EADSF - Curtiss-Wright: A Buy And Hold On End Market Growth

2023-11-03 17:20:31 ET

Summary

- Curtiss-Wright has exposure to aerospace, defense, and industrial markets which are enjoying some tailwinds.

- The company saw double-digit growth in sales and operating profits in the second quarter, driven by strong performance in the defense and commercial aerospace markets.

- Curtiss-Wright has revised its financial guidance for 2023, expecting 8%-10% growth and higher operating margins, but dividend growth rates are falling short of sector medians.

In a report I published in June, I marked Curtiss-Wright Corporation (CW) stock a hold , and in September I re-ran the analysis with the most recent numbers and the stock remained a hold, in my view. The stock, however, has shown favorable returns appreciating 18% on a flat market showing the ability of the aerospace company to show strong outperforming returns even when the market is going nowhere. In this report, I revisit the company and analyze the latest results, guidance update and its valuation.

Curtiss-Wright Corporation Serves Different End Markets With Growth Prospects

{kind=link}

Curtiss-Wright

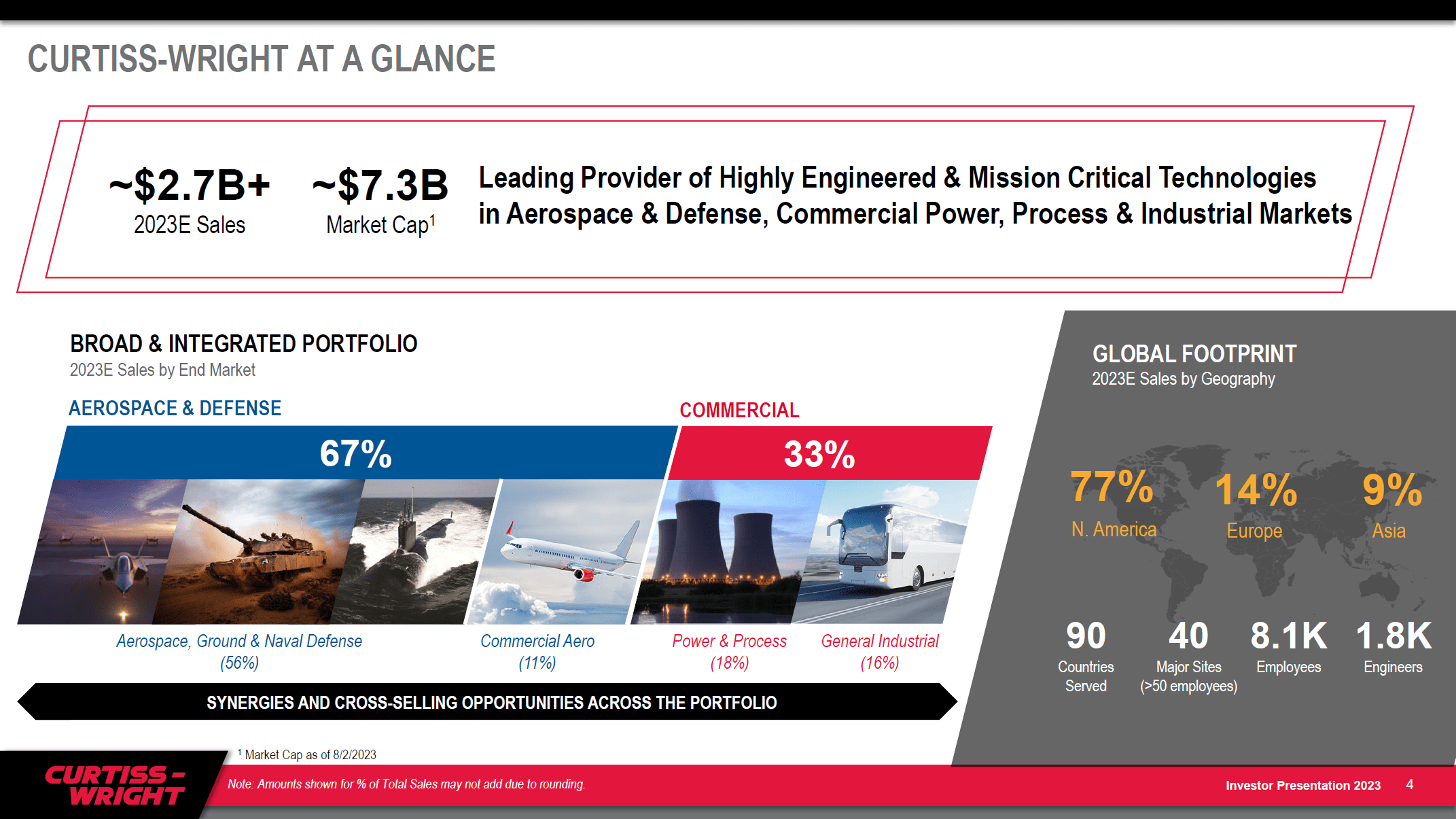

Curtiss-Wright Corporation serves three main end markets, namely aerospace, defense and commercial. The commercial segment contributed a third of the revenues consisting of 18% Power & Process revenues and 16% from General Industries. Currently Power & Process results are a somewhat pressured due to the winddown of the CAP1000 program for which the company delivered coolant pumps for AP1000 nuclear plants in China.

The Aerospace and Defense segment contributes 67% to the revenues and is mostly focused on defense which provides 56% of the revenues with product destined for air, ground and sea. The commercial aerospace segment contributes around 11% of the commercial aerospace sales. Aerospace & Defense is seeing significant growth potential ahead as defense budgets are expanding with positive effect on sales expected for years to come while commercial aerospace revenues also enjoy upward pressure as many commercial airplane programs will see increases in production rates at least into mid-decade to late-decade. Currently, Curtiss-Wright Corporation is not so much a plan on commercial aerospace as that actually is the smallest contributor to revenues, but I do like the upside that the aerospace & defense market offers overall.

