CMI - Cummins: Still Cheaply Priced

2023-07-12 17:39:57 ET

Summary

- Cummins presents a compelling investment opportunity as the US economy is performing much better than expected.

- The spending of the construction industry continues to trend up, which should drive the demand for trucks and construction equipment.

- Thanks to the favorable backdrop, the latest earnings demonstrated strong growth in both the top and the bottom line.

- The current valuation is discounted compared to the historical average and other industrial companies such as Caterpillar.

Investment Thesis

As the US stock market continues to rise, it is getting increasingly harder to find great companies trading at bargaining prices. Cummins ( CMI ), despite trading near its 52-week high, is still a compelling value pick in my opinion. The company's backdrop remains favorable in the near term as construction spending continues to increase rapidly. The US economy is also holding up much better than expected, which should provide support for demand. I believe this, alongside its cheap valuation, should translate to an accretive opportunity for investors.

Cummins Background

Cummins is an industrial giant that specializes in a broad range of power solutions including diesel and natural gas engines, battery systems, and other related components such as filtration and control systems. The Indiana-based company is present in over 190 countries with blue-chip customers such as Paccar ( PCAR ), Air Products and Chemicals ( APD ), and NextEra Energy ( NEE ).

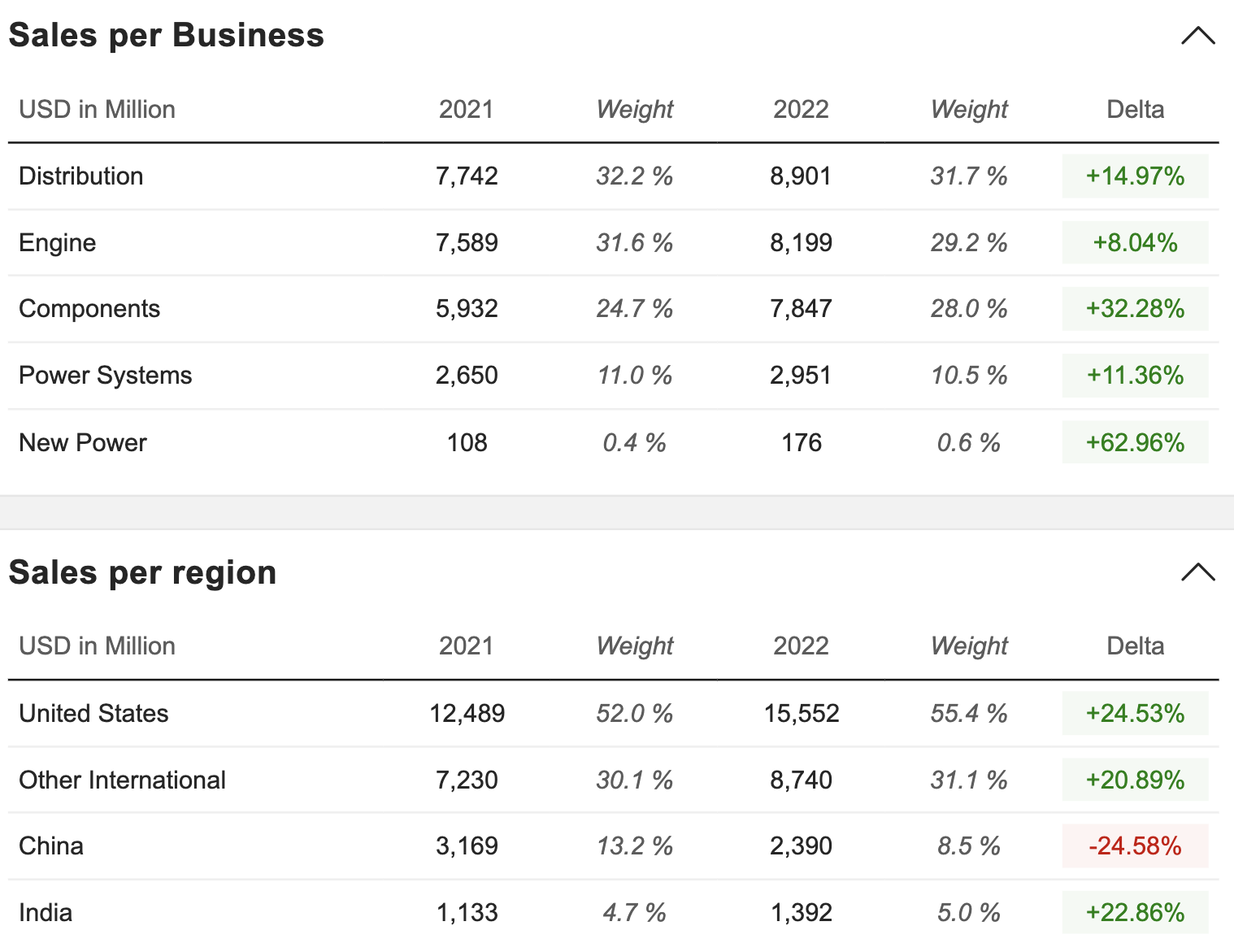

As shown in the chart below, its business is separated into 5 segments including distribution, engine, components, power systems, and new power. Most of the company's revenue comes from the engine segment, which manufactures engines for trucks, vehicles, construction equipment, etc. The distribution segment is then responsible for the sales of these products and their aftermarket services and supports. Currently, over 55% of Cummins' revenue is generated in the US, followed by China and India at just 8.5% and 5% respectively. Given the nature of its business and target demographic, the company's sales growth largely depends on the US economic growth, especially around industrial and construction-related industries.

{kind=link}

Favorable Construction Spending

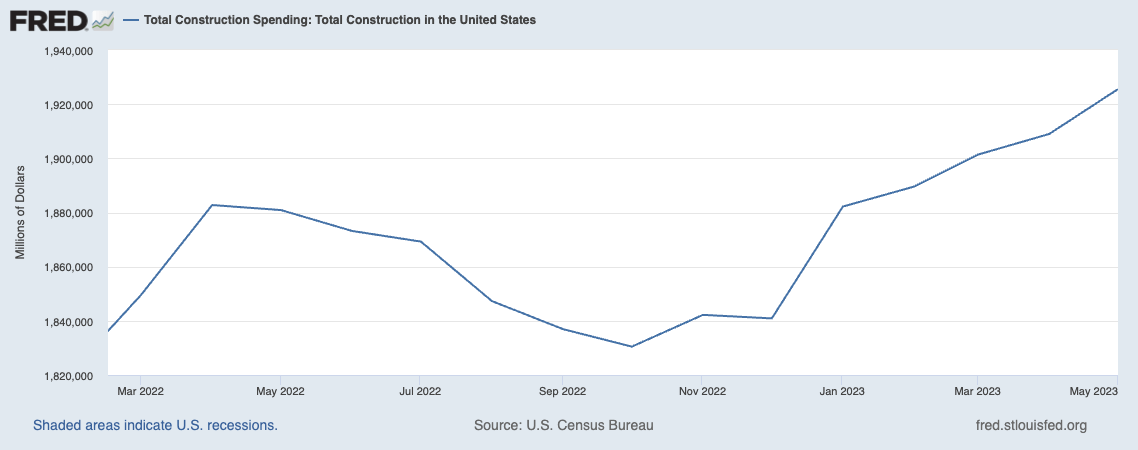

The overall economy has been softening amid higher interest rates, but the construction industry remains an outlier as spending continues to pour in. According to FRED (Federal Reserve Economic Data) , the annual seasonally-adjusted construction spending reached an all-time high of $1.93 trillion in May. This is up 1% from $1.91 trillion in April and up 2.7% from $1.88 trillion in the prior year. As shown in the chart below, spending has rebounded significantly since October last year. This should present meaningful tailwinds for the company as the ongoing increase in construction spending should continue to drive the demand for heavy trucks.

