MHO - D.R. Horton: Beating Estimates Again

2023-11-08 01:44:37 ET

Summary

- D.R. Horton continues beating analyst estimates in revenues, margins, and earnings per share.

- Its mortgage division handled the financing for 76% of D.R. Horton's home buyers, increasing from 69% last year.

- The management will continue to return capital to shareholders through share buybacks and dividends, which have been increased by 20%.

- DHI has competitive advantages such as scale, geographical diversification, centralized control, and long-term relationships, contributing to its market share growth.

D.R. Horton, Inc. (DHI) has exceeded consensus estimates again in Q4 2024 , as it did in all the previous quarters during the year, demonstrating how the current shortage in the U.S. housing market can provide construction companies with higher margins for longer than expected.

{kind=link}

The company has reported earnings per share ((EPS)) of $4.45 per diluted share for its last quarter of the year, while the consensus expected $3.93, beating it by 13%. Revenues have increased 9% YoY to $10.5B and the number of homes closed has increased during the year while prices remain high because of the housing shortage.

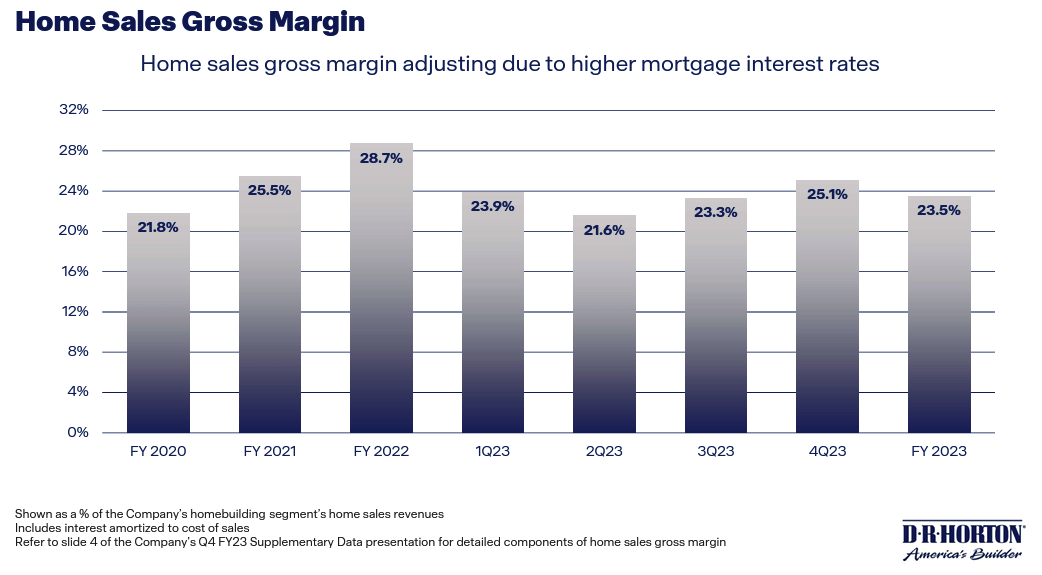

DHI has also surpassed expectations on gross margins due to higher stability on interest rates and higher sales prices, but management has stated during the earnings call that they are expecting it to decrease during the next quarter.

Since I stated my view on the U.S. housing market in my recent NVR article and nothing has significantly changed since then, I am not going to repeat myself on the market conditions but will focus on DHI's performance over the last quarters and its expected performance.

Company Overview

DHI has a great history of entrepreneurial success. Founded by Donald R. Horton in 1978, who constructed his first home in Fort Worth, Texas, and scaled the company over the years until it became the largest U.S. home builder with over $40B in market cap.

Its main business is the construction and sale of single-family homes (91% of home sales ) at affordable prices (68% of homes are priced under $400,000) but also has smaller operations in the multifamily segment, rentals, mortgage financing, and title agency services through DHI Mortgage.

Despite operating in a relatively fragmented industry with low barriers to entry, DHI has achieved great success by offering a wide range of products, focusing on customer satisfaction, and adapting to the demand of each market while maintaining a strong financial position.

