EFSC - Customers Bancorp: Still Offers Some Upside

2024-01-22 07:59:54 ET

Summary

- Customers Bancorp stock has outperformed the S&P 500, generating a 49.1% gain for investors since my last article.

- Net interest income and net profits have improved for Customers Bancorp, showing progressive improvement for the company.

- The value of deposits has increased, while the value of loans and securities has slightly declined. The company's book value per share has also risen.

One of the best investment calls that I have made over the past several months has been Customers Bancorp ( CUBI ). In late August of last year, while looking for some cheap banking stocks to dig into, I stumbled across this particular firm. I discovered very quickly that the firm recovered rapidly from the banking crisis it began in March of 2023 and, as of the time of the writing of that article , the firm had even started trading at a premium to where it was before the crisis began. An overall growth in deposits paved the way for this appreciation. But even in spite of that, the stock was trading at really low multiples. This led me to rate the enterprise a 'buy' to reflect my view that the stock should outperform the broader market for the foreseeable future.

So far, that call has proven to be a successful one. While the S&P 500 is up 8.6% since the article was published, shares of Customers Bancorp have generated upside for investors totaling 49.1%. Deposits continue to grow at a nice clip and debt has recently declined. Shares are now trading at a premium to both book value and tangible book value, which does make the business look a bit less attractive. But relative to earnings, the stock is very affordable. So long as nothing majorly negative comes out of the woodwork, I would make the case that some additional upside is probably still on the table. And because of that, I am keeping the business rated a soft 'buy' for now.

