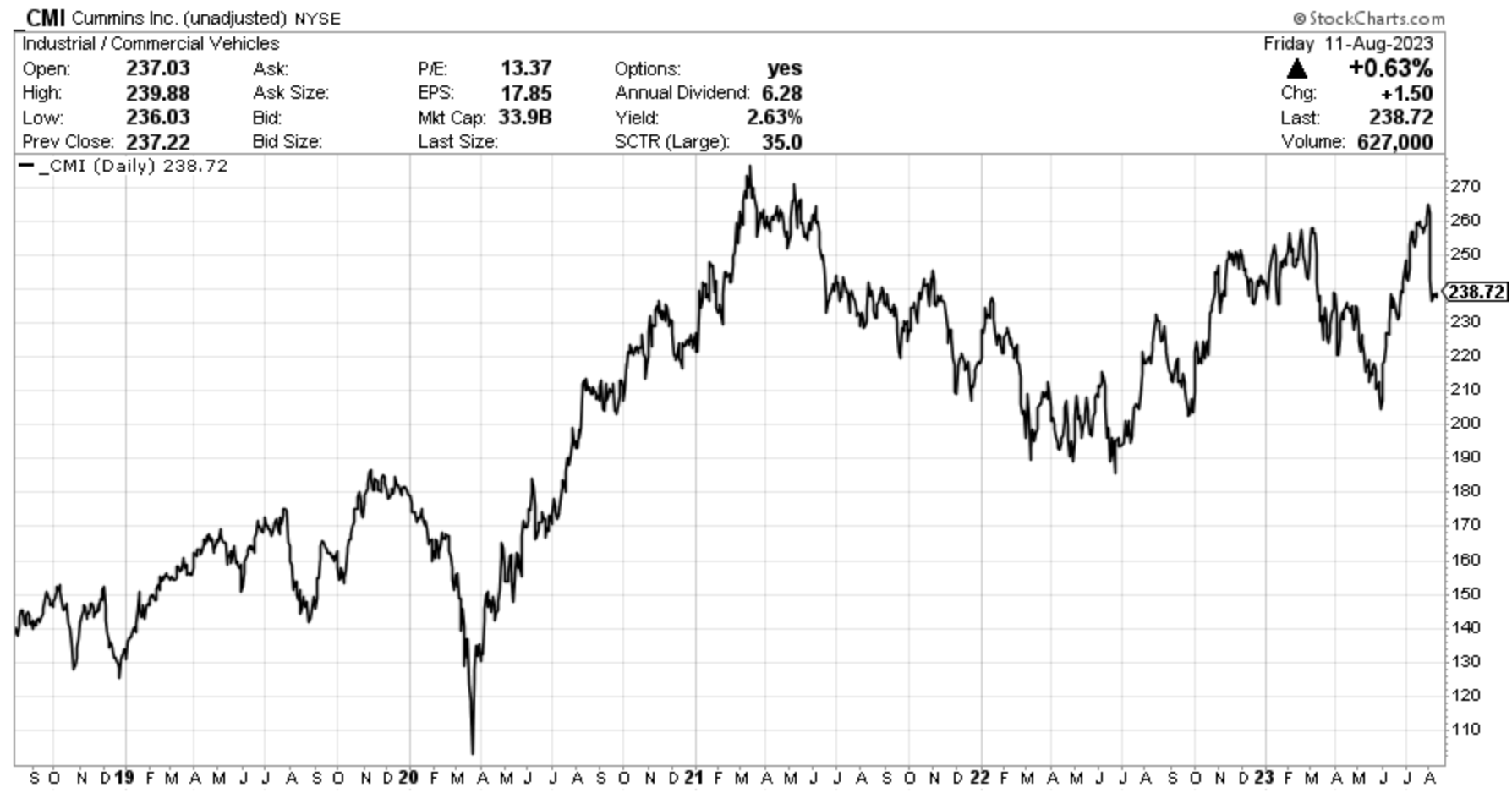

However, the stock showed some weakness recently, as it fell roughly 10% since reporting its earnings.

{kind=link}

StockCharts

The problem is that the company hinted at potential headwinds down the road.

