HAWX - Currency Impact In International Investing: A Guide For U.S. Investors

2023-12-11 13:56:12 ET

Summary

- Many investors are looking at international equities for their lower valuations and higher expected returns.

- The question of currency hedging seems to be answered with the idea that it does not matter.

- Looking at the evidence and the real returns however shows that hedging currency may make sense for U.S. investors.

A Dynamic Look at Currency Hedging: Theory vs Practice

Recently I was asked about investing in international markets. Given their lower valuations and potential to outperform US markets in the years to come, I advised the questioner to consider it given their objectives. Then they asked me an interesting question: "Should I hedge my currency exposure?" This got me thinking. Of course, most of the academic studies indicate that it is a question not worth investors' time. In the end, whether you hedge or do not hedge, your returns are likely to be similar. But this is really an academic answer.

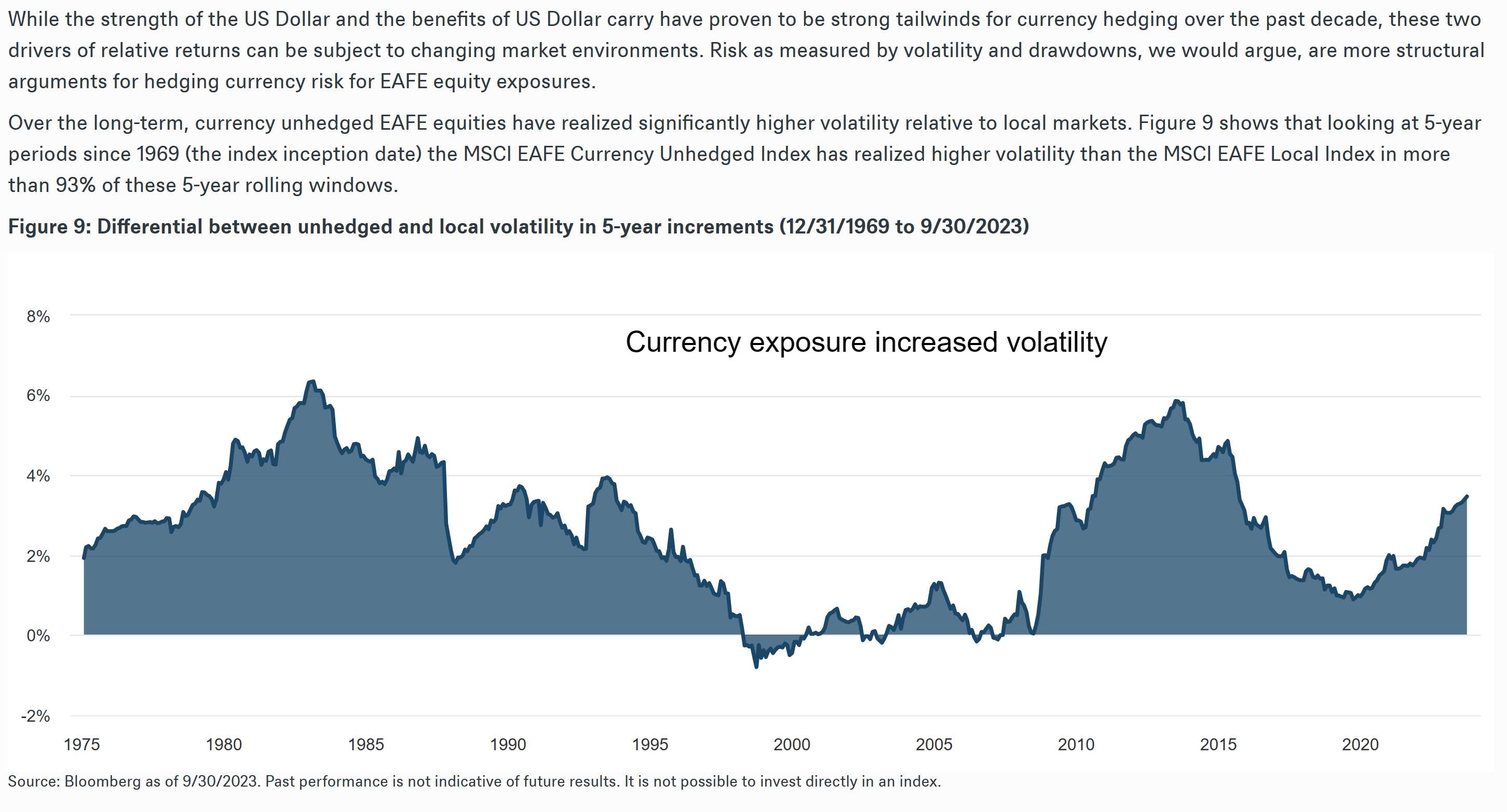

In reality, whether an investor is likely to stay with their investment strategy comes down to how volatile it is, and what returns it produces. The one seemingly free lunch in investing just might be currency hedging. When you hedge your currency in international markets, you are likely to bring down the overall volatility of the portfolio.

{kind=link}

Even if you are an investor who does not care about short-term volatility, there are several reasons to consider currency hedging. Most importantly, you are likely a US investor, you store your wealth in US dollars, and thus, hedging your currency provides you with the returns of the international stocks you own, without having to make an additional investment in international currency markets. This becomes quite important because while stocks tend to go up over time, international currency markets, move wildly. This may create a situation where your international investments did quite well in USD terms, yet are looking at a loss when converted from a foreign currency.

Academic Evidence on Currency Hedging

There is a great deal of evidence supporting the idea that currency hedging is something that investors should not concern themselves with. Here are just three examples.

1. The Performance of Currency-Hedged Foreign Equities, by Lee Thomas

This study:

"examined the performance of equities in Germany, France, Canada, the United Kingdom, Japan and Switzerland from 1975 through 1988, comparing unhedged results to hedged results for a U.S. dollar investor. These six stock markets accounted for about 88% of the world market capitalization, excluding the United States. The study used FT-Actuaries Indices equity returns, included dividends, and assumed that at the beginning of each month the investor hedged by selling forward (for U.S. dollars) for one-month delivery the foreign currency value of his equity shares. Over the 1975 through June 1988 study period, the compounded annual returns on hedged and unhedged foreign equities were 16.4% and 16.5%, respectively."

Thomas, conclusively found in another study that hedging foreign currency exposure in foreign bond portfolios, substantially reduced overall volatility.

2. Asset Allocation with Hedged and Unhedged Foreign Stocks and Bonds, by Philippe Jorion

"examined the hedged and unhedged results for an investment in the Morgan Stanley Capital International (“MSCI”) EAFE (Europe, Australasia, Far East) Index from January 1978 through December 1988. This study, like the preceding study by Lee Thomas, assumed that at the beginning of each month, the foreign currency exposure was hedged through a one-month forward sale of the foreign currency value of the equity holdings. Over the January 1978 through December 1988 period, the average annual returns on hedged and unhedged foreign equities were 20.9% and 22.9%, respectively."

3. Currency Hedging Programs: The Longer-Term Perspective, by The Brandes Institute.

"compared the results of hedging currency versus not hedging currency from the perspective of investors in each of the 23 developed market countries in the MSCI World Index over the 32-year period from the end of 1972 to December 31, 2004. The Brandes study developed a database of quarterly results for each of the 23 countries and then calculated simulated passive fully hedged and unhedged results from the standpoint of an investor whose home currency was the particular currency of each of the 23 countries."

"The study showed that in six of the eight largest countries (Australia, France, Germany, Japan, Switzerland and the United Kingdom), the hedged results exceeded the unhedged results by between .20% and .94% annualized over the 32-year period. In two of the eight largest countries (Canada and the United States), the hedged results were worse than the unhedged results by .65% and 2.23% annualized, respectively, over the 32-year period that ended December 31, 2004. For the other 15 countries in this 23-country study (Austria, Belgium, Denmark, Ireland, Italy, Netherlands, Norway, Spain, Sweden, Finland, Greece, Hong Kong, New Zealand, Portugal, and Singapore), the currency hedged results exceeded the unhedged results by between .21% and 2.34% annually for 12 of the countries, and the unhedged results exceeded the currency hedged results by between .52% and 2.19% annually for three of the countries."