Curtiss-Wright Financials Show Strong Organic Growth

{kind=link}

Curtiss-Wright

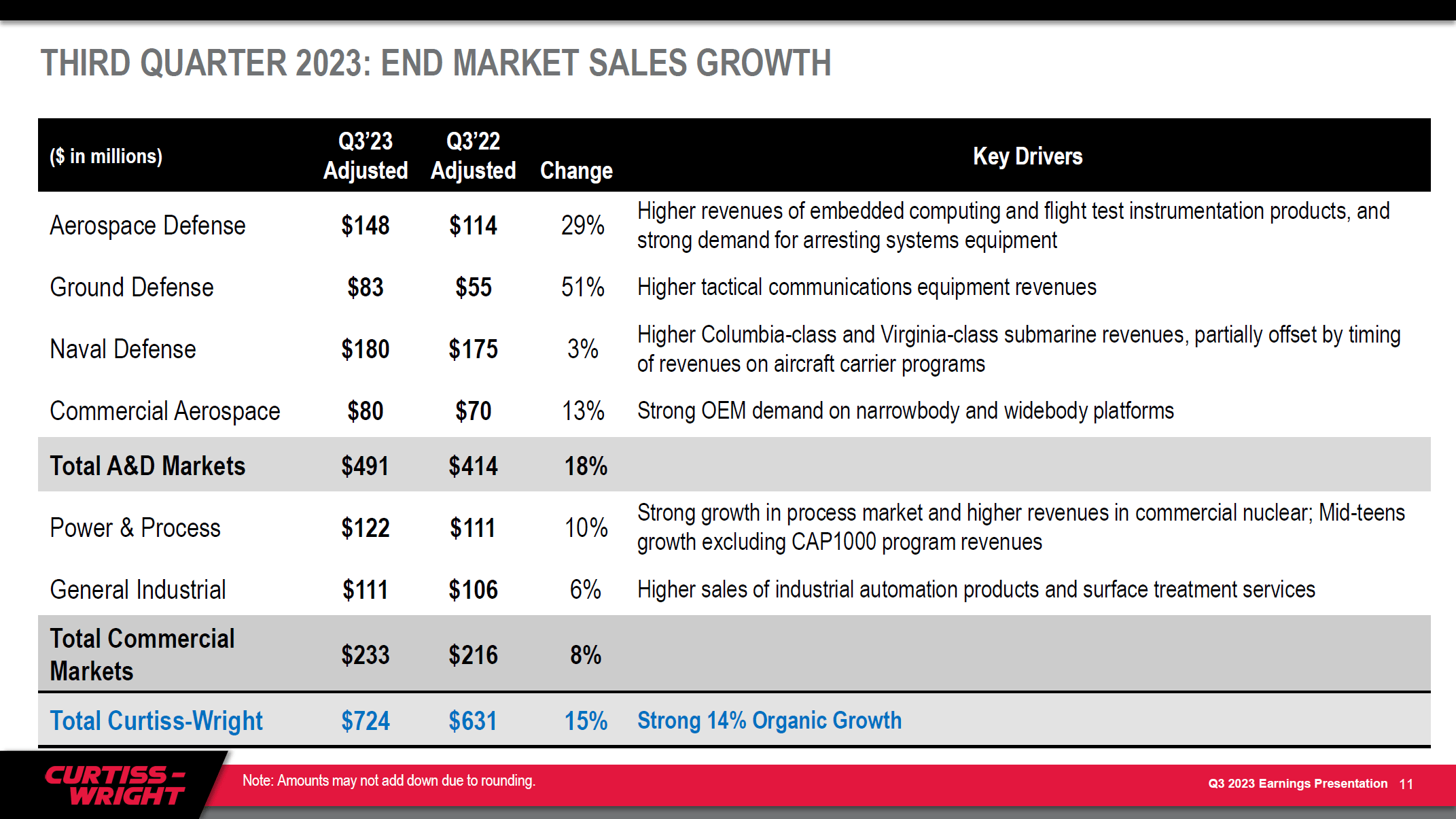

The results for Curtiss-Wright are somewhat challenging to analyze as sales are presented by end market, but results are not. Aerospace Defense, Commercial Aerospace and General Industrial sales with a part of the sales assigned to Defense Electronics while Power & Process revenues are combined with Naval Defense in the Naval & Power segment. I wouldn’t say it's not logical to combine, but reporting both the revenues as well as the profits by end market would have provided better insights on end-market demand and performance.

Aerospace defense revenues were up 29% and as seen in prior quarters that was driven by demand for flight test instrumentation and arresting systems which seems to have been a valuable addition for the company acquiring it from Safran ( SAFRF ) in July 2022. Ground Defense saw its revenues increase by 51%. This was driven by easing supply chain issues as well as strong demand for tactical communication equipment which saw $15 million to $20 million in accelerated sales. So, looking at the increase of $28 million in revenues year-over-year around 60% was driven by sales acceleration from inventory and the remaining was driven by easing supply chain issues.

Naval Defense sales were up 3% year-over-year and flat sequentially driven by higher submarine sales which provides some confidence that the supply chain for submarines is slowly rebuilding capacity, but this was offset by timing of sales on aircraft carrier revenues which provided some negative offset in the previous quarter as well.

Commercial aerospace sales were up 13% benefiting from continued strength in aftermarket sales which account for 15% of the sales and OEM build rate increases which account for 85% of the sales with a healthy split between narrow body and wide body programs.

The aerospace and defense segment saw 18% growth which can be attributed primarily to easing supply chain issues and sales acceleration in Ground Defense and demand strength for embedded computing, arresting systems and flight test hardware in Aerospace Defense.

Power & Processes revenues were up 10% driven by commercial nuclear revenues partially offset by winddown in sales for the CAP1000 program. As Poland and more recently Bulgaria announced approval for construction of four and potentially eight AP1000 reactors, Curtiss-Wright also has opportunities to sell and deliver reactor coolant pumps in the coming two to four years. General Industries sales were up 6% driven by industrial automation revenues as well as surface treatment services bringing commercial market revenue growth to 8%.

Total sales were up 15% to $724 million and primarily consisted of organic growth with only 1% growth being provided by inorganic growth. So, there's a lot of sales growth generated by the existing business and end-market strength suggests that we will see that continuing in the coming years.