Some mixed results

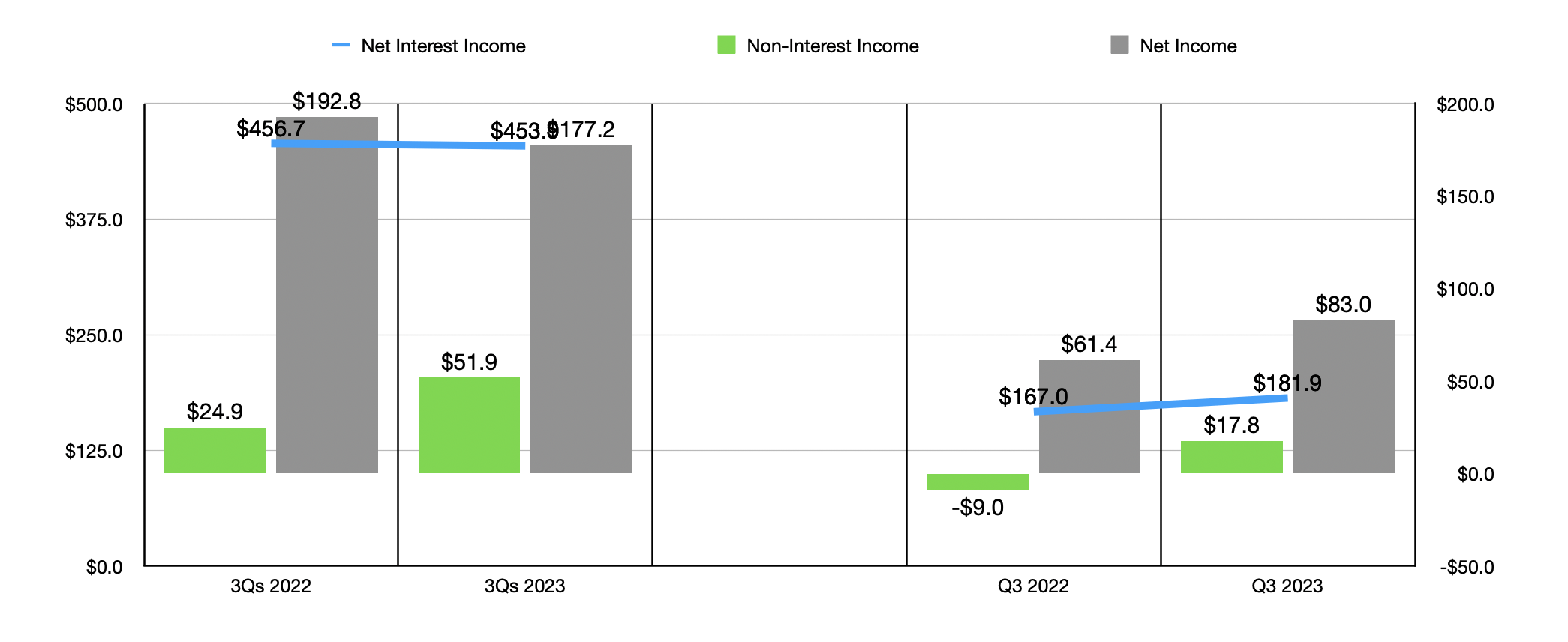

When I last wrote about Customers Bancorp in August of last year, we only had data covering through the second quarter of the 2023 fiscal year. Fast forward to today, and that data now covers through the third quarter . Because of this, our primary focus should be on that most recent data. Net interest income during that window of time came in quite strong, hitting $181.9 million. That represents an increase of 8.9% over the $167 million that the company reported the same time one year earlier.

{kind=link}

At a time when the net interest margin at many institutions is on the decline because of high interest rates and the impact those have on deposits, not to mention higher debt levels that many banks have had to resort to because of concerns over financial stability, Customers Bancorp is an exception. The net interest margin for the business as of the end of the third quarter of 2023 was 3.75%. That was an increase over the 3.18% reported the same time one year earlier. Even though the institution had to deal with higher interest rates on a variety of liabilities, most notably on interest bearing deposits that went from 1.82% to 4.29%, its growth on the asset side was far more robust. Under the specialty lending loans and leases category of its commercial and industrial loans, for instance, the firm has $5.72 billion recorded as the average balance throughout the third quarter of 2023. That's up from the $5.06 billion average balance one year earlier. That increase, combined with a rise in the average interest rate from 5.07% to 10.94%, played a major role in pushing the company's net interest margin up.

{kind=link}

Other areas of the company also improved. As an example, non-interest income went from a negative $9 million in the third quarter of 2022 to a positive $17.8 million in the third quarter of 2023. This, combined with the aforementioned rise in net interest income, pushed net profits up from $61.4 million to $83 million. It should be mentioned that the third quarter was a bit special for the company. I say this because, if you look at the first nine months of 2023 as a whole relative to the same time one year earlier, you actually would see that net interest income and net profits actually worsened year over year. This shows a progressive improvement for the company at a time that is challenging for many of its peers.