Currency Fluctuations are Real and Can Be Significant

So, what exactly does it mean to hedge one's foreign currency against the US Dollar, for example? Well, an investor who engages in this practice may have a contractual gain, or cost, depending on whether U.S. interest rates are lower or higher than interest rates in the target currency being hedged. If an investor sells forward the foreign currency of a country whose rates are lower than the US, they will have a locked in contractual gain, and vice versa.

{kind=link}

If one chooses not to hedge their foreign currency, they should know what they are in for. Movements in foreign currency markets can be significant, ultimately increasing the volatility of the international equity investment.

"Possible losses from changes in currency exchange rates are a risk of investing unhedged in foreign stocks. While a stock may perform well on the London Stock Exchange, if the British pound declines against the U.S. dollar, your gain can disappear or become a loss. In addition, currency fluctuations are generally more extreme than stock market fluctuations.

During the more than fifty years that Tweedy, Browne has been investing, the Standard & Poor's 500 Stock Index has declined on an annual basis more than 20% only four times, in the back-to-back bear market of 1973 and 1974, in the technology and telecommunications crash of 2002 and in the financial collapse of 2008. By contrast, the U.S. dollar/pound, U.S. dollar/Swiss franc, U.S. dollar/euro, and U.S. dollar/yen relationships have moved more than 20% on numerous occasions. There was a four-to-five-year period from 1979-1984 when the U.S. dollar value of British, French, German and Dutch currency declined by 45% to 58%.

More recently, during the years 2011 through 2016, the U.S. dollar value of Eurozone, Swiss, British and Japanese currency experienced peak to trough declines of between 29% and 40%. There have also been numerous steep declines in foreign currencies in the shorter term. In the 16-month period between November 8, 2007 and March 10, 2009, the U.S. dollar value of a British pound declined from $2.10 to $1.37, a 35% decline; in the seven-month period from April 22, 2008 to November 20, 2008, the U.S. dollar value of a euro declined from $1.59 to $1.24, a 22% decline.

To recoup the 45% to 58% losses that a U.S. investor incurred by owning British, French, German and Dutch currency unhedged during the 1979-1984 period, returns ranging between 82% to 138% were required. Similarly, during the years 2011 through 2016, returns of 41% to 67% were required to recoup the 29% to 40% declines in the Euro, the Swiss franc, the British pound and the Japanese yen. The chart that follows illustrates the extraordinary interim exchange rate volatility faced by U.S. dollar-based investors in Euro-denominated securities since the currency’s introduction in 1999." (How Hedging Can Substantially Reduce Foreign Stock Currency Risk-Tweedy Browne & Co)

Bloomberg/Tweedy Browne & Co.

{kind=link}

Comparing Hedged and Unhedged Products

Hedging can mean the difference between sticking with your international allocation and not. When we look at the last five years of stock returns from international markets. The Vanguard FTSE All-World ex-US index ( VEU ) returned 1.20% vs 4.18% for the ACWI Ex-USA Currency Hedged ( HAWX ). The currency hedged portfolio not only did better, but it did so at considerably less volatility and higher overall Sharpe ratio.

Portfolio Visualizer/Authors Calculations

{kind=link}

These indexes are nearly identical, so the difference you see is really the added return or loss from currency fluctuations. Both results are abysmal compared to the S&P 500 Index ( VOO ) which returned 9.35%, but this is immaterial. The benefits of international diversification are many, including a higher return for reduced overall risk, when added to a well-diversified portfolio.

Again, when we look at quality, and look at the WisdomTree Quality Dividend Growth Fund Currency Hedged ( IHDG ) and compare it to both the Vanguard International Dividend Growth Index ( VIGI ) and the DFA Intl. Hi Relative Profitability Fund ( DIHRX ) both unhedged products, the results were wildly different for the same five-year period as above.

Portfolio Visualizer/ Authors Calculations

{kind=link}

Again, notice not only did the currency hedged product beat both of the non-currency hedge products, but it did so with less risk producing a higher Sharpe ratio.

