DTGHF - Daimler Trucks: One Of The Best Trucking Manufacturers On Earth I Say 'BUY'

2023-10-25 02:28:10 ET

Summary

- Daimler Trucking is a manufacturer of one of the best trucks on the planet, with a strong product lineup.

- The company's profitability has room for improvement, but it has seen positive trends and increased guidance.

- Daimler Trucking has a market-leading position in the trucking industry and has potential for future growth as the demand for zero-emission vehicles increases.

Dear readers/followers,

In this article, I'll be taking a look at Daimler Trucking ( OTCPK:DTRUY ) for the first time. I haven't covered this business before, even though I've covered Daimler for a few years.

This specific company is, as I see it, the manufacturer of one of the best trucks on the planet. The closest competitor would be Traton ( OTCPK:TRATY ) - and I've invested small positions in both of these businesses at levels I viewed as undervaluation.

{kind=link}

Let's look at the company what we can expect from the business here, and why I view the company as investable at the right price.

Daimler Trucking - I like trucking investments at the right price

So, Daimler Trucking is a company that has been around for a long time, but in its current form since around 2019, as part of Daimler AG. The company was announced as an official spin-off in February 2021. This was then approved by shareholders in early October two years ago, and incorporated to manage assets by Daimler Truck AG. Daimler retained 35% ownership of the company, with 5% going to its pension trust.

The new company was made public in December of 2021, meaning the company is now less than 2 years old.

The company has one of the most appealing line-ups of products. Daimler Trucking's brands include things like:

- Mercedes Benz , including light, medium, and heavy-duty trucks and buses (not vans, this remains in Benz)

- Freightliner trucks and vans

- Western Star heavy trucks

- Fuso trucks and buses

- Thomas-Built Schoolbuses

- Setra Buses

- BharatBenz , an Indian truck brand

- Detroit Diesel , a medium/heavy powertrain business

- Truckstore , for its used vehicles, financing, leasing, rental warranty, contracts, and buybacks

- Fleetboard , a telematics/connectivity business

- Rizon , EV medium-duty trucks

The company employs around 100k people across the world and has global production plants and research centers. This includes sites in Japan, Turkey, South Africa, China, India, Germany, India, USA, South Africa, Colombia, Mexico and many other locations.

The company, as of right now, does not have the best fundamentals around. Where we can highlight positives is in the company's margin developments and where it seems to be going. But currently, Daimler Truck Holding's business model isn't the best around.

I say this because on a revenue/net income basis, the company manages a $5.2 profit from a $100 revenue - with an operating margin of around 6.7%. Not the greatest around, and in the mid-50th percentile compared to other manufacturers of trucks, heavy-duty, and construction machinery, which is the comparable sector here.

The company's native listing is DTG, on the German stock market - and that would also be the listing that I would, and am investing in.

The fundamental case for investing in the transport sector is an easy one, as I see it. Transport remains the backbone of a working, modern society. Logistics is a core business, and we'll see a growing global transport volume that seems to continue to grow at a rate of around 1.5-2.5% per year, with road transportation being the primary sector here that's relevant.

New entrants in this industry are not likely - at least not bigger ones. Close customer relationships, high moats and barriers due to the cost of capital, and massive production and manufacturing bases required put new players in a very difficult position.

