TMHC - D.R. Horton: A Robust Bet In The Shifting U.S. Home Market

2023-12-13 23:07:38 ET

Summary

- D.R. Horton demonstrates strong adaptability in the fluctuating housing market thanks to its dynamic pricing strategy.

- Despite increasing mortgage costs, the company succeeded in increasing its sales by 8%.

- Efficiency improvements stemming from a shift to a capital-light business model unlocked significant capital, boding well for its cash flow metrics.

Investment Thesis

D.R. Horton ( DHI ) stands out as a solid investment in the US homebuilding industry. They have consistently demonstrated an ability to navigate shifting housing market trends, a crucial factor in an industry often subject to economic fluctuations. Despite rising interest rates and inflation, DHI's sales are up 8% this year.

The current housing market, marked by a tight supply, offers accommodative tailwinds going into 2024 despite high interest rates. Today (Wednesday, 13 December,) the Fed announced it is maintaining its wait-and-see approach to monetary policy for the second consecutive meeting. After a period of rapid interest rate hikes, this shift towards policy normalization allows consumers to adapt to the higher-for-longer regime. DHI's order cancellations are down from 2022 peaks, and new orders are up. The combination of these trends and a supportive macroeconomic climate, underscored by the resilience of the US economy, tight labor market, and GDP growth, reinforces our bullish stance on DHI as we approach 2024 despite higher mortgage costs.

The House Market Is Stabilizing

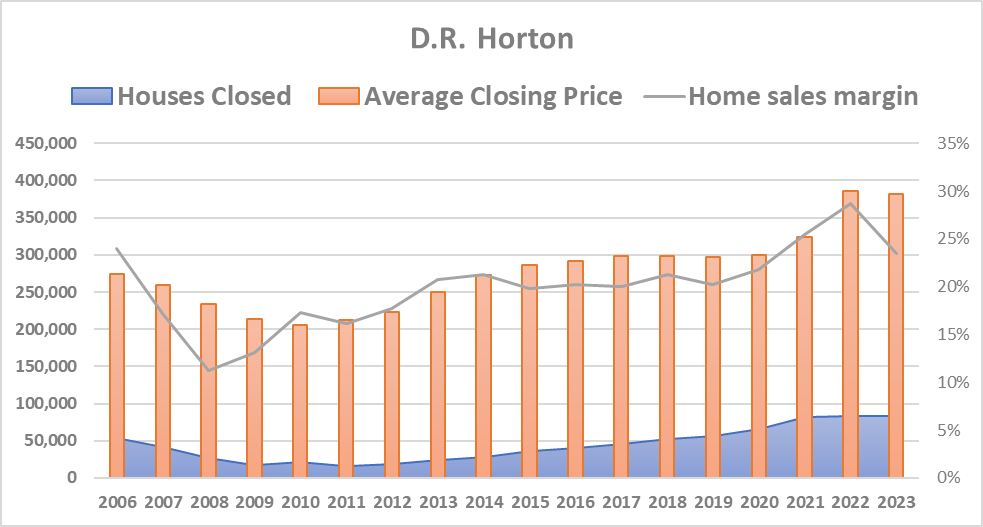

Despite high mortgage rates and inflation, DHI's recent performance has been exemplary. Revenue rose 9% in the September quarter. Although net income dropped slightly, it is still above Wall Street consensus, and more importantly, it aligns with its dynamic pricing model and strategic focus on maintaining volumes and market share, a critical buffer in the face of ever-changing market demand, as shown in the chart below.

DHI. Graph created by the author.

{kind=link}

DHI closed 82,917 homes in fiscal 2023, almost unchanged from last year's 82,744 units. The average price per unit stood at $381,600/unit, slightly down from 2022's $385,100/unit. Home sales margins declined from 29% to 25% YoY but are still above the historical average. These dynamics entail that DHI bore the brunt of inflationary pressures instead of passing costs to clients, mirroring their focus on maintaining market share and volumes. This volume stability translates to better communication with suppliers and contractors, a critical factor that rose to the surface recently as material shortage, inflation, and tight labor market impacted the sector's operations. With lumber prices falling and supply chain issues subsiding, these conditions support our positive outlook on the company. The recovery in new home orders also shows that consumers have adapted to high interest rates. New home orders increased by 39% in Q4 2023, supporting this conclusion.

