VLKPF - Daimler Truck Ahead Of Nikola After Q3

Summary

- In this article, I want to share an update on Daimler Truck Holding.

- The company should be seen as a major North-American player.

- I compare its BEV business to Nikola to show how it is ahead of its competitor.

Introduction

If you are interested in seeing a game where the runner-up is trying to catch the industry leaders, then Daimler Truck Holding ([[DTRUY]], [[DTGHF]]) is a company you may want to follow. In this article, I would like to give an update after the company released its Q3 earnings report and compare it to Nikola ( NKLA ) as far as electric truck sales are concerned.

Summary of previous coverage

At the beginning of the summer, I published a few articles covering the three spin-offs that took place in the European truck manufacturing industry that saw two other players come around alongside Daimler Truck: Traton ( TRATF ) that was spun off from Volkswagen ( VWAGY ) and Iveco Group ( IVCGF ), that spun off from CNH Industrial (CNHI). I will leave at the end of this article the links to the articles where I shared my initial coverage of these stocks, which I think is still updated. My research aimed at finding out and assessing if and how these spin-offs are unlocking value and to what extent.

One key point: the industry has traditionally been a low margin one. Because of this I think we will see some further M&As that will lead to more consolidation. When margins are low, volumes and synergies are quite important.

In my first article on Daimler Truck , I pointed out how the company is focused on reducing costs and increasing profitability. I also showed how the company has a leading position in North America and by becoming stronger in this market it will have the chance to reach double digit margins. In addition, the company sees weak results in the bus segment, both because of the pandemic and because of very low margins that need to be bumped up a bit.

I then published an update where I compared Daimler Truck to Traton and Iveco after their Q2 results. I showed how Daimler was ahead of its main peers in terms of margins and return on sales and this is why I wanted to monitor the company more closely to see if it would have been able to catch up with industry leaders Paccar ( PCAR ) and Volvo ( VOLAF ).

In this article I would like to go over Daimler Truck results paying also particular attention regarding the developments of the zero-emission truck business (electric and hydrogen), comparing it to Nikola, which, though it may be a much-discussed company, is, in any case, a player that could have a role in the electrification of trucks.

Q3 Results

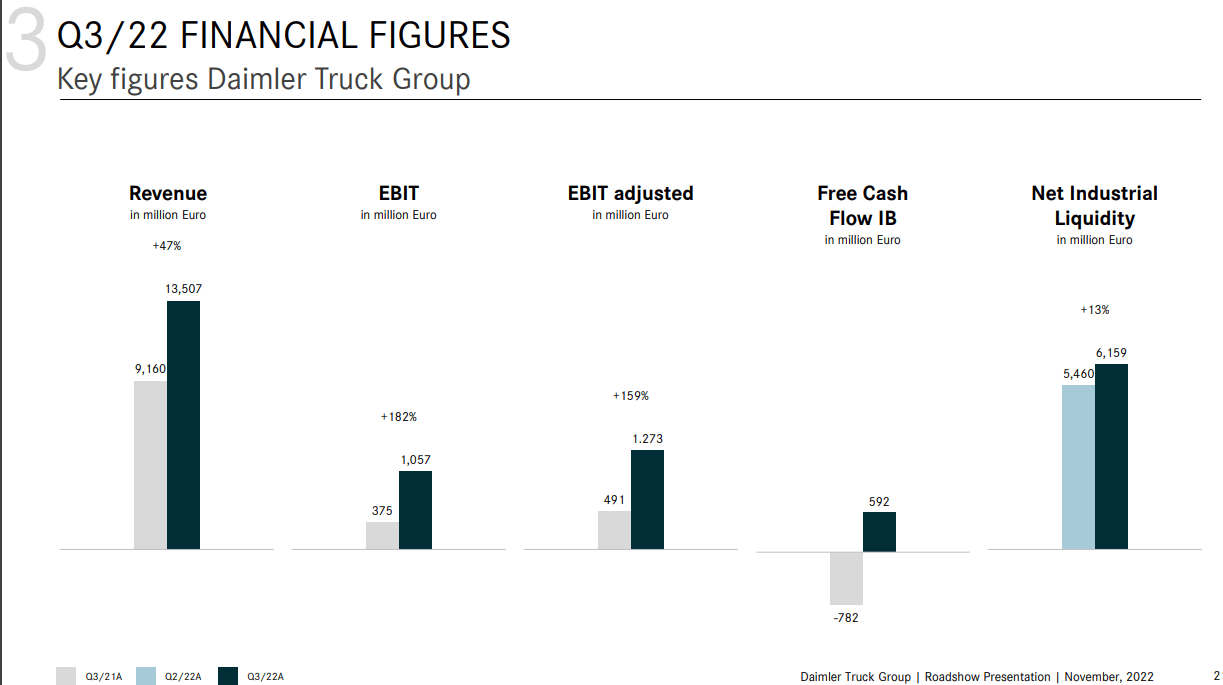

As we can see from the key financial figures published by Daimler Truck, the company achieved record-breaking results:

- revenue of €13.5 billion, up 47% YoY

- Adjusted EBIT with more than €1.2 billion, up 159% YoY

- Free cash flow of the industrial business (IB) was strong and came in at €592 million versus the € -782 a year ago.

- Looking at the balance sheet, we see that net industrial liquidity was €6.2 billion at the end of Q3.

{kind=link}

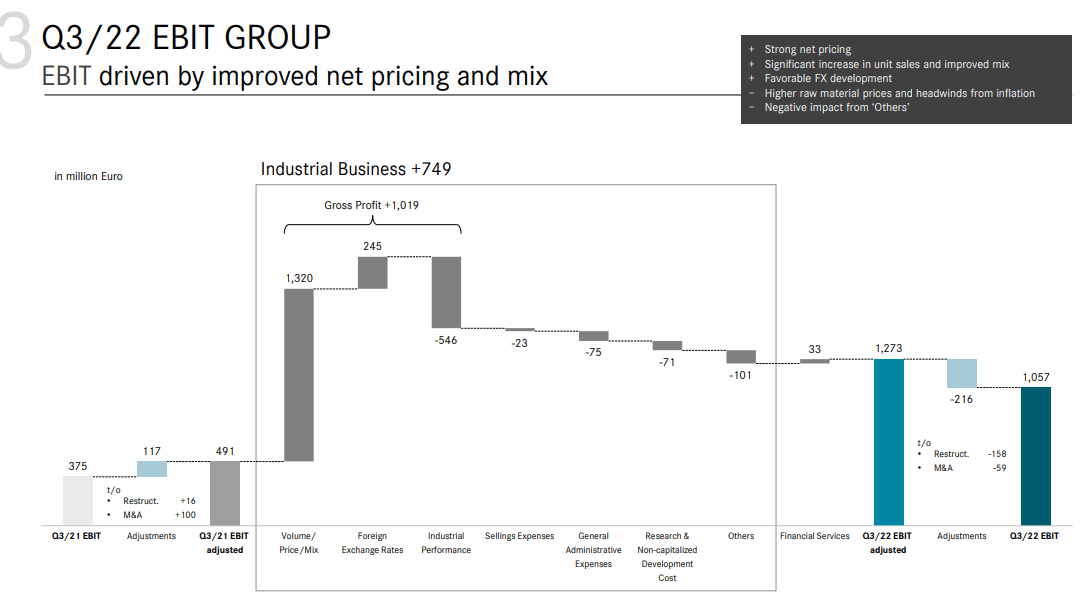

We know that for the automotive and truck manufacturing industry, EBIT is more important than EBITDA since depreciation and amortization have a big impact on financials and can vary significantly from one quarter to the other.

So, let's look at the EBIT breakdown to understand where the strong performance came from.

{kind=link}

The answer is quite clear: pricing power. This is supported by high-demand and the leading role the company has in key high-margin markets, as we will see in a moment.

Let's take a look at the geographic breakdown because I want to spend a few words about something that I think is being overlooked when considering Daimler Truck.