While we see demand remaining strong through 2023 and we are maintaining our guidance on revenue and profitability, we continue to closely monitor global economic indicators . Should economic momentum slow, Cummins will remain in a strong position to keep investing in future growth, bringing new technologies to customers as we advance our Destination Zero strategy, and returning cash to shareholders.

While I don't want to put words in the company's mouth, this is a very diplomatic way of saying we may have to adjust our guidance lower in the next few months .

In this case, the company's fears are supported by significant weakness in indicators like the ISM Manufacturing Index.

While the factory activity gauge improved to 46.4, it remains in contraction territory for the ninth-straight month.

Bloomberg

This is what Bloomberg commented shortly after the data release:

While other parts of the economy remain firm, high interest rates paired with an ongoing rotation in consumer preferences toward services have stifled the manufacturing sector. Sluggish demand abroad has proved to be an additional headwind.

With all of this in mind, let's dive into the details!

What Happened In 2Q23?

Despite the fact that economic growth started to slow two years ago, the company continues to fire on all cylinders.

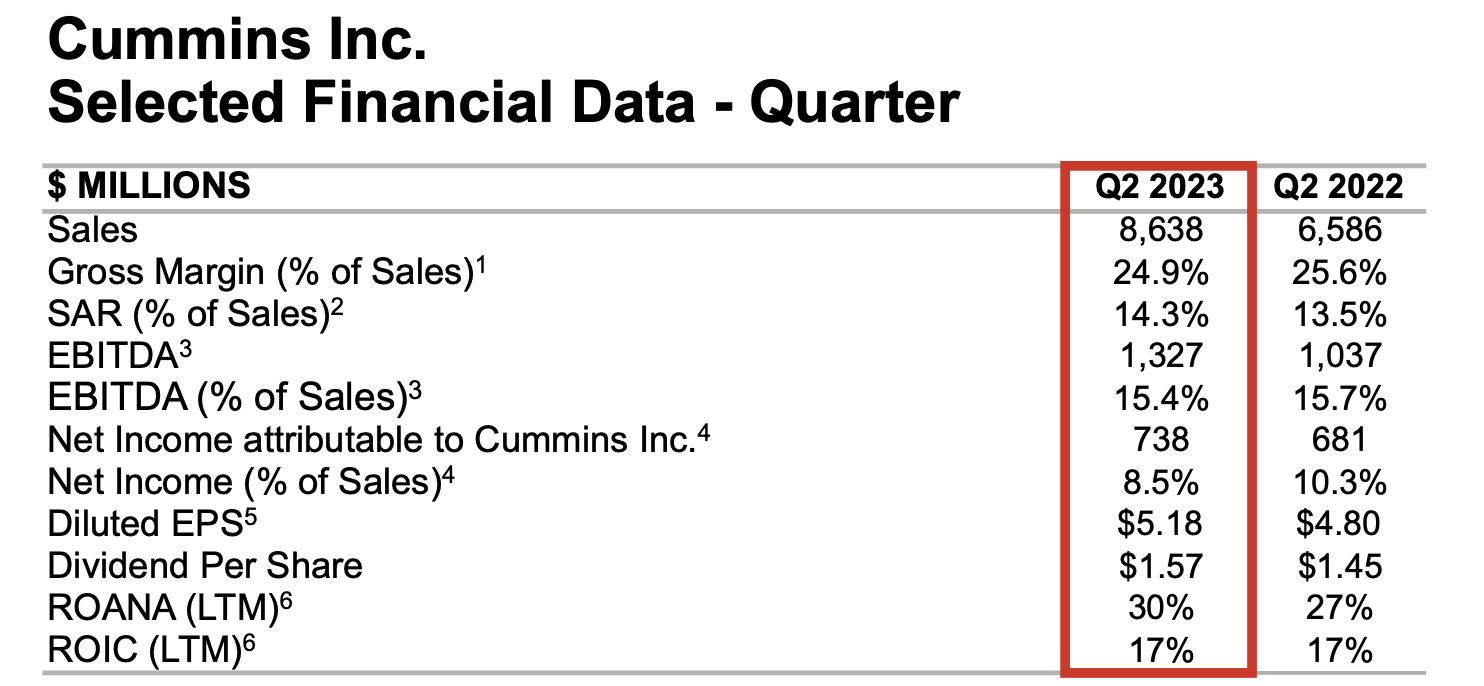

In the second quarter, the company reported record revenues of $8.6 billion, a remarkable increase of 31% compared to the previous year. Notably, sales in North America grew by 31%, and international sales saw a 32% increase.

