CVI - CVR Energy: Despite Economic Concerns Dividend Growth Should Continue

2023-04-03 04:09:10 ET

Summary

- Due to never-before-seen refining margins, 2022 was very profitable for CVR Energy but economic concerns do not create a positive backdrop going forwards into 2023.

- At least their guidance for 2023 capital expenditure shows minimal spending, which helps generate free cash flow.

- They also have a solid financial position, which means they are well-positioned to ride out any proverbial storms later in the year.

- In turn, this also supports their dividend growth in the medium to long-term once these short-term economic concerns abate.

- Until we know the banking crisis is definitely over, I only believe that maintaining my hold rating is appropriate.

Introduction

Notwithstanding the otherwise tragic loss of life in Eastern Europe, the first half of 2022 was very profitable for the energy sector, especially CVR Energy ( CVI ) as refining margins hit never-before-seen levels and thus as my previous article discussed, it seemed their recovery was now complete. In the subsequent months, their shareholders enjoyed massive special dividends as management passed along this cash windfall. Going forwards into 2023, it appears that despite economic concerns in the short-term, their dividend growth should continue into the medium to long-term.

Coverage Summary & Ratings

Since many readers are likely short on time, the table below provides a brief summary and ratings for the primary criteria assessed. If interested, this Google Document provides information regarding my rating system and importantly, links to my library of equivalent analyses that share a comparable approach to enhance cross-investment comparability.

