LGIH - D.R. Horton: Well Equipped Market Leader Positioned To Overcome Macroeconomic Pressures

Summary

- Regardless of the macroeconomic tailwinds, D.R. Horton is a great company to own.

- I believe there is a clear value opportunity as the company continues to deliver outsized returns.

- Lagging indicators of success will not shine through until later.

The Current State Of Affairs

D.R. Horton ( DHI ) is the largest homebuilders in the United States, with a strong track record of revenue and earnings growth. The company has a diversified geographic presence, which helps to mitigate the risks associated with a downturn in any one specific housing market. During COVID-19, the company entered smaller markets and become leaders in those territories. They have a strong balance sheet and a history of consistently paying dividends to shareholders. I believe that there is an opportunity to buy the company and hold for 5-10 years.

The company benefits from a decentralized structure, whereby “division presidents” have power to make executive decisions in the market that they are based. Division presidents receive performance-based compensation if they achieve targeted financial and operating metrics for their division.

Advantages (Moats)

Because of their scale, each operating division benefits from:

- Greater access to and lower cost of capital, due to their balance sheet strength/ lending & capital markets relationships

- Volume discounts and rebates from national, regional and local materials suppliers and lower labor rates from certain subcontractors;

- Lastly, enhanced leverage of general and administrative activities, which allows them to adjust quickly to changing market conditions.

{kind=link}

Homebuilding Industry Results (Capital IQ); data as of 27/01/2023

As you can see from the table above, the market is pricing in the risk of rising mortgage rates and the prohibitively expensive nature of housing that is occurring and will continue in the near future. All the big homebuilders in the US are being affected by this and it is causing higher than usual Greenwald Ratios (Net Income/Market Cap).

You might see a table like this and consider other options, for instance the Lennar Corporation (NYSE: LEN ) looks very attractive, but they do not generate the same amount of Cash as DHI and have worse margins. DHI also has a ridiculous ROE of 31.3% per latest data, the smaller companies like PulteGroup (NYSE: PHM ) and NVR (NYSE: NVR ) do not have the same growth rates as DHI and the last two companies, although significantly undervalued, did not strike my interest as DHI is the market leader and I would rather invest in the largest company in an industry as opposed to smaller ones. (in general)

For the Q1 2023 DHI reported a consolidated pre-tax income of $1.3 billion with a 3% increase in revenue and a pre-tax profit margin of 17.5%. The homebuilding return on inventory for the trailing 12 months ended December 31 was 39.5%, and the consolidated return on equity for the same period was 31.5%. However, the company has seen a moderation in housing demand due to affordability challenges such as high mortgage rates, inflation, and economic uncertainty. Despite this, the company closed over 17,000 homes and sold more than 13,000 homes in what is typically the slowest quarter of the year. They have seen increased sales activity in January and believe they are well positioned to navigate the current market conditions with their experienced operators, affordable product offerings, flexible lot supply and strong supplier relationships. The company also has a strong balance sheet, liquidity and low leverage which provides them with significant financial flexibility to optimize returns, consolidate market share, and generate increased cash flow.

Net Income for the quarter decreased 16% on a 3% increase in revenues which was $7.3 billion. The main reasons for this were supply chain issues and increased costs for materials. In the early months of 2022 Lumber prices peaked and so the costs (to the homes) were only reflected in the later months of 2022. This makes sense as homes aren't built overnight. The Net income margins compressed as DHI decided to lower the prices of homes sold in general to get rid of inventory that had not been sold. In the Q1 earnings call they also said the following, “We feel very good about our inventory position. And through the last 3, 4 quarters, we limited sales to better align inventory cost, demand and our ability to deliver.” So, they have actively slowed down sales (coupled with lower demand in general) to avoid overbuilding which would then cause a lot of issues with regards to the supply chain, logistics and labor issues that the market is enduring.