The Quantitative Approach

The final approach is defined by Jason Chen of the DWS Research Institute as the "correlation breakeven" which he defines as:

"the volatility of an unhedged EAFE investor consists of 3 components: 1. The volatility of the local equity market, 2. The volatility of the basket of currency exposure, and 3. The correlation between the local equity and the currency. If we combine these components into a formula, we can determine at which level of correlation investors would be indifferent between the volatility of currency hedged EAFE versus currency unhedged EAFE. We refer to this equation as the “Correlation Breakeven”:

DWS Research Institute

In simplified terms, the correlation between the local equity market and the currency must be less than negative one-half of the ratio of the currency volatility to the local equity volatility. Perhaps the most important part of this equation is that this correlation breakeven must always be negative. In other words, the correlations between equities and currencies must be negative (and in some cases significantly negative) to justify not hedging the currency risk purely as it relates to risk or volatility reduction."

His analysis Currency Hedging: how has it worked, and how might it work going forward? concludes with a reasonable application of the correlation breakeven.

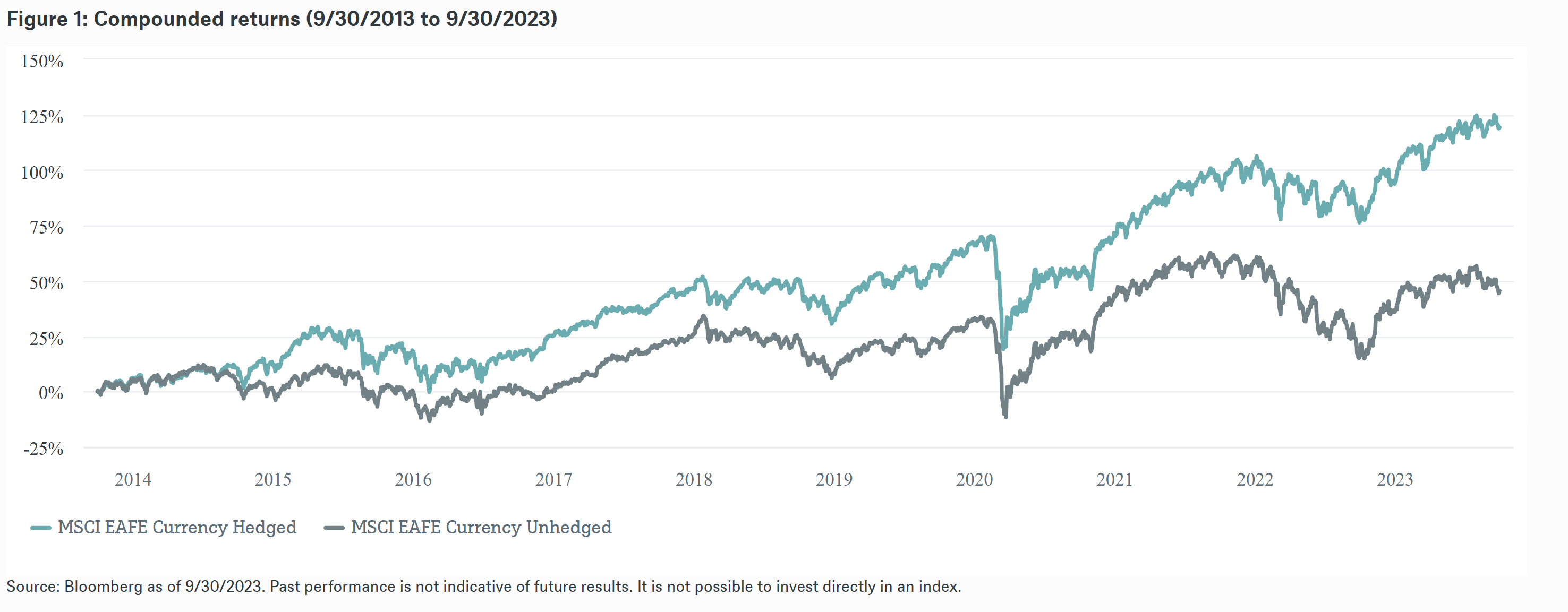

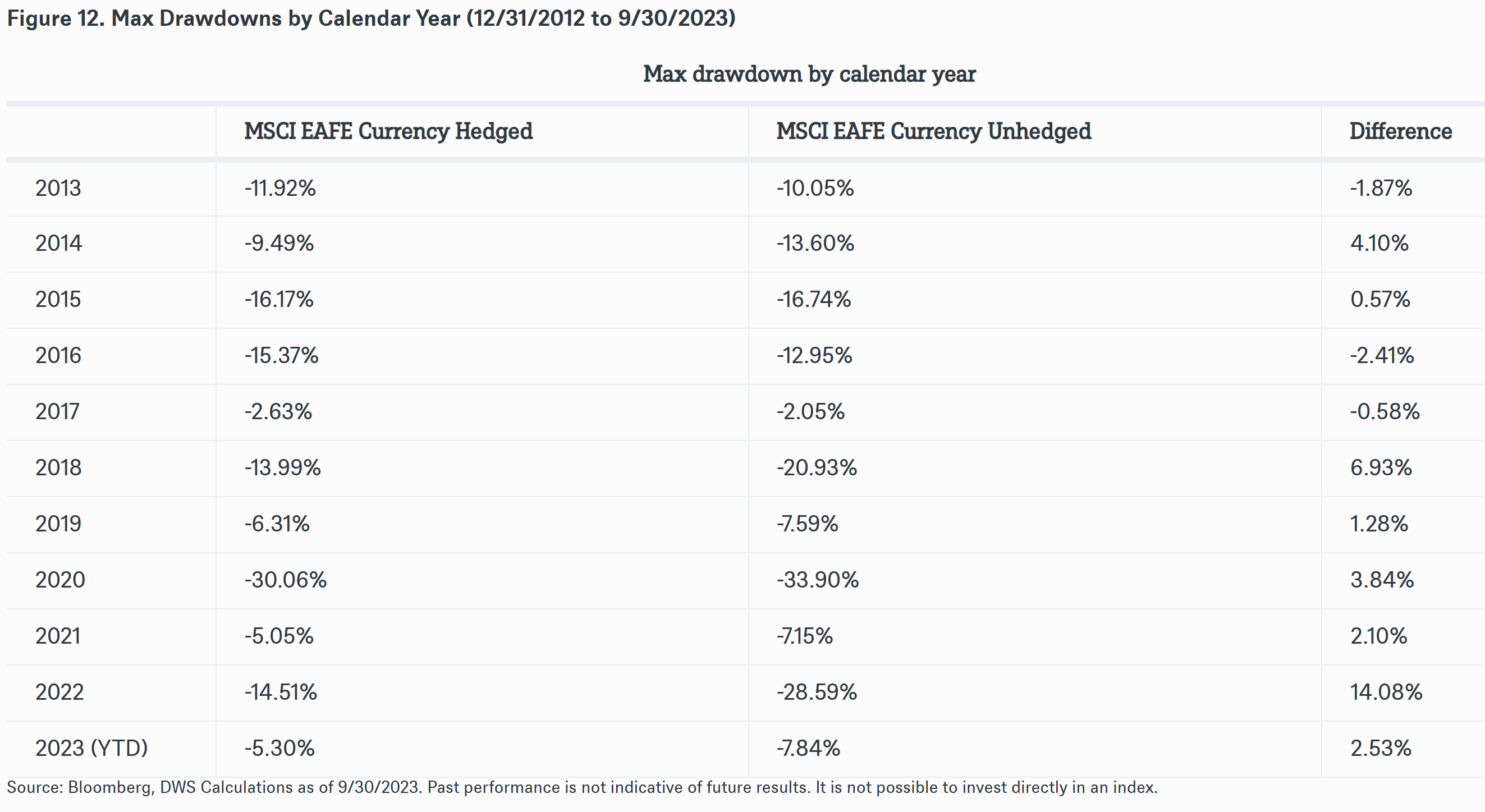

"Over the past decade, currency hedging EAFE equity exposure added tremendous benefit to investors through both increased realized returns (excess return over MSCI EAFE Currency Unhedged of 4.3% per annum) and reduction of realized annualized volatility by about 2.5%. Looking forward, On the return side of the equation, predicting the direction of currency markets has proven historically challenging, although currency carry continues to favor currency hedging for the foreseeable future. Alternatively, the risk argument for currency hedging is structural in nature and has not historically been beholden to changing market conditions. The calculus of owning an implicitly levered portfolio of equity and currency risk results in higher levels of volatility, and by extension, more severe market drawdowns, for EAFE investors who choose not to hedge their currency risk.