{kind=link}

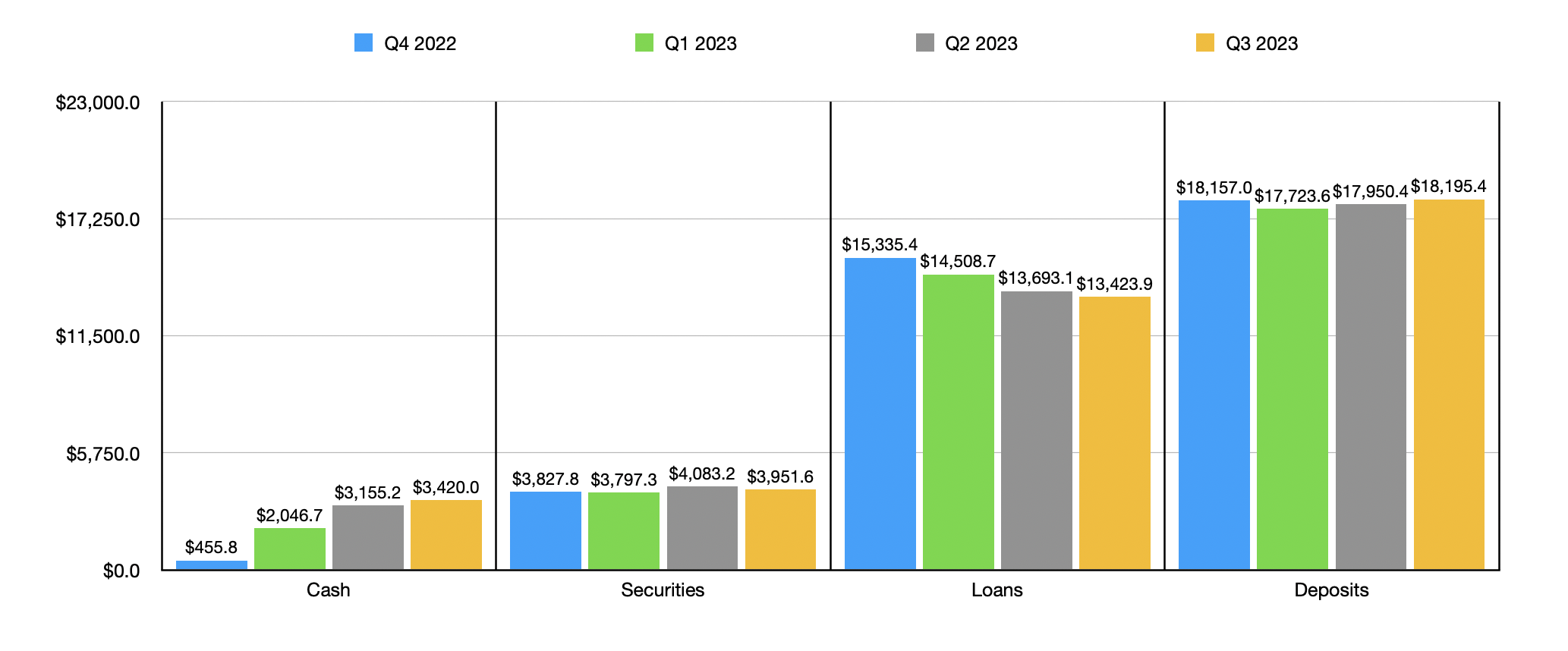

Outside of the income statement, there have been other areas where the institution has improved. For starters, the value of deposits at the bank hit $18.20 billion during the third quarter. Although this is only marginally higher than the $18.16 billion reported for the end of 2022, it's a nice increase over the $17.95 billion reported in the second quarter of last year. Although the company did see an increase in its uninsured deposit exposure from 24.5% in the second quarter to 25.8% in the third quarter, both of those readings are still below the 30% threshold I look at as a maximum that I'm usually comfortable with.