How to Deal with Increasing Interest Rates

In my mind a lot of the stereotypical ways to address increasing interest rates are exactly what DHI are currently doing:

Increase marketing and sales efforts: DHI have increased SG&A spend particularly in the smaller markets that they joined and became market leaders in (think rural areas). They joined these areas mainly after Covid-19 to become dominant forces in those areas, knowing that there was a growing trend of people moving out of the cities. They are relatively aggressive with this strategy For instance, they spent $107 million to buy Riggins Custom Homes , one of the largest builders in Northwest Arkansas.

Cost-saving: The company is continually negotiating with suppliers, so it is safe to assume they will do well here considering their bargaining power. Furthermore they have slowed down their actual home building in order to sell more of their homes that have already been built.

Wide product offerings: It will be hard for DHI right now to adjust their marketing spend and building efforts, but going forward in this new environment they will most likely sell more cheap homes at a profitable price point, they just need to weather the storm and we are relying on them to be perspicacious managers here.

Offer different financing options: They are already doing this through their affiliate services . They elaborated on this strategy in the Q1 Earnings call “We are continuing to offer mortgage interest rate locks and buy downs and other incentives to drive traffic to our communities, and we are reducing home prices where necessary to optimize the returns on our inventory investments.”

Valuation - My Subjective Hypothesis

{kind=link}

The above table of my calculations are somewhat subjective, with all amounts listed in USD. The thinking here is we are trying to find out how valuable DHI would be if you take all the assets and strip away liabilities 10 years from now, aka the NAV (Net Asset Value) or Equity of the company. The 18.3% growth rate we assume for 2022 is the previous 5 year revenue CAGR.

We then take the Opening NAV + NPAT + Dividends = Closing NAV

The cost reflected as $33,244 million represents the market cap at time of writing (27/01/2023). From 2023 onwards I have assumed a 13% growth rate just because I believe the 18.3% isn't sustainable, and I am aware 13% is quite aggressive in itself but bear with me. And so the same process follows all the way through to 2032, where we see the following:

Total dividends paid in the 10 year period: $7.1 billion

Closing NAV: $146.9 billion

Closing Market Cap: $236.4 billion

The closing market cap was calculated by using the following dataset:

{kind=link}

P/B industry (Capital IQ)

So we take the final NAV and x it by the 1.7 which then gives us our market cap of $236.4 billion. All of this leads us to the most important part of this exercise, which is the Returns we can expect:

Financial Output (Author's Calculations)

The market return CAGR is the expected stock market return we would receive yearly assuming the final market cap ($236.4 billion) + Total Dividends Paid ($7.1 billion) in 2032. This takes into account our capital appreciation and then all the dividends we receive during the period

The Intrinsic Return CAGR is the expected return we would get assuming the closing NAV ($139.7 billion) + Total Dividends Paid ($7.1 billion). This part of the equation is to see our return if we ignored capital appreciation and were private investors.

This then averages out to a 19% average return for the 10 year period, which is an amazing result. I am 100% sure any investor would gladly accept a return like that! This calculation is relatively subjective, so let's look at the facts.

Valuation - Financial Track Record

{kind=link}

Financial Ratios (Capital IQ) (2000 represents LTM figures, and every prior period is represented accordingly)

Key Takeaways:

- D.R. Horton have done an excellent job of paying down debt, while growing their return on equity brilliantly.

- Their margins have drastically improved and are generating more sales with their assets than before, reflected by the increase in the asset turnover ratio over the years.