Author

Detailed Analysis

{kind=link}

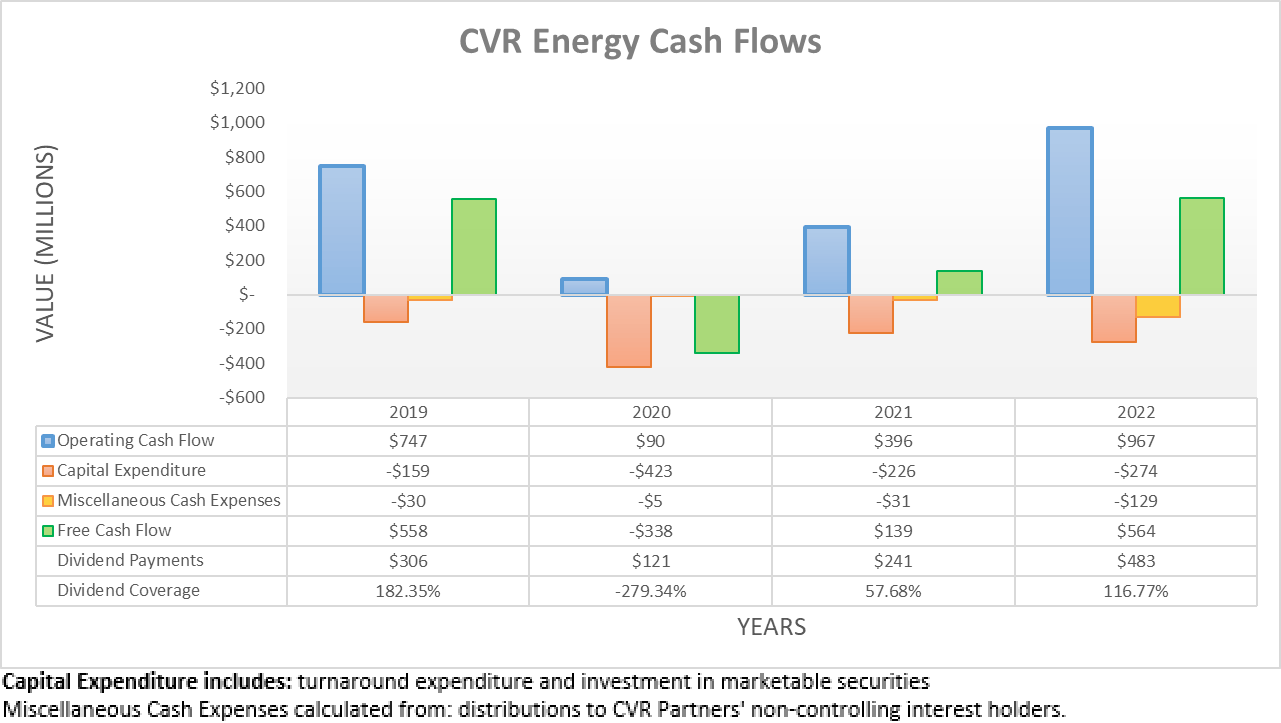

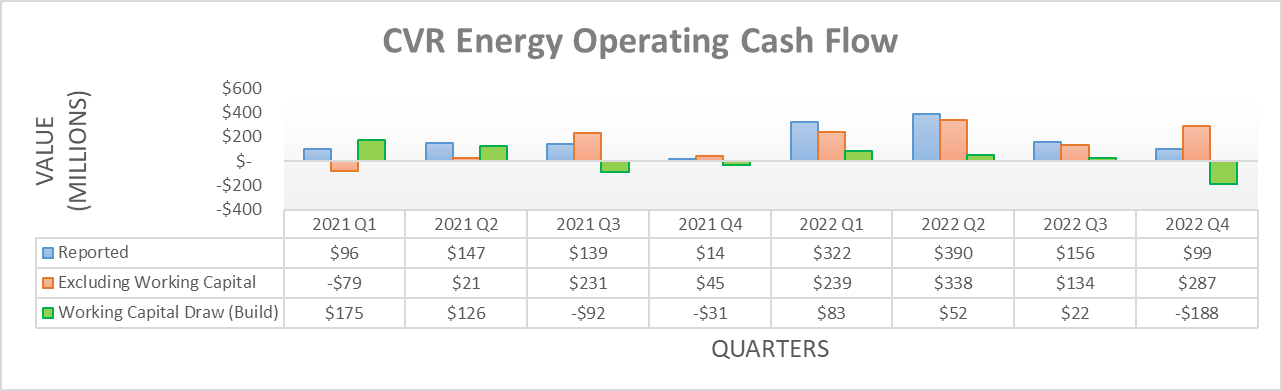

Following a massive cash windfall during the first half of 2022 on the back of the booming refining margins after the Russia-Ukraine war, the second half was far more modest. As a result, their operating cash flow closed out the year with a result of $967m, which was only a modest increase compared to the $712m they had already generated during the first half, although this was partly due to working capital movements.

{kind=link}

Despite having seen only relatively small working capital movements during the first, second and third quarters of 2022, the fourth quarter saw a very large build of $188m that materially weighed down their reported operating cash flow. If excluded, their underlying result of $287m was actually quite strong based on their historical performance since at least the beginning of 2021, as it amounts to the second-highest result.

Whilst a positive end to the year, going forwards into 2023 the inherent volatility of their industry will see results continue fluctuating. That said, the recent economic concerns on the back of banks collapsing do not create a positive backdrop because refining margins are heavily influenced by economic conditions and there is no positive way to spin a baking crisis for the economy. As for the time of writing, a fragile stability seemingly returned to markets following the takeover of Credit Suisse ( CS ) but alas, uncertainties persist as investors await to see whether this is an intermission or hopefully, the end of the banking crisis. Even though their operating cash flow remains impossible to predict, thankfully their guidance for 2023 forecasts minimal capital expenditure, as per the commentary from management included below.

Looking ahead to the first quarter of 2023, for our Petroleum segment…

…total capital spending to be between $40 million and $50 million and turnaround spending to be between $35 million and $45 million.

For the Fertilizer segment…

…total capital spending to be between $5 million and $10 million.

For renewables…

…total capital spending to be between $20 million and $30 million."

- CVR Energy Q4 2022 Conference Call.

If aggregated together at the midpoints, this sees forecast capital expenditure of $117.5m during 2023 and if forthcoming, it would be their lowest capital expenditure during 2019-2022 that varied between $159m and $423m. Obviously, the biggest contributor is always their operating cash flow that cannot be predicted but at least this helps limit their cash outflows and therefore by extension, helps generate free cash flow. Unless they experience a downturn, their minimal capital expenditure should see excess free cash flow after dividend payments now that the massive ones pertaining to their special dividends are seemingly a thing of the past, as per the commentary from management included below.