{kind=link}

Cummins Inc.

Note that revenue growth was supported by a 19% increase in sales due to the acquisition of Meritor.

Even adjusted for this major deal, the company saw organic sales growth of 12%, supported by improved pricing and strong demand for its products on a global scale.

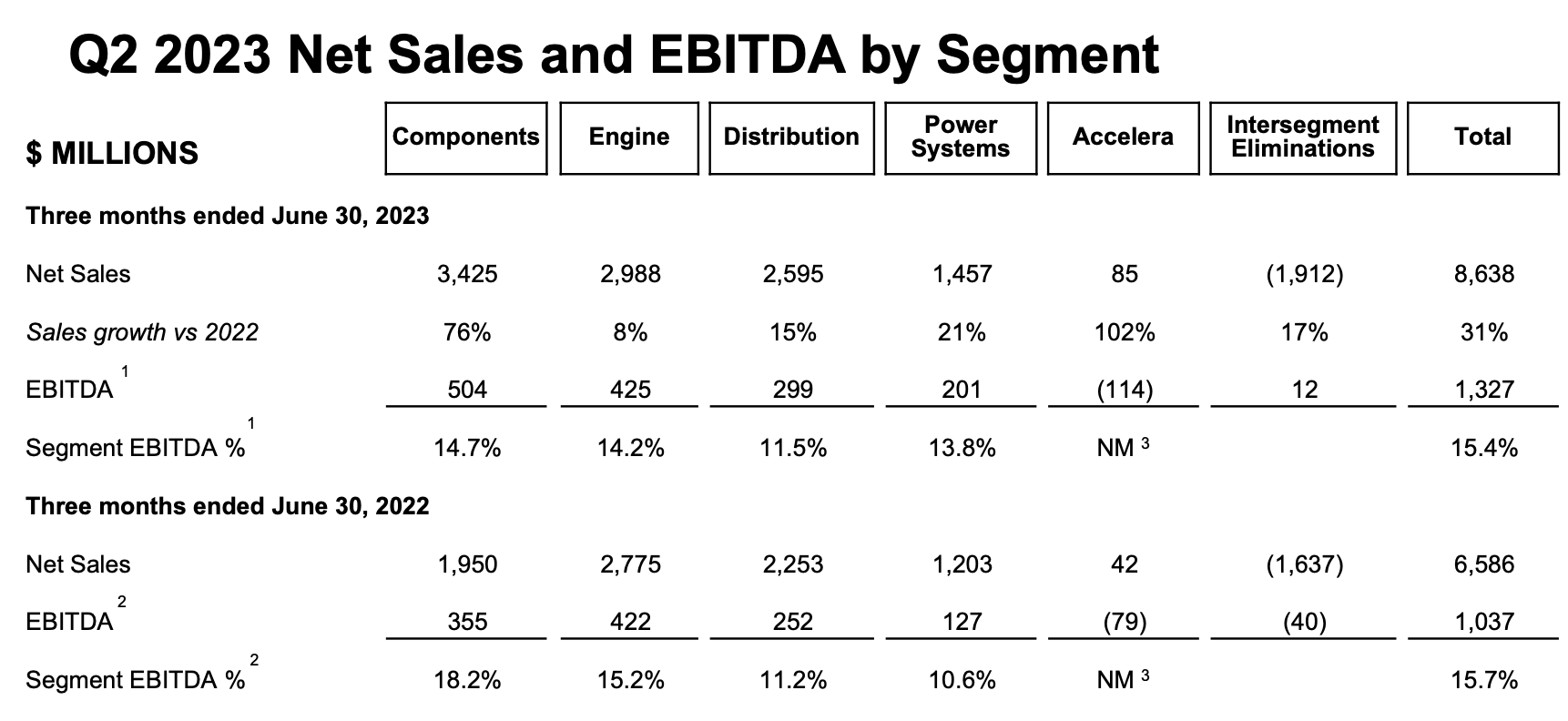

The table below shows sales growth per segment, in addition to the total EBITDA margin and EBITDA margin per segment.

{kind=link}

Cummins Inc.