Cash Generation

{kind=link}

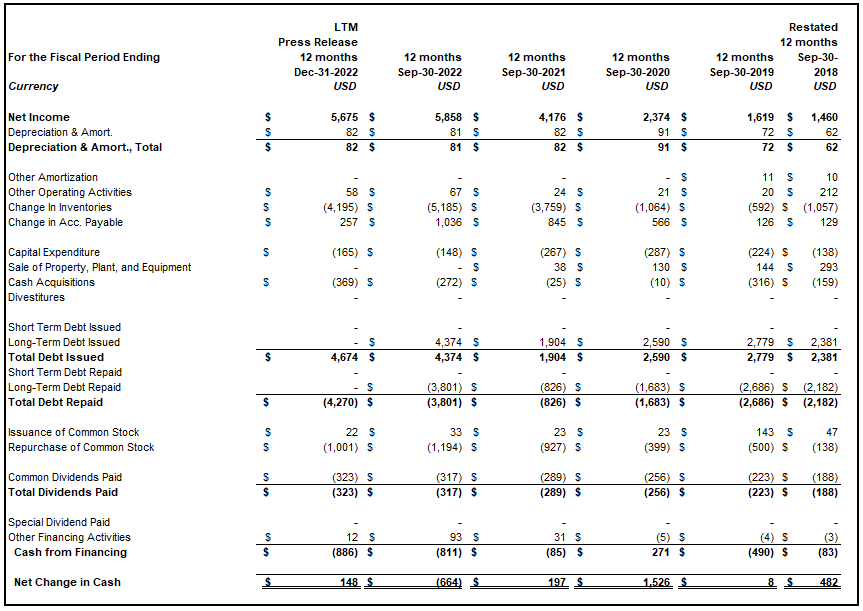

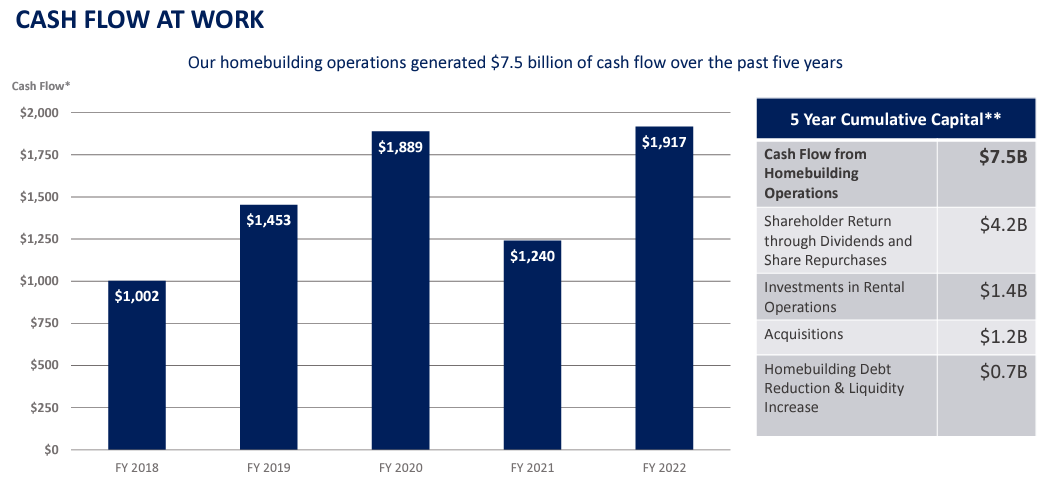

As you can see DHI have done an excellent job of creating value for shareholders by continually increasing their dividend, and repaying their debt. Obviously they are issuing debt at the same time so it is a net-negative, but they can easily afford to do so. And need to. The graph below from their Q1 2023 investor presentation depicts how impressive their capital management has been in creating value!