Looking at specials, I think the reason that we did specials was because we viewed the cracks that we were experiencing as somewhat unusual and not sustainable. And so they were onetime deals. We view a little bit today that, with the shortage of refining capacity out there, the inventories where they're at, the backlog of turnarounds that the industry is experiencing and yet to execute that we're cautiously optimistic of the outlook. So that's the reason that I think the Board had pretty good confidence that the regular dividend should be increased."

- CVR Energy Q4 2022 Conference Call (previously linked) .

Whilst not exact guidance, I interpret their commentary to mean that special dividends are not likely to be forthcoming going forwards into 2023, unless we see another repeat of the booming refining margins from 2022 but obviously, this is not likely given the economic concerns. That said, they are obviously open to the idea of dividend growth in line with the ability of the company during normal operating conditions, which in my eyes is effectively going back to the old way from before the Covid-19 pandemic threw a spanner into the works, metaphorically speaking.

After increasing their quarterly dividends to $0.50 per share, these should now cost $201.1m per annum given their latest outstanding share count of 100,530,599. Even though their free cash flow will continue fluctuating across the years, this only comprises a modest amount versus their operating cash flow and thus, it is not necessarily a burdensome commitment. To this point, 2019 was the last normal year and they generated $747m of operating cash flow that if utilized as a basis point, would see their new dividend payments only consuming circa 27%.

Unfortunately, the inherent volatility of their industry makes it impossible to provide more accurate assertions but as a rule of thumb, this indicates they have scope for more dividend growth in the medium to long-term once economic concerns abate. Admittedly, it would likely be at a slower pace than recently but at least, their financial position remains solid and thus well-positioned to ride out any proverbial storms whilst also supporting their dividend growth.

