RNECF - Cycle Worries Weighing On Renesas Electronics And Creating A Bargain Valuation

Summary

- Semiconductor lead-times have started to retreat and the industry is likely to see meaningful price erosion in 2023 on weaker demand, but Renesas's MCU exposure is a positive.

- Underlying auto demand should be fairly healthy in 2023, and Renesas has multiple program launches on the way, as well as healthy channel inventory.

- The Industrial/Infrastructure/IoT business is looking at a more challenging year given weaker demand across multiple markets, but management is looking to integrated solutions to gain long-term share.

- Renesas is likely facing some elevated miss-and-lower risk over the next couple of quarters, largely driven by industrial end-markets, but the valuation looks appealing for longer-term investors.

Semiconductor stocks are off their lows, but I certainly wouldn’t say that sentiment is particularly healthy – lead-times have started to shrink and companies have started openly acknowledging customers inquiring about pushouts (if not outright cancelations). With declining ASPs likely to push total industry revenue into contraction next year, valuations have retreated to the low end of historical ranges.

Japan’s Renesas Electronics ( OTCPK:RNECF ) ( OTCPK:RNECY ) (6723.T) has been holding up relatively well with respect to reported results since my last update , and the shares haven’t done too badly – more or less keeping pace with peers like NXP Semiconductors ( NXPI ) and ON Semi ( ON ), though modestly lagging Microchip ( MCHP ) and Texas Instruments ( TXN ), and lagging SiC-driven rivals like Infineon (IFNNY) and STMicro ( STM ) more significantly.

At this point I continue to believe that Renesas shares are meaningfully undervalued. Auto chip demand is holding up better and inventories are not particularly robust heading into a year where many OEMs are looking to catch up on deferred production schedules. I don’t ignore the risk of a steeper decline in the non-auto business, but I like Renesas’s leverage to auto MCUs and ADAS, as well as longer-term opportunities in industrial MCUs and integrated solutions, and I think today’s valuation is too low.

2023 Will Be A More Challenging Year For The Industry

Sentiment on the semiconductor space migrated from “it’s different this time” (analysts arguing that the industry had moved beyond its historical cyclicality) to “here we go again” as 2022 rolled on, with the second half of the year seeing the start of contraction in lead-times and the third quarter seeing decidedly more negative guidance. With that, the SOX index sold off meaningfully in 2022 (the worst performance in over a decade).

This year (2023) is going to be a year of normalization, and I expect to see lead-times shrink further as end-user demand cools in many markets, inventories reach more sustainable levels, and prices start to fall. I don’t expect a sharp fall in volumes in 2023, it’s actually rather rare to see meaningful year-over-year volume declines in the semiconductor industry, but much of the gaudy growth reported in 2022 has been driven by pricing, and I believe investors are going to see that pricing leverage largely vanish in most markets in 2023, leading to a modest decline in industrywide revenue.

Not all markets are equal, though, and I think the auto market will hold up better than most. I expect healthy mid-single-digit growth in underlying unit volumes, and I could see a least some sub-sectors of auto semiconductors growing faster on increased unit content.

Renesas generates more than 40% of its revenue from the auto end-market, so this is a relatively benign backdrop for the company heading into this new year. Along those same lines, Renesas is heavily weighted to MCUs within its auto business, and not only have MCUs in general held up better in terms of demand and lead-times, but auto MCUs have led MCUs, with many customers still on allocation. Renesas also has multiple launches and platform wins that will start scaling up, adding a little extra insurance to the underlying business.

The outlook is not as strong for the Industrial / Infrastructure / IoT (or “3I” as a I call it) segment. Like NXP, Silicon Labs ( SLAB ), and most other players in the IoT space, Renesas has seen a notable dropoff in the business, with consumer devices (PCs, appliances, etc.) notably weak. While Infrastructure spending has held up comparatively better and there should still be server growth in 2023, data center spending is definitely slowing and Renesas lacks the exposure to high-end niches (like networking and interconnect) that are likely to hold up better.

Industrial is a harder call, but between the reports from companies like Broadcom ( AVGO ), NXP, Texas Instruments, this category too is starting to crack. Automation and metering spending is likely to slow in 2023, driving weaker demand for MCUs, power, and Renesas components.

