CVRX - CVRx: Price Response For Barostim Trial Equals Uncertainty On Equity Curve

Summary

- Heavy selloff following top-line data from the BeAT-HF trial, that failed to meet primary endpoint.

- Still, there were numerous secondary data that were positive.

- CVRX is subsequently submitting for label expansion for Barostim.

- Price needs to find equilibrium in order to guide price visibility looking ahead.

- Paring back rating to hold until further clarification is obtained on the next moves for Barostim.

Investment Summary

One of the key challenges with investing in early-stage medical technology and devices ("med-tech") companies is that much of the potential equity upside in the first stages of the growth cycle is dependent on impeding clinical trial data, versus fundamental factors such as sales, profitability and/or earnings. Whilst this is a key differentiator of success, it also means tremendous risk potential if the trial data goes against the expected outcomes. Here we have CVRx Inc (CVRX) exhibiting just that. In what was a strong equity curve for the stock over the 6-months to February FY22', the stock met our price target of $19.45 set in the December publication called " Barostim Accelerating, Upside Targets Forming ". However, following the top-line data readouts of its Baroreflex Activation Therapy for Heart Failure ("BeAT-HF") study yesterday, investors wiped out >$210mm in value from the company's market cap, seeing the stock drop from ~$17 at the start of the week to ~$7 per share at the time of writing. As a reminder, the trial, that spanned 7 years in total, looked into safety and efficacy of its Barostim device in respect to heart failure. The results open up an interesting debate, as the study missed its primary endpoint, but showed statistical significance in other measurements. Subsequently CVRX intends to apply for an expansion of Barostim's labelling through the FDA. Alas, the key questions that need answering now are 1) how much, if any, further pain will investors inflict on its stock price, 2) can the firm achieve the label expansion, and 3) does the market believe it can do so. A clear explanation of each is needed in order to guide price visibility down the line, notwithstanding the propensity of Barostim's successful commercialization. With that in mind, it would be wise to pare back our rating to hold until further clarification of the above points are obtained.

CVRX heavy selloff in response to Barostim data

The BeAT-HF [from hereon in, simply, "BeAT Trial"] trial was a multi-centre RCT that examined safety and efficacy of Barostim in patients suffering heart failure ("HF") with reduced ejection fraction. As a quick reminder, the Barostim device uses an electrophysiology route, via an implantable neuromodulation device to electronically stimulate baroreceptors located in the carotid artery wall. Stimulation of these receptors produces an autonomic reflect from the heart, i.e., a stimulating or depressive effect that modulates heart rate, stroke volume and cardiac output. The Barostim hypothesis is thought to stimulate these carotid receptors, to increase ejection fraction and the propensity of the heart to sufficiently pump oxygenated and deoxygenated blood around the heart. The BeAT trial, that examined the progress of 323 patients longitudinally, looked to measure this effect by reducing HF events requiring hospital or emergency department admission as its primary endpoint. Unfortunately for CVRX longs [including thyself] the study did not achieve statistical significance in terms of this primary outcome measure. This is despite collecting data over 332 primary events with a median follow up of 3.7 years. This is a large blow for the Barostim hypothesis, and more so CVRX equity investors, as the market was pricing in a successful progression from this study onto later-stage clinical trials, and a potential approval.

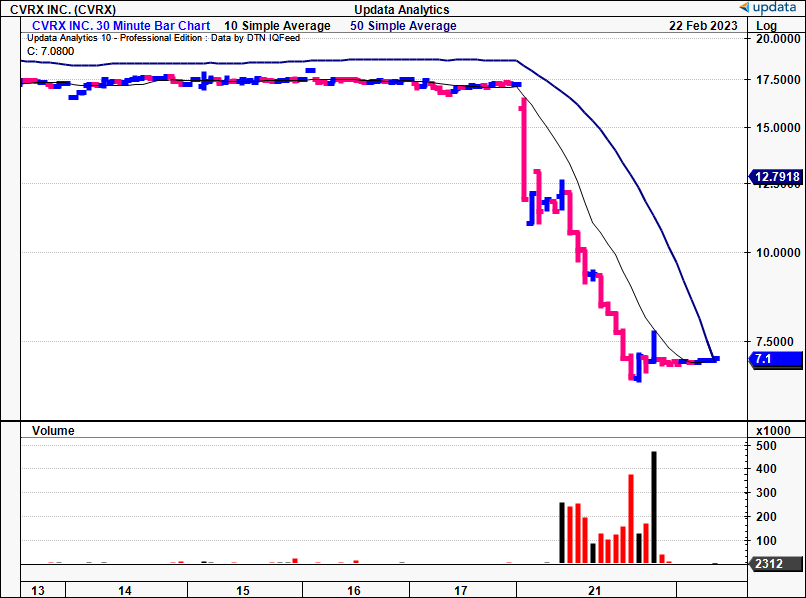

Immediately, investors exited the stock and either closed or trimmed back positions en masse as a result of the readouts. To understand the magnitude of negative sentiment, see Figure 1 below, that looks at 30-minute price data for CVRX since February 13th. Each bar represents a 30 minute time frame, with red bars indicating a negative price change. Note, that near-precisely at the timing of the release, the stock immediately gapped down and continued a heavy selloff into the rest of the trading session. There's only ~20mm CVRX shares outstanding, and we can see the heavy selling volume represented by the volume bars below. Interestingly, there were buyers at some point, however it's difficult to ascertain who these might be.