{kind=link}

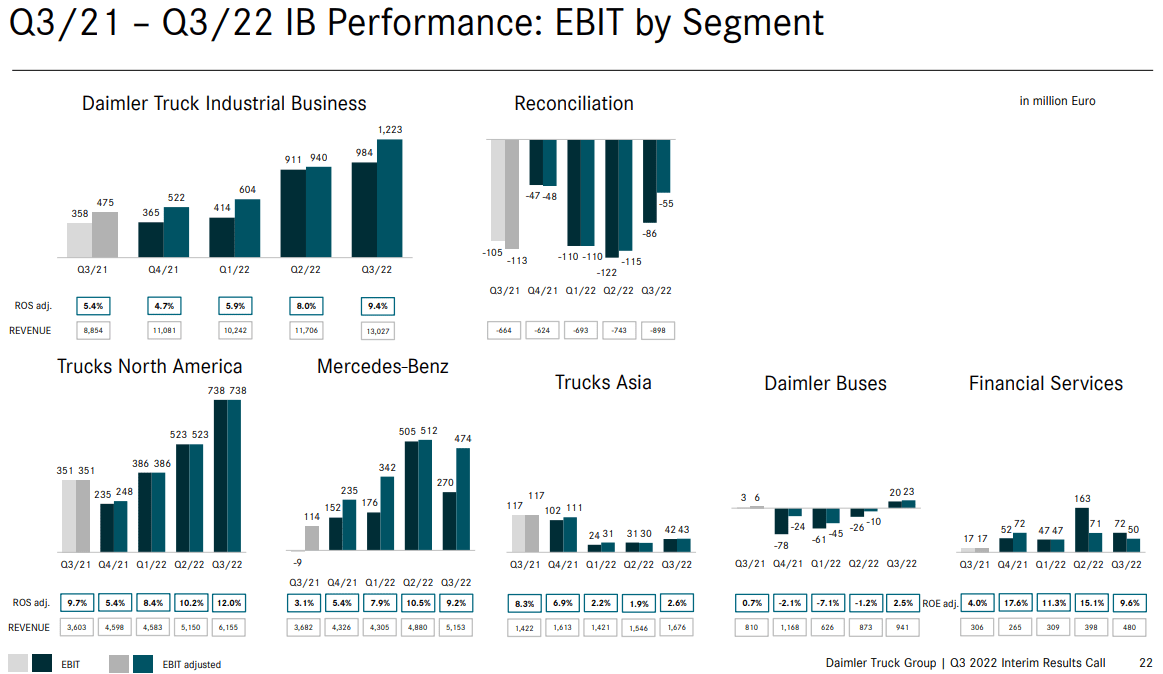

In the slide above, the company shows the EBIT by segment, pointing out the performance over the past five quarters so that we can compare this Q3 to the one of the prior year. The growth shown can also be understood as the harvest after sowing, as the company now begins to deliver a larger number of vehicles as supply chain constraints are easing up. In addition, the EBIT growth is also due to correct pricing that is now offsetting inflation.

We can see that Trucks North America, Mercedes-Benz (Europe) and Daimler Buses are all growing, pushing the whole industrial business EBIT upwards. Asia is performing poorly, but we all know that China has just started to change a bit its zero-Covid policy which slowed down the whole economy.

But what I really want to highlight is that, though Daimler Truck is conceived as a European company, more than half of its EBIT comes from North America.

