ASC - d'Amico International Shipping: Best Risk/Reward Product Tanker Company For A Long-Term Hold

2023-11-15 09:13:57 ET

Summary

- d'Amico International Shipping is trading at a significant discount to its Net Asset Value, presenting a potential 40% upside in the short term.

- The company has a strong presence in the maritime industry, specializing in the transportation of refined petroleum products, vegetable oils, and various chemical commodities.

- This last decade has been the best one for the tanker market, with the potential for rates to reach new highs due to low inventories and a low order book.

Investment Thesis

Despite improved fundamentals and an impressive tanker market, d’Amico International Shipping (DMCOF) continues to trade at a huge discount to Net Asset Value ((NAV)). The stock holds promising potential for long-term investors, and I believe shareholders’ return should improve (I see a potential 40% upside) in the short term closing the valuation gap.

d’Amico Story

d'Amico Group , founded by Ciro D'Amico in Italy in 1936, began as a modest shipping company with a primary focus on transporting bulk cargo, particularly wood. In its early years, the company operated relatively small vessels, however, after World War II, D'Amico Group underwent significant expansion. This expansion involved not only broadening its fleet but also diversifying its operations to encompass the transportation of a wide range of bulk commodities. As a result, the company emerged as a highly regarded and well-established shipping company, with a strong presence in the Mediterranean region.

In the 1960s, d'Amico Group underwent a significant strategic shift by expanding its focus to include the tanker segment. This move marked a pivotal moment in D'Amico's history, as it entered the oil and petroleum product transportation. As the late 20th century unfolded, the group continued its impressive growth and global expansion, expanding its fleet to include dry bulk carriers, product tankers, and container vessels.

From the year 2000 onward, the group focused on its core business and extended its global reach by opening new offices around the world, including key locations such as Singapore, Dublin, and Mumbai. In 2007, d’Amico International Shipping, the segment specializing in product tankers, made its debut on the Milan Stock Exchange. Between 2012 and 2019, d’Amico initiated an extensive fleet renewal program, demonstrating a strong commitment to reducing its environmental impact and enhancing fleet efficiency.

Today, D’Amico International Shipping remains a family-owned company, with D'Amico Group maintaining a significant 65.65% ownership stake in the enterprise.

Under the leadership of CEO Paolo D’Amico, continues the family's legacy in the shipping industry. Paolo D’Amico graduated in Economics from Rome University and joined d’Amico Società di Navigazione S.p.A. in 1971, with a particular focus on the product tanker aspects of the business. Over the years, he has held various pivotal roles within the organization and since 2006 he has also served as a director of d’Amico Tankers Limited, the wholly-owned subsidiary of the publicly listed d’Amico International Shipping S.A. Following the company's listing on the Italian Stock Exchange, he assumed the role of Chairman of the Board of Directors at d’Amico International Shipping. Additionally, he is actively involved in several companies that are not part of the d’Amico Group.

Adding to this leadership team is Carlos Balestra di Mottola, who has served as the Chief Financial Officer ((CFO)) since May 2016, and brings a wealth of financial expertise to the company. He joined the d'Amico Group in 2003 and has held several significant roles within the organization. Carlos has a distinguished academic background, having obtained a Master's in Business Administration from the Columbia Business School in New York and before joining d’Amico, worked at the Lehman Brothers investment bank (in the London and New York offices) and at Banco Brascan (in the São Paulo offices, in Brazil).

Business Overview

D'Amico International Shipping, hereafter referred to as DIS or d'Amico, is a renowned player in the maritime industry, specializing in the transportation of refined petroleum products, vegetable oils, and various chemical commodities. DIS boasts a modern and environmentally-conscious fleet designed to meet the evolving demands of the global shipping market.

