DTGHF - Daimler Truck: Supportive Capital Market Day Buy Reiterated

2023-07-12 01:37:08 ET

Summary

- Daimler upgraded its 2023 guidance following strong Q2 sales, expecting to increase turnover by 10-14% to €56-58 billion. It also declared a new €2 billion share buyback program.

- The company is on track to reduce R&D costs by 15% by 2025 while maintaining a dividend policy of at least 40% on the payout.

- A better margin in a slowdown cycle means a better valuation (or a lower discount vs. peers). Our buy rating is then confirmed.

In the Seeking Alpha community, we were the first to initiate coverage of Daimler Truck ([[DTRUY]], [[DTGHF]]) following the Mercedes-Benz spin-off . Since our publication called ' Strong Performances Continue ' released almost one year ago, the company stock price is up by more than 20%. Favorable MACRO trends supported our buy investment thesis: 1) EV adoptions with autonomous driving solutions and 2) continuous higher food requirements to meet growing population demand. This was also based on our research on Corteva and Iveco Group N.V (IVCGF). On the MICRO level, our upside was backed by a compelling valuation vs. competitors such as Volvo (and Paccar) and a deleveraging story with a good plan on the company's capital allocation priority (1. lower debt evolution, 2. accretive acquisitions, 3. dividend payment, and 4. buyback).

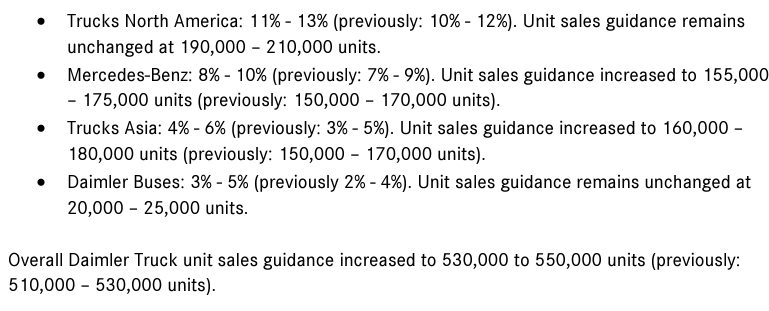

Unlike peers like Iveco , the company didn't raise its guidance in Q1 due to logistics uncertainty and supply chain issues. However, the company announced an increase in its 2023 full-year outlook and declared a new share buyback program at €2 billion. In light of strong second-quarter sales, thanks to supply chain stabilization, strength in key markets, robust pricing, and strong aftermarket business performance, Daimler upgraded its 2023 numbers. In detail, the group expects to increase turnover by +10/14% to €56-58 billion (from previous estimates at €55-57 billion). This is supported by volume growth of +2/6% to 530-550,000 (from the last forecast at 510-530,000 units). Wall Street was pricing top-line sales of €56.1 billion. In addition, the industrial activity free cash flow is expected to increase significantly compared to a previous estimate of " slight improvement ." Given the sequentially stable supply chain and a solid operating environment, we are not surprised to see an FCF yield of 9% vs previous estimates at 8%. The ROS was raised in all GEO areas, especially in North America. Industrial companies were recently penalized for economic slowdown following the latest MACRO data with Daimler's recent update; this leads us to think that even on these fronts, there is no significant slowdown to justify potential stock underperformance. We also underline how Iveco is positively reacting to Daimler's numbers and is up by an additional 2% at the stock price level.

{kind=link}

Today, the company also updated the investor community with a Capital Market Day. In the past, Daimler management already indicated a cost-saving target of 15% by 2023. This target was shifted to Fiscal Year 2025 and confirmed (once again) today. The company cost optimization was related to lower fixed cost and R&D reductions, excluding currency development, excess inflation, and autonomous driving R&D. On a negative note, we did not like that there were no split improvements on a divisional level. In detail, we were interested to see Mercedes-Benz's standalone competitiveness. As a reminder, one of the key investor concerns is related to Daimler Truck's quarterly earnings variability. Per our expectations, management was not very proactive in this area, which could be a tailwind for the stock. However, what is also important to report is the fact that Daimler:

- Increased adj ROS to 8.5-10%, confirming its target of 10% by 2025

- Announced a more stable dividend per share expectation not related to the business cycle with a payout ratio in the 40%/60% range

- Related to the buyback announcement, Daimler management indicated an estimated €4-6 billion net cash to run the business in the past. Given the strong company's liquidity, we are not surprised to see the share repurchase disclosure. Here at the Lab, we would have preferred a special dividend

{kind=link}

In Q2, Daimler's worldwide unit sales increased by 9.0% compared to last year, and the company sold 131,888 units. Looking beyond the 2025 financial targets, after a profitable year in 2022, we are confident that the company is on track for 2025. Consensus is pricing a market downturn in 2024; however, Daimler's management introduces new targets for the medium term. To quote the company CMD report :

Looking beyond 2025, we see multiple growth opportunities in our industry, and we are fully equipped to exploit these opportunities. This should translate into a 40-60% revenue increase between 2025 and 2030 and an above 12% adjusted return on sales for the Industrial Business in sunny conditions ".

We believe that a Wall Street concern is Daimler's ability to consistently deliver a double-digit core EBIT margin, such as Paccar and Volvo. This could present a meaningful upside if Daimler reaches a credible path to a double-digit EBIT margin outside a supportive MACRO scenario. In our scenario, Daimler Truck FCF is estimated at €2.2 billion for 2023. This is based on a forecast industrial margin of 8.8% (5.8% in 2019), while the company targets a 10% plus for 2025. Thanks to a positive FCF evaluation, Daimler is on track to deleverage. Our net debt/EBITDA estimated is at 2x at 2023 end with a total net debt of €12.4 billion.

Here at the Lab, we also like the disclosure of a new project on a hydrogen combustion engine. Further partnerships and M&A activity could allow the company to optimize CAPEX investment in autonomous driving and electrification. For this reason, the company is on track to reduce R&D costs by 15% on a 2019 basis while maintaining a dividend policy of at least 40% on the payout.

Conclusion and Valuation

As a result of Daimler CMD, our internal team sees upside potential for an improved market outlook. Wall Street analysts were currently pricing Daimler with an 8% EBIT margin, which is not the case with the new guidance. In addition, our FCF yield estimates reached >9% vs a dividend yield payment of 4%, so the company FCF well covered the dividend payments. Daimler track is trading at 2.5x EV/EBITDA on a twelve-month horizon. With a positive FCF trajectory and a solid balance sheet, this is not justified. Given Volvo's strong track record, a 20% discount on a P/E basis is justified (vs a current discount of 40%). Therefore, we continue to value Daimler Truck with a buy price target of €38 per share. In addition, on a P/E basis, we believe that Daimler should trade at a premium price compared to Iveco (8.65x vs 9.36x), given the company's historical execution, better margin profile, and GEO diversification. Downside risks include management execution that may continue to lag competitors, additional supply chain constraints, economic slowdown with MACRO deterioration, and a lower truck cycle in 2024. In addition, failure in R&D development in fuel cells and hydrogen technology.

For further details see:

Daimler Truck: Supportive Capital Market Day, Buy Reiterated