{kind=link}

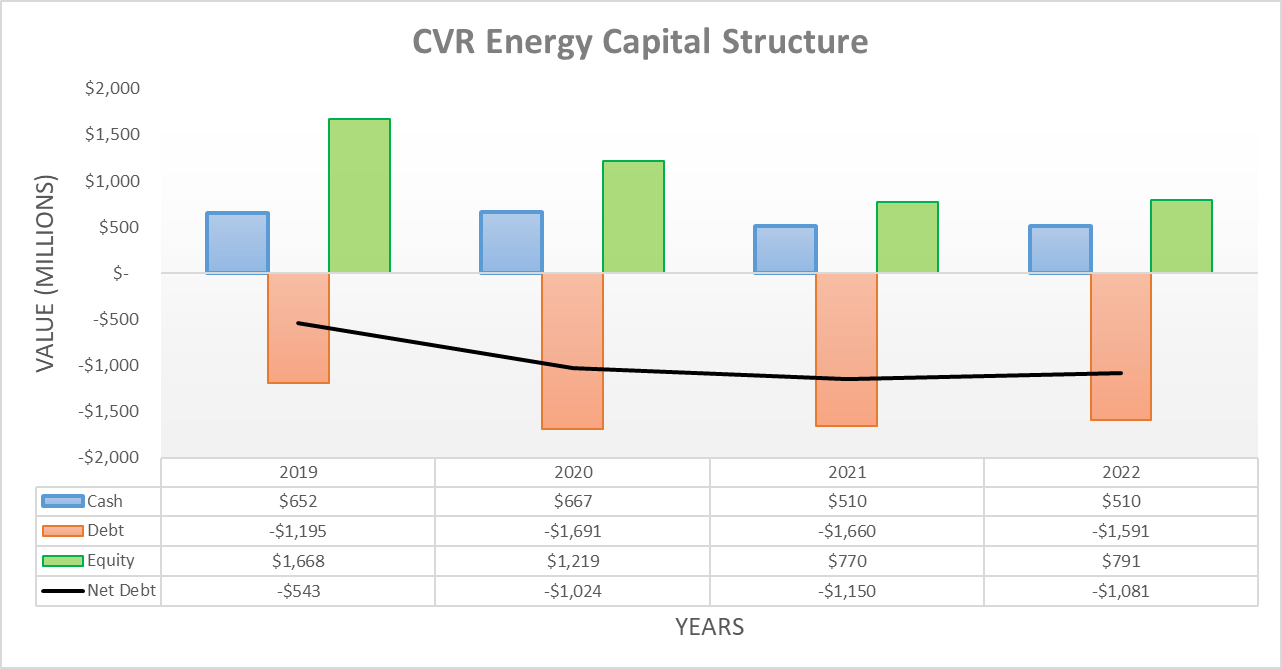

When conducting the previous analysis following the second quarter of 2022, their net debt had decreased to $701m but following the second half, it ended the year at $1.081b. On the surface, this might sound contrary but it mostly stems from the timing of their dividend payments, especially those massive ones pertaining to their special dividends because out of their payments of $483m during the full year, the second half saw $443m alone.

Once everything is said and done, their net debt decreased slightly during 2022 versus its previous level of $1.15b at the end of 2021. Going forwards into 2023, their net debt should continue decreasing thanks to their guidance for minimal capital expenditure and thus their aforementioned prospects to generate excess free cash flow after dividend payments, although the extent is impossible to ascertain given the inherent volatility of their industry.