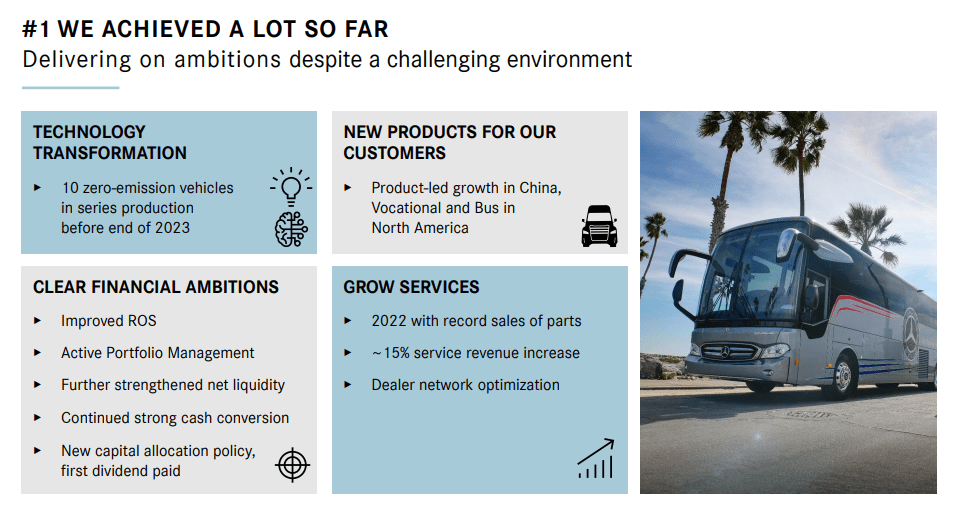

The company claims it's seen impressive trends since listing, and part of this is certainly true.

{kind=link}

However, the company's profitability has not been as hoped yet, with goals to improve not only the top line but the bottom line. EV and Tech transformation is obviously part of this as well.

However, the latest results we have so far are 2Q23 results, and trends so far this year are encouraging despite the overall macro. We're seeing an increased guidance, with a RoS growth of 8.5-10%. This is especially coming from trucking North America, and the Mercedes Benz segment as well as finance services, due to increased interest rates and related income. Buses and Trucks in Asia are expected to grow far less.