Operating Income Growth Outpaces Sales Growth

{kind=link}

Curtiss-Wright

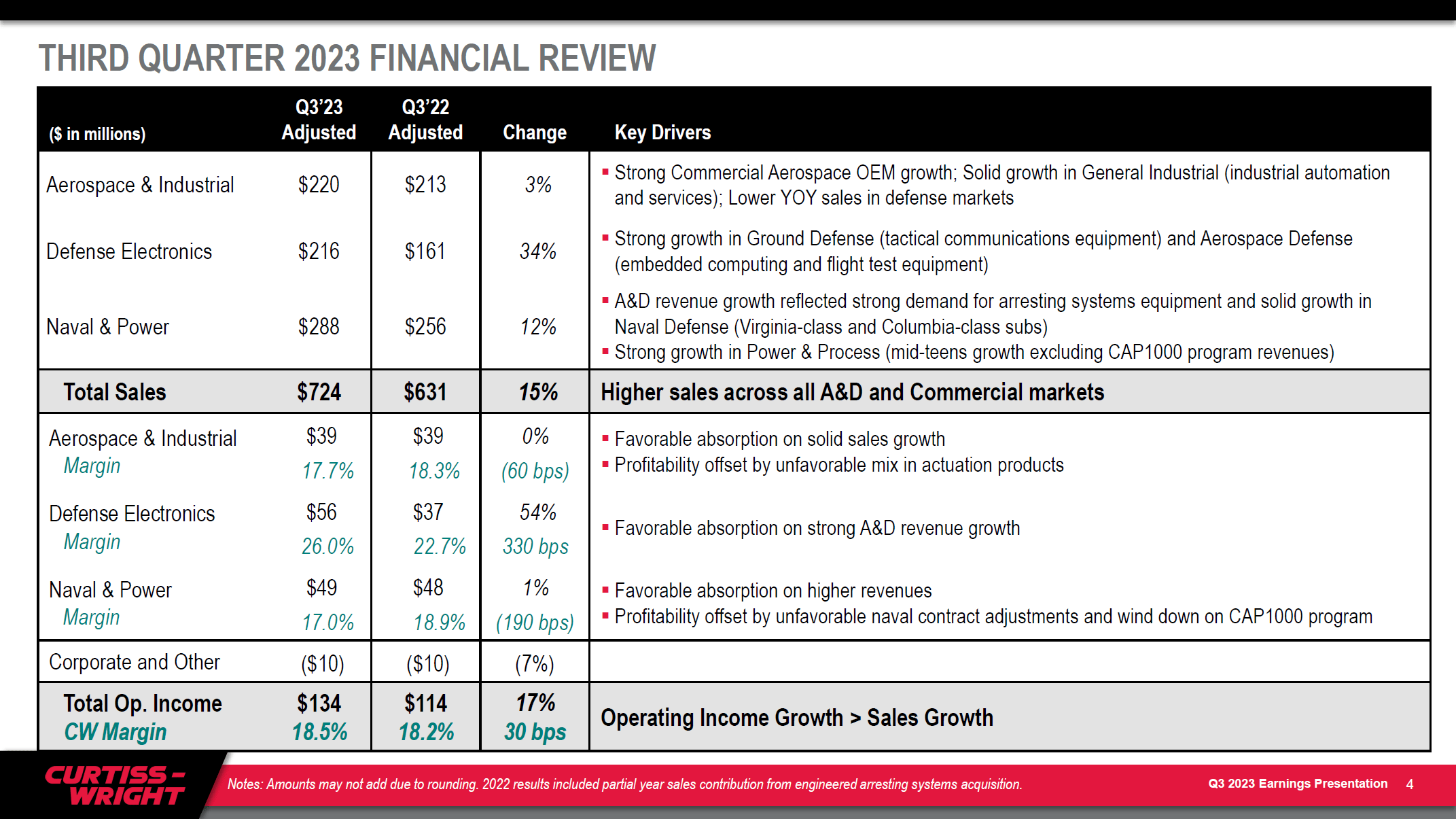

The tricky part is to look at how end-market sales translated to earnings level, since the reporting structure used is different as I mentioned. Aerospace and Industrial sales grew 3% indicating that much of the growth in commercial aerospace and industrial was offset by lower Aerospace Defense sales and some of the Aerospace end-market revenues being part of the Defense Electronics reporting segment. Operating income in the segment remained stable pointing at margin erosion due to unfavorable mix for actuator sales and lower defense sales.