Fig. (1) CVRX 30-minute price data - immediate selloff following BeAT trial top-line data

{kind=link}

Where to next for CVRX: mid-term growth levers

It's important to acknowledge that it wasn't all doom-and-gloom from the top-line data. Although the study didn't hit a statistical significance with respect to the primary endpoint, there were several other secondary clinically relevant outcomes that point to a favourable result for Barostim. Per the announcement , these include:

- All-cause survival for those free from left-ventricular assist device ("LVAD") and cardiac transplant

- Win-ratio composite related to the primary endpoint measures - cardiovascular mortality, HF events, quality of life

- Clinical stability

Further, Barostim the data did in fact keep in-line with the FDA's pre-market approval, namely symptomatic improvement at 6 months and the device's safety profile. Both were " durable" at 24 months follow up.

Consequently it really boils down to whether CVRX can obtain label expansion for the Barostim device. We estimate that it would be arguing that Barostim could in fact be a valuable addition to the armamentarium of current therapies commercially available for HF patients. CEO Nadim Yared was actually very constructive on the results, "This new evidence is welcome news for the many patients with heart failure, who remain symptomatic despite optimal medical therapy. We plan to submit the totality of evidence of BeAT-HF to FDA seeking an expansion of Barostim labelling". Further, Michael. R. Zile, M.D. of University of South Carolina noted that Barostim is "an effective treatment for heart failure".

This segways into the company's FY22' results posted last month. It booked a 108% YoY growth in its HF business to $6mm in Q4' underscored by a total volume of 193 units versus 95 the year prior. Full-year revenues were $22.5mm for the year, a 73% YoY growth schedule. On this, it recognized a core operating loss of $42.5mm, still a loss of $32.5mm when excluding R&D and treating it as an investment. Moreover, it had 106 active implanting centres under its wings by the end of FY22', with 26 U.S. territories in the U.S. relative to 14 the year prior. It also had $106mm in on balance sheet cash by the end of period after burning through $11mm in Q4', totalling $36mm burn-rate for the entirety of FY22'. As such it is well capitalized from a solvency perspective, with a current ratio of >15x and only $6.7mm in long-term debt. Importantly, the firm guides to top-line revenues of $35-$38mm for FY23', calling for a ~69% growth rate at the upper end of range on a gross margin of ~79%. It also expects OpEx of ~$80mm at the upper bound, which calls for a $49mm operating loss for the year.

Subsequently, we firmly believe the company's medium-term growth route will be largely dependent on the productivity of its existing and new accounts, combined with new the adoption of new accounts. Management have noted that success in this regard is in fact driven by a combination of this duo. In fact, the addition of new accounts has reduced average productivity when looking across the entire provider base. This is self-explanatory, but does call for an uptick in both the new and existing prescriber base. To this point, management have said in the past that when they start a new account, the provider treats 1-2 patients before pausing for 3-6 months to observe results. This is also due to reimbursement dates and payments as well. However, following the 3-6 month date, management note that productivity is said to accelerate, meaning the tail of new starts begins to accelerate as time goes on. Hence, it boils down to the combination of existing accounts spending some time with CVRX, and, the adoption of new accounts to start this 'process' as it were.

Final remarks

It's difficult to ascertain what the resultant selloff from CVRX's Barostim data will mean for its stock price over the coming weeks to months. It first needs to achieve price equilibrium before we have greater clarity on what to do with respect to positioning. Noteworthy, is that CVRX met our previous targets of $19.45, outlined in the report from December [see introduction for link]. Still, there's no model, either fundamental, technical or quant-based that can make this kind of projection without the equilibrium to establish where the stock might bottom by best estimation. A few points of consideration, however:

- The market was heavily rewarding the Barostim story prior to the top-line data. CVRX had pushed to 52-week highs of ~$20 just before the selloff.

- Management are still going to submit the total evidence from the BeAT trial, to push for label expansion of Barostim, as mentioned.

- This is supported by the second-line data obtained from the study, and so there's still an indication it could achieve label expansion.

- Should this occur, there's a probability investors will again pile into the stock.

- Remember, the market often over-reacts to both good and bad news, but the key is understanding 1) where the bottom may be, and 2) providing clarity on future expectations. Related to point 2, David Kostin, Goldman Sachs, chief equity strategist, notes the stock market is "anticipatory; it traditionally looks forward into the following year, on average around July, although it has in the past looked forward as early as March and as late as November". In that vein, it's important to emphasize that we continue to factor the long-term prospects of CVRX, whilst not completely ignoring the short-term machinations following this repricing.

Net-net, we are paring back our rating on CVRX to a hold for now. That's not to say there isn't scope for the company to continue its growth route over the mid to long-term. We just need more clarity on the market's directional bias in the stock, and advocating to buy now could be a downside risk not worth accepting at this stage.

For further details see:

CVRx: Price Response For Barostim Trial Equals Uncertainty On Equity Curve