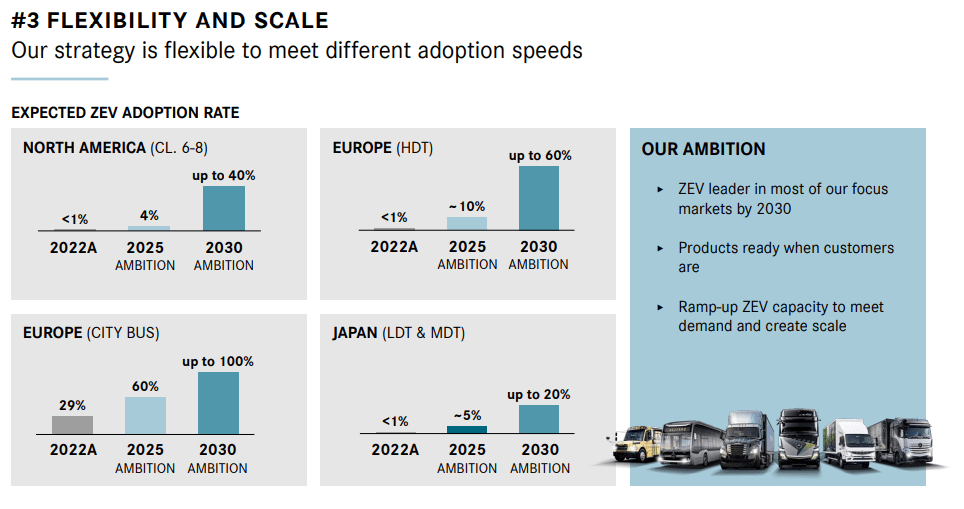

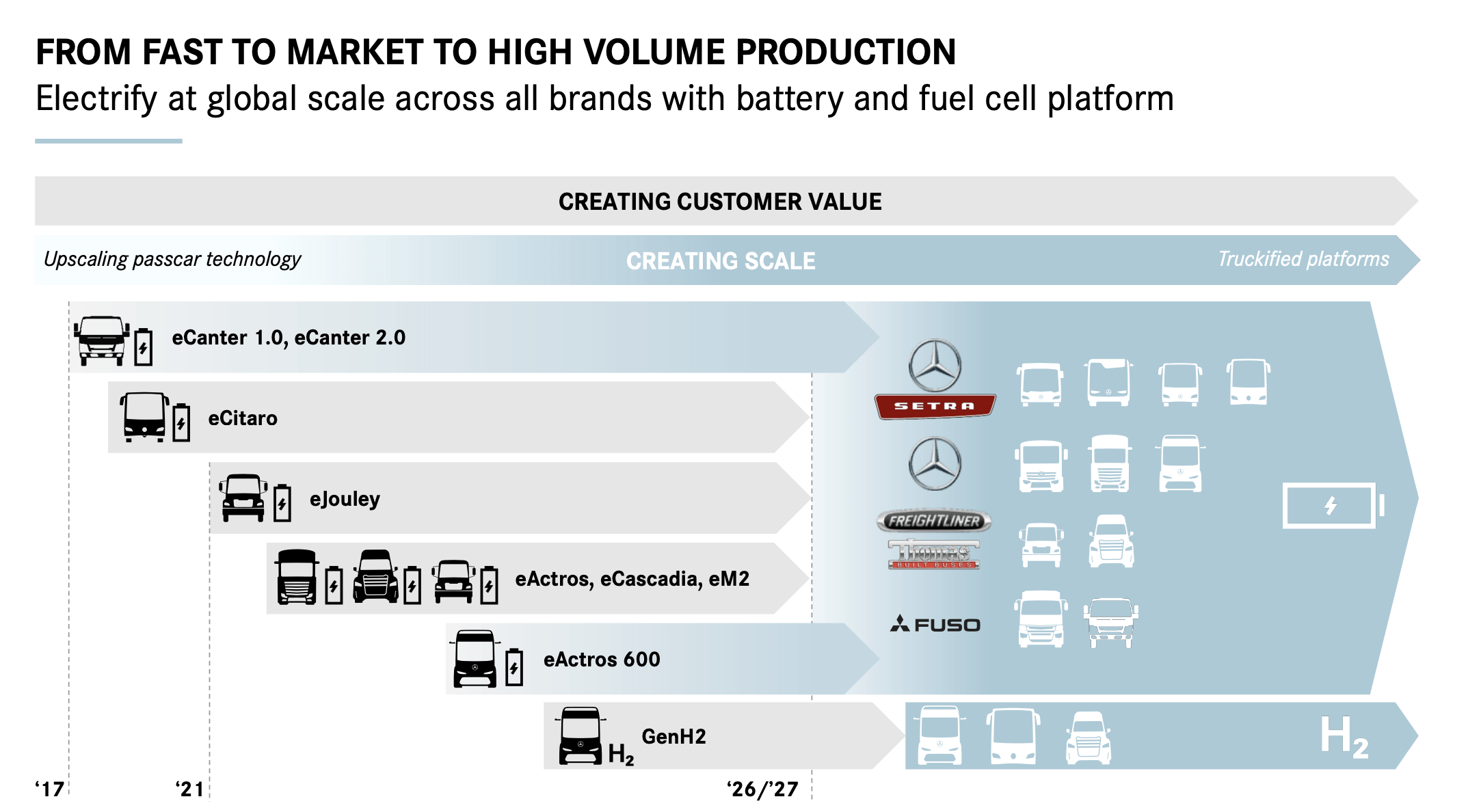

When it comes to Trucks, the heavy-duty trucks segment is where the company earns its biggest margins. That's why the heavy-duty EV sector, with the company's push into eActros, eCitaro, Cascadia, and other products is some of the most important.

At the same time, Daimler confirms that the transformation path remains somewhat uncertain, given the current geopolitical tensions, emissions, infrastructure availability, ramp-up speeds, and investments into these new technologies given the increased cost of capital. Still, the goals are lofty and ambitious.

{kind=link}

Another appeal the company has is that it already has ongoing partnerships with most of the important infrastructure, parts, services, and autonomous companies. Given that it also has its own finance services business, the company is well-prepared for any up, downside, or headwind that could appear here - at least this is how I see it.

The company's sheer scale and market share of a highly attractive segment is a core reason why you'd probably want to consider investing here. Aside from pure EV, the company is also focusing on hydrogen trucks, with the GenH2 truck.

This company, as I see it, has a complete segment/sector coverage in a way that makes any downturn momentary in the larger time period. In a way, I like the fact that the company listed during what turned out to be a very chaotic period because this has prevented the company from really being at any sort of significant premium.