Source: D.R. Horton Q4 2023 Investor Presentation

{kind=link}

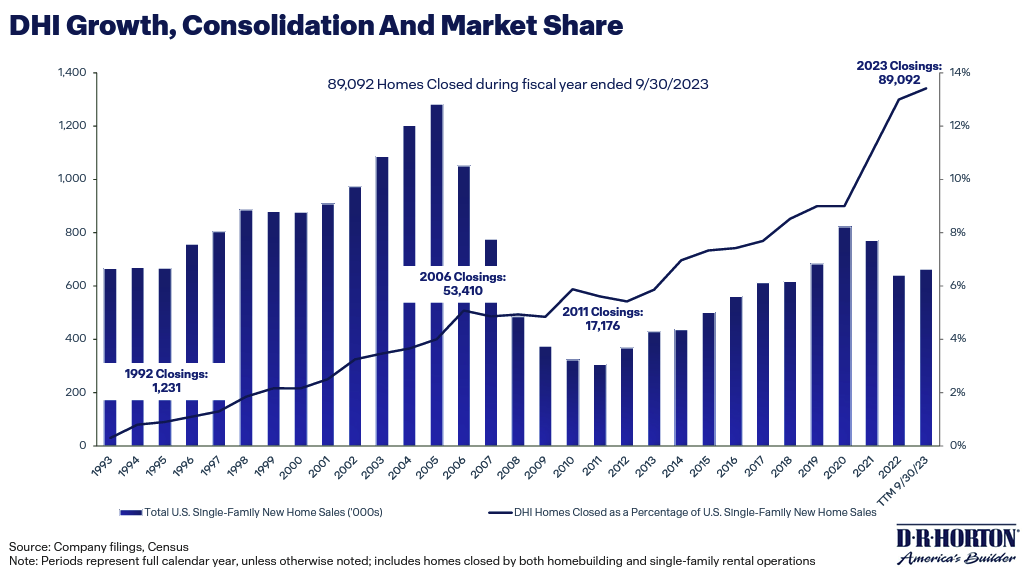

Its growth strategy has been focused on expanding into new geographic markets while gaining market share in existing markets through a high reinvestment rate of its operating cash flows and strategic acquisitions.

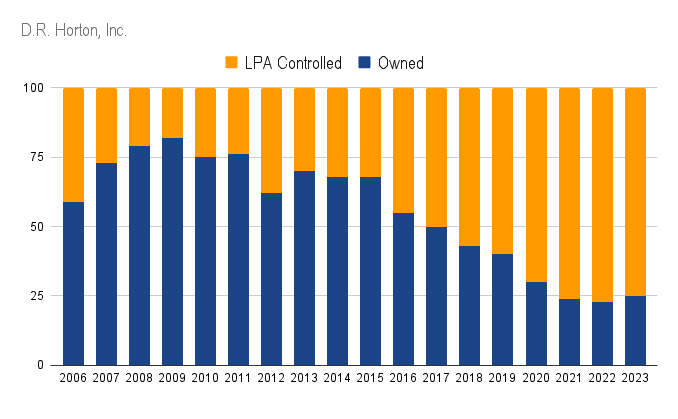

Since the great financial crisis, which had a huge impact on DHI's business when the stock plumbed 91% from peak to bottom, the company has been increasing the portion of land controlled through land purchase agreements ((LPA)) instead of direct ownership.

Source: Author (Data from D.R. Horton's Reports)

{kind=link}

Competitive Advantage

D.R. Horton has been gaining significant market share over the years (currently at >13% in single-family new homes), and I believe this brings some competitive advantages such as:

- Scale: Access to greater amounts of capital at lower costs than its competitors, volume discounts from suppliers, and SG&A leverage.

- Geographical diversification: By operating in 33 states and 106 markets, the company reduces its concentration risk and mitigates the effects of local and regional economic cycles while enjoying greater opportunities to deploy capital.

- Centralized control: despite operating through a decentralized structure with local management teams with better knowledge of the local markets, these are relieved from some tasks such as financing, cash management, capital allocation, legal, and other administrative tasks that are conducted by the corporate offices.

- Long-term relationships: after 45 years in the business, D.R. Horton has built strong relations with land developers, municipalities, landowners, subcontractors, and suppliers.

Leadership Transition

Since October, Paul J. Romanowski (age 52) has become the new CEO and President of DHI after working in the company since 1999. He studied for a bachelor of business administration and worked for M/I Homes, Inc. ( MHO ) before joining DHI as a Division President of South Florida's Division.

Until his promotion to CEO, he was serving as Executive Vice President and Co-COO and had a base salary of $500,000, while receiving total compensation of $13.7MM in 2022 and holding 146,185 shares of the company.

I do not doubt his ability to continue creating value for shareholders due to his extensive experience in the business, but I don't fully like DHI's compensation structure.

Excluding Donald R. Horton, all directors and executive officers as a group hold about 0.4% of outstanding shares, which I consider to be relatively low, and despite most of the compensation being based on performance, 60% of performance-based compensation is received in cash and only 40% in equity.