Defense Electronics had a very good quarter with 34% sales growth driven by the acceleration in tactical communications equipment, easing supply chain issues and the part of sales that we are missing in Aerospace & Industrial possibly also drove some growth in Defense Electronics translating to 54% growth in operating income.

Naval and Power revenues were up 12 % , but it barely translated to the bottom line due to negative catch-up adjustments for the Naval Defense business and the winddown of the CAP1000 program.

Putting it all together, Curtiss-Wright saw sales growth of 15% with 1% being inorganic and 17% income growth to $134 million with the growth almost exclusively being driven by performance in Defense Electronics.

Curtiss-Wright Corporation Increases 2023 Guidance Again

{kind=link}

Curtiss-Wright

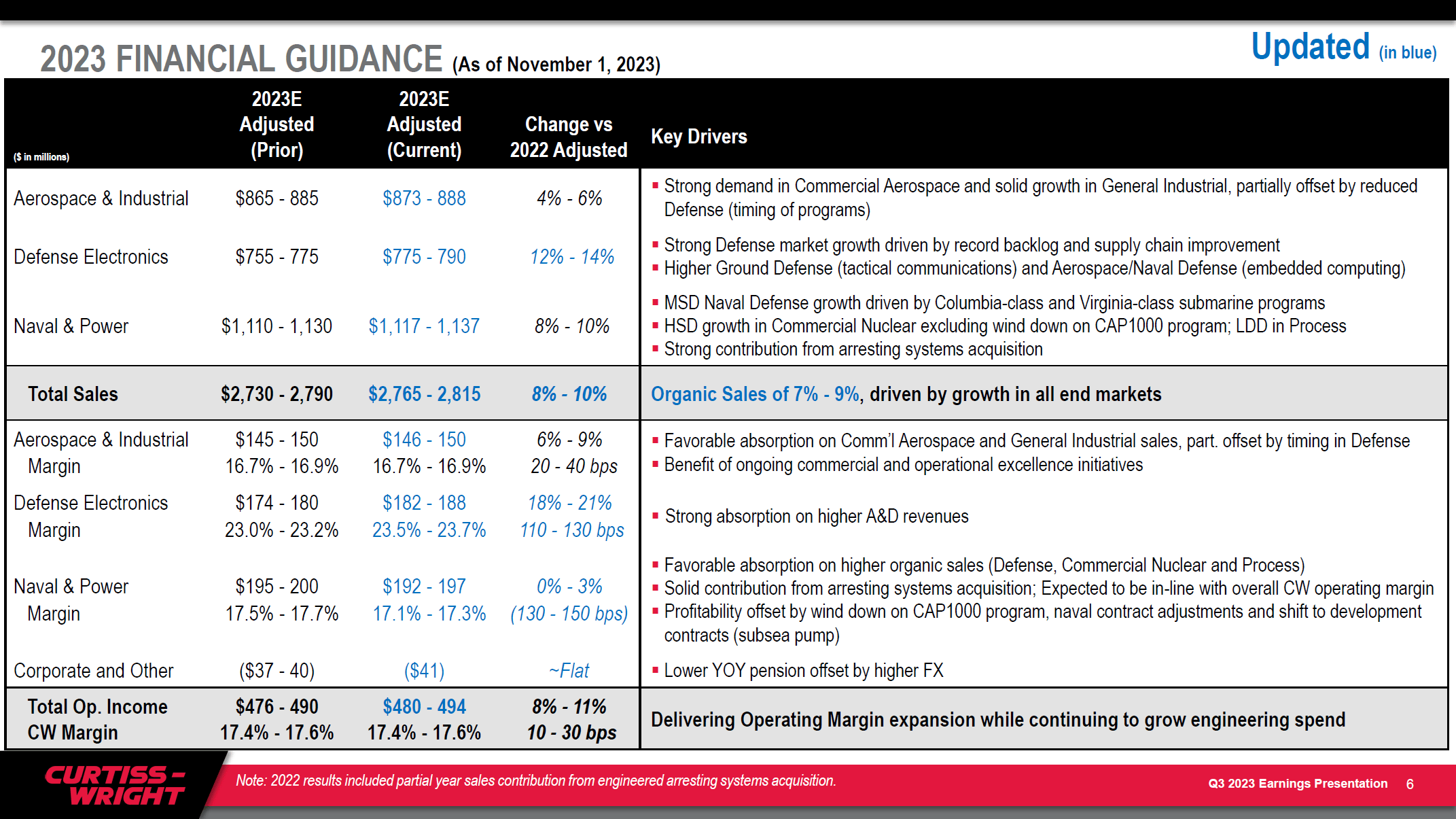

Just like during the prior quarter, Curtiss Wright Corporation has updated its guidance again. The company increased the lower end of its guidance for Aerospace & Defense sales by $8 million while it increased the upper bound by $3 million on 4% to 6% sales increase year-over-year being unchanged so this seems to be more of an update narrowing the sales guidance range to be in the upper half of the 4% to 6% range.

Defense Electronics saw it sales guidance boosted by $20 million and year-over-year sales growth now being in the 12% to 14% range compared 9% to 12% guided for previously. This guidance change seems to be incorporating the accelerated sales seen in the third quarter.

On income level, expected operating income has been increased by $4 million to $480 million at the lower end and $494 million at the higher end and I would say the increase there is less impressive than the boost in sales.

What we see is that aerospace and industrial saw the lower bound of the range being increased by $1 million which is not a huge change. Defense Electronics saw an $8 million boost to the operating income guidance while Naval and Power saw the guidance being lowered by $3 million and Corporate and Other expenses and eliminations are expected to be $4 million higher.

So, the guidance increase is a welcome one, but I would say it mostly reflects strength in Defense Electronics as seen in the quarter offset by corporate costs and eliminations and lower expectations for Naval and Power.

