CVI - CVR Energy: Solid Q3 Results But The Icahn Overhang Remains

2023-10-31 08:00:07 ET

Summary

- CVR Energy shares have underperformed despite strong profits and dividends, likely due to drama surrounding Carl Icahn.

- CVR operates refineries and owns a stake in a fertilizer producer, with strong refining margins and positive operating results.

- Refining margins are expected to stay wide, in my view, due to a lack of capacity, making CVR an attractive investment for income-seeking investors.

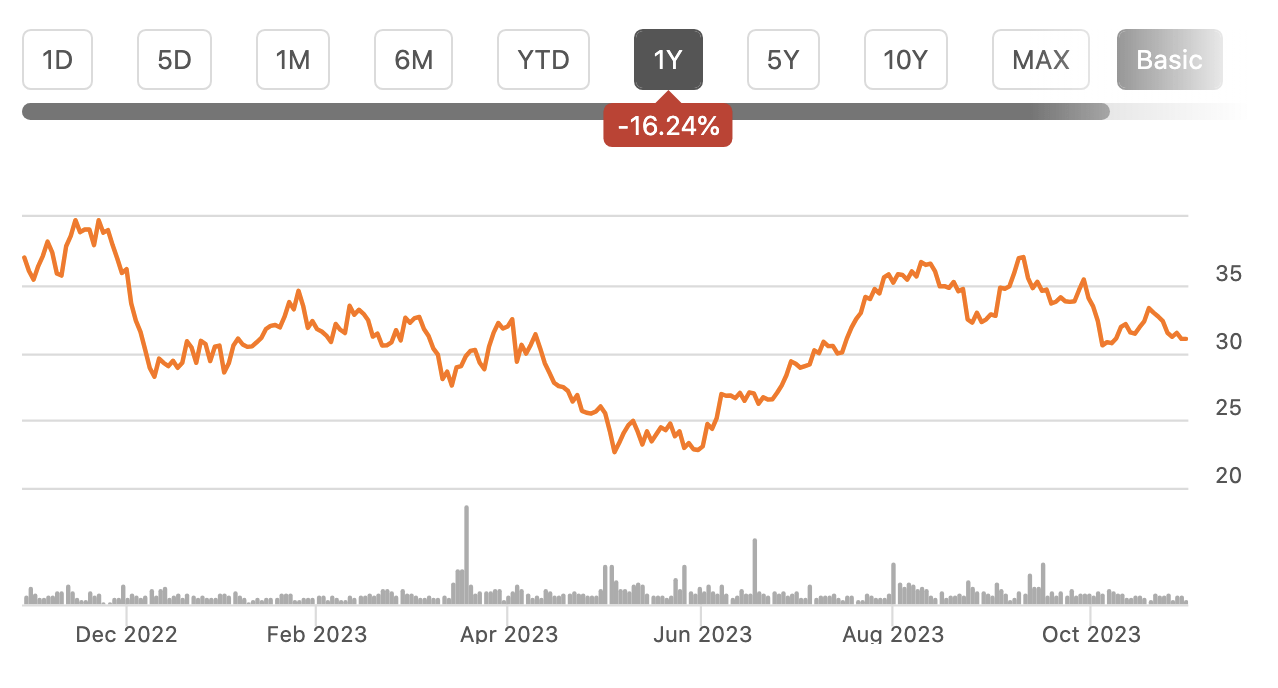

Shares of CVR Energy ( CVI ) have been a poor performer over the last year, losing about 16% of their value, even as the company has churned out strong profits and paid out significant regular and special dividends. Additionally, drama surrounding Carl Icahn has likely weighed on shares. Still, I view the stock as attractive, given tailwinds for the refining sector.

{kind=link}

CVR operates 2 mid-Continent refineries with just over 200,000barrels/day of processing capacity. It also owns 37% of CVR Partners (UAN), a fertilizer producer. Its stake in UAN is worth about $300 million or $3/share. It also has general partner control over UAN and consolidates its financials even though the obligations are non-recourse. The company is controlled by Carl Icahn, which I will discuss further below.