Despite strong revenue growth, the EBITDA margin slightly declined from 15.7% to 15.4%. This was primarily attributed to factors like the dilutive impact of the Meritor acquisition, higher variable compensation costs, and increased development spending.

Lower margins are also the reason why the company missed adjusted EPS expectations, despite beating revenue estimates by $250 million.

Seeking Alpha

Based on this context, the company noted favorable industry tailwinds, including an 11% rise in heavy-duty truck production, while engine sales to construction customers increased by 8%. Power generation revenues improved by 16%.

International revenues increased by 32%, attributed to Meritor and strong demand.

The company's revenue from China rose by 37%, with improved medium- and heavy-duty truck demand and sales. Light-duty market sales increased by 23%. From India, its revenues grew by 22%, driven by strong power generation and on-highway sales.

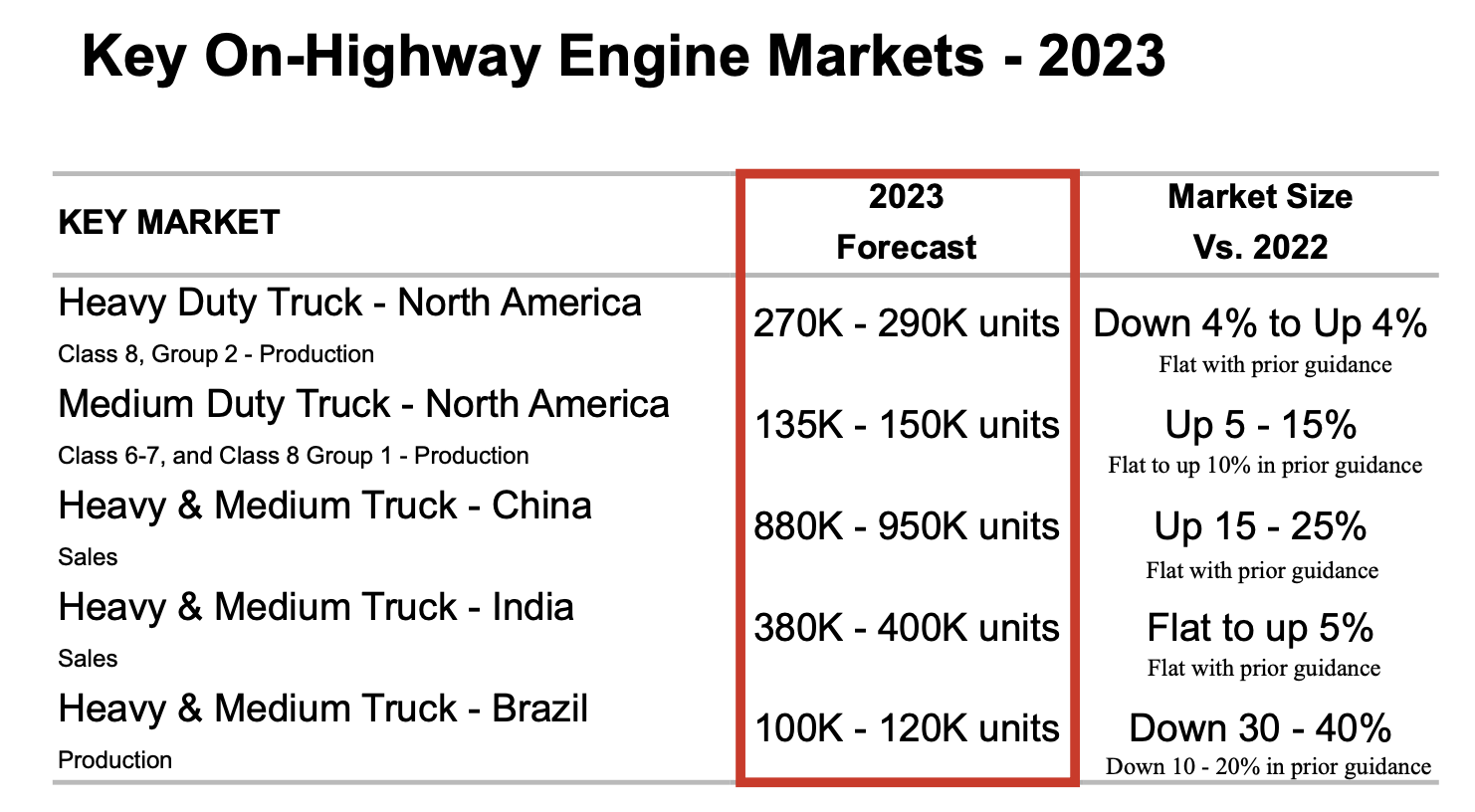

In general, it can be said that the company's key markets remain strong. The company was also able to stick to its guidance in major truck markets like North America, China, and India.