{kind=link}

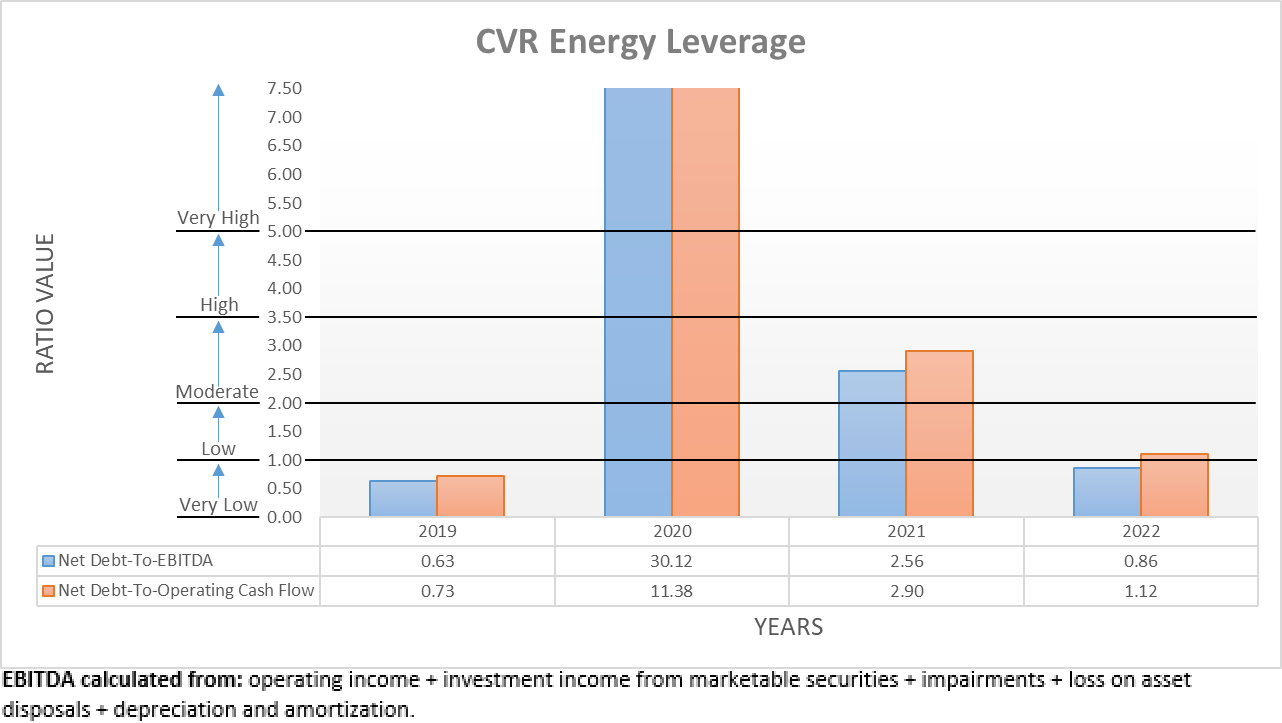

Thankfully, the extent their net debt decreases does not necessarily matter given their existing leverage. Even after seeing their net debt increase during the second half of 2022, their net debt-to-EBITDA still ended the year at 0.86 versus its previous result of 0.46 following the second quarter. It may be a sizeable change in percentage terms but from such a low base and thus even now, it remains beneath the threshold of 1.00 for the very low territory. Unsurprisingly, their net debt-to-operating cash flow also increased to 1.12 versus 0.61 across these same two points in time, respectively. Whilst it now sits above the threshold for the very low territory, it still sits towards the bottom of the range of between 1.01 and 2.00 for the low territory that is obviously not problematic. Going forwards into 2023, their leverage will continue to increase and decrease alongside their prevailing future financial performance and thus, operating conditions.

{kind=link}

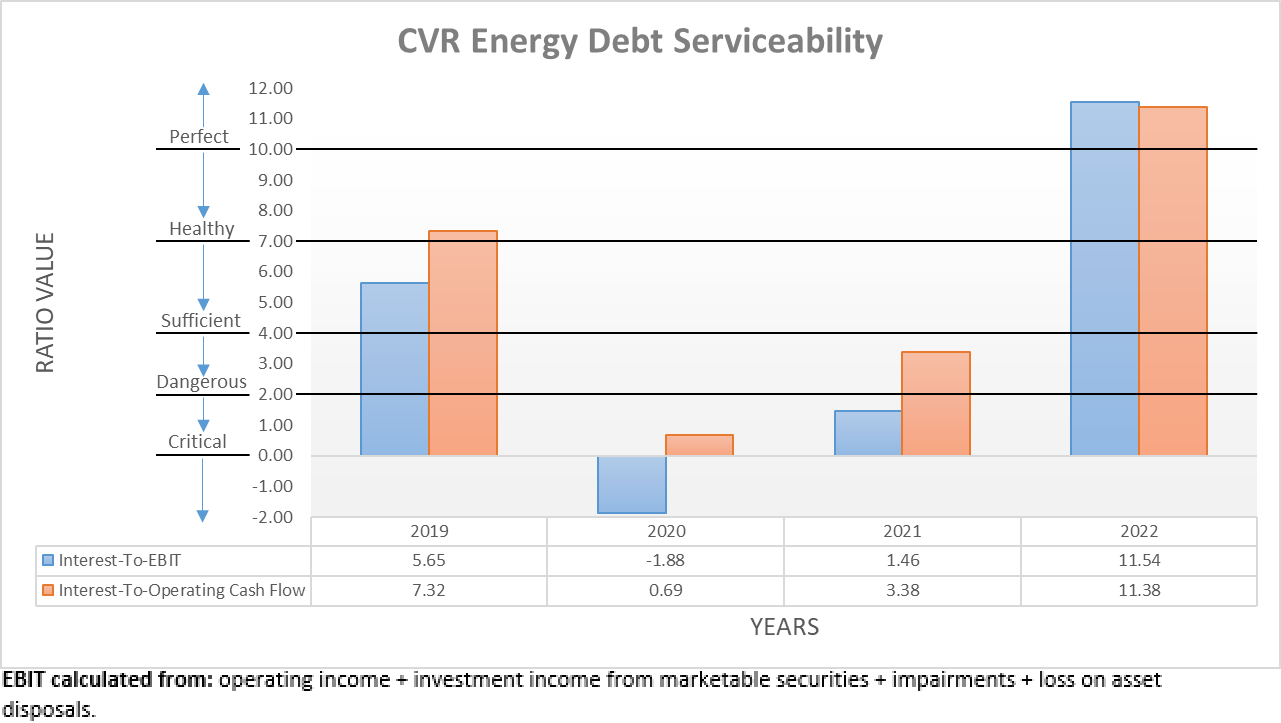

Similar to their leverage, their debt serviceability also sees them well-positioned given their interest coverage is still perfect at the end of 2022, despite their net debt increasing. When compared against their EBIT, they see a result of 11.54, which is only a small change versus their previous result of 12.98 following the second quarter. Likewise, when compared against their operating cash flow, they see a very similar result of 11.38 and thus, once combined with their low leverage, this sees a margin of safety before their net debt would become burdensome.