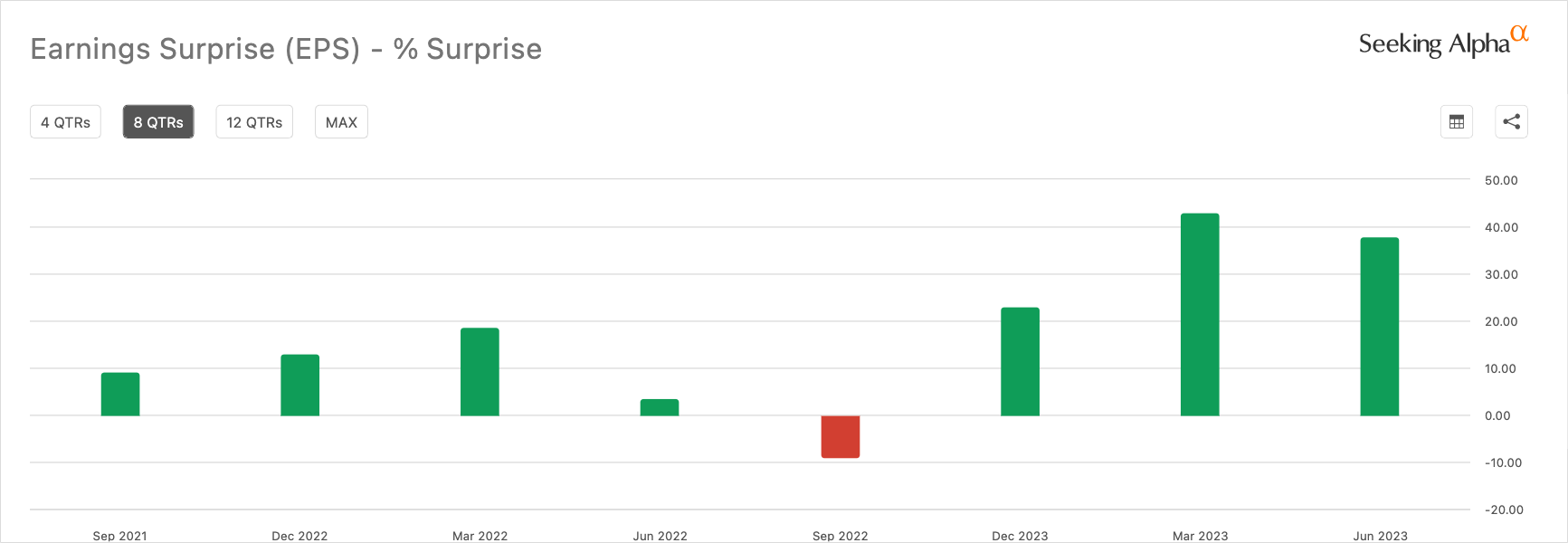

Beating Consensus Estimates

DHI has been beating the consensus estimates over the four quarters of the 2023 financial year and the company is in a good position to continue delivering despite the high interest rates due to its strong focus on affordability.

Firstly, it is important to note that the company had abnormally high margins during 2021 and 2022 because of the fast increase in home prices and the housing shortage in the U.S. market, so a decrease in EPS was already expected.

Source: D.R. Horton Q4 2023 Investor Presentation

{kind=link}

Even though gross margins have significantly decreased from the previous year, we can see a positive trend over the last two quarters and EPS has only decreased 5% in 4Q YoY to $4.45 per share, while revenues have increased by 9% YoY to $10.5B.

For the full year, EPS is $13.82 per diluted share, a 16.3% decrease compared to 2022 but beating analyst consensus estimates ($13.28) by 4%, and delivering a record of 89,092 homes closed during the year.

Also, one of the most positive aspects is the increase in mortgage originations. In 2022, only 69% of the homes closed were financed by DHI Mortgages, while during this last quarter, the rate has increased to 76%, which is highly positive since it is the highest margins segment of the company with EBT margins at 38.9%.

The fastest-growing segment during the year has been the rental operations, which started as a small segment of the company and is already generating $2.6B in revenues and pre-tax income of $524.2MM, compared to $510.2M during 2022.

Despite the positive results, I'd like to highlight some negative aspects:

- Reinvestment rate has reduced significantly over the year, which should affect future growth rates. Cash from operations has increased from $561.8MM in 2022 to $4.3B, but when adjusted for change in net working capital, it has reduced from $6.18B in 2022 to $5.04B.