The importance of North America

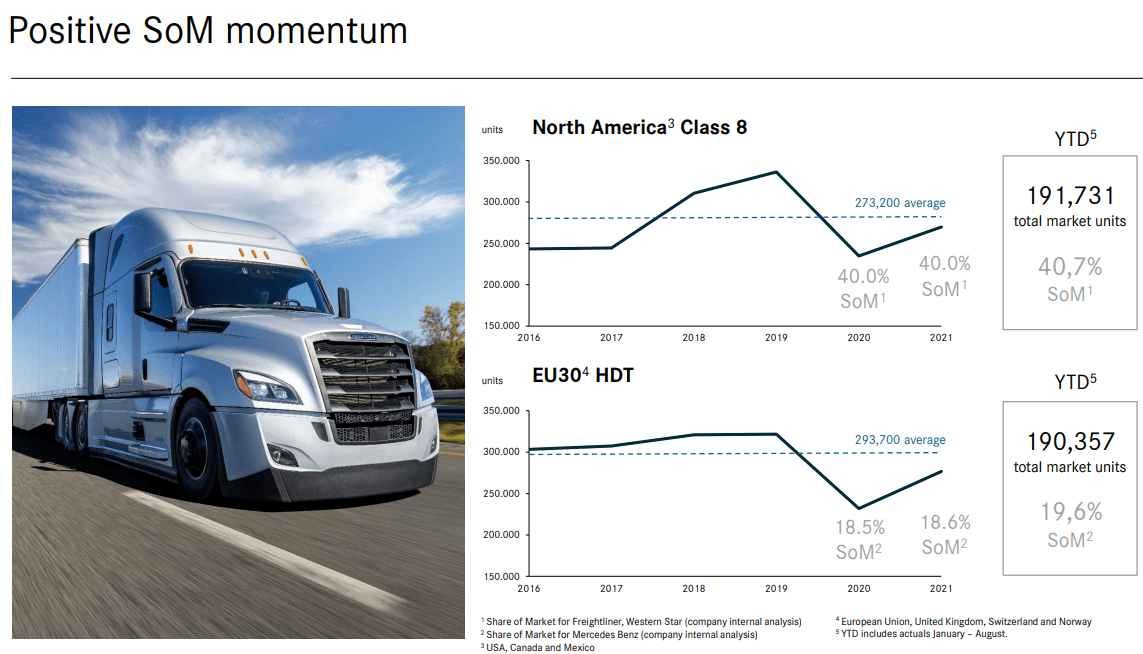

Daimler Truck division in North America has around 40% of the class 8 market share. As we can see from the slide below, the share of market in North America is much bigger than the one Mercedes-Benz has in Europe (just shy of 20%), even though the two markets have very similar volumes (190k units each from January to August).

{kind=link}

This shows how Daimler Truck is more reliant on North America and that it needs to be considered as such, rather than just being a European manufacturer that exports to North America. In fact, Daimler owns brands such as Freightliner and Western Star that are highly appreciated in the U.S.

In addition, the return on sales in North America is already a double-digit one: 12% for the quarter versus the 9.7% reached in Q3 2021. Mercedes-Benz in Europe improved more, considering that last year it had a return on sales of 3.1% versus the 9.2% achieved this year. However, it is still lagging behind the strong performance in North America.

This is why I believe it is important to look at some data about the U.S. transportation industry and its future outlook.

I have already shared some of these in a recent article on Paccar but, as I tried to explain, I believe these data are even more important for Daimler. Let me quote a part of what I wrote:

Although the U.S. railroad infrastructure is about 92,282 miles long, the national highway system together with interstates roads are more than four times larger with 440,480 miles. In addition, about 75% of public sector funding goes to highways and streets which creates a tailwind for trucks.

{kind=link}

According to the U.S. Department of Transportation , trucking contributed the largest amount of all the freight modes to GDP with $359.5 billion.

Another reason why I am bullish on trucking is because trucks carry the largest shares by value, tons and ton-miles for shipments moved less than 1,000 miles, while rail becomes dominant in the range between 1,000 and 2,000 miles. Since 82.9% of the value of goods moved in the U.S. travel a distance under 1,000 miles, we clearly see that the nation can't go without trucking.