{kind=link}

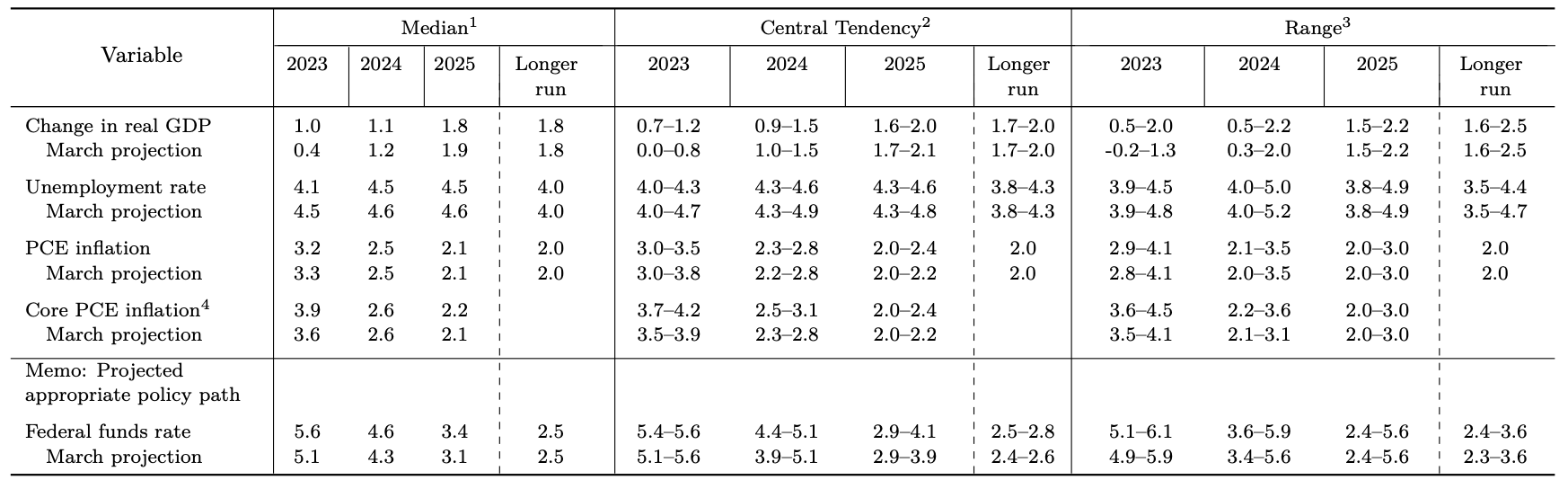

The US economy is also holding up much better than most expected. Thanks to the robust labor market, the Federal Reserve raised its median real GDP projection from 0.4% YoY (year over year) in March to 1% in the recent meeting, as shown in the chart below. The projected median unemployment rate was also revised from 4.5% in March to 4.1%. This should favor Cummins considering its high exposure to the US economy.

{kind=link}

Strong Financials

Amid the favorable backdrop, Cummins' latest earnings were very strong. The company reported revenue of $8.45 billion, up 32% YoY compared to $6.39 billion. The growth was largely driven by the acquisition of Meritor and the upbeat momentum in North America. Organic sales growth was 12%.

Amid strong construction spending, the industry's production of heavy-duty trucks grew 17% YoY while the company's heavy-duty unit sales grew 27%. The overall revenue from North America increased 39% to $5.1 billion.

The bottom line was also impressive, as spending remains disciplined. SG&A (selling, general, and administrative) expenses as a percentage of revenue declined 70 basis points from 9.6% to 8.9%. R&D expenses as a percentage of sales also dropped 60 basis points from 4.7% to 4.1%.

This alongside higher pricing resulted in the adjusted EBITDA up 48.4% from $930 million to $1.38 billion. The adjusted EBITDA expanded 170 basis points from 14.6% to 16.3%. The net income was $790 million compared to $418 million, while the diluted EPS was $5.55 compared to $2.92, up 90% YoY.

Given the strong momentum, the company also raised its full-year guidance. It now expects revenue growth to be between 15% and 20%, up from the previous range of 12% and 17%. The adjusted EBITDA margin is also now expected to be between 15% to 15.7%, compared to the prior 14.5% to 15.2%.

Cheap Valuation

Despite trading near its 52-week high, Cummins' valuation remains cheap in my opinion. The company is currently trading at a PE ratio of 14.3x, which is discounted compared to both its historical average and peers.

As shown in the first chart below, the current multiple is near the low end of its historical range, representing an 8% discount from its 5-year average PE ratio of 15.5x. If we use the fwd PE of 12.8x, which accounts for the upcoming growth, the discount is even larger at 10%. The company is also cheaply priced against other major industrial peers such as Caterpillar ( CAT ). As shown in the second chart below, the two companies had been trading at a similar valuation but the trend has recently diverged. Caterpillar's PE ratio of 18.7x now represents a significant premium of 30.8% compared to Cummins.

Risk

Recession is the obvious risk for Cummins at the moment. The global economy has been quite soft and the yield curve is already extremely inverted, which often correctly predicts a recession. However, I believe the most important question here is not whether a recession will come, but when will it come.