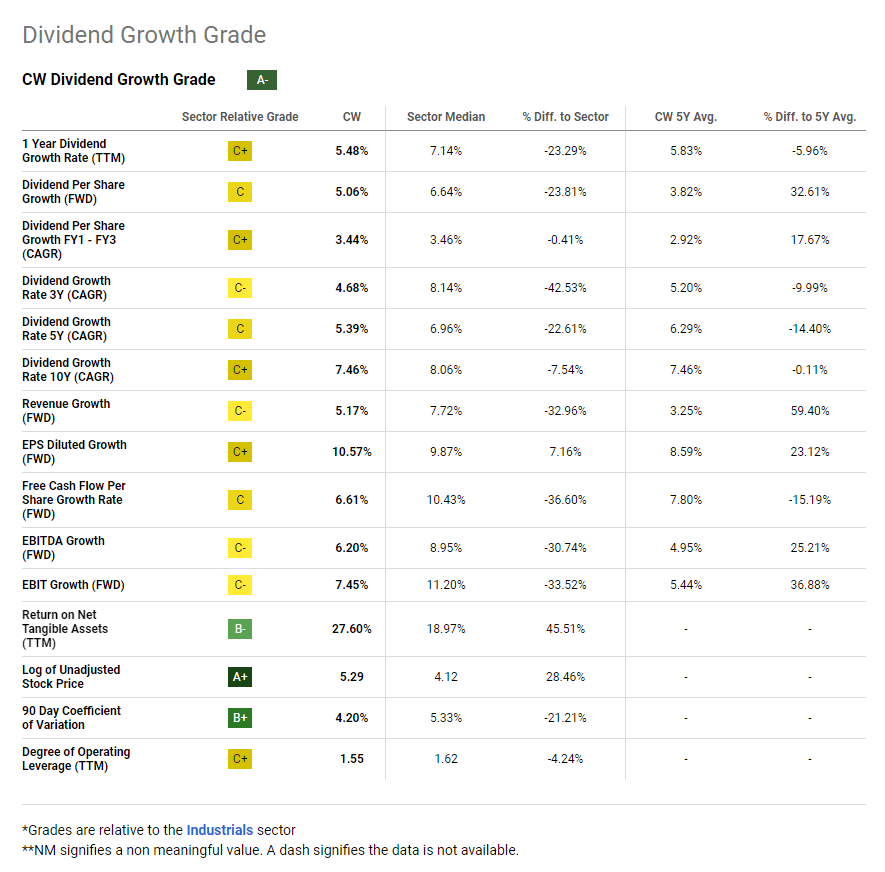

Curtiss-Wright Corporation: Not Attractive For Its Dividend

{kind=link}

Curtiss-Wright

Seeking Alpha Quant has provided Curtiss-Wright Corporation with an A- rating which seems good but the reality is that its dividend growth rates are falling short of the sector medians and its 0.4% dividend yield is not quite an impressive one. So, this is a name you would want to invest in for upside in the price target and not so much for the dividend. That’s just a nice to have with eye on dividend increases in the future.