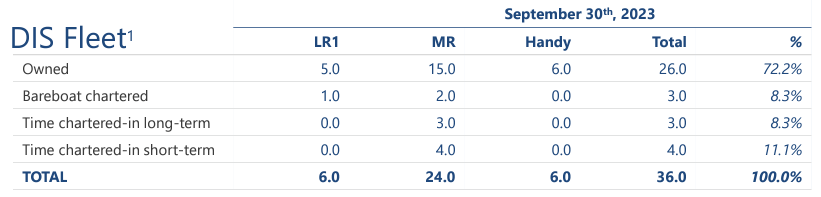

DIS maintains strict control over its fleet, which comprises a total of 36 product tankers. Of these, 26 are owned outright, while seven are chartered in, and three are operated on a bareboat basis.

DIS Fleet (d'Amico Q3 presentation)

{kind=link}

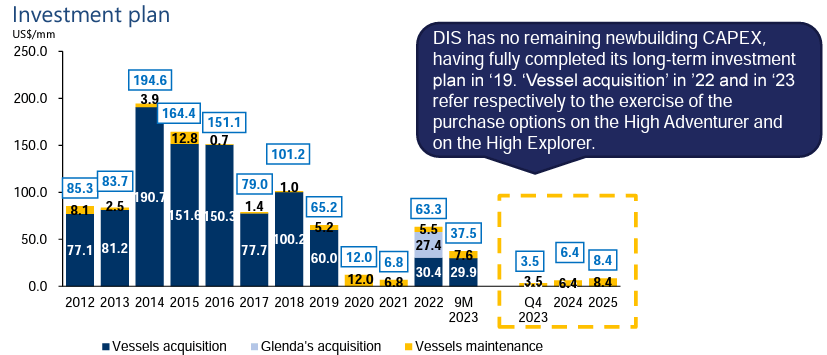

D'Amico has long taken pride in maintaining a youthful fleet, a strategy that aligns with its commitment to environmental sustainability. The company has actively engaged in the sale and purchase (S&P) market, as well as the ordering of new vessels. Notably, between 2012 and 2015, DIS embarked on a significant investment initiative, acquiring 22 vessels with a total investment of $755 million. The fleet received its last newbuild in October 2019, with the delivery of a LR1 scrubber-fitted vessel. Subsequent to this delivery, the company has refrained from new vessel orders, indicating a conservative approach to expansion. Instead, the focus now revolves around the judicious exercise of purchase options on leased vessels.

CAPEX Commitments (d'Amico Q3 presentation)

