EPI - CVD Equipment Corporation's Recovery Looks Set To Continue

2023-07-24 07:34:59 ET

Summary

- CVD Equipment Corporation is strategically reorienting on secular growth markets and there are signs this is paying off with strong revenue growth and margin recovery.

- The company keeps introducing new systems and solutions with the upcoming Epi system for the SiC market, especially interesting.

- Revenue is lumpy quarter-to-quarter due to the timing of orders.

- CVV stock needs to scale up to put finances on a sustainable footing, but they're not far off and this looks eminently possible.

- The shares are not expensive, and the company isn't bleeding much cash.

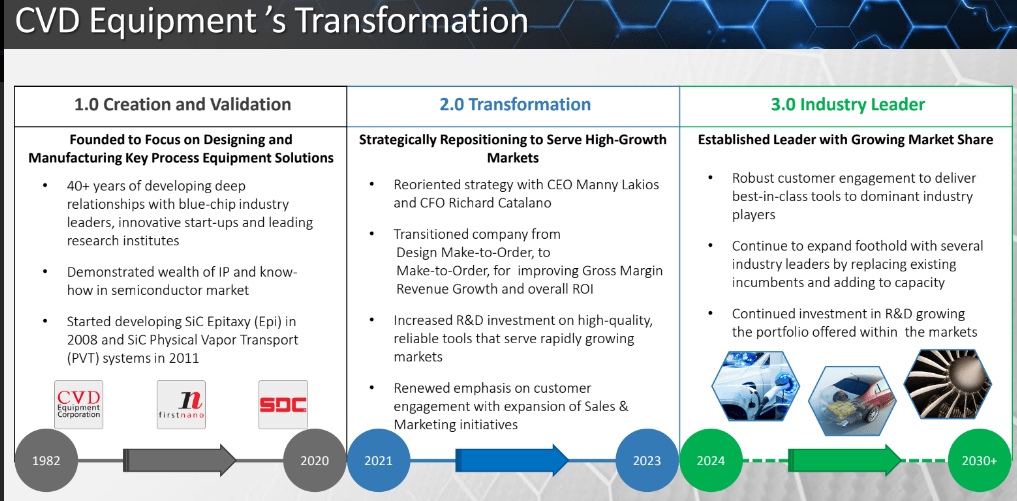

We wrote about CVD Equipment Corporation ( CVV ), a company not unlike Richardson ( RELL ) three years ago but since then the company has embarked on a transformation that is now well advanced, from the company's May 2023 IR presentation :

{kind=link}

The company is adding standard (but configurable) products to its bespoke solutions (their traditional strength) and is focusing on three segments that will be less cyclical and driven by secular tailwinds:

- The power electronics market

- The emerging battery materials market

- The legacy aerospace and defense market.

Power Electronics

{kind=link}

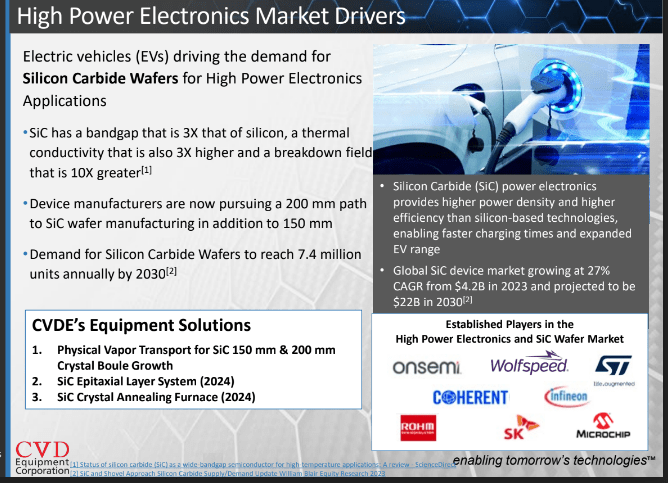

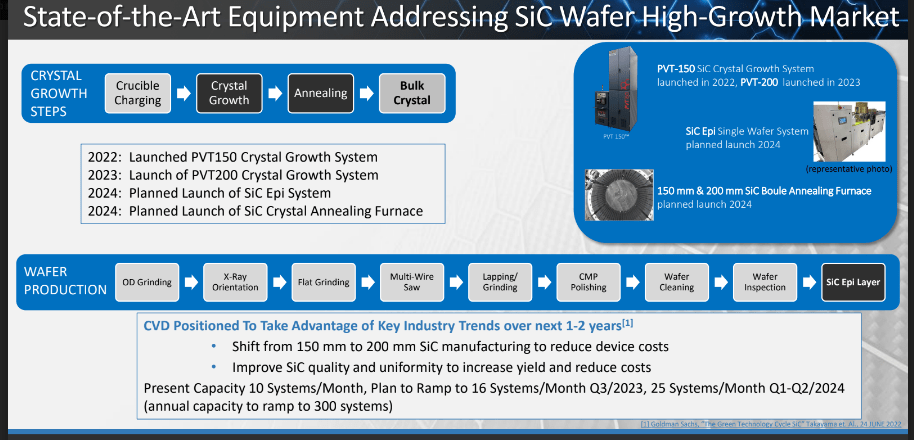

This is one of the reasons our interest was piqued again as the company produces the PVT 150 , which is used for growing silicon carbide crystals that are subsequently processed into 150-millimeter silicon carbide wafers.