Growth-Oriented Home Builder

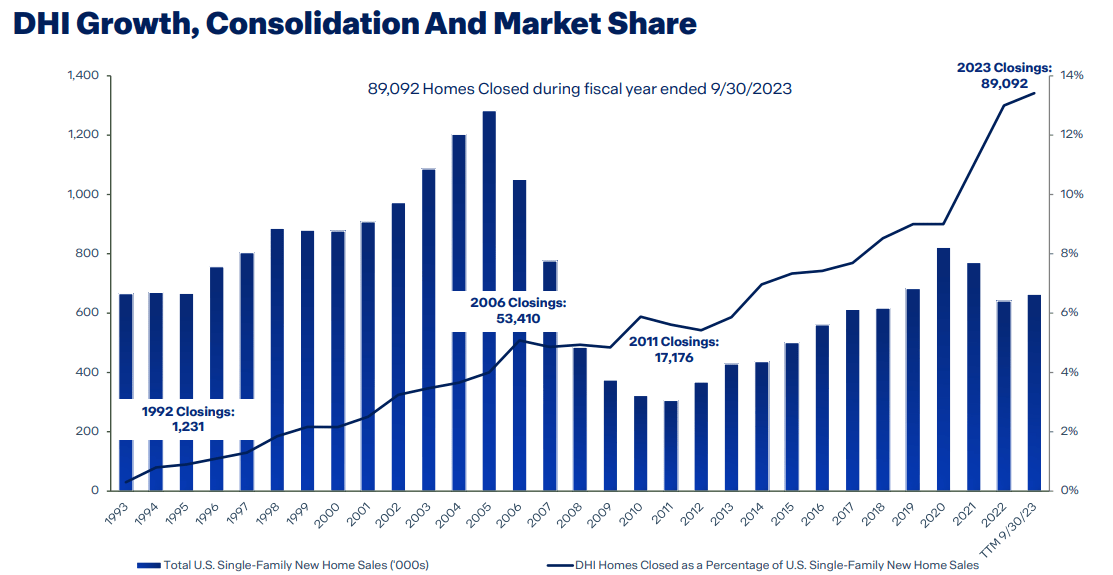

DHI has shown remarkable growth and market leadership over the years. Since 2009, the company has expanded its operations from 36 markets to 118. More notably, DHI's leadership position has seen a significant uptick. From being the top player in just seven markets in 2009, the company has progressively increased its dominance, leading 15 markets by 2015 and now holding the market leader position in 55 markets.

Moreover, DHI's focus on affordable housing, with an average selling price of 381,600 in FY 2023, strategically positions the company to attract customers adjusting to rising mortgage rates by opting for more budget-friendly homes. This alignment with current market needs and trends boosts our confidence in DHI's ability to sustain its growth momentum going into 2024.