In the company’s third quarter , CVR earned $1.89 in adjusted earnings, which was $0.04 below consensus even as revenue beat by $140 million at $2.52 billion. This EPS excludes a $1.30 gain from the re-evaluation of its renewable fuel standard liability. Adjusted earnings were essentially flat to last year’s $1.90.

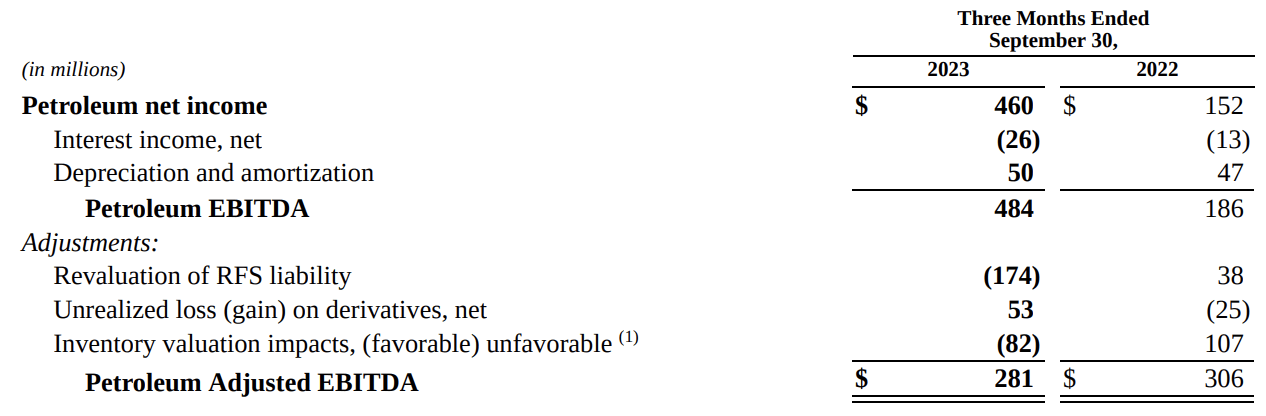

Its refining unit earned $31.05/barrel, up from $16.56 last year, driving operating income up nearly $300 million to $431 million. However, there was a lot going on under these numbers, which overstate this year’s strength and understate last year’s results. Renewable fuel standard costs were $90 million, down from $98 million. CVR also had a $173 million benefit from re-evaluating RINs vs a $38 million cost last year, which are credits earned by producing ethanol and biodiesel. Excluding mark to market reevaluations, its refining unit had $262 million in earnings from $175 million, last year. However, the company had some gains from inventory timing, partially offset by hedging losses on commodity derivatives. The below table is a helpful way to disentangle underlying operations from one-item items and re-evaluations.

{kind=link}

As you can see, while net income tripled, true run-rate EBITDA was down by $25 million to $281 million. In terms of actual operating results, there were several important highlights. On the positive side, refined output rose 5.5% to 211,032. Additionally, direct operating expenses fell by nearly 3% to $5.39/barrel. Against these operating positive, CVR was negatively impacted by the fact the 321 crack spread, which measures how much refineries net by turning crude oil into diesel and gasoline, declined by $4.84/barrel.

As you can see below, crack spreads have been narrowing of late, but they remain at historically attractive levels. This is a major reason why the refining sector has generated such substantial profits. The key question for future profit levels is whether this margin can remind wide.

Energy Stock Channel

In my view, refining margins are likely to stay structurally wider because we have a lack of refining capacity. In the US, refining capacity is down 6% from its peak pre-COVID. Given all of the regulatory constraints and governmental push to move to greener sources of energy, it is all but impossible to build a new refinery. Indeed, America has not built a major refinery since the 1970’s .

EIA

Even around the world, despite the growth in emerging markets, refined capacity is flat the past four years. Considering the fact Mexico’s effort to build a refinery ran to $20 billion , we are simply not likely to see the level of investment needed to create spare refined product capacity.