{kind=link}

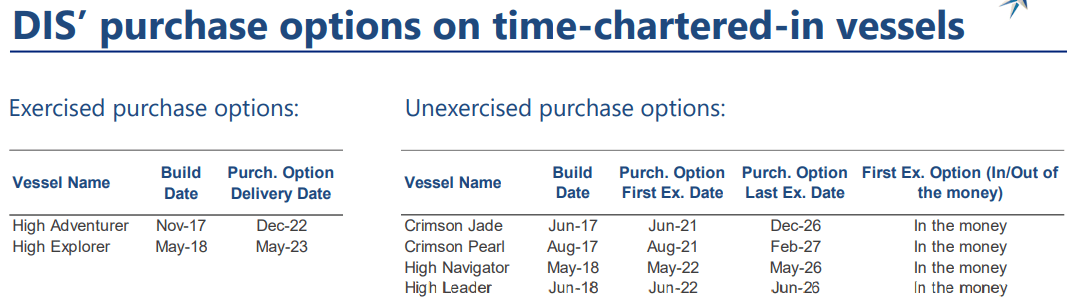

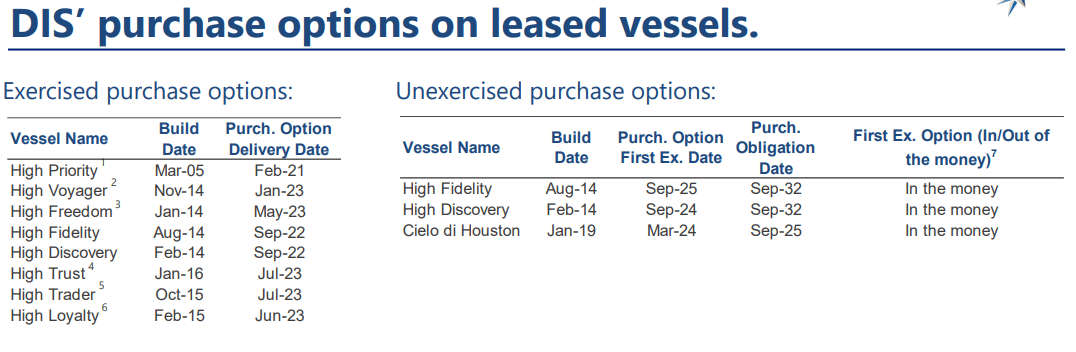

DIS maintains a strategic position by holding flexible purchase options on a substantial portion of its chartered-in and bareboat vessels. Over the last couple of years, D'Amico has exercised 10 purchase options, representing a substantial cash outflow. While all remaining purchase options are currently in the money, management has commented that they currently do not expect to exercise these options, given the highly favorable time charter-in (TC-in) rates and fixed interest rates on the bareboat agreements. As purchase option expiration dates draw nearer, around 2026, they will assess the prevailing market conditions before deciding whether to exercise them. This measured stance allows for better cash flow management and the potential to distribute capital to shareholders in an efficient manner.

d'Amico Q3 presentation d'Amico Q3 presentation

{kind=link}

{kind=link}

An integral feature of d'Amico's operational approach is the maintenance of a high-quality Time Charter ((TC)) coverage book. Management continually adapts the extent of employment day coverage to market dynamics. For instance, in 2020, over 60% of employment days were secured through time charters, whereas in 2022, this figure reduced to 34%. Typically, DIS targets a period of contract coverage of 40% to 60% for the subsequent 12 months, with adjustments according to prevailing market conditions. Currently, owing to the very positive market outlook, d'Amico aims to keep more of its fleet on the spot market, illustrating its agility in seizing opportunities amid dynamic market conditions. In the nine-months ended 2023, 27.9% of DIS’ employment days were ‘covered’ through period contracts at an average daily rate of US$ 27,951.

Product tanker overview

As I have previously discussed in my Ardmore Shipping article , the product tanker market is currently experiencing its most robust conditions in the last decade, with solid fundamentals that indicate sustained strength.

To delve deeper into the information provided, it is worth examining the robust seasonality characteristic of the product tanker market. Typically, the summer months exhibit softer conditions, while there is a substantial improvement during the winter period. As illustrated in the Cleaves Graph, November marks the onset of rate improvements, which then remain elevated until April. Recent data strongly suggests that this year will adhere to the established seasonal pattern as rates have already started moving upward.

MR seasonality (Cleaves Shipping)

The seasonality in the product tanker market can be attributed to two primary factors. Refinery maintenance plays a pivotal role, with October being the month when higher capacities are taken offline. This strategic shutdown occurs just before the anticipated uptick in demand for winter, contributing significantly to the pronounced seasonality observed in November and December.

Refinery Maintenance (STNG Q3 Presentation)