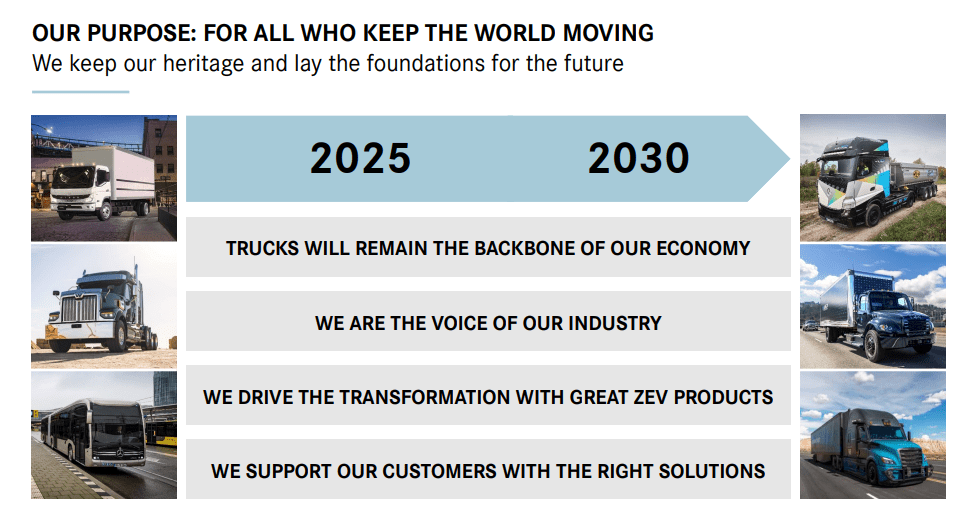

The company's targets are very lofty, not only when it comes to EVs; but also for growth in general.

{kind=link}

The company is currently working on a completely encompassing battery platform, optimized for safety as well as longevity as well as cost. The company's ambition is that this battery pack technology will cover over 80% of the heavy-duty segment. The partnership for cell production has not been announced just yet - but at least it's based in the USA, that much is currently clear.

{kind=link}

However, the continuing expectation is for the cost of ZEV trucks to remain as comparatively high as a diesel vehicle as is the case today. Even with efficiencies and improved production and technology, Daimler expects the combination of eDrive and eComponents as well as the battery pack to result in a significantly more costly product, with a key factor of the cost naturally being the cost of energy, and specifically the "green energy price". Something that's hard to estimate or forecast here.

The company is working to make sure the infrastructure with regard to charging is available. Various solutions from Siemens ( OTCPK:SIEGY ), Engie ( OTCPK:ENGIY ), and Detroit/Power Electronics are being brought to bear.