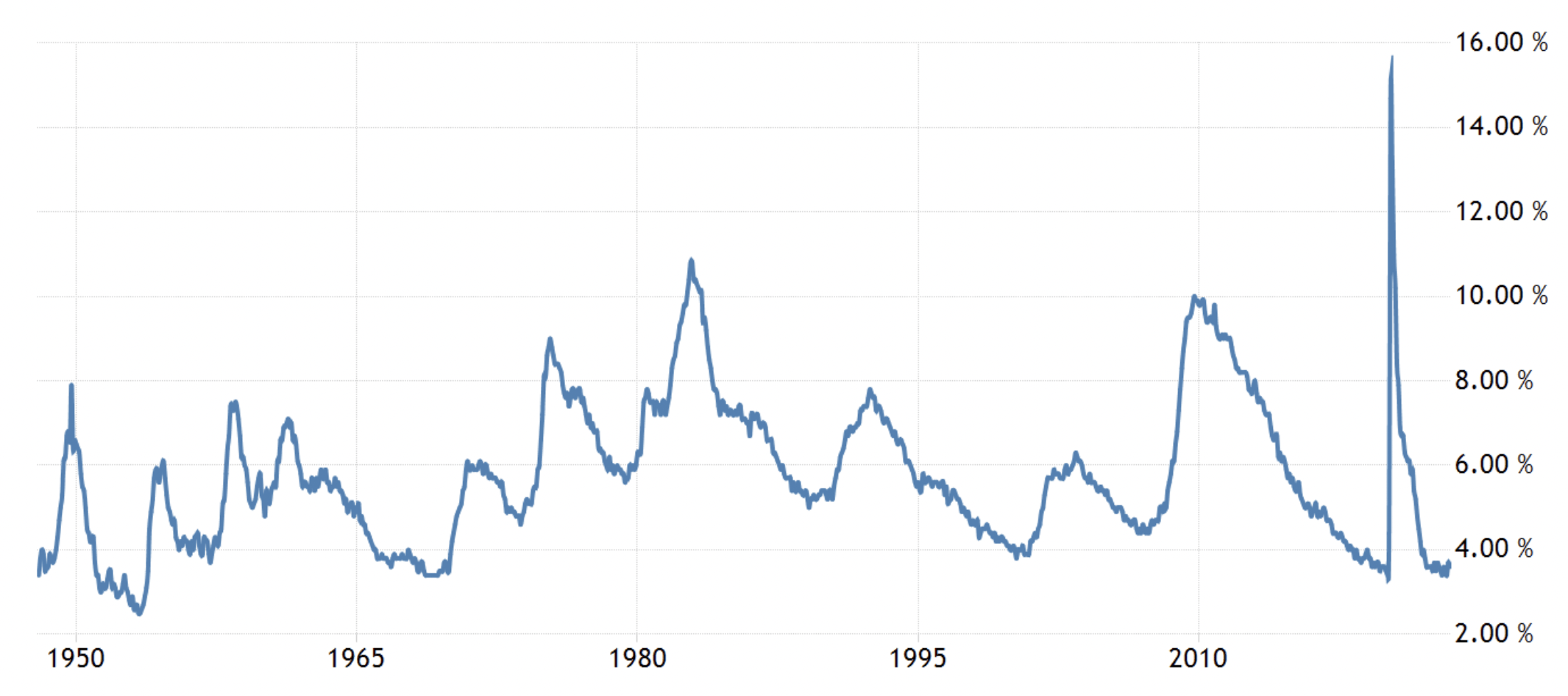

The compressed valuation seems to be pricing in a recession this year but I am leaning more towards next year. As shown in the chart below, the current unemployment rate is still near a historical low at just 3.6%, which should continue to support overall demand. Job gains are softening but it will likely take months before we see a meaningful deterioration in unemployment, which should buy some time for the economy.

{kind=link}

Investors Takeaway

Cummins looks like a great value pick in my opinion. The strong construction spending trend should continue to be a major growth driver in the near term. The tailwind is clearly shown in the latest earnings, as the demand for heavy-duty trucks remains upbeat and the guidance was also raised.

The strong fundamentals and discounted multiple should present ample opportunity for multiple expansions. There should be meaningful upside potential if the valuation can catch up to peers such as Caterpillar. Therefore I rate Cummins as a buy at the current price.

For further details see:

Cummins: Still Cheaply Priced