{kind=link}

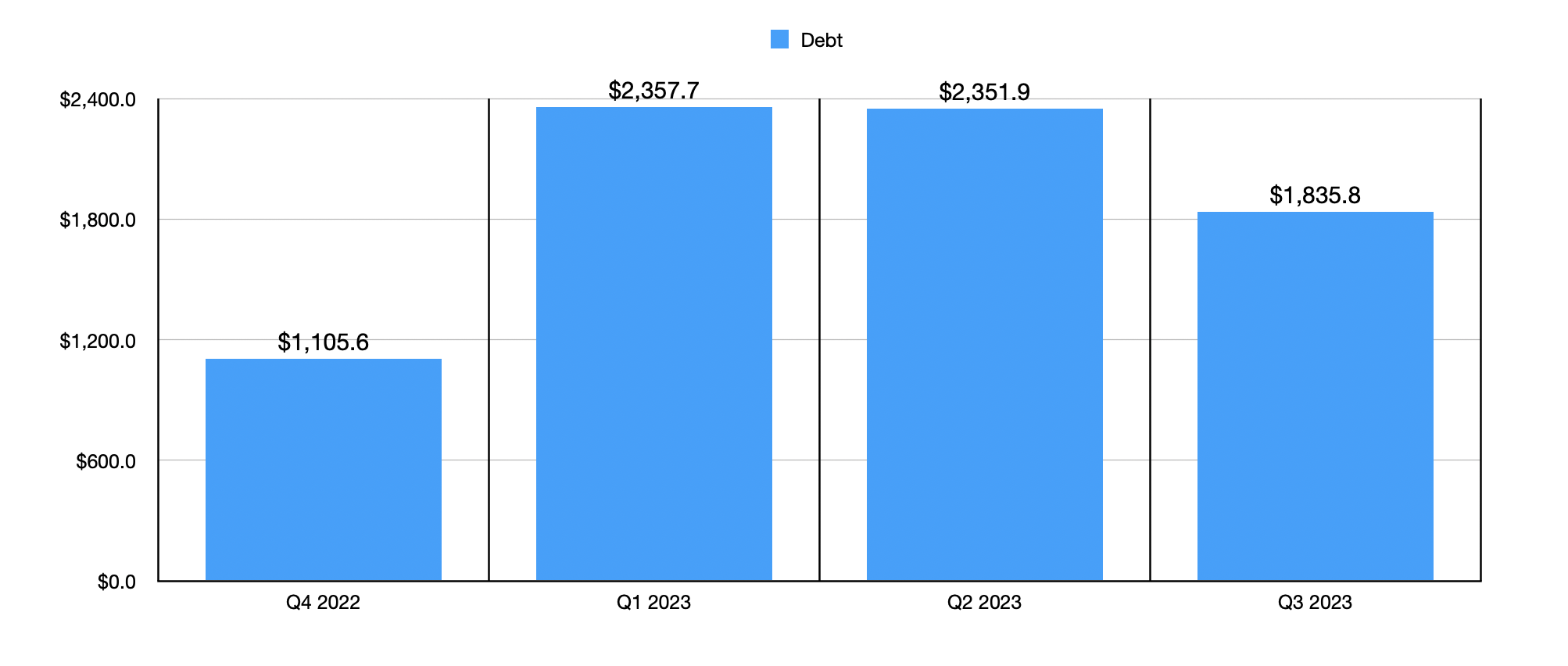

The value of loans has, unfortunately, done the opposite of grown. At the end of the second quarter, loans totaled $13.69 billion. By the end of the most recent quarter, they had dropped slightly to $13.42 billion. A similar decline in the value of securities from $4.08 billion to $3.95 billion also occurred. However, this seems reasonable when you consider that cash and cash equivalents increased from $3.16 billion to $3.42 billion, while debt on the company's books dropped from $2.35 billion to $1.84 billion. Frankly, I would have preferred the value of loans and/or securities to increase while cash decreased. But I am happy to see that at least the decreases went for not only bolstering cash, but also reducing leverage. The largest chunk of the company's borrowings carries an annual interest rate of 4.96%. So it's great to see that come off the books.

