CWK - Cushman & Wakefield: Risky But Cheap Best Commercial Real Estate Advisor

2023-04-19 08:31:00 ET

Summary

- Cushman's current goal is to meet the needs of its clients through a broad service offering that includes property, home, and asset management and administration, and renting.

- The company anticipates $90 million in-year cost savings thanks to permanent and temporary actions. Besides, management believes that the company will likely experience sequential improvement in brokerage trends through 2023.

- I believe that further increase of sales or marketing channels thanks to new contracted agents or independent distributors will likely improve sales growth and FCF margins.

- According to Euromoney, Cushman is the world’s best commercial real estate advisor and consultant.

Cushman & Wakefield plc ( CWK ), one of the leaders in commercial services for the real estate industry, recently announced $90 million in-year cost savings in 2023. Guidance also included consistent growth at the end of the year, and market analysts are expecting stable FCF in 2023, 2024, and 2025. In my view, assuming further hiring of agents and sufficient investments in data analysts and technology, the company could be worth around $13.35 per share. Even taking into account potential risks from the total amount of debt or failed acquisitions, in my opinion, the stock is undervalued.

Cushman & Wakefield Runs International Operations Having A Diversified Customer Base

Cushman & Wakefield offers commercial services for the real estate industry in the United States and outside. The company currently operates in more than 60 countries, with 400 offices distributed throughout these countries and an employee plant estimated at 44,000 people, offering value opportunities for investors, homeowners, and tenants.

Cushman's current goal is to meet the needs of its clients through a broad service offering that includes property, home, and asset management and administration, renting, and recommendation as well as advice on the capital market and the appraisal of homes or real estate projects.

Results of operations are managed in three business segments that respond to the company's geographic activities: Americas, Europe and the Middle East, and Asia-Pacific markets. These represent 73%, 11%, and 13% of annual earnings respectively. The services in each segment are similar and the ways to carry them out as well. Among the list of services that the company offers, a large part of the profit is given by the management and administration of goods and assets, representing 48% of the company's profits, above the 29% generated by income.

Clients for this company range from single property owners looking to manage their real estate to large scale investors with multiple properties around the world. The multinational companies from various sectors see in Cushman's services the possibility of managing their assets as well as obtaining valuable properties for the development of their specific activities.

I believe that the company is worth having a look because of the guidance given by management. The company anticipates $90 million in-year cost savings thanks to permanent and temporary actions. Besides, management believes that the company will likely experience sequential improvement in brokerage trends through 2023.

Source: Investor Presentation

Market Expectations Include Stable FCF And Net Sales Growth In 2024 And 2025

In my view, it is also worth noting that financial analysts out there are quite optimistic about the future of Cushman & Wakefield. Market estimates include 2025 net sales of $10.731 billion, net sales growth close to 5.10%, an EBITDA of $950 million, and an EBITDA margin of around 8.9%. Additionally, the 2025 net income would stand at $238 million with 2025 EPS of $1.36 and FCF close to $402 million.

Market analysts believe that from 2023 to 2025, the free cash flow would stand at close to $338-$422 million. I believe that the FCF is sufficiently stable to run a DCF model.

Source: Marketscreener.com

Balance Sheet: The Total Amount Of Debt Appears Quite Under Control

In 2022, I did not see many changes in the balance sheet. The total amount of assets increased driven by an increase of non-current assets, but goodwill and intangible assets decreased. The total amount of liabilities decreased a bit thanks to decreases in long-term debt, accrued compensation, and other non-current liabilities. I believe that the balance sheet remains solid, but investors may want to study the long term debt.

In the last annual report, the company reported a significant amount of cash worth $644 million, which the company could use for acquiring other competitors. Trade and other receivables stood at $1.462 billion with income tax receivable of around $55 million and short-term contract assets worth $358 million. In sum, total current assets were equal to $2.766 billion, more than 1x the total amount of liabilities.

Property and equipment were worth $172 million with goodwill of $2065 million, intangible assets of $874 million, equity method investments of $677 million, deferred tax assets of $58 million, and total assets of $7.949 billion.

Source: Annual Report

Liabilities included short-term borrowings and current portion of long-term debt of $49 million, accounts payable and accrued expenses of around $1.199 billion, and accrued compensation of $916 million. Besides, with income tax payable of $33 million and other current liabilities of $192 million, total current liabilities were equal to $2.390 billion.