- Completed but unsold homes have increased to 7,000 from 4,400 a year ago.

- The backlog of homes under contract has decreased by 23% from the previous year.

Capital allocation

Given the positive results during the year and the strong balance sheet, the management has decided to increase its quarterly dividend by 20% to $0.30 per share. At the same time, DHI has reduced the outstanding share count by 3% during the year, allocating $1.2B in share buybacks ($423MM during Q4 2023).

Debt

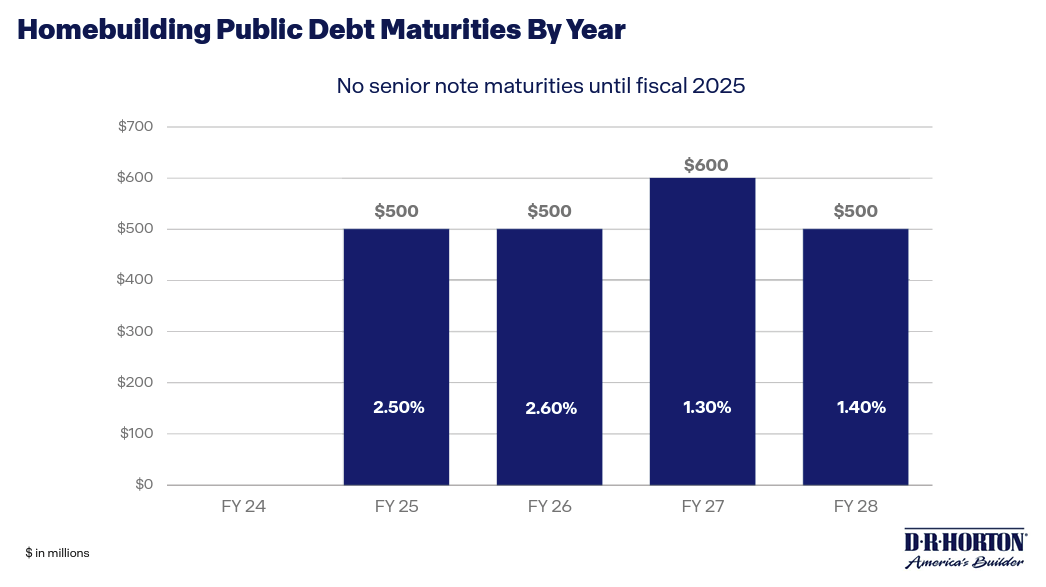

DHI has delivered the lowest consolidated leverage in the history of the company and has reduced its long-term debt by almost $1B YoY while increasing its cash position to $3.87B as a result of the lower reinvestment rate.

Its long-term debt totals $5.1B, with no senior notes maturing until 2025. As shown in the image below, the company has an incredibly low cost of debt.

Source: D.R. Horton Q4 2023 Investor Presentation

{kind=link}

Expected Growth

The first quarter of DHI's fiscal year (September to December) tends to have the lowest revenues and net income contribution to the yearly results, and the management is expecting to generate revenues of ~$7.5B, a 3% increase compared to the previous year, which I believe is highly positive given the slow-down on inflation .

Regarding gross margins in the home sales segment, they are expected to decrease compared to last quarter to between 23.7% to 24.2% but in line with Q1 2023 margins.

For the full 2024 year, management is not guiding on margins, but from the comments on the earnings call and the recent stability on margin decline from 2021 and 2022, I would expect a slight decline.

I expect revenues in line with management expectations for the next year ($36B to $37B) since I believe the U.S. housing market is highly undersupplied and despite the increase in interest rates, DHI's revenues are mainly low-price homes.

The company will continue returning its cash flow via share buybacks ($1.5B) and dividends ($400MM) during the next twelve months.