Concluding Thoughts

So, investors should hedge their currency, right? The answer is... it depends. As there is no quantitative advantage over the long run, it is really about volatility and whether this will change your behavior as an investor. If a wild fluctuation in your international investments (see below) may make you bail on the allocation in favor of a US only portfolio, then yes, hedging currency may result in lower volatility and likely similar returns to the unhedged investor.

{kind=link}

{kind=link}

The goal is to get exposure to foreign equities, not necessarily partake in the significant volatility of their home currency. Ultimately, whatever you choose the key is to stick with your approach through thick and thin. Much of this decision will be made based on your specific situation, capacity for risk, and desire to take on exposure to foreign currencies.

I believe taking an evidence-based approach is best when it comes to investing. Therefore, we know from Rex Sinquefield that most of the returns from international stocks come from value and small cap stocks. Therefore, an investor who holds a balanced approach of hedged and unhedged products is likely to increase their long-term returns and lower their overall volatility.

From the period 1995-2023 (28 years) a comparison of the Global Ex-US Index vs the International Value and Small Cap Indexes equal weighted showed that the value and small cap approach handily beat the Global Ex-US Index and did so without increasing volatility, yet also produced a higher Sharpe ratio.

Portfolio Visualizer/Authors Calculations

{kind=link}

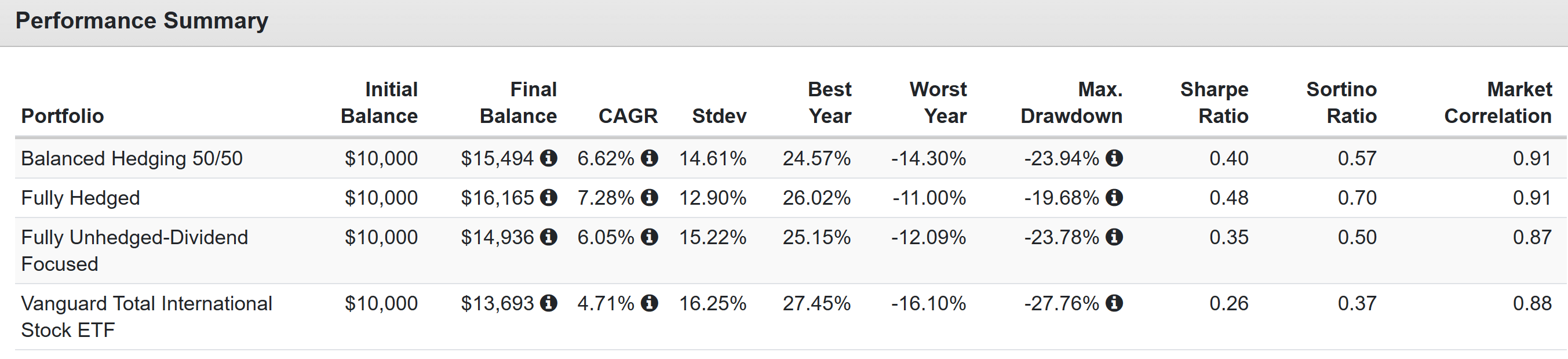

Combining this with a currency hedged core and looking at the limited data available (2017-2023) shows a clear advantage vs the Vanguard Total international stock index ( VXUS ).

Portfolio Visualizer/Authors Calculations

{kind=link}

Also included in this analysis is a portfolio of international dividend stocks. This is another approach many may use to reduce their volatility. Still, the currency hedged approach produced the best return, lowest volatility, and highest Sharpe ratio. Over time however, we would expect this to move up and down. This is why a more sensible approach is to follow the evidence and include exposure to international small cap and value stocks in an unhedged manner. Holding the balanced hedging portfolio allows an investor to enhance their total returns over the long run, while also lowering their volatility in the short run, which is likely to reduce investment behavioral errors.

For further details see:

Currency Impact In International Investing: A Guide For U.S. Investors