Statista

Supply constrained markets lead to wider profits all else equal. Usually, this leads to investments in increased capacity to compete those margins away. For refiners, I expect this to persist structurally. Of course, in economic downturns that reduce demand for gas and diesel, margins will tighten, but on average, I expect them to stay wider than normal. While 321 spreads moved between $10 and $20 pre-COVID. I suspect we are now in a $20-30 world. At $20 refined margins, CVR has $3.75-$4.00 in earnings power. In the meantime though, the company is earnings more and generating extraordinary cash flow. CVR had $319 million in free cash flow in Q3 and $802 million year to date. Cash and cash equivalents are $889 million, up $379 million year to date. CVR carries just $1.6 billion of debt ($1 billion excluding UAN), or a bit less than 1x EBITDA at the refining operation. This is a very manageable debt load.

Due to the strong cash flow, alongside these results, the company declared a $1.50 special dividend on top of its regular $0.50 quarterly payout. The regular payout alone provides a 6.3% annual yield with this special payout nearly 5%. In Q2 , CVR also made a $1 special payout. While some companies like Valero ( VLO ) have used their cash flow to dramatically reduce their share count, CVR has chosen to pay dramatic dividends with an all-in yield north of 15%.

Personally, I am agnostic on special dividends vs share repurchases, as each has its pluses and minuses. Dividends provide you cash directly, but dividends can result in you paying taxes whereas buybacks do not cause you taxes if you hold shares, only if you sell. Much of course depends on where shares are trading, to determine if buybacks add value. I appreciate though that many investors value income. What I think is critical is that CVR is paying a special dividend on top of its regular dividend.

Refining is cyclical, and this level of cash flow may not persist forever. I would not want to see management to commit to a regular payout based on boom-time cash flow. Similar to a share repurchase that can be turned off during a downturn, special dividends are not a commitment. I believe separating out a base dividend from a special dividend is the prudent move. With $1 billion in run-rate refining EBITDA, its $200 million regular dividend can be safely covered. I also suspect CVR has chosen the dividend route because its primary investor likes the cash flow the dividends provide.

Carl Icahn and Icahn Enterprises ( IEP ) sold 4.1 million shares in September , after selling 400,000 in August . Through these sales, Icahn has raised $157 million. He still owns about 67% of the company though. Given the stresses felt at IEP following the Hindenburg short-selling report, it would not surprise me if there were further sales by Icahn, but it is hard to know. It is important to be clear that challenges at IEP should not impact CVR’s underlying financial results, but further sales could put pressure on shares. I would be concerned if CVR appeared to be approving excess dividends, but for now, this is not the case. Dividends are covered by cash flow.

CVR’s refining operation should be able to sustain $3.75 in earnings under my average refining environment, given the view of refining spreads staying somewhat wider than their pre-COVID average. At 10x earnings, this would make CVR a $37.50 stock. This would also value CVR at an EV/EBITDA of just under 5x, which I view as a fair multiple given CVR’s smaller size. Adding the $3/share stake in UAN, and we get a $40.50 valuation without assigning any value to its general partner interest.

That points to nearly 30% upside to fair value. I believe a significant portion of this discount is due to Icahn’s stake. As a controlled company, it does not sit in as many indices, and some institutional investors may be less inclined to hold it. That is during normal times. We can add to that the fear of him continuing to sell shares, which in a stock that is not that liquid can apply quite some pressure.

For patient and income-oriented investors, I think CVR is attractive, and I expect the special and regular dividend combined yield to stay safely above 10% into 2025. However, the Icahn overhang is likely to persist, and there could be further share sales, which create a bumpy ride. All else equal, I would rather own Valero, which also trades at a low multiple but does not have the same idiosyncratic pressures. It however pays a smaller dividend. CVR is a buy for income-seeking investors as it will generate substantial cash flow thanks to the bullish medium-term outlook for refining, but investors should not expect its multiple to expand to my fair value in the near future, given Icahn’s stake.

For further details see:

CVR Energy: Solid Q3 Results, But The Icahn Overhang Remains