U.S. Department of Transportation

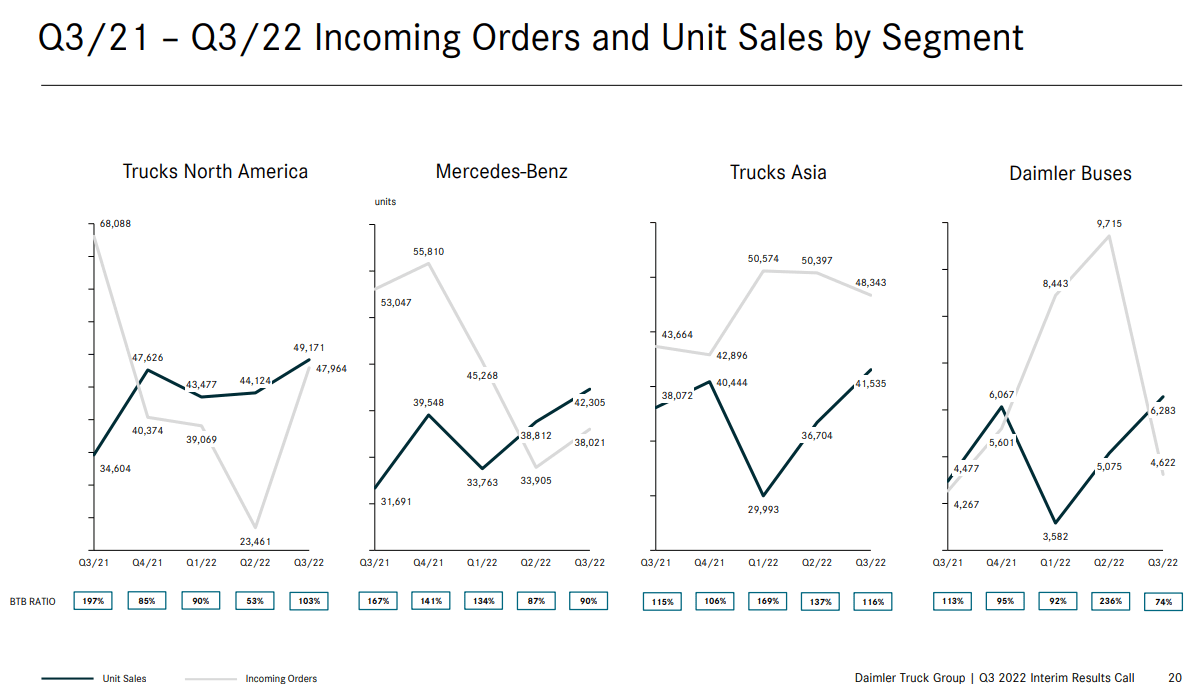

Allow me now to show one more slide from Daimler Truck's investor presentation. Here we see how incoming orders and unit sales by segment are performing over the past five quarters. While many are forecasting a recession in the U.S., it seems like North America already saw a slow-down in incoming orders as it is now picking up speed once again.

{kind=link}

Recession or not, this industry is somewhat set to offset some of its usual cyclicality due to the tailwinds I have outlined and the fact that pent-up demand is still strong. As Jochen Goetz, Daimler Truck's CFO, explained during the last earnings call :

we are managing the order book very carefully. In North America, we opened the order book late and are very pleased with the order intake so far. September orders are a further testimony that there remains a tremendous level of pent-up demand.

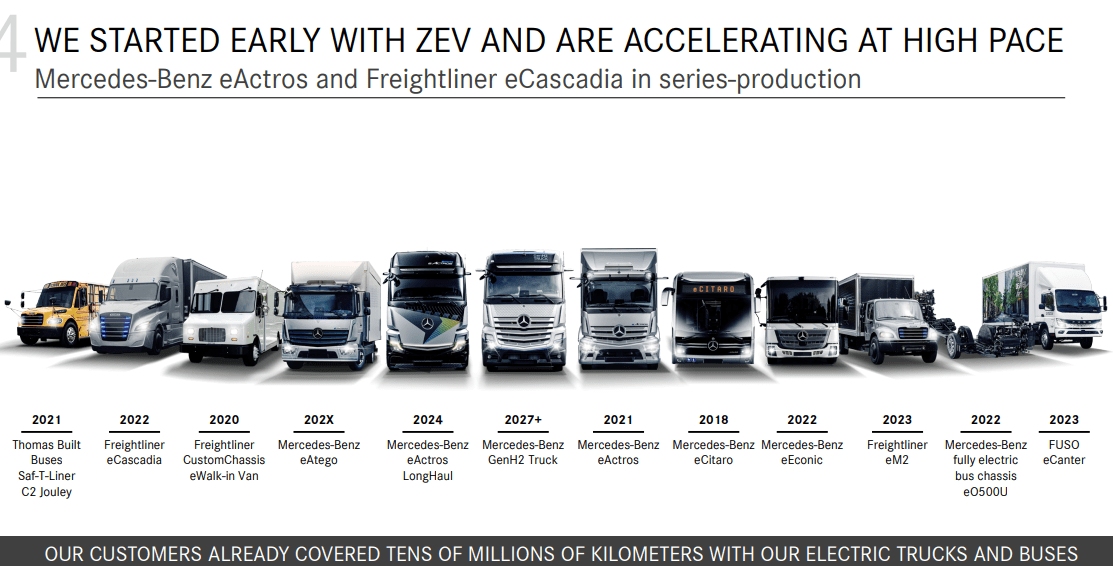

Now, let's recall to our mind the graph where I showed the percentage of goods shipped in the U.S. by distance miles traveled. It is particularly interesting because it shows that most of the goods shipped move less than 1,000 miles and this enables electric trucks to take care of most of these volumes. Here, Daimler Truck is particularly strong, since it was one of the first players to start producing electric trucks and buses, as we can see below.

{kind=link}

Mr. Goetz disclosed that:

From January until September this year, we sold 624 battery-electric trucks and buses. In the same period last year, we sold 308 zero-emission units. Year-to-date, orders for zero-emission vehicle increased to 1,705 units, this year from 497 units in 2021. We are continuously expanding our portfolio of battery-electric trucks.

A comparison with Nikola

Let's take a look at Nikola ( NKLA ), a company that, in order to be fair with the industry, I covered back in June rating it with a sell (the stock is down 60% since then), warning that it was still trading at very high multiples and that shareholders would see a big impact on the share price coming from share dilution.