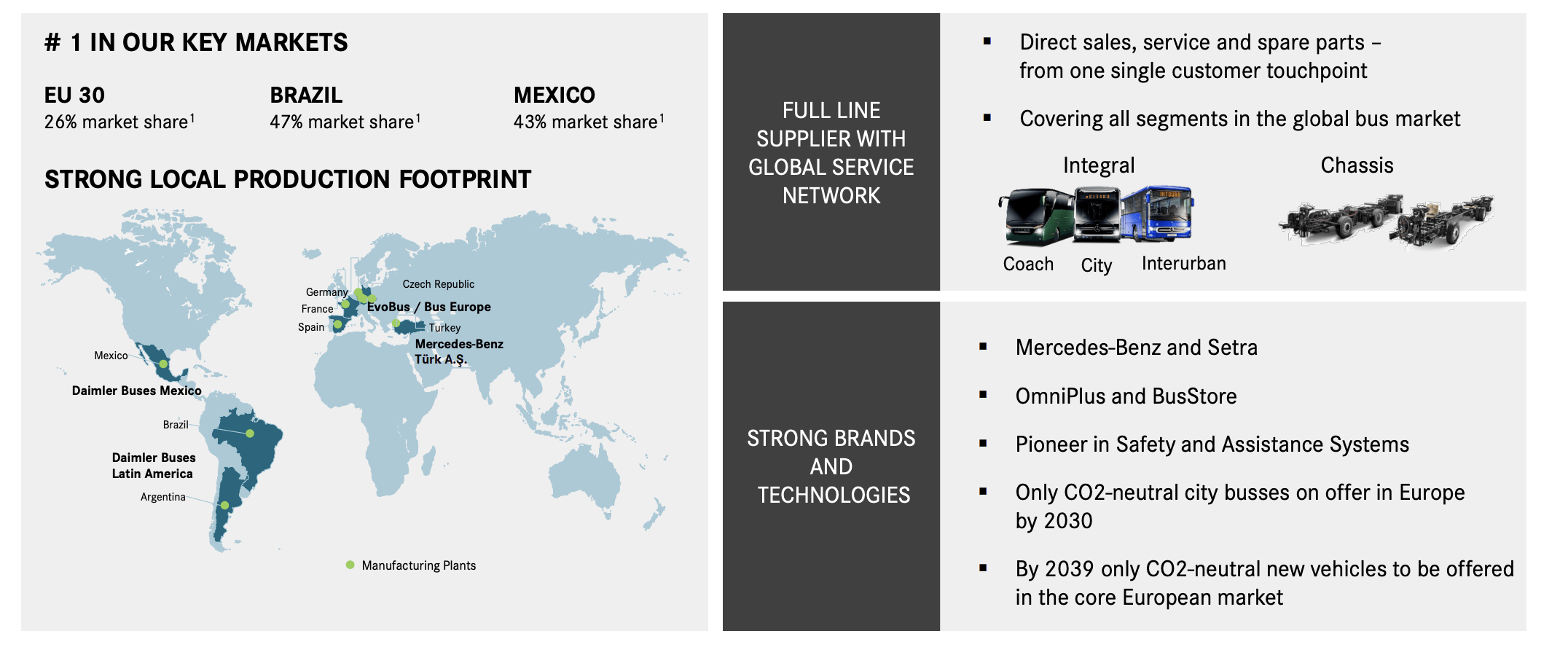

The company is a clear market leader, with a #1 spot in all core markets.