{kind=link}

Cummins Inc.

Furthermore, Accelera, Cummins's brand for its new power business, launched in March. Accelera is an energy technology leader with a portfolio of zero-emission solutions, including battery systems, fuel cells, ePowertrain systems, and electrolyzers.

In other words, it's the net-zero business of Cummins that people are increasingly talking about.

{kind=link}

Cummins Inc.

While these technologies come with strong growth, it's far from being a major driver of the company's total sales and income.

For example, in 2Q23, Accelera saw 102% revenue growth to $85 million. Unfortunately, EBITDA was negative $114 million.

Nonetheless, the company is making great progress in this segment and seeing robust demand supporting its expansion plans.

Accelera is initially dedicating 89,000 square feet of the existing Cummins power generation facility in Fridley to electrolyzer production with the opportunity to expand to meet the growing demand. Accelera also reached a further milestone of electrolyzer order backlog totaling over $500 million at the end of the quarter. The Fridley facility will help address that growing demand, along with other capacity being added globally. - Cummins 2Q23 Earnings Call

With that in mind, let's take a look at the company's forward-looking statements.

The Company's Guidance

Despite the decline in economic growth, the company maintained its full-year 2023 revenue guidance of 15% to 20% growth, and EBITDA is expected to be in the range of 15% to 15.7%.

- Heavy-duty trucks in North America are projected to be 270,000 to 290,000 units.

- Revenue from China is expected to increase by roughly 15%.

- Revenue from India is projected to be up around 6%. Major high horsepower markets are expected to remain strong.

As we discussed in the introduction, the company also hinted at uncertainty, which could mean that it might lower guidance in the not-too-distant future.

Hence, Cummins emphasized its ongoing focus on achieving strong incremental margins, improving the performance of Meritor, reducing inventory levels, and investing in products and technologies that align with lower carbon solutions. Not only are these things important, in general, but they are great ways to protect the bottom line in case the economy starts to weaken more than expected.

The company also acknowledged a potential decrease in second-half revenues and plans to manage operating expenses accordingly.

Dividend & Valuation

As I already briefly mentioned, the company hiked its dividend by 7% to $1.68 per share (per quarter). This translates to a yield of 2.7%. It also marks the company's 14th consecutive annual hike.