In the third quarter, the company managed to produce 75 Nikola Tre BEVs and to deliver 63 of them to its network of dealers. It was the second quarter of production. This generated $24.2 million in revenues that were not enough to lead the company to profitability, as its loss per share was $0.54. On the fuel-cell side, the company is still in test mode, though it reported that in the quarter it completed 6 beta trucks and that Tre FCEV are being tested with Walmart.

True, the company received a big order of 100 Tre BEV from Zeem Solutions, however these numbers show that Nikola is still behind Daimler Truck by at least two years, not counting the significant lack of know-how for the mechanics of trucks (i.e. chassis) that the other manufacturers have.

In fact, the company said won't be able to deliver the 300 trucks it planned to do at the beginning of the year.

So far, the cost of revenues is more than double the sales revenue. This means that the cost per unit is much higher than the average selling price, which doesn't bode well for the future. The company gross profit was another -$30 million during the quarter, for a total of -$59 million in the first nine months of the year. When we look at the bottom line, net loss for the quarter was $236 million, a slight improved YoY (-$268 million last year). However, YtD, the company has lost more money than last year: $562 million vs. $531 million. Stock-based compensation has a big impact: this quarter it amounts to $102 million versus $49 million last year in the prior quarter. It seems like the company needs this tool to reward employees because it needs to preserve its cash. In fact cash and cash equivalents are once again down from $497 million at the end of 2021 to $316 million at the end of September 2022. The company burns roughly $60 million per quarter.

We have also to consider that during the earnings call, Kim Brady, CFO of Nikola, disclosed that

the Q4 gross margin will deteriorate from Q3 once we start consolidating Romeo Power into our financials. When we announced the acquisition on August 1, we summarized the potential long-term benefits from the merger to be approximately 30% cost reduction in non-sale related battery pack cost by the end of 2023. However, our BOM cost for the battery pack enclosures will increase temporarily for the next five quarters as Romeo Power was subsidizing Nikola's battery packs by approximately $110,000 per truck.

This is not good news for a company whose financials are at risk.

Now, though I am bearish on the company and I think that it may actually risk bankruptcy, I don't want to pick on Nikola. I do think that the company is financially walking on a razor's edge. However, the strong demand for BEV trucks and the fact that its competitors can't fulfill it could actually help it gain a big enough market share to cope and survive. However, I see it as a very risky pick that, as such, could actually be the best performer in the stock market if things change around. However, I am not willing to invest in this kind of risky company.

Conclusion

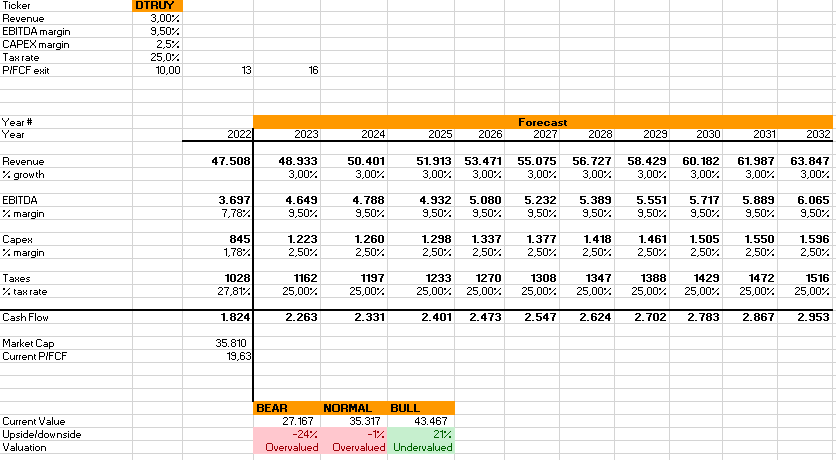

I think it is time to update my future cash flow forecasting model. Given recession fears, I brought down from 4% to 3% the average revenue growth over the next decade. I also chose to use two different price/FCF exit multiples, a 13 and a 16 for the normal and the bull case scenario instead of a 14 and an 18.

{kind=link}

The result is that we are close to fair valuation. However, I think this forecast doesn't take into account that Daimler Truck seems to be going in the right direction and is turning more and more profitable while being one of the technological leaders in the electrification of trucks. At the moment, I still want to stick to a hold while I am long Volvo Group, as some readers may already know. However, Daimler Truck could already be in buying territory for some investors who are willing to bet on this turnaround in the making that is becoming more and more promising.

On the other hand, I can't upgrade Nikola's rating to a hold, but I have to stick to a sell, even though the price is plummeting.

For further details see:

Daimler Truck Ahead Of Nikola After Q3