{kind=link}

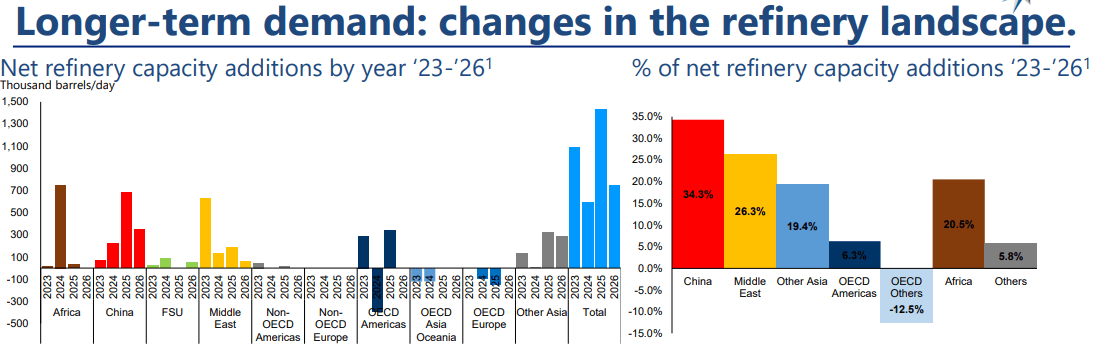

Another positive factor for the long run is the shift in refinery capacity worldwide. Since the onset of COVID-19, older refineries, notably in Europe but also in regions like Australia/New Zealand and the US, have faced challenges with poor profit margins and ESG pressure and have consequently been earmarked for closure. Over the past few years, Europe alone has witnessed the closure of 2 million barrels per day (mbpd) in refining capacity, moreover without access to Russian products, Europe is now expected to turn to sources in the Middle East and Asia, leading to increased demand for long-haul trades.

Refinery Changes (DIS Q3 Presentation)

{kind=link}

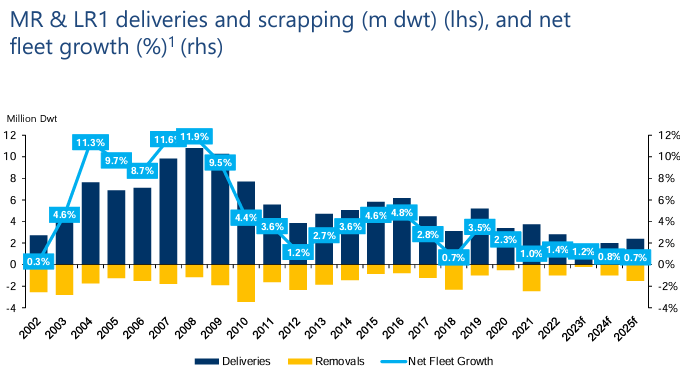

As for the supply side, the orderbook has been on a consistent rise, constituting approximately 10% of the total product fleet. However, there is a notable concentration with a significant portion allocated to LR2 vessels, whereas smaller vessels only account for a 6% share of the orderbook. It's important to note that the majority of these ships are not expected to commence operations until 2025. Moreover, given the substantial demand for containers and gas carriers, vessels ordered in the present day are slated for delivery in 2026 and 2027.

Fleet growth (d'Amico Q3 presentation)

{kind=link}

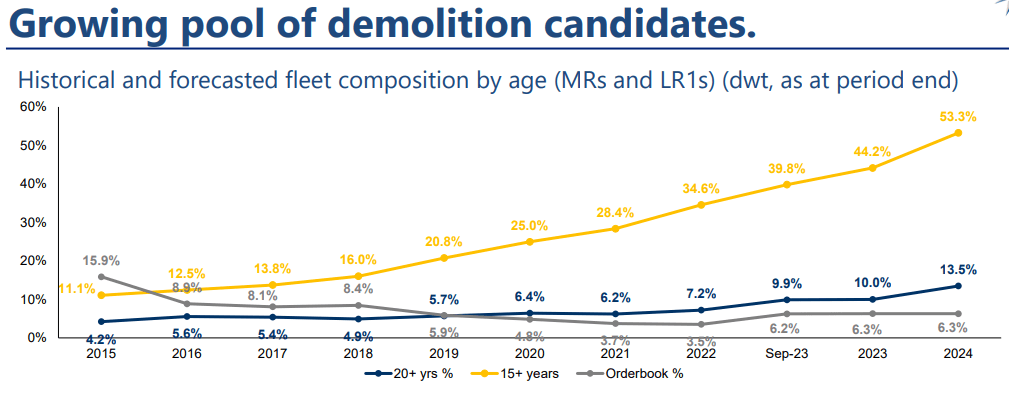

Simultaneously, there has been a notable increase in the percentage of vessels surpassing the 15-year mark, when drydocks are mandatory every 2.5 years instead of 5. This upward trend is anticipated to gain momentum in the upcoming years, driven by the aging of vessels delivered during the super cycle spanning 2003-2008. Additionally, a noteworthy subset of these vessels is of Chinese origin, characterized by comparatively lower quality, thus accelerating their likelihood of being scrapped in the near future.