Long-term debt stood at $3.211 billion with deferred tax liabilities of around $57 million, non-current operating lease liabilities of close to $334 million, and total liabilities of $6287 million. The asset/liability ratio was equal to around 1x.

Source: Annual Report

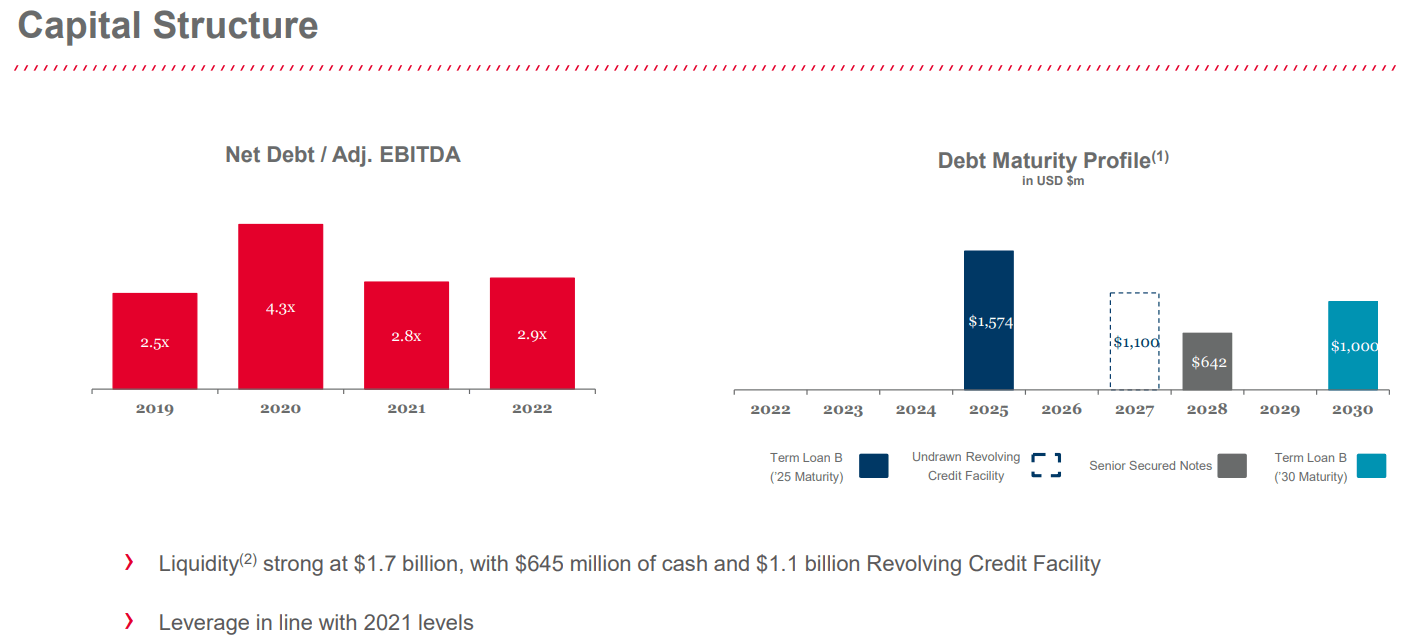

In the Q4 2022 report, the net debt/ adjusted EBITDA was said to be close to 2.9x, which appears pretty much under control. However, I would understand that certain investors feel a bit uncomfortable with the total amount of debt. The company will have to pay $1.574 billion in 2025, so I believe that Cushman & Wakefield will be able to find new debt investors, or negotiate the current debt terms.

{kind=link}

Fragmented Market, But Cushman & Wakefield Is One Of The Leaders

Competition in the real estate market is high, and the market is fragmented. Competition conditions depend on the region and the type of market. Cushman is one of the top three companies in the international real estate market for both profit rates and workforce recruitment.

Today, Cushman & Wakefield is one of the top three real estate services providers as measured by revenue and workforce. We have gained third-party recognition as a provider and employer of choice, having consistently been named in the top three in our industry’s leading brand study, the Lipsey Company’s Top 25 Commercial Real Estate Brands, and the world’s best commercial real estate advisor and consultant by Euromoney. Source: Annual Report

If we talk about other multinational companies, we must name Jones Lang LaSalle Incorporated ( JLL ), CBRE Group, Inc. ( CBRE ), and Colliers International Group Inc. ( CIGI ). In many cases, small local entrepreneurs with knowledge and contacts in the region could also be competitors. We can also consider some banking firms or brokers as well as real estate services via the Internet as competition factors.