{kind=link}

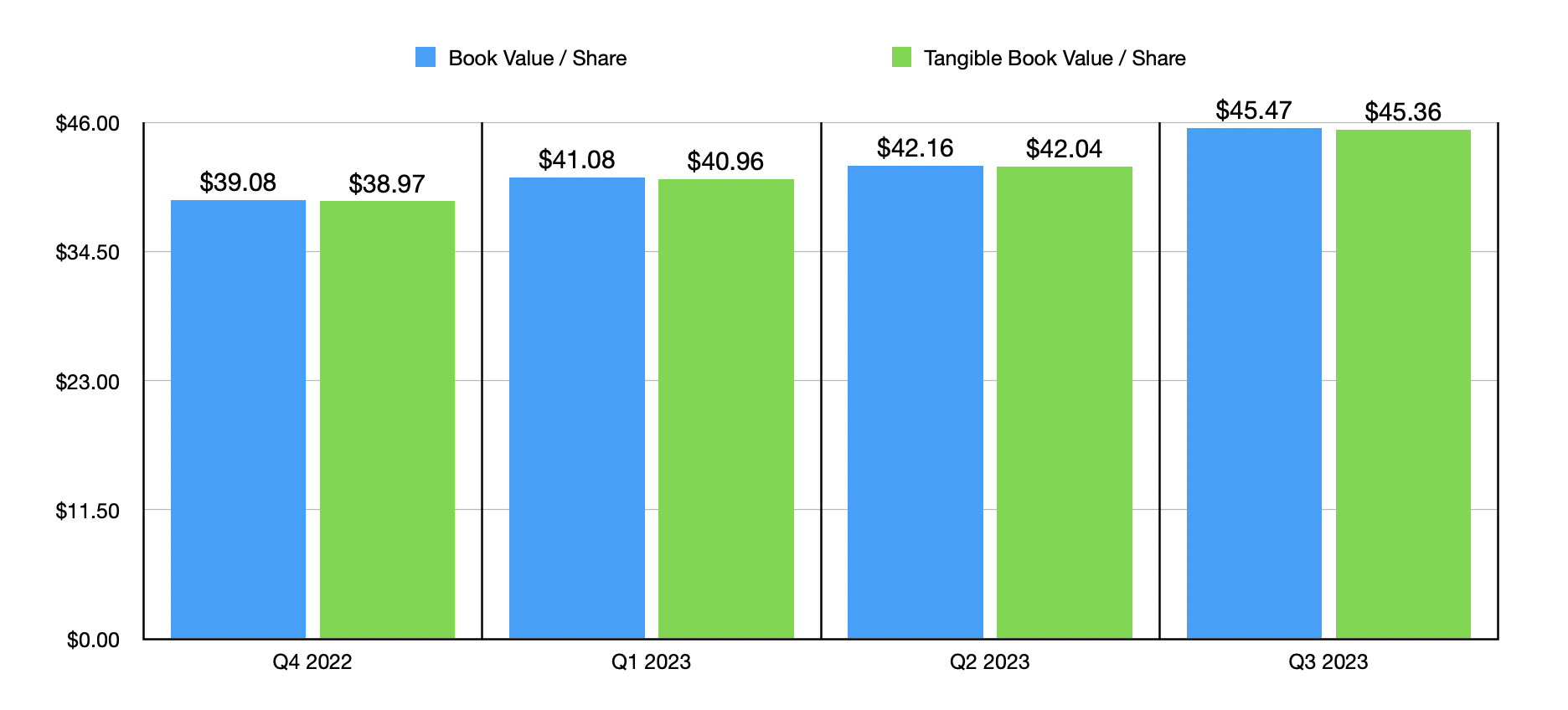

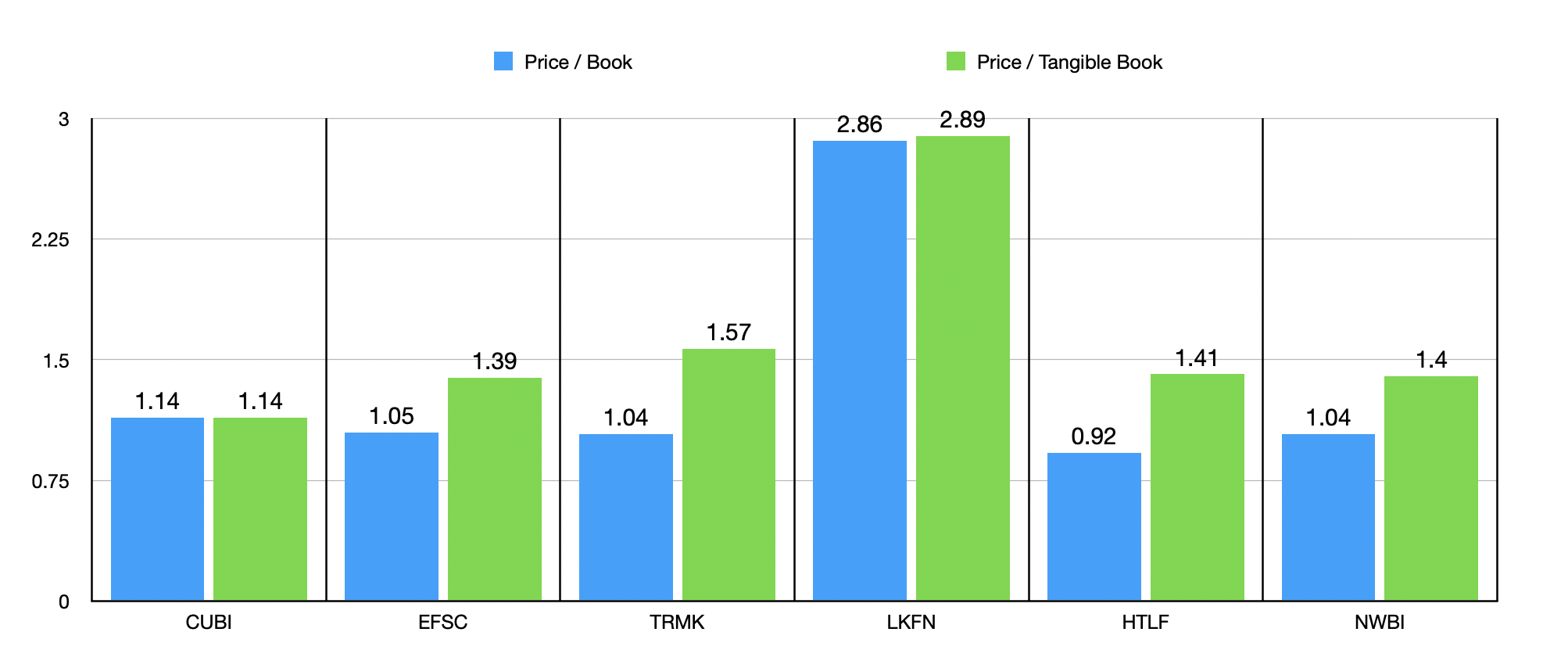

Another improvement that the company saw during this window of time was a rise in its book value per share. This managed to grow from $42.16 in the second quarter to $45.47 in the third quarter. A similar increase was seen when it came to the tangible book value from $42.04 to $45.36. With the increase in the company's share price, this resulted in a rise in its price to book multiple to 1.13, while the price to tangible book value multiple increased to 1.14. In the chart below, you can see how these figures stack up against some other firms. Although four of the five companies ended up being cheaper than Customers Bancorp on a price to book basis, it was the cheapest of the group when it came to the price to tangible book value multiple.