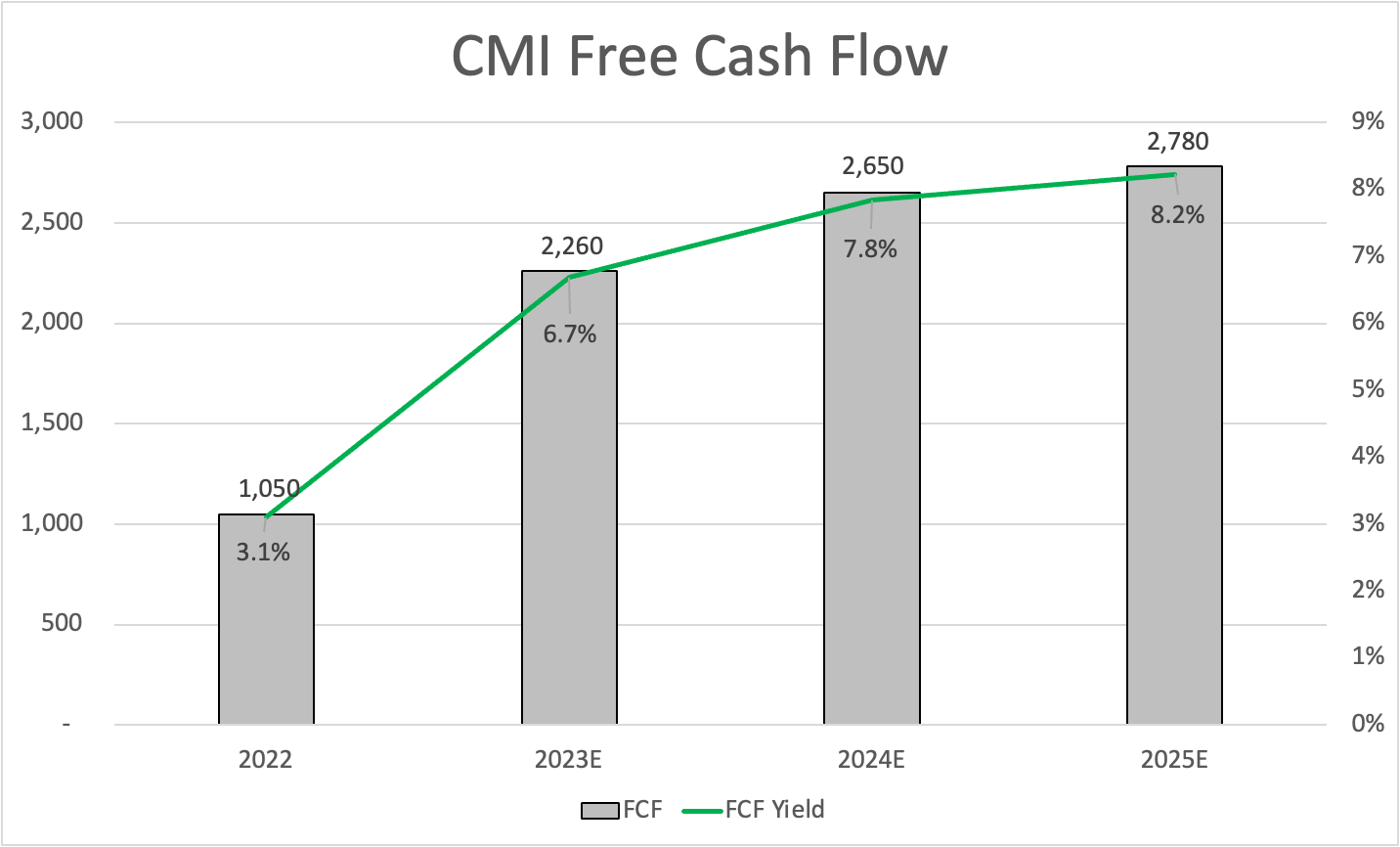

This dividend is backed by a load of free cash flow. This year, the company is expected to generate $2.3 billion in free cash flow, which translates to a 6.7% free cash flow yield. This also implies a 40% cash dividend payout ratio, which is very healthy.

{kind=link}

Leo Nelissen (Based on analyst estimates)

On top of that, free cash flow is expected to gradually increase to $2.8 billion, which shows tremendous room for accelerating investments in new technologies and excess free cash flow for solid long-term dividend growth.

These numbers also suggest that CMI is trading at less than 13x 2024E free cash flow.

The longer-term median is 18x free cash flow.

Although economic uncertainty persists, investors are getting a good price for CMI shares at these levels.

In other words, I do agree with the consensus price target of $262, which is 10% above the current price.

However, I cannot make the case that CMI is a no-brainer buy.

Given economic challenges, I advise investors interested in CMI to buy gradually. Start small and add gradually over time. If shares decline, investors can average down. If the stock were to suddenly take off, investors would have a foot in the door.

This is how I usually deal with (new) investments - especially at this stage of the economic cycle.

Takeaway

Cummins shines as a standout machinery dividend stock. While I don't hold it due to my existing Caterpillar and Deere positions, the recent earnings report showed remarkable resilience.

Despite global challenges, Cummins achieved record revenues, boosted its dividend, and stuck to its guidance.

However, the company subtly hinted at potential headwinds ahead, causing a recent stock dip.

Despite changes in economic indicators, Cummins is well-positioned for growth, innovation, and creating value for shareholders.

For example, the launch of Accelera's net-zero solutions is promising, although it's a small part of the business.

With a steady dividend increase and strong cash flow, Cummins presents an enticing opportunity, especially at a conservative valuation.

Although I agree with the consensus price target and maintain a Buy rating, I do suggest that investors interested in CMI should be cautious and add gradually over time.

For further details see:

Cummins: Navigating Challenges With Resilience And Record Revenues