{kind=link}

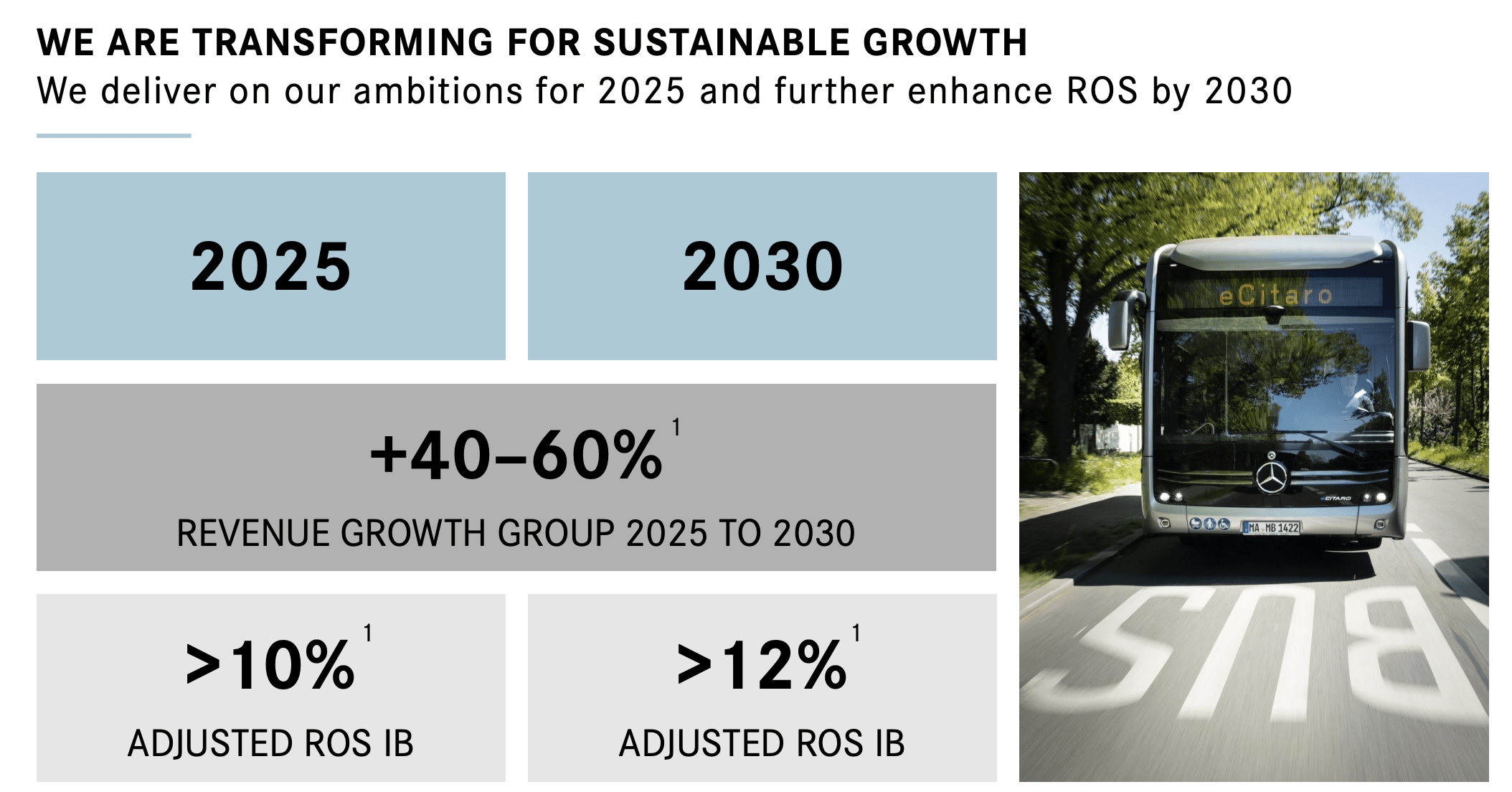

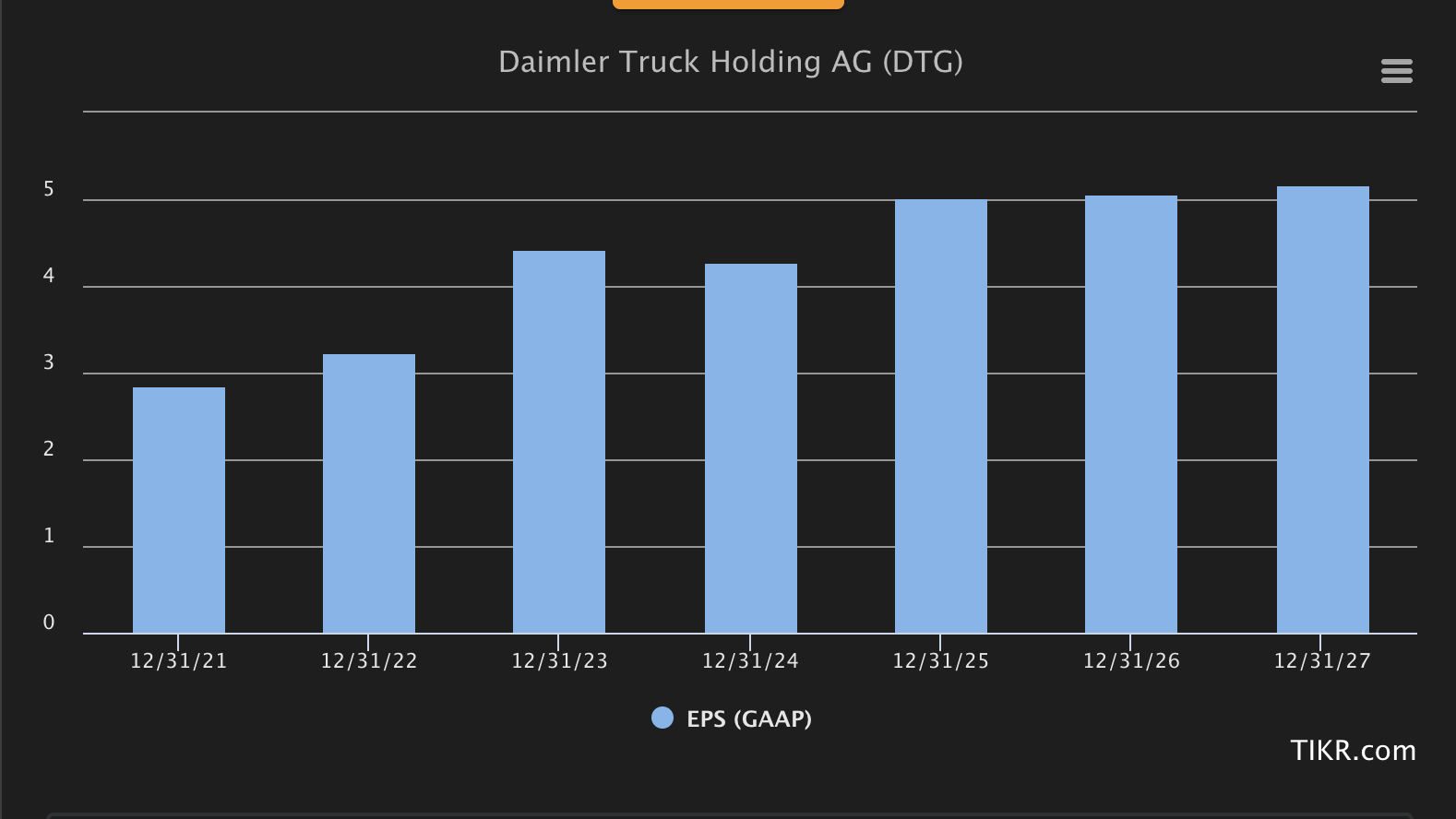

The company is a market-leading business in a crucial sector, and I believe it to be a story of future growth - with current EPS estimated to start on a significant growth trajectory starting in 2023E, but moving upwards towards, and beyond the €5/share mark in 2025E as well as coming years after that.

{kind=link}

Based on this, Daimler Trucks has incredible potential - and it should be treated as a company with a potential for outperformance as ZEV trucking ramps up, as well as the added appeal of the legacy platform of these various products.

Here is where I see the company's valuation and what upside I see.

Daimler Truck Valuation - a lot to like.

A company with a limited history like this can be tricky to value. We have to use peer multiples and more straight-line P/E, P/S, and P/B multiples because the company really doesn't have a history worth speaking of.

What can be said is that the company beat targets in the one year it's been in operation. What also can be said is that the company has almost €25B worth of market cap with a BBB+ credit rating and a yield that's currently at 4.33%. You can throw a rock on the market today and hit a better yield, including better yields in the automotive or construction machinery sector - though heavy-duty products tend to come at a lower yield than your typical car company, which yields far more.

However, the upside I see here I - is also the reason why I actually invested a small stake in the company very recently. I believe that given pressure, the company could certainly go down further in valuation - but I follow the strategy of continually investing, and the fact is that the upside for Daimler is "good".

Let's say you believe Daimler is worth only 9.5x P/E. Fine. I believe the world-leading trucking company should be worth more, but let's go with a 9-10x P/E range.

Even if you use those numbers, and you estimate it at 9.5-9.6x, the company's upside based on current estimates of EPS growth, comes to over 30% annualized RoR per year, or over 78% total RoR. And that's at a 9.6x P/E.

S&P Global analysts have the company at a range starting at a low of €31, which means that the current share price is a full euro lower, and a high of almost €60/share, with an average of €44/share. With 18 analysts following the company, 17 out of 18 consider the company a "BUY" or outperform here".