Further Hiring Of Agents, Economies Of Scale, And Data Analysis Could Imply A Valuation Of $13.35 Per Share

Considering the guidance given for 2023, I am optimistic about Cushman & Wakefield expanding the range of existing services to provide better conditions and comforts to its customers. As a result, I would expect higher profits from sale or rent besides expansion of its margins of activity through higher quality of services, further recruitment, hiring, and retention of great talent.

I also believe that further increase of sales or marketing channels thanks to new contracted agents or independent distributors will likely improve sales growth and FCF margins. In this regard, I believe that economies of scale will continue to play a major role in the FCF margin increase. If more agents use the software offered by Cushman & Wakefield and further network effects appear, the work of each agent will be, in my view, more valuable.

Finally, investing and developing more technologies to optimize the company's services besides improving the customer experience could bring further business growth. I believe that the use of information processing and data analysis through specialized software and artificial technology connected to the real estate industry could bring substantial revenue growth. In this regard, I believe that the following lines from a recent annual report are very relevant.

Our systems and processes are scalable enabling us to efficiently onboard new businesses and employees without the need for significant additional capital investment in new systems. In addition, our investments in technology have helped us attract and retain key employees, enable productivity improvements that contribute to margin expansion, and have strongly positioned us to expand the number and types of service offerings we deliver to our key global customers. We have made significant investments to streamline and integrate these systems, which are now part of a fully integrated platform supported by an efficient back-office. Source: Annual Report

My numbers from 2023 to 2033 include certain net income declines from 2024, D&A declines, increases in changes in deferred taxes, increases in income taxes accounts payable, and increases in accounts payable. I believe that my numbers are quite conservative, and they are not very different from what I have seen in the numbers reported for 2020, 2021, and 2022.

The financial figures for the year 2025 would include 2025 net income of $116 million, 2025 depreciation and amortization of $140.5 million, lease amortization of $100.5 million, changes in income taxes payable close to -$177.5 million, 2025 accounts payable and accrued expenses of $519.5 million, and a cash flow from operations worth $517.5 million. Besides, with a capex of -$74.5 million, I obtained 2025 FCF of $443.5 million.

My numbers for 2033 include net income of -$132.5 million, depreciation and amortization close to $175.5 million, and a CFO around $1854.5 million. If we also include capital expenditures of -$55.5 million, 2033 FCF would be $1.7995 billion.

Source: My DCF Model Source: My DCF Model Source: My DCF Model

My results include an enterprise value of $5.5995 billion, cash close to $644.5 million, long-term debt of $3.2115 billion, and an equity valuation of $3.0315 billion with a fair price of $13.35 per share.

Source: My DCF Model

Regulations And Legislation Risks, Or Risks From The Total Amount Of Debt

Cushman may suffer from risk factors in terms of regulations and legislation as well as local policies in relation to the real estate market. Besides, expansion, acquisition failure, or the inability to retain some of its key executives and employees could deteriorate future cash flow statements.

It is also worth noting that the real estate market is governed by changing cycles that go hand in hand with the state of the economy at the national and international level, and in many cases, it is unpredictable and generates a lack of short-term projection in terms of strategic decisions. This is a natural risk of these types of markets.

Lastly, Cushman reports a significant amount of debt, which, although it is not urgent, could eventually lead to complications for the company in terms of accessing credit lines or short-term liquidity operations. If the net debt/adjusted EBITDA ratio does not lower soon, I believe that certain investors would decide to sell their shares.

My Takeaway

Cushman & Wakefield is one of the leaders in the real estate market, and management expects to report $90 million in-year cost savings in 2023 and consistent growth. I believe that the international exposure to international markets and the diversified customer base will most likely protect the company from revenue volatility in case of a recession. In addition, I believe that sufficient increase in the number of contracted and independent agents as well as data analysts could bring future FCF generation. Even taking into account risks from the current level of debt, failed acquisitions, or expansion, I believe that the stock is undervalued.

For further details see:

Cushman & Wakefield: Risky But Cheap, Best Commercial Real Estate Advisor