{kind=link}

Robust Balance Sheet

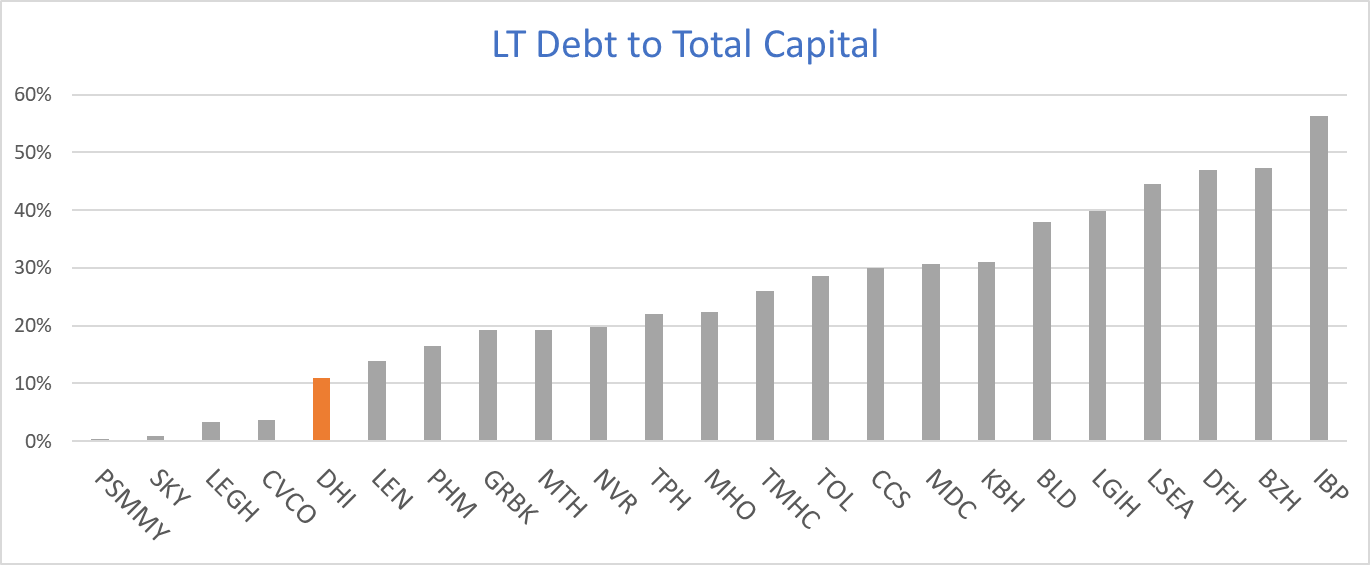

Capital-intensive companies often maintain high leverage ratios, given the extensive capital requirements needed for operations. DHI, on the other hand, has net zero debt with a cash balance of $3.7 billion, exceeding its long-term borrowing of $3 billion. Its Long-term Debt-to-Capital ratio is about 10%, one of the lowest in the sector. These numbers position DHI favorably when compared to industry peers.

Seeking Alpha. Graph created by the author.

{kind=link}

In Q4 '23, DHI generated $2 billion in operating cash flow, its highest on record, bringing total operating cash flow for FY 2023 to $4.3 billion, a significant increase from the $550 million average in the past two years. The company attributed this performance to inventory management improvements. In the past years, DHI has been transitioning into a more capital-light model, emphasizing land purchase options instead of outright purchase, thus unlocking capital. Therefore, the improvements in operating cash flows are not a one-time spike. Management expects FY 2024 operating cash flow of $3 billion, citing their strong order book, operational efficiencies, and faster inventory turnover.

Shareholder Returns and Valuation

DHI currently trades at a 10x PE ratio, which is quite attractive on a standalone basis. Compared to peers, it stands at a midpoint. However, when considering its market position as the largest US homebuilder and the fact that it is one of the only four among its peers listed on the S&P500 ( SP500 ) index, a factor that enhances its visibility and liquidity, its price seems advantageous even compared to other players with lower valuation ratios, such as Green Brick Partners ( GRBK ), KB Home ( KB ) and Taylor Morrison ( TMHC ). Moreover, DHI has a more diversified operational footprint than smaller peers, decreasing risks stemming from regional economic variations, which also warrants a premium.

Augmenting DHI's attractive valuation is a shareholder-friendly dividend and repurchase program. In 2017, DHI initiated a share repurchase program, which has since resulted in a 13% decline in shares outstanding. In recent years, the company has been accelerating its shareholder capital return policies, buying back 3% of total shares outstanding in FY 2023 alone.

The company's dividend policy is a bit more modest, with a pay-out ratio below 10%, reflecting a prudent capital allocation strategy that ensures the company has an adequate cushion to maintain and grow its dividend distributions throughout different economic cycles. This year marked the 10th year in which DHI grew its dividend after the board approved a 20% increase.

How I Might Be Wrong

As a cyclical stock, DHI's performance is particularly sensitive to broader economic shifts. While the risk is low, the company's pricing strategy that helped it maintain volumes, inventory cycles, and cash flow metrics might not be enough to fully mitigate the impacts of severe economic downturns.

Additionally, rising land costs, which increased by 11% this year, pose a challenge. If this upward trend continues, it could pressure working capital and potentially affect DHI's ability to sustain its share repurchase program and dividend growth, both key aspects of our bullish stance. Moving forward, monitoring land prices for significant volatility will be crucial, as will keeping an eye on overall economic conditions.

Summary

DHI's strategic focus on affordable housing, coupled with a strong balance sheet and impressive operational efficiency, positions it favorably in a market grappling with high mortgage rates. The company's ability to adapt to market dynamics, reflected in its stable sales volume and revenue growth, aligns well with the current housing demand trends. As we move into 2024, DHI's diversified market presence, capital-light business model, and commitment to shareholder returns underpin a promising outlook. This blend of resilience, growth, FCF improvements, and shareholder-friendly capital allocation policy makes DHI a compelling investment choice despite economic uncertainties.

For further details see:

D.R. Horton: A Robust Bet In The Shifting U.S. Home Market