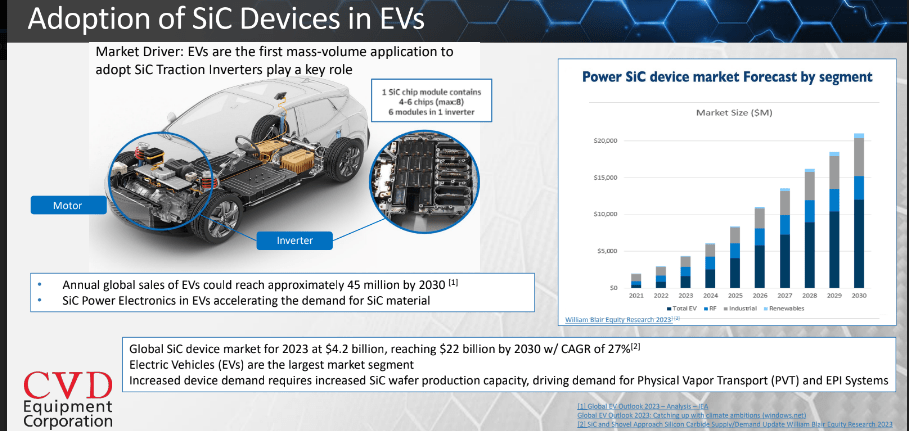

SiC wafers, our members are familiar with these as our best-performing stock Aehr Test Systems ( AEHR ) is killing the market for testing these wafers, and we also know this is very much a market that is still in the very early innings.

{kind=link}

From the Aehr Q4CC, we know that William Blair sees SiC wafer demand for just EVs and EV chargers to grow from 220K in 2022 to 4.5M in 2030, a stunning 45% CAGR with other SiC segments (industrial applications, energy conversion, RF amplifiers, etc.) delivering another 2.8M wafers by 2030.

So needless to say there is a secular tailwind, if not tailstorm blowing in this market, but not all participants have an ironclad competitive position as Aehr.

CVD did receive an order for 30 of their PVT 150 systems and recognized $2.5M of revenue in Q1 from this with the remaining 10 systems to be shipped in Q2.

And they are planning additional wins in the SiC segment (Q1CC):

Yes, we do plan to expand to other US manufacturers and then European manufacturers of wafers, some wafers and devices. Some are devices, wafers, flash and also equipment. So, we have a strategy for each one of those categories... reached out to at least seven and engaged in discussion with at least three additional ones to the one account that we have already an installed base. So, we're in the selling process.

What is also pleasant to know is that they have new products planned for the next couple of years:

{kind=link}

The upcoming Epitaxial (Epi) system in particular has a much bigger TAM and much higher ASP, and they have some experience in this field having shipped an SiC Epi tool in 2008 (Q1CC):

We have demonstrated the ability to control temperatures up to 2,000 degrees with four long campaigns days, weeks, with plus/minus 0.5 degree, which is fairly exceptional, I would say. I our ability also to manufacture the product in-house gives us what I anticipate to be a competitive advantage from a price performance perspective.

The Epi tool is scheduled to enter the market in Q3/24, so we'll have to wait for that for quite a while yet, but discussions with prospective customers will start early next year when they can deliver performance data already.

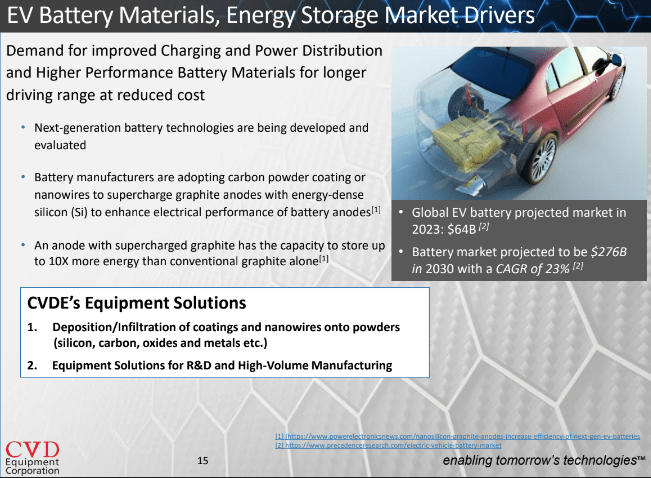

Battery materials

{kind=link}

The company received a $1.8M repeat order for their PowderCoat 1104 system but this spilled over into Q2.