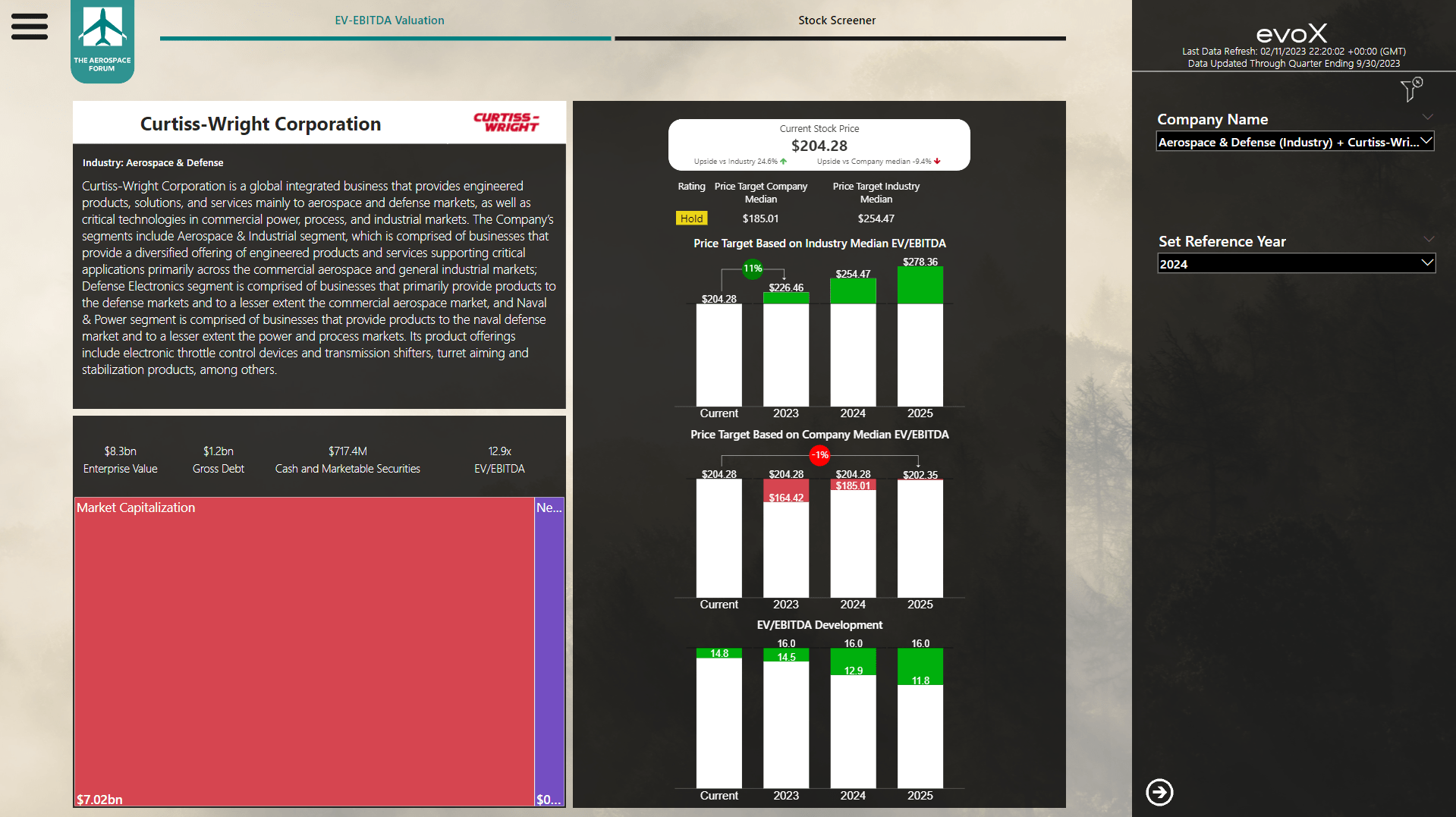

Curtiss-Wright Stock Price Valuation

{kind=link}

Curtiss-Wright

In my book, Curtiss-Wright Corporation is a hold, but I could see why some consider it a buy as well. Measured against the median EV/EBITDA, balance sheet data and forward projections on earnings suggest the company is fairly valued with 2025 earnings in mind. However, if we were to assume that it is justified for the stock to trade in line with its peers, which is not at all an unreasonable assumption, there's around 11% upside based on 2023 earnings and roughly the same year-over-year upside in the years after. Dividends, although minor, layer on top of that. So, given the stable relative year-over-year upside I could also see why this is a name that you would buy and hold.

Further Considerations That Could Warrant A Buy

My stock screener provides a Hold rating on Curtiss-Wright Corporation stock, so we could be done with it and say it is a hold and not a buy but that's not the case as I can perfectly understand why someone would be charmed by this name. It's not a stock with explosive growth ahead but that is also not needed. Moreover, the end markets served by Curtiss-Wright Corporation do have significant appeal as discussed below.

Defense

{kind=link}

The defense market has been seeing supply chain issues which affected the submarine supply chain as well as the Defense electronics chain, but those headwinds are dissolving while end-market demand is increasing on the back of higher defense budgets globally. So, we do see ability to supply improve and increasing demand which unlocks further growth in the years ahead.

Commercial Airplanes

Boeing