This is a conviction I can get behind, and both the math and the logic make sense to me here. I believe, even not being the biggest fan of EV investments, that Daimler trucks at a sub-€30/share which is where I bought it, to have a significant upside. It's been cheaper, and I hope it drops down again to those levels so that I can buy more. But for now, I believe in an upside of at least 20-30% per year. A full reversal to something like a 10-12x P/E, which I do not consider to be unlikely, would result in a RoR at current 2025E estimates, of over 120%, or 43% per year. Less likely given the slight premium to peers, but not impossible either.

Because of what I consider to be a very "visible" upside, here is my current thesis for Daimler Truck Holding, and where I would "BUY" it.

Thesis

- This is a market-leading trucking company with, as I see it, the most attractive product portfolio in the world and in its segment. We're talking about market-leading portfolio positions in all segments for the company's products, and an almost-global sort of dominance. Regardless of the future speaks Diesel or ZEV or H2, Daimler will certainly, as I see it, be a part of this future.

- Daimler was listed at a relatively attractive valuation and has not moved up materially from this valuation. The current normalized P/E implies a valuation below 7x, which is cheap for this sort of quality. You're buying the company at below 0.5x to sales, and below 0.75x to revenues, and you're not paying above 1.2x to book value. No matter how you turn this thesis, it comes out as pretty damn attractive at this price.

- The company's yield is not market-leading, but it's certainly good enough for what the company offers. I won't say the company is worth €45-€50/share, as some do, but I put my introductory price target at €38/share, which gives us an upside of over 20% here.

- I consider Daimler trucks to be a "BUY" here.

Remember, I'm all about:

- Buying undervalued - even if that undervaluation is slight and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

- If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

- If the company doesn't go into overvaluation but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

- I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside that is high enough, based on earnings growth or multiple expansion/reversion.

For further details see:

Daimler Trucks: One Of The Best Trucking Manufacturers On Earth, I Say 'BUY'