Managing The Channel Should Help

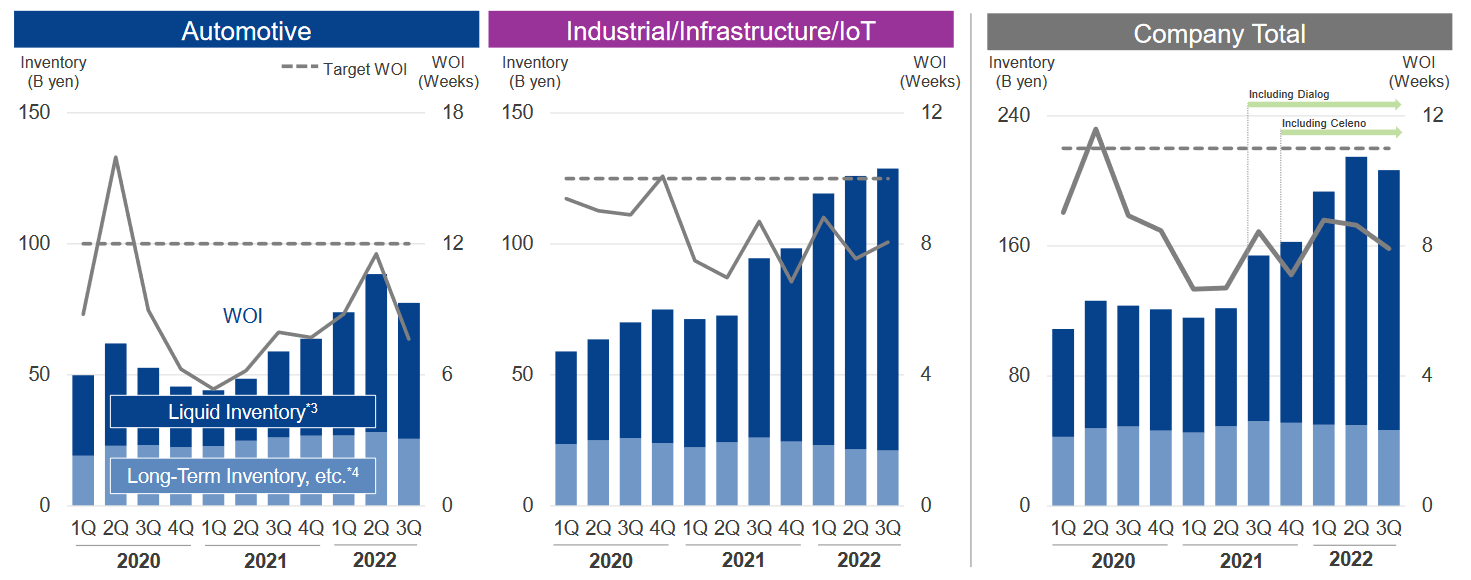

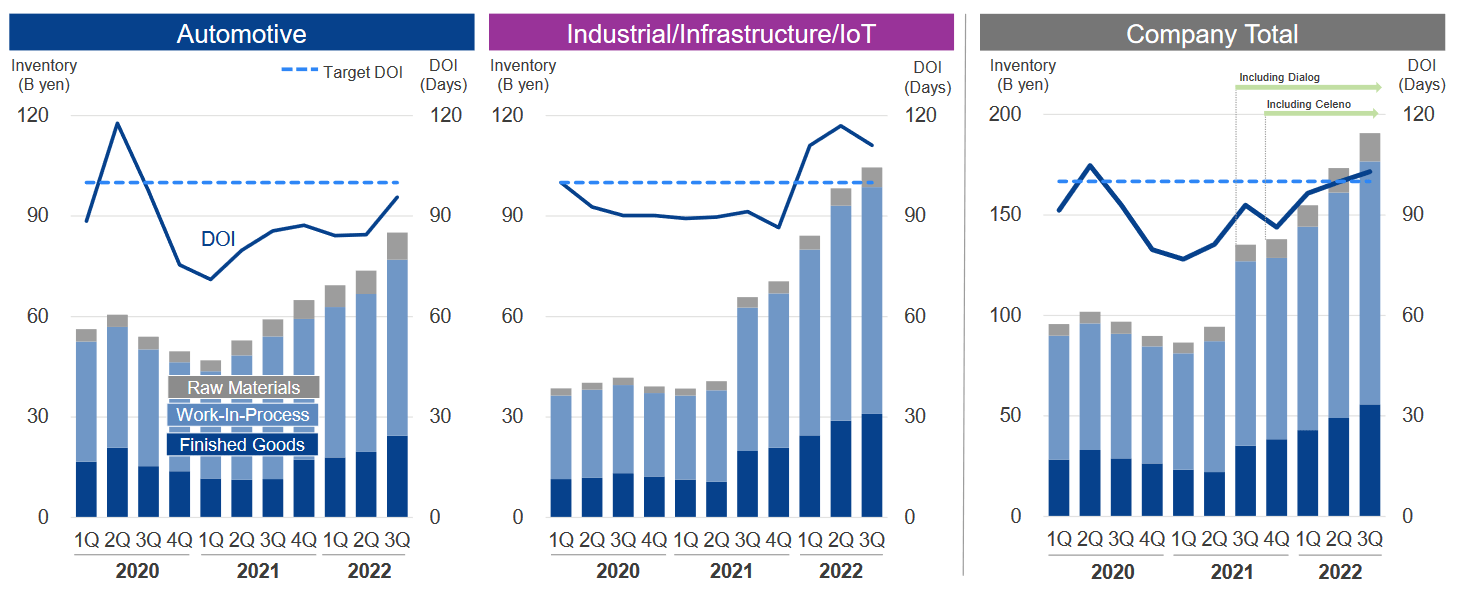

I do think that one of the overlooked positives at Renesas is that, although some of the numbers haven’t looked as good as those at peers, the company seems to be doing a good job of managing channel inventories.