Commercial airplanes are high in demand with the pandemic being a two-year exception. Overall, the trend is up and OEMs are significantly below targeted, required and historical production rates meaning that there's significant growth potential ahead absent of any shock events. On a growing global fleet of commercial airplanes, Curtiss-Wright Corporation also could see more revenues derived from aftermarket sales. So, while Commercial Aerospace is the smallest end-market currently there are higher growth opportunities.

Power

{kind=link}

The war in Ukraine has had significant impact on energy prices as cheap Russian gas is a no-go while many countries are also targeting lower emissions. With that in mind more countries are considering building new nuclear plants. How much Curtiss-Wright can benefit from this depends on what type of reactor is selected. The company supports new build reactors of the type AP1000 and SMR. Poland, Bulgaria and Ukraine are planning on building AP1000 type reactors and the desire to build new nuclear reactor plants is not just limited to Eastern Europe but also in The Netherlands, where I currently am, there are plans to build a new reactor although the preference is the EPR reactor type.

Conclusion: Curtiss-Wright Stock Is A Buy And Hold

The results of Curtiss-Wright Corporation are good. Defense Electronics is seeing some easing of supply chain issues, but Naval and Power is facing some naval contract adjustments while CAP1000 program winddown also is providing some pressure on the comp. I can appreciate that the company has become more positive on its 2023 financials and has no debt maturing until 2025. So, I could see reason for investors to buy the name expecting stable returns based on the industry median upsides projected in the years ahead as well as the tailwinds in the end markets. So, while the stock screener rates Curtiss-Wright Corporation a hold I believe there are even more compelling arguments for a buy and hold.

For further details see:

Curtiss-Wright: A Buy And Hold On End Market Growth