{kind=link}

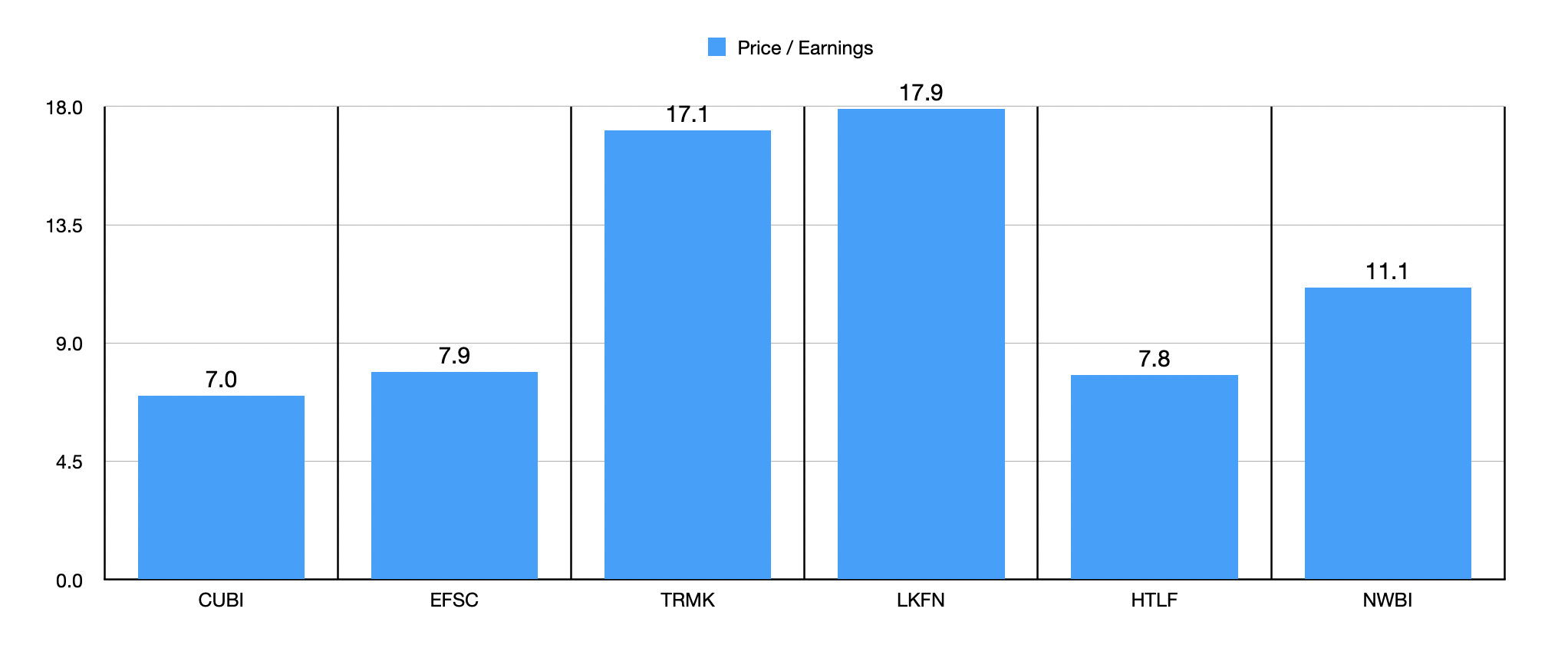

In the chart below, I also decided that look at the picture through the lens of the price to earnings multiple. This is one of the most important metrics in my opinion when it comes to looking at banks like this. Even after seeing shares rise so much, the companies trading at a price to earnings multiple of 7. This assumes, of course, that analysts are correct about the firm generating earnings per share of $1.69 for the final quarter of the 2023 fiscal year. This would represent a sizable increase over the $0.77 per share reported one year earlier. Speaking of forecasts, analysts believe that revenue should also grow, climbing from $142.5 million in the final quarter of 2022 to $172.6 million in the final quarter of 2023.