Valuation

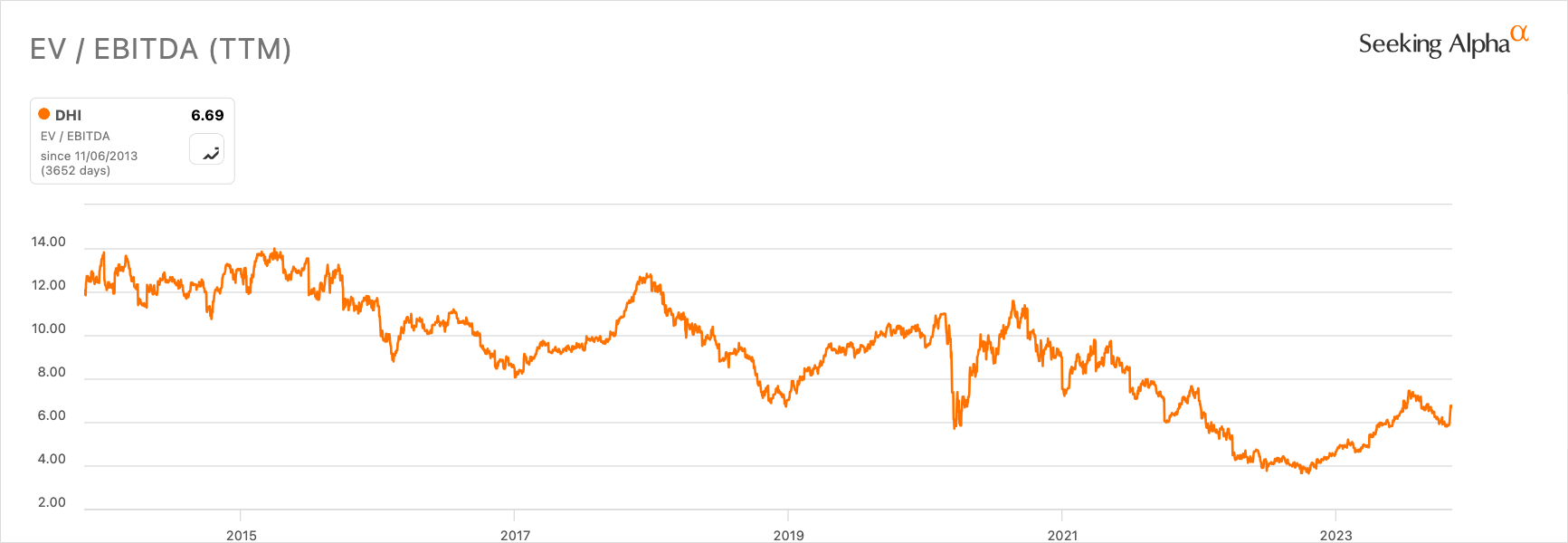

DHI is trading in its low valuation range at a last twelve months EV/EBITDA multiple under 6.5x, implying the market is expecting its earnings to decrease over the next years.

{kind=link}

For the full 2023 year, EBITDA margins have decreased to 17.8% from 21.7% in 2022. If margins continue decreasing to 17% in 2024 and revenues are in line with management's guidance, EBITDA would slightly decrease to $6.2B.

I don't expect DHI to continue profiting from the inflationary pressures as in previous years, but as interest rates decrease over the next years, the demand for new constructions should increase given the low housing inventory .

For the next year, even if the valuation remains under its 10-year average but increases to 8x EV/EBITDA, DHI could increase its market cap to $49.6B.

Given the 3% share reduction per year, it would represent a share price of $150 at the end of 2024 assuming the company has 329MM shares outstanding.

Risks

The main risk I see for DHI would be a rapid deterioration in macroeconomic conditions with an increase in unemployment while interest rates and inflation remain high. In this situation, despite the shortage in house inventory, the market would be supplied with already existing homes, which would have an impact on prices.

Also, high inflation with lower demand would pressure DHI's margins significantly due to an increase in construction material prices.

Given that DHI has $22.3B in inventory, a decline in home prices would cause impairment losses. One aspect that I believe has improved significantly DHI's position is the transition from direct ownership to land-controlled through LPA, so the consequences would be softer compared to the great financial crisis.

During 2008 and 2007, inventory impairments were $2.5B and $1.3B respectively, compared to inventories of $4.6B and $9.3B, but I don't expect this situation to repeat even in a similar environment, given the company used to own 75% of the land directly, compared to the current 25%.

From the interest rates perspective, the pain would come from decreasing demand, since the company sells its mortgage originations to third parties, mainly Freddie Mac or Fannie Mae.

Conclusion

D.R. Horton is well-positioned to benefit from the housing shortage as the supply of both new and existing homes at affordable prices remains limited, and the company has exceeded analyst consensus expectations for the fourth consecutive quarter.

The company has reduced its exposure to a drop in home prices by transitioning its land ownership model, has a strong financial situation, and enjoys competitive advantages due to its size.

Despite some negative signs in its latest reports such as an increasing inventory of finished homes unsold, and a decrease in reinvestment rate and backlog, I believe the company could outperform the market given the cheap valuation.

Even with a further decrease in margins over the next year, I expect the company to provide its shareholders with a 20% increase in price over the next year plus a 1% return from dividends.

For further details see:

D.R. Horton: Beating Estimates Again