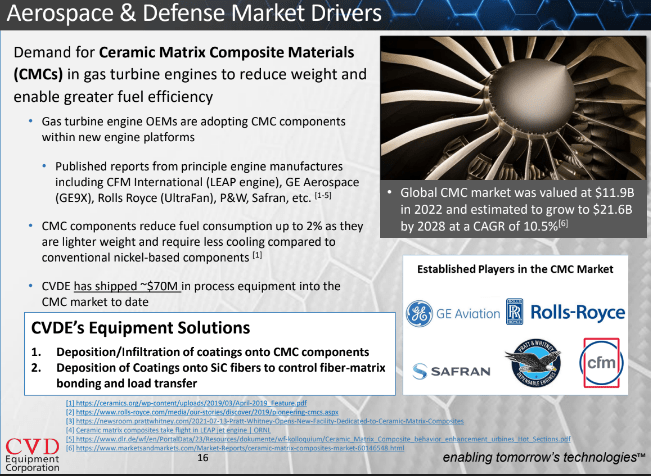

Aerospace and Defense

{kind=link}

The company's main product is (Q1CC):

a chemical vapor infiltration systems and also tow coating systems to manufacture ceramic matrix composite materials also referred to as CMC for use in gas turbine engine components. CMCs can withstand extreme temperatures and are one-third the weight of nickel-based super alloys. This allows jet engines to run hotter, thereby consuming less fuel and emitting less pollutants.

The company received a $3.7M order in Q4 for the production CIV tool order to manufacture CMCs for aerospace gas turbine engines with a $300K contribution in Q1 from this order. They now have two leading producers of gas turbine engines as a customer.

Finances

Growth is quite remarkable and seems to be accelerating:

The Company operates through three segments:

- CVD Equipment that supplies chemical vapor deposition, physical vapor transport, and thermal process equipment.

- SDC (Stainless Design Concepts, that is, gas delivery systems) designs and manufactures ultra-high purity gas and chemical delivery control systems.

- CVD Materials provide products related to advanced materials and coatings, it's a non-core business, and one of the two businesses, Tantaline, was sold in May.

Readers might want to look at the website ( here and here ) to get a feel for the huge amount of systems that the company produces.

From the 10-Q:

CVV 10-Q

Another split out to market type:

CVV 10-Q

Again the contrast with a year ago is notable:

CVV 10-Q

The energy market includes SiC wafer and battery customers. The aerospace market includes customers that manufacture aircraft engines. The industrial market has various customers in diverse industries. The research market services universities and other research institutions.

The $3M increase in CVD Equipment is mostly related to the PVT 150 system sales (for a single customer), constituting 42.2% of the CVD Equipment segment. SDC also had a very good quarter with revenues rising 63%, although from a very small base.

Backlog declined from $17.8M at the end of Q4 to $12M at the end of Q1, not due to the loss of orders to competitors but this could spill over into weakness for the rest of the year.

One thing investors should take on board is that growth is quite lumpy quarter to quarter, simply due to the timing of orders, for instance (Q1CC):

In the silicon carbide area or arena for our PBT product line, there it is a bit of waiting for qualification by our customer to take the next step on expansion and us then also getting our order from our second potential customer and there's always capital raise involved with that.

But management is expecting additional orders for the PVT 150 system from the same customer and is also talking to other potential customers.

There were similar delays in the other two growth areas, in the battery segment they hoped to close an order in Q1 but that spilled over into Q2.

Margins have been trending upwards (these are the GAAP versions):

The cash flow also recovered:

The company had $11M of cash left at the end of Q1 and should expect some payments from the sale of Tantaline (although these are unlikely to move the needle all that much). It's enough to meet their CapEx and cash needs for the coming 12 months.

Valuation

6.77M shares out with 900K options but only 252K of these are exercisable so a fully diluted share count of 7.02M shares, at $7.30 per share that's a market cap of $51.2M or an EV of $40M which makes the shares trade at a modest 1.3x EV/S.

Conclusion

This is an interesting company to follow and one could establish a first position here (we won't as we can't buy everything), a lot is going for it:

- It is serving markets that are benefiting from secular tailwinds, most notably the SiC wafer market.

- It is continuously developing new solutions, delving from a wealth of technical expertise and know-how with the upcoming Epi tool for the SiC market, especially interesting.

There are also risks, the vagaries of order timing produce the odd disappointing quarter and the company needs to scale up to produce sustainable finances, in the words of management (Q1CC):

Our return to consistent profitability is dependent, among other things, on the receipt of new equipment orders, our ability to mitigate the impact of supply chain disruptions and inflationary pressures, as well as managing planned capital expenditures and operating expenses.

For further details see:

CVD Equipment Corporation's Recovery Looks Set To Continue