{kind=link}

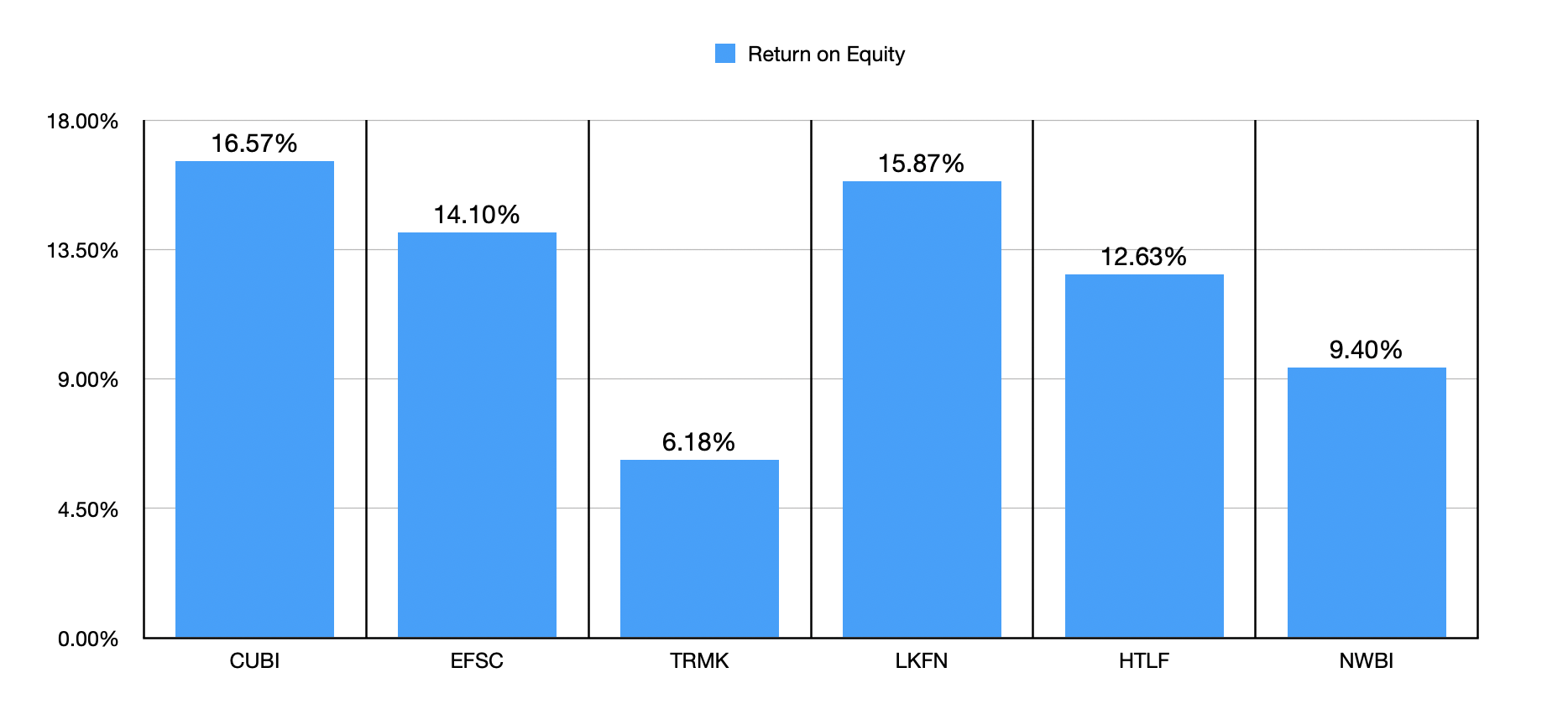

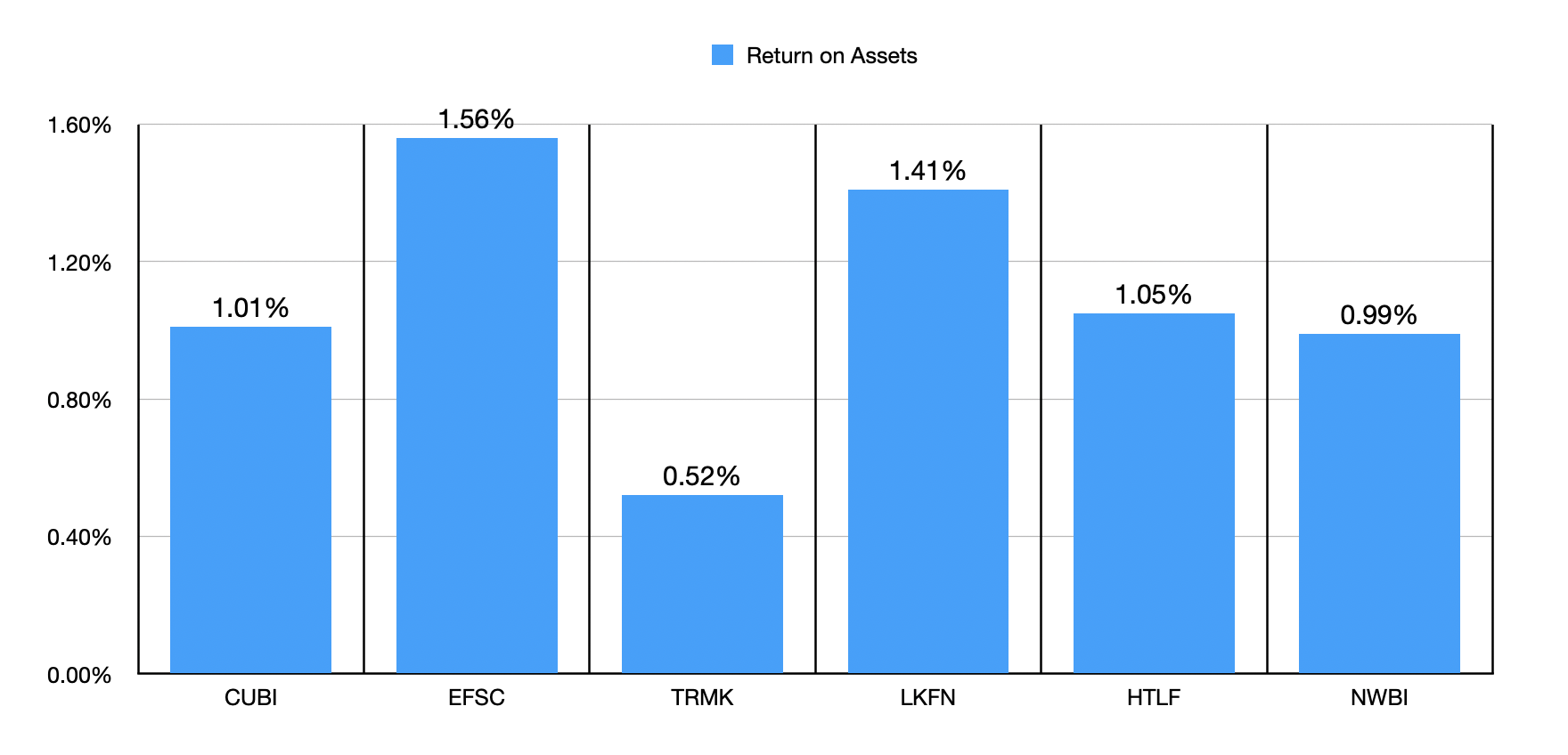

Relative to the five other companies that I compared Customers Bancorp to, only two ended up being cheaper. Now, before I finish things up, I would also like to look at two other metrics, both shown in the charts below. When it comes to return on equity, it's worth noting that Customers Bancorp is a true winner in the space. The 16.57% reading that it gets made it the best performer between it and the five companies I compared it to. Although when it comes to the return on assets, shown in the final chart of this article, it does drop some, with three of the five companies having a higher reading than it does.

{kind=link}

{kind=link}

Takeaway

Based on all the data provided, I must say that Customers Bancorp strikes me as a solid institution. It's not perfect, especially when it comes to some of the comparable data we have looked at and some of its performance earlier in 2023. But for the most part, the institution is holding up well and while the stock is not the cheapest anymore, it does still look attractively priced. Because of all of this, I do believe that a soft 'buy' rating still is appropriate at this time.

For further details see:

Customers Bancorp: Still Offers Some Upside