Auto channel inventories are actually well below management’s target, and 3I channel inventory is likewise below target. While in-house inventory is a little high in the 3I business, that’s not the case for the auto business, so I believe Renesas is in good shape with respect to its capacity and end-user demand/sell-through.

{kind=link}

{kind=link}

To this end, I’d note that Renesas guided to a 4% sequential revenue decline in fourth quarter revenue – in line with the guidance from NXP Semiconductors and quite a bit better than the 12% decline forecast by Texas Instruments, though not as strong as the 4% growth projected by Microchip.

Overlooked Growth Opportunities

Renesas has long enjoyed a leadership position in the MCU market, and I think there’s a perception that the company is in a position where share loss is inevitable from here. While competition from the likes of Infineon, Microchip, NXP, STMicro, and Texas Instruments is nothing to ignore, Renesas has by most accounts stabilized share losses seen during the pandemic (due in part to production interruptions and aggressive inventory management) . More importantly, the company enjoys strong share in more highly-valued 32-bit MCUs and has new products lined up using both ARM and RISC-V architectures.

In the auto space, the company has booked numerous wins in ADAS, xEV, communications/networking, and 32-bit MCUs, with these wins scaling up over the next two to three years. Renesas has seen notable wins with integrated solutions that combine MCUs with analog and power chips, an offering that not all of its competitors can match.

While definitely lagging in silicon carbide (or SiC), the company has acknowledged this deficit and indicated that they will be getting more aggressive in building up its advanced power capabilities – whether this will include meaningful M&A remains to be seen, as the company does have in-house capabilities but may look to accelerate the process and augment its capabilities with a strategic buy. Along those lines, I’d note the company recently acquired a small fabless Indian chip company to boost its radar capabilities (important in ADAS systems).

In the industrial business, the company is well-placed to leverage growth in industrial automation and electrification through its MCU and power products, here again with the opportunity to offer integrated solutions. Renesas is likewise well-positioned for higher-function industrial IoT by virtue of its 32-bit MCU capabilities, though improved communication/connectivity abilities would be desirable (another possible acquisition target).

The Outlook

Given a weakening macro outlook for many industrial end-markets, not to mention the weaker IoT results reported by many chip companies in the third quarter earnings cycle, I do see some risk of miss-and-lower performance in the next quarter or two. I’m not as concerned about the auto business. Elevated lead-times in auto and industrial MCUs would normally be a risk factor, but I believe demand will hold up relatively better here (particularly in auto) and Microchip management has talked about the possibility of ongoing capacity shortages here due to a lack of trailing-edge capacity investment.

Renesas’s outperformance in Q3’22 has led to higher numbers in my model, but I’m still looking for a high single-digit revenue decline next year due to pressures in consumer and industrial end-markets. I believe that at this point my FY’23 revenue number is in line with the low end of sell-side estimates and about 7% below the average estimate. I do expect a rebound in FY’24/FY’25, though, and I’m looking for long-term revenue growth of around 3% from FY’22 onward.

Given weaker pricing and ongoing inflationary pressures, as well as some risk of capacity under-absorption and launch costs (including the company’s new 300mm IGBT production), I’m looking for a sizable year-over-year decline in operating margin (more than six points), but I do believe that 30% operating margins can be sustained over time. I’m expecting adjusted free cash flow margins in the low 20%’s, which should drive low-to-mid single-digit FCF growth.

Discounting those cash flows back, I believe Renesas is priced for a low-to-mid-teens long-term annualized total return, which makes it a relative standout in the space. Likewise, even using cycle-low multiples (on top of cycle-low margin, revenue, and EBITDA assumptions), Renesas looks significantly undervalued (40%-plus) on a multiples-based approach.

The Bottom Line

Clearly, the market has a grimmer assessment of the company’s near-term leverage to the auto and industrial end-markets. While I can appreciate at least some of the bear case, including ongoing forex risk, I think that’s more than reflected in the current valuation. I can’t rule out the risk of a quarter or two of miss-and-lower results, but I think long-term investors should consider doing some due diligence on this leading MCU player.

For further details see:

Cycle Worries Weighing On Renesas Electronics And Creating A Bargain Valuation