{kind=link}

Cash Flow Generation (Q1 2023 DR Horton Investor Presentation)

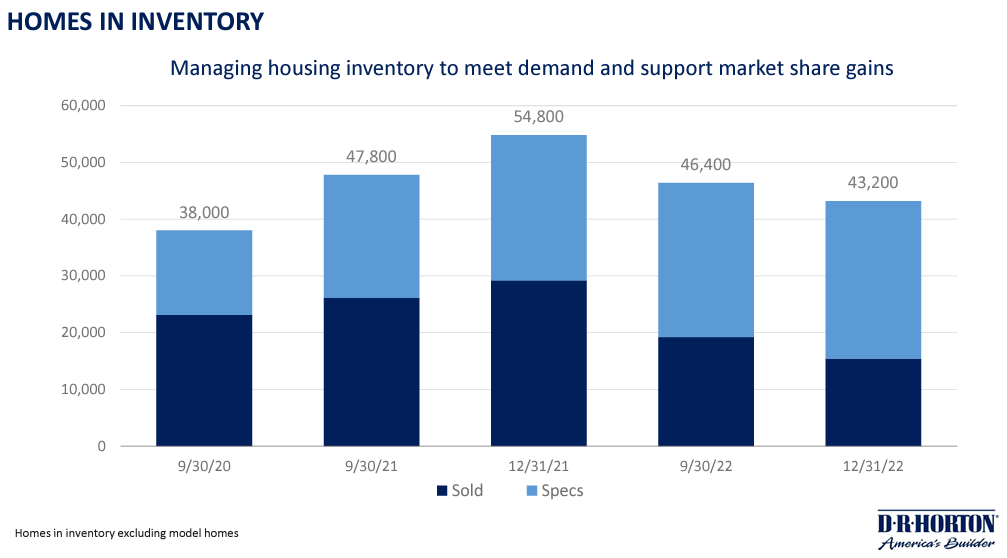

Inventory levels are higher than before when you look at the sold/unsold ratio and this obviously implies that demand is lower than usual. Management has said that they did this on purpose in order to effectively manage their sales mix. Realistically they will need to completely re-strategize as they won't be able to sell houses as easily, their management team is experienced enough, so this shouldn't be an issue.

{kind=link}

Homes In Inventory (D.R. Horton Investor Presentation (Q1 2023)

{kind=link}

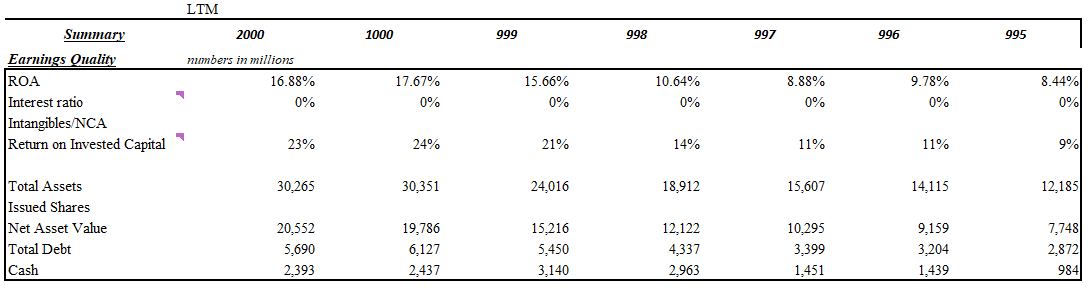

Earnings Quality (Capital IQ)

Once again, we see that this business is a cash cow that has managed to outdo themselves year after year, realistically with the growth they've seen in top line the amount of debt they've taken in is very reasonable and goes to show how much of their growth has been natural.

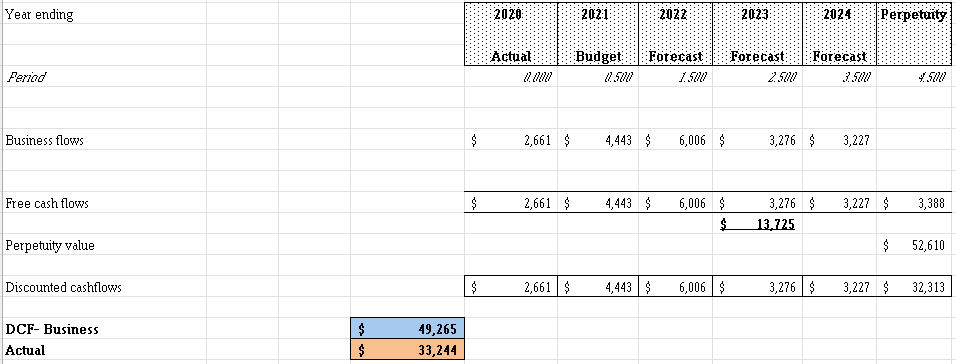

Valuation - Discounted Cash Flow

Lastly, I decided to use the DCF to see what the outcome would be, I used the following inputs:

A beta of 1.3

Rf of 4.5%

MR of 15% (personal preference)

Additional 4% to factor in risk

which gave me a WACC of 11.4%

I also assumed a growth in perpetuity of 5% when calculating the perpetuity value.

{kind=link}

As you can see the final results show a clear margin of safety of 32.5% ( 1 - 33,244/49,269) according to my calculations! This makes perfect sense to me as we are looking at a company with a market cap of $33.2 billion and $5.6 billion in earnings at time of writing, a ratio of market cap/earnings this high is unusual and I believe "Mr. Market" is being very generous at the moment.

The market has overvalued the influence of macroeconomic pressures on the company's potential performance causing the company to be undervalued. D.R. Horton's strong management and cash generation will enable them to handle rising interest rates and maintain profitability through superior pricing strategy and a changed sales mix, even if housing demand drops. Even at a $49.2 billion market cap the company's Greenwald Ratio is equal to 11.3%, this is still outstanding. I believe the company is a buy at that point, obviously any Greenwald Ratio lower than this makes the investment riskier and so I most likely wouldn't add to my position at a sub 10% Greenwald Ratio.

Therefore, at a $49,265 billion market cap (the DCF output), the share price would be $143, compared to the actual share price of $96.81 at the time of this writing. Taking any position in the stock between $96.81 and $143 will be a safe investment, in my opinion.

Risks & Challenges to my thesis

It is entirely possible I could have made some assumptions that are inaccurate or I am possibly not taking into account how severe the macroeconomic factors could be to DHI's future performance.

Homes could become too expensive (more so than I predict) and it would lead to a much larger drop in revenues than anticipated, this would then have a domino effect causing DHI to have too many houses in inventory and if these houses are part of their Emerald range lets say (these are their expensive high-end homes) they might stay unsold for a long time.

Additionally, if the prices of raw materials fall, take lumber for instance, it can increase profits for the homebuilder, as long as the decrease in the cost of materials outweighs any decrease in demand for housing construction. For example, if a homebuilder was previously purchasing lumber at a price of $500 per unit, and the price decreases to $450 per unit, the homebuilder's cost of materials will decrease, leading to higher profit margins. However, if the decrease in the cost of materials is not enough to offset other decreases in revenue, such as a decrease in demand for housing construction, overall profits may still decline. Add to this the increased costs of servicing debt and DHI's margins might sink more than I am expecting.

Final Thoughts

In summary I believe that DHI is well equipped to handle the oncoming headwinds and if we are looking at a 5-10 year timeframe they will do very well. The company benefits from a large market share, prudent management and definitely have a lot of bargaining power, which will allow them to manage costs during inflationary periods.

The company's track record speaks for itself, they have a clear focus on shareholder value and building homes in the most profitable/sustainable way. I believe there is a clear Margin of Safety, 32.5% as shown earlier by the DCF calculations and my NAV calculations illustrate that. In my opinion, DHI is a stellar company to own! And if correct, they should deliver outsized returns to any investor over 5-10 years. By no means will it be easy for the company to continue to do well, but I have faith in them as shown by their past performance.

As Warren Buffett says: "We don't try to forecast what the economy is going to do. The economy is going to do what it's going to do, and you can't do anything about it."

For further details see:

D.R. Horton: Well Equipped Market Leader, Positioned To Overcome Macroeconomic Pressures