In turn, this situation lowers their requirement for deleveraging, which supports their dividend growth in the medium to long-term once these short-term economic concerns abate. It also quite importantly means they are well-positioned right now to ride out any proverbial storms in capital markets, which is especially useful and helps lower downside risks in general.

{kind=link}

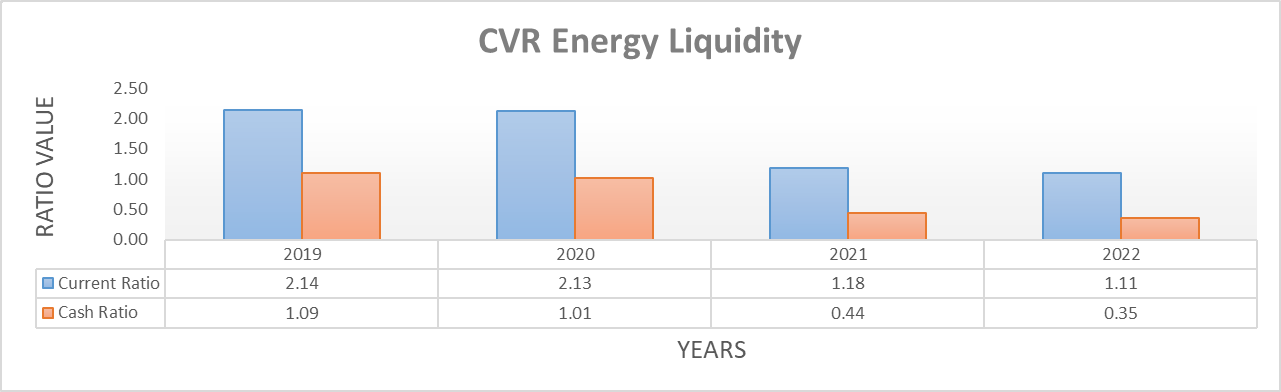

Whilst already positive, the proverbial cherry on top is their liquidity that most importantly sees a cash ratio of 0.35 at the end of 2022. Despite being less than their previous result of 0.53 following the second quarter, it still points towards strong liquidity, especially given their accompanying current ratio of 1.11 at the end of 2022 that is barely changed versus their previous result of 1.25.

It remains to be seen whether the recent banking crisis reemerges going forwards into 2023 but thankfully, they are isolated as much as possible given they should be a net contributor to capital markets. This primarily stems from the outlook for their cash inflows and accompanying outflows, as the former should outpace the latter thanks to their minimal capital expenditure, hence their aforementioned prospects to reduce net debt. Secondarily, this also stems from a lack of debt maturities until February 2025 when their next senior note comes due and thus when combined, these two variables ensure they should survive even if the banking crisis reemerges. Normally, requiring access to capital markets is not necessarily problematic but if the banking crisis reemerges whilst monetary policy remains tight, this could prove difficult and thus by extension, it could have otherwise created risks for their dividends.

Conclusion

Since their financial position is solid, they are well-positioned to ride out any proverbial storms later in the year given the economic concerns and possibly banking crisis, especially as a net contributor to capital markets. As for their dividend growth, I suspect they are returning to the old way, whereby they take a steady approach instead of the flood of cash shareholders enjoyed during 2022 from their massive special dividends. Thankfully, their modest size and lack of requirement for deleveraging supports their dividend growth in the medium to long-term once these short-term economic concerns abate. Whilst positive, due to economic uncertainties right now, I only believe that maintaining my hold rating is appropriate for the time being until it becomes evident the banking crisis is well and truly in the rear-view mirror given the risks it poses to the economy and thus by extension, their refining margins.

Notes: Unless specified otherwise, all figures in this article were taken from CVR Energy's SEC Filings , all calculated figures were performed by the author.

For further details see:

CVR Energy: Despite Economic Concerns, Dividend Growth Should Continue