Fleet composition (d'Amico Q3 presentation)

{kind=link}

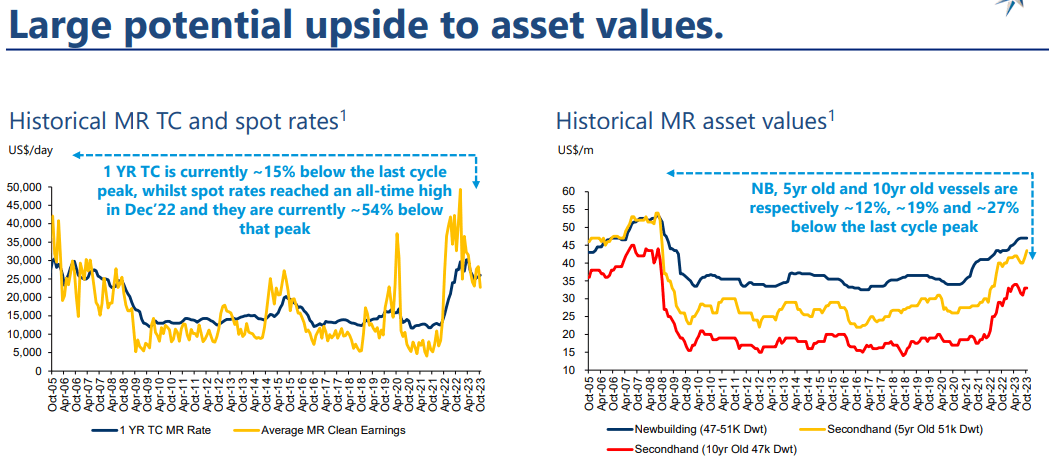

Finally, if we take a look at asset values we can see that there is still some upside left. As illustrated in the accompanying graph, the continuation of robust rates could lead to further enhancements in second-hand values, subsequently bolstering the Net Asset Values ((NAV)) of all tanker companies.

Asset Values (d'Amico Q3 presentation)

{kind=link}

Financial Position & Stock Valuation

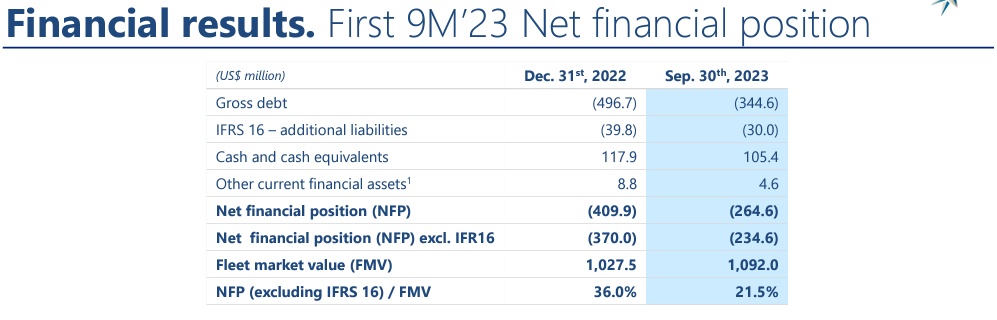

d'Amico Financial results (d'Amico Q3 presentation)

{kind=link}

D'Amico's financial position has undergone a significant transformation in recent years, reflecting a remarkable turnaround. The company's leverage ratio currently stands at 21.5%, a noteworthy improvement from the 60.9% reported on September 30th, 2021. Notably, while reducing leverage is a positive step, I hold the view that maintaining a moderate level of leverage remains important, especially for companies with young fleets. This approach not only enhances returns but also fosters financial flexibility, offering a balanced strategy for sustained success. Management has expressed their comfort with the current leverage but with current strong rates leverage will continue to decrease.

As of the most recent quarter, DIS boasts a healthy cash reserve of $105 million in cash and cash equivalents, ensuring ample coverage for near-term financial commitments. An important reduction in daily average repayments has been observed, primarily due to the prudent exercise of purchase options on leased vessels, which DIS plans to keep debt-free.

Bank repayments (d'Amico Q3 presentation)

{kind=link}

Management has indicated their intent to boost shareholder payouts, and based on their historical actions, current robust balance sheet, and lack of expansion plans, for next year it is reasonable to anticipate a substantial increase. I expect at least 50% of earnings per share ((EPS)), with the potential to reach 75%, depending on repurchases.

d’Amico is one of the few tanker companies that discloses their Net Asset Values.

NAV evolution (d'Amico Q3 presentation)

{kind=link}

As can be seen, d'Amico's shares have consistently traded at a significant discount to their NAV, however, I anticipate this gap to close over time. The product tanker industry faced challenging rates for the better part of the last decade. Nevertheless, with a clean balance sheet, management can now focus their efforts on closing this disparity in valuation.

In the second quarter of 2022, d'Amico initiated a share buyback program, which has been running consistently, with weekly repurchases continuing until the end of September. I anticipate the resumption of these buybacks in the upcoming week. While the buyback pace may seem slow, at approximately 0.1% per week, the cumulative impact over time is substantial. Notably, the company issues a weekly press release to communicate the amount of shares repurchased, serving as a positive signal for investors.

Transitioning to the company's performance, a closer examination of d’Amico's recent Q3 financials reveals a net income of $48.9 million, or $0.40 per share, during what is typically the most challenging quarter. The average Time Charter Equivalent ((TCE)) stood at $30,860 per day.

The Board of Directors has approved the distribution of a gross interim dividend of $20 million, translating to $0.141 per share net. This represents approximately 35% of the earnings per share, a positive move in the right direction, though further progress is still required.

Looking ahead to Q4, d’Amico has secured 33% of its employment days on spot voyages at an estimated daily average of $29,820. Considering the contract coverage, 66% of Q4 employment days have been fixed at $28,869/day. If the remaining 33% of free days are fixed at $35,000/day, a very conservative assumption, DIS would achieve a blended TCE of about $31,000 for the quarter and an EPS of around $0.45 per share. Further improvements in rates could easily push EPS to $0.50.

Year-to-date, EPS stands at $1.22, by year-end they should achieve at least $1.7/share against the current stock price of $5.60. Assuming a 50% dividend, $0.85/share, the yield would be approximately 15%. Considering the positive product market outlook, next year's results may match or even surpass this year's.

Taking all factors into account, I am inclined to believe that d’Amico's stock should trade around its Net Asset Value. This suggests a potential upside of around +40% just to reach the current $7.85 NAV. If market rates remain robust, the NAV is poised for further growth.

Finally, another positive development that should help valuation is d'Amico's application for membership in the OTCQX Best Market, with expected admission by year-end. This step represents a notable improvement, as the OTCQX offers U.S. investors a more transparent, liquid, and efficient cross-trading alternative compared to the OTC Pink market. It's important to note that D'Amico's primary listing remains on the Italian stock exchange, but this addition provides a valuable alternative avenue for U.S. investors, particularly in cases where some U.S. brokers may not facilitate the purchase of DIS shares on the Italian market.

Risks

Recession or demand destruction. Product tankers move the marginal barrels, so a small reduction in consumer demand can have a big impact on tanker demand. If high oil price and the dollar continue their trend higher, it could affect demand.

Orderbook: the actual orderbook is manageable but if it continues to climb much more, it will be a risk for long-term outlook.

Another huge Investment Plan. D’Amico is a family business and must continue to invest in the future. Some S&P or new builds are normal but a huge investment plan as the 2012 one will be a big negative. Management has stated no desire to do it, so this should not be a huge risk.

Conclusion

d’Amico is one of the cheapest product tanker companies and with a management team that understands capital allocation policies and is committed to long-term shareholder value maximization, I believe the company is well positioned for generating substantial returns. I see a potential 40% upside to the share price, which could close the NAV gap in a matter of months. d’Amico is a rare choice for a long-term hold, provided management sustains its performance and the market conditions remain robust.

For further details see:

d'Amico International Shipping: Best Risk/Reward Product Tanker Company For A Long-Term Hold